nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

Agree, it makes sense to keep shaving their shareholding so that buybacks can continue. I haven’t done the numbers but intuitively this should be the case up to ~€3 say an 80-85c dollar.

-

Very accretive at these prices. Fingers crossed we get a bit of a downturn in the market and they can keep firing away at these prices or even lower.

-

Doubt Bradstreet’s pulse raised at all .

-

Agree, I think price discovery on Ki has a lot of us intrigued. What has me so fired up about Fairfax at the moment is there is multiple positions that are in line for material revaluations and management has consistently said this will be the case and backs it via TRS and buybacks. Will post when I can pull a thorough set of notes on Meadow but had some great conversations at the AGM. I can see at least 3 positions joining the Fairfax billion dollar club in the foreseeable future. Edit: I think anyone watching the company is paying close attention to reinvestment/allocation. Stellar so far.

-

MS with a bullish note on Metlen. PT raised from €48 to €62 “PT Raised to €62 (from €48); 47% upside to current price (€42.12). EBITDA to double to ~€2bn mid-term; driven 60% by core (Energy, Metals, Infrastructure) and 40% by new ventures (Defence, Circular Metals, Gallium). Strong FCF: Positive even during €2.6bn capex cycle; FCF yield >13% from 2028. Dividend yield projected to reach 7% on 35% payout. Circular Metals & Defence highlighted as high-ROCE growth levers. Valuation disconnect: Trades at 4.5x 2028e EV/EBITDA vs 8–10x for peers. SOTP valuation implies €72–88/share – up to 100% upside. Risks: Execution, commodity prices, interest rates.” “In March 2025, Fairfax and METLEN agreed to a €110 million exchangeable bond. This gives Fairfax the option to acquire 2,750,000 METLEN treasury shares within two years at €40 per share-representing 1.92% of METLEN’s share capital. Upon exercising this option, Fairfax’s total shareholding in METLEN will rise to 8.35%, up from 6.43% in February 2025. This cements Fairfax’s position as a major and long-term investor in the company.” Another $1b+ position in the making? A billion here a billion there, pretty soon you are talking real money METLEN_20250515_1530.pdf

-

Good one. This is a 60c on the euro opportunity so buybacks add a lot of value. Lazy thinking suggests it makes sense for Fairfax to pay the capital gains tax and allow Eurobank to buyback more after this block. The good news is there will be no lazy thinking. What a remarkable situation, it does seem like this is shaping up as a go forward 15% CAGR embedded in a float leveraged entity striving for 15%. Where it becomes a bit heady is that Eutobank seems to be one of many.

-

Definitely, at current prices it would put Fairfax just over the 33.3% limit. So I think they are expecting some appreciation Buyback Impact on Fairfax’s Ownership Buyback authorization: €287.94m Share price: €2.41 Shares to be repurchased: €287.94m ÷ €2.41 ≈ 119.46m shares Shares outstanding (from TBV): €8.764b ÷ €2.39 ≈ 3.668b shares Buyback % of float: 119.46m ÷ 3.668b ≈ 3.26% Fairfax’s current stake: 32.3% × 3.668b ≈ 1.184b shares Post-buyback total shares: 3.668b − 119.46m ≈ 3.5485b New ownership %: 1.184b ÷ 3.5485b ≈ 33.36% At €2.41 per share, Eurobank is quietly delivering a near 7% capital return yield—split between a well-covered €0.09 dividend (3.7%) and a newly approved €288m buyback (3.3%). Pretty tasty

