nwoodman

-

Posts

1,388 -

Joined

-

Last visited

-

Days Won

8

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Great podcast episode recommendation thread

nwoodman replied to Liberty's topic in General Discussion

I really enjoyed William Green's interview with Bob Robotti. Transcription attached. No doubt some confirmation bias on my behalf because what he is arguing is very much where Fairfax and Berkshire are investing today. https://podcasts.apple.com/au/podcast/we-study-billionaires-the-investors-podcast-network/id928933489?i=1000659920472 1. Robotti believes we're entering a new "golden age" for value investing and active management. He argues: "The next decade is going to belong to stockholders... the indexes will not outperform selecting stocks and the ability to identify, do research, select companies that are well positioned and have valuations that are attractive." 2. He sees major structural changes happening, including: - The "evolution of globalization" as manufacturing shifts from China to Southeast Asia and India - North America becoming structurally advantaged in energy-intensive industries - A global energy crisis driving demand for both fossil fuels and renewables 3. On energy, Robotti states: "We're in a very tight supply demand balance in oil today, which I don't think is recognized at all in pricing and yet is an important backdrop." He emphasizes North America's advantage: "North America, because it has an abundance of natural gas that you can't export, has an energy cost that's disconnected from the rest of the world. And that is a persistent long-term advantage." 4. Robotti is particularly enthusiastic about opportunities in unfashionable "old economy" industries. He describes this as: "the metamorphosis of the old economy. Poor industries that have done poorly for a long time are capital deprived, have consolidated, have restructured and maybe the underlying economic environment is different where they've gone from being disadvantaged to potentially very advantaged today." 5. He provides specific examples of old economy sectors with potential, such as chemicals, building products, lumber, and energy services. Robotti highlights companies like LSB Industries in ammonia production, noting how they benefit from low US energy costs and potential new markets in energy transition. 6. On these old economy stocks, Robotti emphasizes: "These are fundamentally, structurally different businesses than they've ever been... And yet valuations are extremely modest because, oh, I know that business, it's a cyclical crappy business. It changed. It isn't what it used to be. It's a butterfly today. It's not a caterpillar." 7. He draws parallels to Warren Buffett's investment in railroads, noting how industries once considered terrible can transform into attractive investments due to changing economic conditions. 8. On indexing, Robotti predicts: "It's the restoration of the fallen stock pickers, active managers. In the next decade, I think have a bright future. And I think I'll be shocked that they don't outperform industries." 9. Robotti credits much of his success to emotional fortitude: "The successes we've had have been the ability to, the behavioural advantage, of being able to tolerate a loss." Podcast: We Study Billionaires - Richer, Wiser, Happier.pdf -

Thomas Cook India and SOTC Travel see significant growth in DomesticTravel demand Impressive stuff. All filings for future reference

-

Definitely more engagement than in the largest shareholder go figure. Just putting it out there but can you imagine the multiples for a US based company that grew 36% in a sector growing at 14%. https://www.gicouncil.in/media/4403/flash-report-may-2024.pdf

-

Summary of the CC. Go Digit General Insurance had a gross written premium (GWP) of ₹9,016 crore in FY2024, representing a 3.1% market share in total insurance and 6% in motor insurance. Key performance indicators showed strong growth in GWP, net earned premium, profit after tax, and assets under management compared to prior years. The combined ratio increased slightly to 108.7% in FY2024. The GWP mix shifted towards more motor own damage and health/travel/personal accident, while motor third party declined as a percentage. Overall growth was strong across segments. Investment leverage increased as assets under management grew faster than net worth. The investment portfolio is predominantly in sovereign and high-rated corporate debt securities. Loss ratios increased in health, fire and engineering segments but decreased in core motor segments. The company absorbed ₹69.4 crore of losses from natural catastrophes and large claims. The company is leveraging technology and API integrations to automate processes and improve efficiency to support future growth. Q&A Summary: Retail health insurance is a small portion of the health portfolio which is dominated by group insurance. This is a challenging but important segment the company is collecting data on to improve underwriting. Solvency ratio will improve to over 200% after the recent capital raise post-IPO. Exact number will be disclosed later. The company looks at combined ratios more holistically rather than targeting specific channel or product mix. It aims to be adequately reserved and profitable, and will avoid consistently loss-making segments. IFRS earnings were provided showing a reconciliation to Indian GAAP profits. IFRS-17 insurance accounting standards will have some impact on reported earnings. In general, the company is focused on calibrated, profitable growth rather than providing specific guidance or targets. It remains agile to market conditions and opportunities across products and channels. I think Kamesh did a great job of fielding the questions and providing enough color on the opportunities and the challenges. Definitely gave the impression that they are only interested in profitable book and will simply walk if it doesn’t make sense. Lots of questions and could have easily run longer than the hour allotted. Find attached the world’s worst transcription, unfortunately my software did not play nice but attached anyway. cc pres also attached. GO DIGIT GENERAL INSURANCE LTD Results Call_otter.ai.txt investor-analyst-presentation_q4fy24.pdf