-

Great podcast episode recommendation thread

nwoodman replied to Liberty's topic in General Discussion

An interesting interview with JP Morgan’s Michael Cembalest. Starts at 24:15. Some notable quotes: Japan “So Japan's interesting because for the first time in like 30 years, Japan is really focused on shareholder value, which is some crazy number, like 50 or 60% of the Japanese market trades below one time's book. The number in the US is 4% or something. They've now said, okay, you have to do special dividends, you have to do spinoffs, and if you don't take steps to reverse that, you could be delisted. I don't think they're serious about that, but they're moving a lot of Japanese companies to do things they haven't done in a while. One of my really informal indicators is how many colleagues of mine have been asked normally against their will to relocate to Japan, to work on corporate finance, spinoffs and M&A activity, and that number for the first time in 30 years is starting to go up. That's a sign that there are things going on in the corporate sector which are focused on shareholder value rather than the other constituencies that the Japanese equity market is usually focused on.” The Armageddonists “It was a brief moment earlier this year, but it was down 20%. When the markets are down 20%, there's a dynamic that takes place, which is all of a sudden, there's this metaphorical crypt that opens up, and the financial media all of a sudden, Nuriel Roubini and Albert Edwards and Soros and all kinds of negative market voices tend to reappear like ghosts whenever the market's down to tell you how it's gonna get so much worse. And I've published this thing over the years called The Armageddonists, where every time there's a correction, then they come out and tell you how much worse it's gonna get, and I plot how much money you make if you take the other side of that.” Wealth Tax “But I'm very concerned about some of those wealth and equality issues. And the dam will break at some point and we will have a wealth tax in the United States. It's just a question of the level that it will be set at.” Drawdowns “Something happened to the psyche of investors, because I've been doing this long enough to have seen it. The Great Depression was this kind of distant thing, like the Civil War or the fall of the Roman Empire. And then all of a sudden, within one 10-year period, we had two 40 percent declines in the equity market. It's something that hadn't happened since the Great Depression. The first one was 2001, 2002, and then 2009 when we hit like 666, the mark of the devil in March of 2009. Because that happened and because so many of the fundamental drivers, particularly of the second one, were obscured and not understood until after the fact, investors ever since have lived with this sense of, is the next one the big one? I live on a seismic fault. And I think that's one of the mistakes that some of the Armageddonists make, is having lived through that experience, they can't shed the notion that I have to prepare for another 40% decline in the equity market. Whereas the kind of standard recession is more kind of a 12 to 20% decline both in equity markets and in earnings.” -

Key Takeaways from April Non-life Industry premium growth was up 13% YoY for Apr-25. Private multi-line players reported growth of 11% YoY in Apr-25. The lower growth since Oct-2024 is due to a change in accounting of long-term policies in certain segments (we do not have comparable base). ICICI Lombard (ICIL.NS) reported growth of 7% YoY vs -2% in Mar-25. Go Digit's (GODG.NS) GDPI was up 12% YoY vs flat in Mar-25. SAHI players reported 9% YoY in Apr-25. Niva Bupa's (NIVA.NS) GDPI rose 9% YoY vs 14% in Mar-25. INDIA_20250508_1818.PDF

-

MS coverage of Eurobanks Q1 25 results (attached) “Eurobank reported Q1 2025 EPS of €0.09, putting it on pace for €0.36+ annualised—just 6.7x earnings at the current share price of €2.41. RoTBV came in at a strong 16.2%, with CET1 at 15.5% and a low NPE ratio of 2.9% covered 89% by provisions. Tangible book value rose to €2.39 per share, meaning the stock trades almost exactly at book despite sector-leading returns, strong capital, and over half of profits now coming from international markets.” https://www.eurobankholdings.gr/en/investor-relations/financial-results-pages/first-quarter-2025 For a bank growing organically and compounding earnings, this remains cheap! EUROBANK_20250508_1614.pdf