-

Digit CC is later today, may be of interest. No mention, that I could find, of a replay or transcript being available afterwards. Following rego they provide a list of toll free numbers for most countries for dialing in. https://www.godigit.com/content/dam/godigit/general/investor-relations/stock-exchange-disclosures/intimation_pursuant_to_reg_30_earnings_call.pdf

-

Digit Earnings for Q4 (31st March 2024). Attached coverage from the Economic Times and the Digit release, USD conversions (assuming an exchange rate of 1 USD = 82 INR): Net Profit (Q4): Rs 53 crore (approx. $6.46 million) (up 104% YoY from Rs 26 crore (approx. $3.17 million)) Gross Written Premium (Q4): Rs 2,336 crore (approx. $284.88 million) (up 19% YoY from Rs 1,955 crore (approx. $238.41 million)) Net Profit (FY 2023-24): Rs 182 crore (approx. $22.20 million) (up 405% YoY from Rs 36 crore (approx. $4.39 million)) Gross Written Premium (FY 2023-24): Rs 9,016 crore (approx. $1.10 billion) (up 24.5% YoY from Rs 7,243 crore (approx. $883.41 million)) Premium Retention Ratio (FY 2023-24):85.8% (previous year: 81.6%) Premium Retention Ratio (Q4): 89.9% (previous year: 88.3%) Assets Under Management (as of March 31, 2024): Rs 15,764 crore (approx. $192.24 million) (up 24.4% YoY from Rs 12,668 crore (approx. $154.49 million)) Combined Ratio: 108.7% FY24 vs 107.4% FY23 & 108.8% Q4 24 vs 102.6% Q4 23 Currently trading about 3.5 x's GWP Go Digit Q4 Results PAT jumps 104% YoY to Rs 53 crore; gross written premium up 19% - The Economic Times.pdf press-release-q4fy24.pdf

-

True albeit with a financing component and +/- cash flow implications. As long as the price direction is correct then you also get the use of the cash in excess of interest payments on the way through. It becomes a bit of a virtuous circle when that cash gets used for buybacks below IV. The Ensign swaps demonstrated that the process can be as simple as Fairfax fronting up with the cash based on the days closing price. The counterparty doesn’t have to dump shares back into the market etc. they get surety of price and Fairfax gets a swag of shares. No epiphany but good to see it can be done this elegantly.

-

Wasn’t that yesterday’s closing price? It seems rather than have the swaps counterparty dump the shares onto the market,they have purchased them directly from the counterparty that arranged the swaps. I haven’t followed this closely but a Perplexity search offered the following: Equity Ownership In April 2022, Fairfax converted C$11.05 million of convertible debentures into 6,314,286 common shares of Ensign, increasing its ownership stake to 12.87% of outstanding shares at the time. In June 2020, Fairfax entered into cash-settled total return swap contracts for 4,557,600 notional common shares of Ensign, representing 2.79% of outstanding shares. On June 10, 2024, Fairfax terminated total return swaps over 7,787,600 Ensign common shares and agreed to purchase those shares at C$2.34 per share, representing 4.24% of outstanding shares. After the June 2024 transaction, Fairfax's beneficial ownership and control in Ensign increased to 29,588,486 common shares, or approximately 16.10% of all outstanding shares. Major Shareholder Along with Murray Edwards (approximately 23% ownership), Fairfax is one of the largest shareholders in Ensign Energy Services. As major shareholders, Fairfax and Murray Edwards have the ability to provide capital to support Ensign's operations and potential refinancing needs. Looks like they must have added to the swaps position after the initial setup in 2020. My quick search doesn’t show this. What I find interesting is that Fairfax purchased the share position from the swap counterparty. Might provide some color around how they intend to eventually wind up the FFH TRS position.