-

Cool, looks like the bank of Fairfax is doing its thing. For context: In an interview with Retail Insider, Schaefer said what the new deal (referring to Fairfax acquiring Sleep Country) means is “probably status quo but maybe even with a greater sense of acceleration.” “It’s almost like a new horizon with some familiar faces. That’s how I look at it. I’m excited about it. We’re already a strong company with some fabulous, incredible brands but the fact that we’re teaming up with another Canadian iconic super power like Fairfax is quite exciting and the possibilities they were endless before but it just became a little bit more endless with the bank of Fairfax behind you if you know what I mean.” Some further color on the origins of the Simba Deal: “Sleep Country’s awareness of Simba Sleep predates the recent acquisition and is rooted in a longstanding business relationship. In 2018, Sleep Country Canada entered into a strategic partnership with Simba to exclusively launch Simba’s mattresses in Canada. According to Sleep Country’s Chief Business Development Officer at the time, Stewart Schaefer, the company was “searching the world for premium products to further enhance our online offering” and discovered Simba from the UK. This partnership allowed Sleep Country to introduce Simba’s hybrid mattress-in-a-box to Canadian consumers, leveraging both brands’ strengths in their respective markets. This collaboration was not incidental-Sleep Country actively sought out innovative international brands to expand its product lineup, and Simba’s reputation as a leading European mattress-in-a-box provider made it an attractive partner. Simba’s co-CEO, Steve Reid, also highlighted that Sleep Country was always their “#1 choice for Canada,” underscoring the mutual recognition and established business ties between the two companies. In summary, Sleep Country’s knowledge of Simba Sleep comes from years of direct partnership and collaboration, making the company well-acquainted with Simba’s products, business model, and market potential long before the acquisition took place.” May the tuck-in acquisitions blossom!

-

I will defer to Viking, but I am not sure they state this anymore. I think the math looks something like this: For 2024: Odyssey Group – 9.99% non-controlling interest Allied World – 16.6% non-controlling interest Brit – Reduced to 0% (acquired remaining interest in 2024) Gulf Insurance – 2.9% non-controlling interest after tender offer The total carrying value of non-controlling interests for insurance and reinsurance companies was $2.74 billion at YE2024, down from $3.12 billion in 2023 Subsidiary Ownership Minority Interest Float Contribution Estimate Deducted Float Odyssey Group 90.0% 10.0% $9.2B -$0.92B Allied World 83.4% 16.6% $8.8B -$1.46B Gulf Insurance 97.1% 2.9% $3.1B -$0.09B Total -$2.47B Interested to see what the answer is myself