-

I am no expert but there are times in a countries economic development that you need a strong leader with a mandate in order to get stuff done. I wouldn’t call that a dictatorship but perhaps a “necesssary evil’. The risk here is that we go back to horse trading and India loses some of its momentum. An issue in terms years but irrelevant in the context of decades. Taking a glass half full perspective, perhaps it is “the pause that refreshes’ and it results in a better outcome long term. The market thinks otherwise.

-

@glider3834 that is good news. Importantly is there any provision to shake out Demetra Holdings and Logicom (25% between them)? I am reading between the lines but it almost appears to be an ideological reticence to sell. I guess everyone has their price but hopefully €2.56 is getting close.

-

@Parsad really sorry you have to put up with that kind of crap. The paywall is a low bar and I could just imagine old mate with 10 different usernames wreaking havoc otherwise.

-

Ouch, what a shitshow. Railway stocks tank 20% as election trends diverge from exit polls https://economictimes.indiatimes.com/markets/stocks/news/railway-stocks-tank-13-as-early-election-trends-diverge-from-exit-polls/articleshow/110693788.cms Download Economic Times App to stay updated with Business News - https://etapp.onelink.me/tOvY/135dde21

-

Unfortunately I think this is the case. Ben comes across as a pretty sharp cookie. If he gets on the front foot and cements his place as a competent chair and an articulate advocate for the company then there could be upside to both FIH and FFH. I was probably a little naive in my thinking about India a few years back, it is a tough nut to crack and you have some seriously entrenched players….Adani I am looking at you. On the flip side, I wonder if Prem can sniff some upside post election, you would hardly put your son in a position to fail.

-

Looking good for Modi and the BJP India Stocks, Bonds Set to Gain as Polls Show Landslide Modi Win Indian stocks, bonds and the rupee are poised to climb on Monday after exit polls indicated a resounding victory for Prime Minister Narendra Modi’s party in general elections that concluded Saturday. The polls suggest the Bharatiya Janata Party-led alliance will clinch substantially more seats than the 272 required for a majority in the 543-seat lower house of parliament, with most pollsters predicting the group will win between 350 and 400 seats in total. In 2019, the alliance won 352. The votes will be counted on Tuesday.

-

Excellent “Fairfax has built a very strong competitive position, through organic growth and strategic acquisitions, based on large and diversified re/insurance operations that are well established in their respective markets. Fairfax is one of the major global P/C re/insurers with $28.9 billion in gross premiums written (GPW) in 2023 (about $31.8 billion on a pro forma basis when including the $2.9 billion of GPW from the Gulf Insurance Group [GIG] acquisition in December 2023). We expect Fairfax's consolidated GPW to increase by about 15% in 2024 mostly driven by the GIG purchase. However, we believe the top line growth will likely moderate to about 5% in 2025-2026, supported by still favorable re/insurance.” https://disclosure.spglobal.com/ratings/pt/regulatory/article/-/view/type/HTML/id/3188808

-

Thanks, have you seen anything with respect to them gaining investment grade? I recall unencumbered vessels is part of the criteria. The summary I provided to the ATCO thread had this quote “Growing the Company's base of unencumbered assets is a fundamental objective in order to achieve an investment grade credit rating, as well as a potential source of liquidity through secured financing or asset sales”. I guess at this stage there would only be a deposit due to secure the build slot, so hopefully they gain an upgrade or two before having to finance another 1bn+ This game is economies of scale so once their borrowing cost is competitive coupled with their operational expertise, it gets very interesting.

-

Thanks @glider3834. Paywalled for me but available here https://archive.is/wOcd6 Key points - Seaspan is reportedly returning to ordering container ship newbuildings after nearly a 3 year pause. The orders are said to be worth $1.58 billion in total. - Seaspan has allegedly ordered 6 LNG dual-fueled 13,000 TEU ships from Chinese state-owned shipyard Hudong-Zhonghua, likely against charters to Ocean Network Express (ONE). The price is said to be at least $180 million per ship. - Seaspan has also reportedly ordered 4 methanol dual-fueled 9,000 TEU ships from private Chinese yard Yangzijiang Shipbuilding for about $125 million each, likely against charters to AP Moller-Maersk. The design is said to be the same as 6 Maersk methanol-fueled ships ordered from the same yard last year. - Deliveries of the 13,000 TEU ships are expected between early 2027-2028, while the 9,000 TEU vessels are due between late 2027-2028. - Seaspan did not order any container ships in 2022-2023 as liner companies were ordering ships directly themselves during that period. - In 2023, Seaspan made its first orders for 8 LNG-fueled car carriers from Chinese yards against 20-year charters to Hyundai Glovis, marking Seaspan's entry into the car carrier sector. - Seaspan has a current fleet of 176 container ships with more newbuilds delivering soon, many against charters to major liners like MSC, ONE and ZIM. It would be interesting to know the terms for the associated debt but good to see them locking in future growth.

-

Foran Mining released the results of their Winter drilling program on the Tesla deposit. As the mine is already feasible, Tesla is the icing on the cake. The close proximity to Macilvenna Bay sweetens the deal and in all probability it is likely to be an extension of the main deposit. Foran Mining is a ~250m position for Fairfax. https://foranmining.com/wp-content/uploads/2024/05/News-Release-Foran-Announces-Additional-Winter-Expansion-Drill-Results-at-the-Tesla-Zone.pdf "Our bold strategy to define the potential scale of Tesla during the winter ice-drilling campaign has effectively doubled the size of the mineralized footprint as our outstanding exploration results continue. The major down-dip step-out holes released today have provided some of the thickest and highest-grade results at Tesla to date, while once again affirming the consistent presence of the mineralized zone across significant strike and dip extents. The expanding scale of Tesla and its potential to continue beyond the currently drilled dimensions represents significant upside for Foran as we progress our flagship development project at the adjacent McIlvenna Bay Deposit High-grade drill results: Hole TS-24-20: 26.9m grading 1.23% Cu, 7.55% Zn, 38.4 g/t Ag and 0.20 g/t Au (3.67% CuEq) Hole TS-24-15: 11.8m grading 0.75% Cu, 8.22% Zn, 41.8 g/t Ag and 0.12 g/t Au (3.41% CuEq) McIlvenna Bay Project Probable Mineral Reserves: Total: 25.7 million tonnes Grades: 2.51% copper equivalent (CuEq), containing approximately 697 million pounds of copper and 1.4 billion pounds of zinc Indicated Resources: Total: 39 million tonnes Grades: 1.20% copper, 2.16% zinc, 0.41 g/t gold, and 14 g/t silver Inferred Resources: Total: 5 million tonnes Grades: 1.8% copper equivalent Bigstone Project Indicated Resources: Total: 1.98 million tonnes Grades: 2.22% copper equivalent, including 1.88% copper, 0.92% zinc, 0.25 g/t gold, and 9.5 g/t silver[1]. Inferred Resources: Total: 1.88 million tonnes Grades: 2.14% copper equivalent, including 1.35% copper, 2.75% zinc, 0.32 g/t gold, and 12.0 g/t silver. Tesla Zone (Part of McIlvenna Bay Project) Dimensions: Strike Length: 1,050 meters Dip Extent: 500 meters The zone remains open in all directions, indicating potential for further expansion

-

Thanks @Viking,although line ball I’d say, it sounds like this year’s AGM get together was one to remember. Aiming to make it next year though

-

Movies and TV shows (general recommendation thread)

nwoodman replied to Liberty's topic in General Discussion

Lolla: The story of Lollapalooza on Paramount+. A trip down memory lane, never got to one but have seen many of the bands featured in the early days. Was fortunate enough to see Jane’s Addiction on their recent tour and Perry is still rocking. Worth a watch. -