-

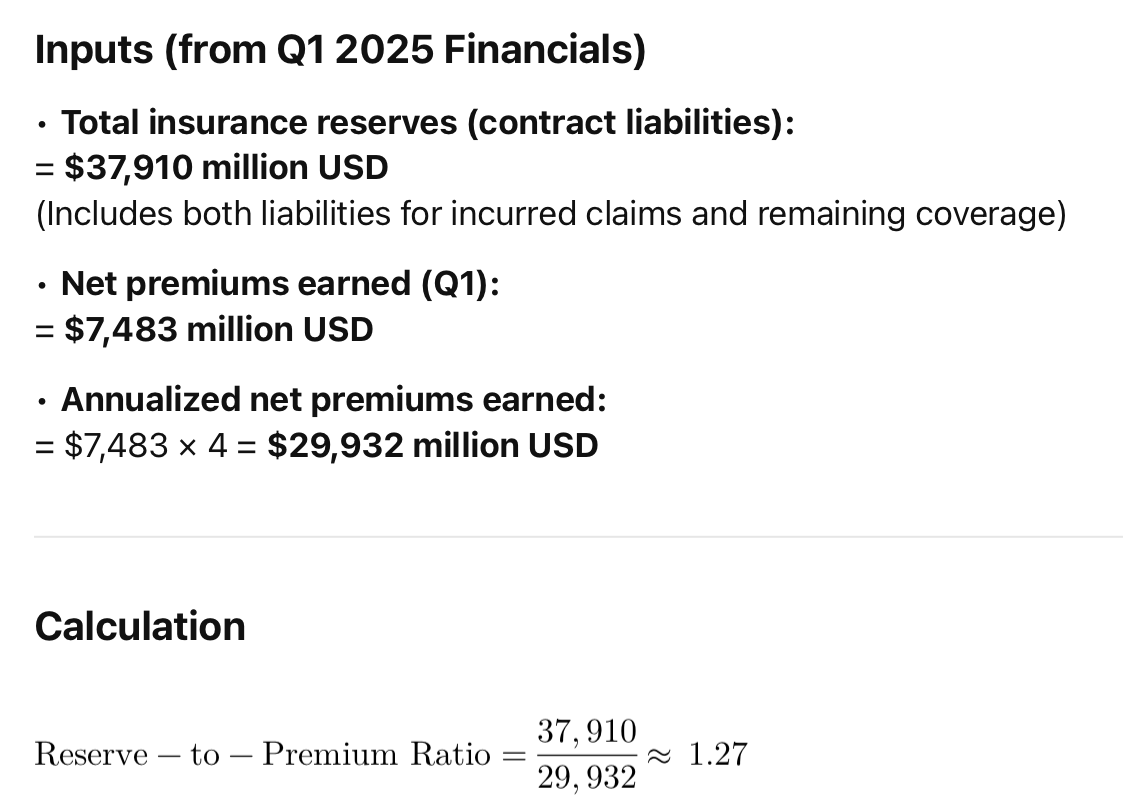

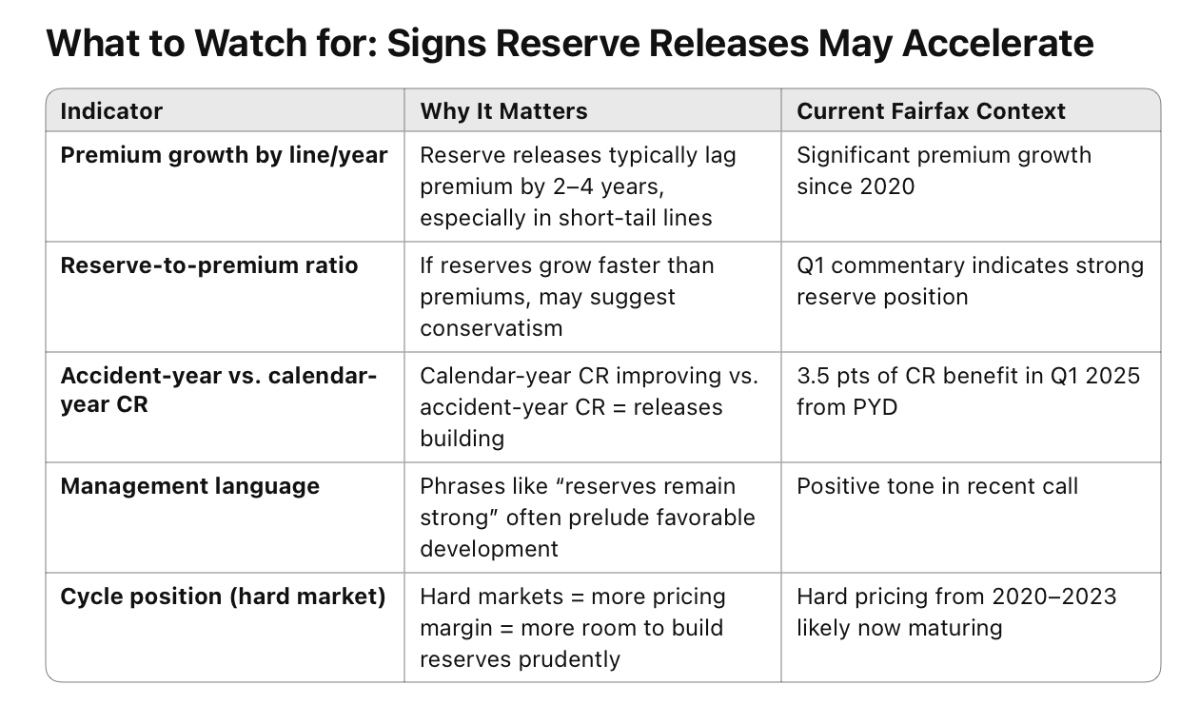

Good observation and great graph. History rhyming makes sense. “In the first quarter, our insurance and reinsurance companies recorded favorable reserve development of $219 million, for a benefit of 3.5 points on our combined ratio. Each of our major segments recorded favorable reserve development, with releases primarily coming on short-tail property business.” — Fairfax Q1 2025 Conference Call “Net favourable prior year reserve development, on an undiscounted basis, of $219.1M in Q1 reflected favourable emergence within each of the reporting segments, primarily at the Global Insurers and Reinsurers reporting segment (non-cat and cat losses at Odyssey, cat at Brit), and International (notably Gulf Insurance and Singapore Re).” — Q1 2025 Interim Report, page 30 “We are focused on setting our ongoing reserves at conservative levels, especially on long-tail lines.” — Fairfax Q1 2025 Conference Call “Fairfax’s reserve-to-premium ratio is approximately 1.27× based on Q1 2025 figures. That means for every $1 of earned premium, Fairfax holds about $1.27 in insurance reserves — a level consistent with conservatively reserved, well-capitalized insurers, particularly those with a mix of long-tail and short-tail business.” Quarterly is a bit clunky but gives a flavour.

-

I think that’s a very rational take. Incentives often drive short-termism, but Fairfax seems to have bucked that trend, 18 straight years of favourable reserve development suggests a consistent, long-term mindset. That deferred gratification thing. I also agree that a hard market creates the opportunity to build in margin, especially in long-tail lines. Setting reserves conservatively, when pricing is strong, can create future release capacity — not as a scheme, but as a strategic buffer. As we all