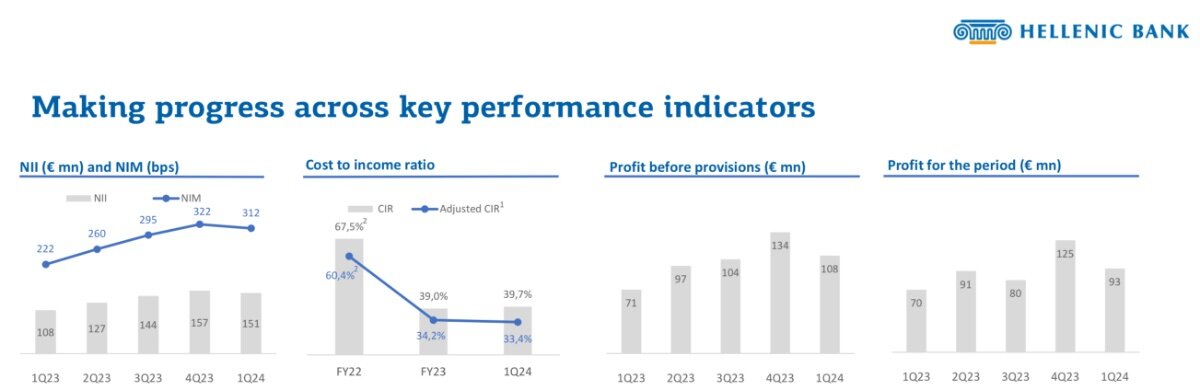

Thanks @glider3834 this is “getting better all the time” (sung to the Beatles tune). A quick recap via Perplexity with some extra notes Intro Eurobank, a major Greek bank, is in the process of acquiring a majority stake in Hellenic Bank, the second-largest bank in Cyprus. Here are the key details about this takeover, including economic aspects and share prices: Eurobank's Stake in Hellenic Bank Initial Stake: Eurobank initially acquired a 29.2% stake in Hellenic Bank in June 2021 by buying shares from a fund manager (€1.80?). Recent Acquisitions: In August 2023, Eurobank signed agreements to acquire an additional 26.1% stake from major shareholders like Pimco, Senvest, and Wargaming Group (€2.35). This would increase Eurobank's total stake to 55.3%. Regulatory Approvals: The Cyprus Competition Commission has approved this 26.1% stake acquisition, concluding it does not harm market competition. Further approvals are pending from the Central Bank of Cyprus, European Central Bank, and the insurance supervisor. Mandatory Public Offer Legal Requirement: After acquiring the 55.3% stake, Eurobank is required by Cypriot law to make a mandatory public offer to purchase the remaining shares of Hellenic Bank from minority shareholders . Investment Estimate: The total investment by Eurobank could reach up to €800 million (and the rest) if all remaining shareholders tender their shares in the public offer. Economic Rationale and Benefits Strategic Alignment: The acquisition aligns with Eurobank's strategy to strengthen its presence in core markets like Cyprus and increase profits from international operations. Economic Confidence: It is seen as a vote of confidence in the Cypriot economy's prospects after recovering from the 2012-13 financial crisis. Synergies: Combining Eurobank Cyprus and Hellenic Bank would create the largest banking group in Cyprus with expected synergies in costs and revenues. Usually hate this term but it could be material as management remains mum on this. Utilization of Liquidity: Eurobank aims to utilize Hellenic Bank's excess liquidity to support lending and projects in Cyprus and the broader region. Share Prices and Financial Performance Hellenic Bank Share Price: See share price graph below, its up around 14% with a current market cap €1.11bn Eurobank's Purchase Price: Eurobank agreed to acquire shares at €2.35 each in its recent transactions. Hellenic Bank's Financial Health: Hellenic Bank reported a net profit margin of 31.54% and a debt/equity ratio of 31.7%. The bank's earnings for the trailing twelve months (TTM) were €176.14 million, with a revenue of €558.47 million. For reference they just did €93.3m for the quarter! Mainly due to NII https://www.hellenicbank.com/en/group/results-and-reporting Next Steps and Challenges Regulatory Approvals: After regulatory approvals, Eurobank will launch the mandatory public offer, likely in Q2 2024. Merger Plans: Eurobank's ultimate goal is to fully merge the two banks in Cyprus, but this requires agreement from Hellenic's remaining major shareholders like Demetra Holdings. Shareholder Challenges: One shareholder, Demetra Holdings, has challenged the competition approval, potentially delaying the merger process. Future Synergies: The timing and structure of the merger, as well as potential synergies, will be clarified after the public offer and new Hellenic Bank management. Can’t wait to see what this looks like when fully integrated