know, it’s part of how insurers build resilience into the cycle. That said, it’s a fine line, and it only works if the reserving is grounded in sound actuarial judgment and continues to pass auditor scrutiny. It’s fun to go back and read the threads from 2010 when everyone was talking about Fairfax and their “crappy insurance businesses.” Wasn’t fun at the time but a good reminder of just how far they have come.

-

In terms of the offer? Potentially, sounds like they have left the door open ‘The Letter of Intent is not a definitive agreement with respect to the Proposed Transaction, and the execution of a definitive agreement in respect of the Proposed Transaction, if any, remains subject to, among other things, (i) the negotiation and execution of a definitive agreement on terms satisfactory to the Fund and Fairfax, (ii) final approval of the Proposed Transaction by the Trustees, and (iii) receipt of the Formal Valuation and Fairness Opinion satisfactory to the Trustees. The consummation of the Proposed Transaction would be subject to various conditions customary for transactions of this nature, including, among others, (i) receipt of any required regulatory, court and stock exchange approvals, and (ii) the approval of the Proposed Transaction at a special meeting of the holders of Units entitled to vote on the Proposed Transaction, including “minority approval” as defined under MI 61-101.”

-

It’s funny, my mind started down this path as well. Long-tail specialty definitely springs to mind. The longer the development horizon, the wider the reserving band, and that’s where some creative structuring could, in theory, create optionality. Not saying it’s common, but the ingredients are there. That said, this isn’t my area of expertise, just thinking out loud. Would be curious to hear from someone with regulatory or tax structuring experience.