-

Tinkerered with some ALS.TO. I think there is some asymmetry but ultimately it’s a a bit of a lottery ticket. Breaks all my rules but the CEO seems to have a good handle on the cyclical nature of the business. Intriguing.

-

Isn’t it crazy and looking back over the last three years it was infuriating. I’ll bet in the next 3 years it will be why bother. Then in 5 years that was a no brainer triple or 5 bagger. It is the way.

-

https://finance.yahoo.com/quote/GODIGIT.NS First day of trade..for posterity. Ended at around 5x’s GWP Some recent contemporaries, take it or leave it in terms of relevancy Lemonade Inc. (LMND) IPO Date: July 2, 2020 IPO Price: $29 per share Opening Price: $50.06 per share Closing Price on First Day: $69.41 per share First Day Gain: +139.3% GWP Multiple: 13.8 Most Recent Stock Price: $14.50 Root Inc. (ROOT) IPO Date: October 28, 2020 IPO Price: $27 per share Opening Price: $27 per share Closing Price on First Day: $27.00 per share First Day Performance: 0% GWP Multiple: 14.9 Most Recent Stock Price: $3.20 Oscar Health (OSCR) IPO Date: March 3, 2021 IPO Price: $39 per share Opening Price: $36 per share Closing Price on First Day: $34.80 per share First Day Loss: -10.77% GWP Multiple: 3.3 Most Recent Stock Price: $6.70 Hippo Holdings (HIPO) (via SPAC Merger with Reinvent Technology Partners Z) Merger Close Date: August 3, 2021 Initial Trading Price: $10.00 per share (SPAC standard price) Closing Price on First Day: $8.50 per share First Day Loss: -15% GWP Multiple: 12.3 Most Recent Stock Price: $1.60 Summary Lemonade Inc. (LMND): Had a highly successful debut with a 139.3% gain but is currently trading at $14.50, a 50.0% loss from its IPO price. Root Inc. (ROOT): Had a flat debut with no change in stock price on the first day, currently trading at $3.20, an 88.1% loss from its IPO price. Oscar Health (OSCR): Experienced a decline of 10.77% on its first day and is now trading at $6.70, an 82.8% loss from its IPO price. Hippo Holdings (HIPO): Saw a 15% decline on its first day after the SPAC merger and is now trading at $1.60, an 84.0% loss from its initial trading price. My take (but really what a bunch of smart people who actually matter): Fairfax (Digit) gets one chance to do this right and be accretive to all stakeholders. I think they have threaded the needle.

-

@Viking another great post. I am firmly in the camp of high prices solves the issue of high prices when it comes to commodities. However, as you point out, there is money to be made with the right investing framework and patience. The thing that strikes me about these recent investments is that they are very supportive of the view that Fairfax’s network and deal flow is in very good shape. I find it quite interesting that along with their investment in Altius came a board seat for Roger Lace. The board seat in itself is not that big a deal but for a relatively small investment they chose Roger for that gig. It might be bit of a stretch but do you get the meadow foods idea from an interest in a potash royalty company. It’s probably more of a case of “opportunities come to a prepared mind’ but it’s truly fascinating to watch it all unfold. As you have been saying, the investment model has evolved from the crappy turnaround to those more consistent with idea of the “100 year company’’. The recent copper thread got me watching a few of the recent interviews with Brian Dalton, Altius’ CEO/President. A fascinating guy and I can see why he would resonate with the team at Fairfax.