-

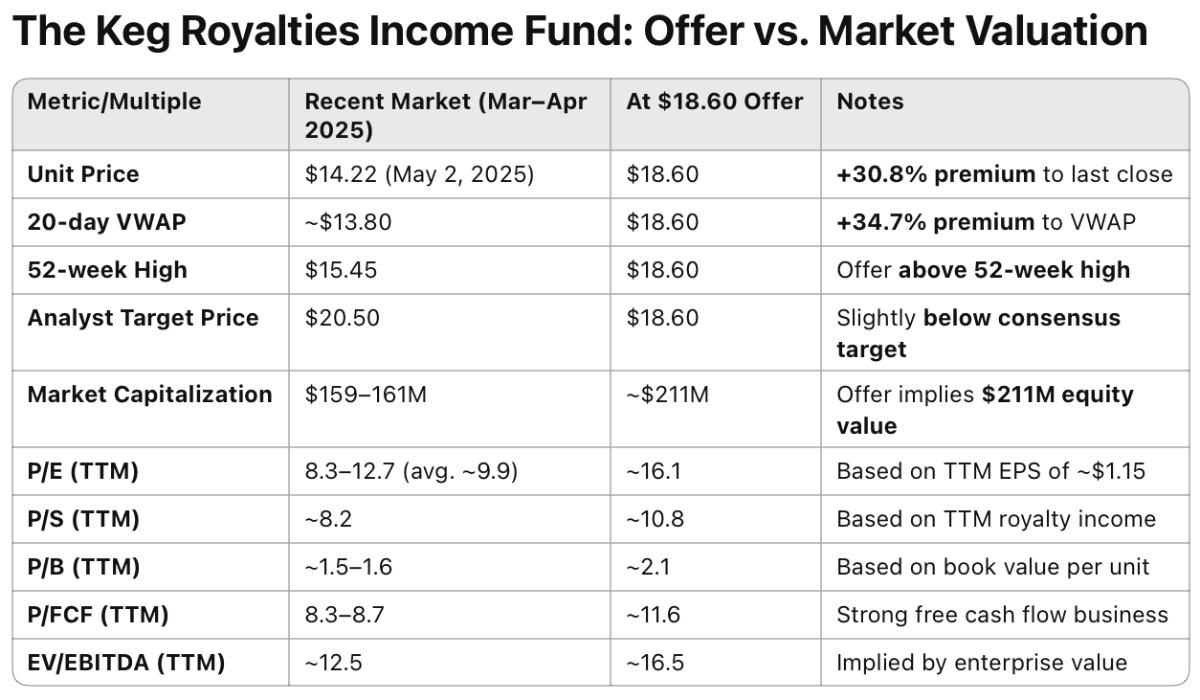

I dare say they are in a pretty good position to value this one: https://www.bnnbloomberg.ca/business/company-news/2025/05/05/fairfax-financial-signs-letter-of-intent-to-buy-keg-royalties-income-fund/ VANCOUVER — The Keg Royalties Income Fund has signed a letter of intent to be acquired by Fairfax Financial Holdings Ltd., its largest unitholder. The proposal for $18.60 per unit in cash values the steak house fund at about $211 million.

-

At the margin (which is your point), there is a natural timing deferral: reserves are expensed upfront and may be released in later years. But there’s little room to game the system — reserve levels require actuarial justification, not management discretion. Both IFRS 17 and the Canadian Income Tax Act (s. 1407) explicitly limit over-reserving as a tax deferral strategy, and regulators like OSFI provide independent oversight. That said, your broader point stands — there is deferred gratification in running a conservative book. The payoff comes in the form of modest tax deferral, smoother earnings, stronger market credibility, and the ability to allocate capital with confidence.

-

Yes, reserve releases reflect that prior years’ losses were overestimated, meaning those years’ combined ratios were actually better than reported. But insurers don’t revise history. The release is recognized in the current year, improving this year’s combined ratio, even though it relates to past underwriting. It’s important to understand: reserves aren’t just a guess, they are the essence of the insurance business. Setting them conservatively, and then seeing favorable development, isn’t just healthy, it’s a hallmark of disciplined underwriting. While reserves are data-driven, they also rely heavily on actuarial and managerial judgment, especially in long-tail lines. That’s why track record matters: it’s not about getting it right once, it’s about doing it consistently. And yes, there’s a smoothing effect to reserve releases but in well-run insurers, that’s a feature, not a bug.

-

Berkshire Hathaway Annual Meeting 2025

nwoodman replied to good-investing's topic in Berkshire Hathaway

My view too. I don’t think IV changed materially with the announcement. Share price was a little head of typical valuations so wouldn’t be surprised with a 10-15% decline. I am looking forward to Greg taking the reigns, I think we will learn a lot. In a couple of years time it might be like buying Apple in 2014. One can only hope. There is certainly more than a little bit of dry powder for buybacks. -

The latter. A reserve release occurs when: 1. A claim settles for less than what was reserved, or 2. An expected claim (like an IBNR reserve) no longer appears likely, based on updated data. In both cases, the insurer reduces the reserve, and the excess flows into earnings. It’s a backward-looking adjustment, based on actual claims experience, and reflects that the original estimate is no longer fully needed. Eighteen years of favorable reserve development certainly quiets the old rumours about skeletons in Fairfax’s reserving closet. +1 @Viking great Q1 summary. Like you, I’m still watching to see where normalized earnings land in the NICs. Key to how the windfalls have been recycled, I’m confident they’ll get there. $US2000 IV no longer seems wildly speculative.

-

Just for fun, Top 20 in 2029 assuming 14% CAGR.

-

Not Greg but sounds like you have this nailed, why stuff around and keep half a position. Plenty of great ideas out there. Keep that alpha coming.

-

A short but succinct conference call. I’m sure the quarterly results aren’t lost on those who’ve followed Fairfax over the long term.To absorb a catastrophe like the California wildfires — and still post an underwriting profit — is proof of Fairfax’s evolution and global diversification. Humming along springs to mind. Here’s the best of the call — in their own words: Insurance & Underwriting “Despite the significant catastrophe losses in the quarter, 781 million in total, our insurance and reinsurance operations produced an underwriting profit of 97 million.” “The ability to withstand such a large catastrophe loss in a quarter while still producing an underwriting profit in the quarter demonstrates the strength and scale of our insurance and reinsurance operations.” “We like that [cat] exposure is on the reinsurance side… it’s easier to control. We know what limits [we’re] standing [behind]… the loss we had was well within our risk appetite.” Investments & Volatility “There’s volatility in stock markets, bond markets and the economy. The good news is Fairfax has historically benefited from volatility.” “We think our stock and bond portfolios are in great shape for the environment we’re in.” “The worse it gets, the better we will perform over the long run.” Poseidon & Trade Risk “Poseidon is a financial and operating company in the shipping business with long term contracts backed by financially strong customers with outstanding balance sheets.” “Talking to the management team, they’re quite confident that the tariffs… and economic uncertainty around the world will not have any significant effect on their business.” “Locking in these contracts was a huge plus for them. So we’re very excited about the prospects of Poseidon.” Non-Insurance Operations “Excluding non-cash impairment charges recorded at Boat Rocker… the non-insurance companies reported stronger operating income in the first quarter of 2025 compared to the first quarter of 2024.” “Principally reflecting increased operating income at the restaurants and retail operating segments, primarily related to the consolidation of Sleep Country on October 1, 2024 and higher business volumes at Recipe.” Capital Allocation “We still think our stock price is very good value and we’ll continue to buy back our shares — but not at the expense of our financial strength.” “We do have minority interests in Odyssey and Allied… companies we know really, really well… over time, we’d like to buy back those minority positions.” “We have about 500 million of preferred shares that are coming up at the end of the year… we’re going to look at that.” Quiet, disciplined, and globally diversified — Fairfax doesn’t just endure volatility. It’s built for it. “The worse it gets, the better we will perform over the long run.” Interested in others perspective but this quarter along with my interactions with management and subs at the AGM I am still strongly of the belief that the company is still mis-priced. Long may it stay that way. To get shaken out because of misperception of fair valuation on the shares is my worst nightmare. There is just not that many good ideas that come along.

-

Some quality names. If you had to pick 5 with no tax considerations?