nwoodman

-

Posts

1,388 -

Joined

-

Last visited

-

Days Won

8

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

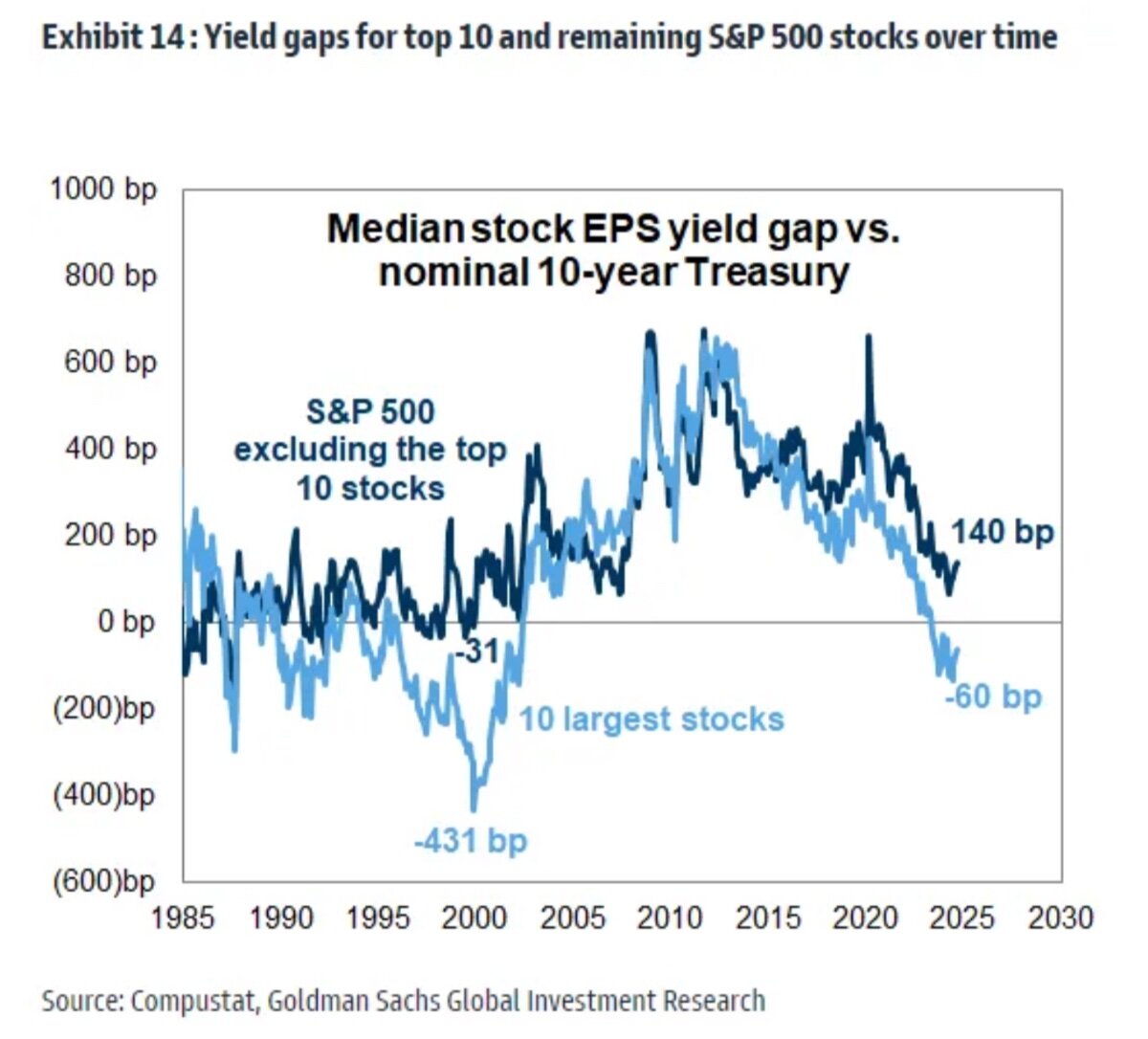

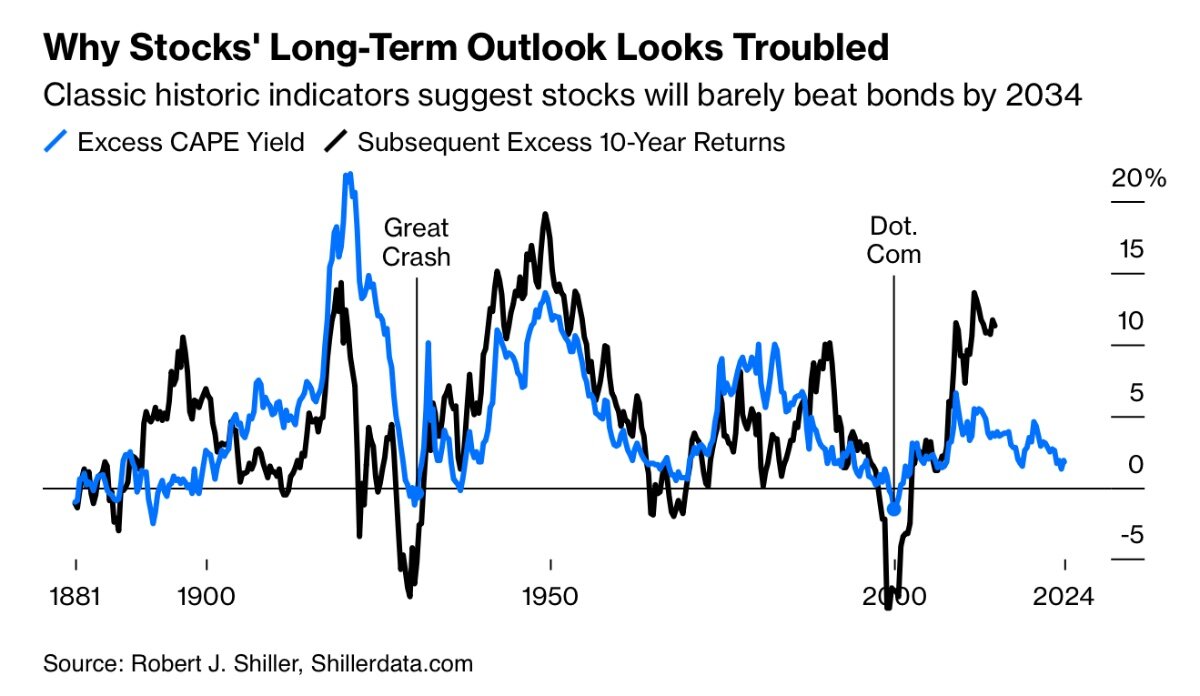

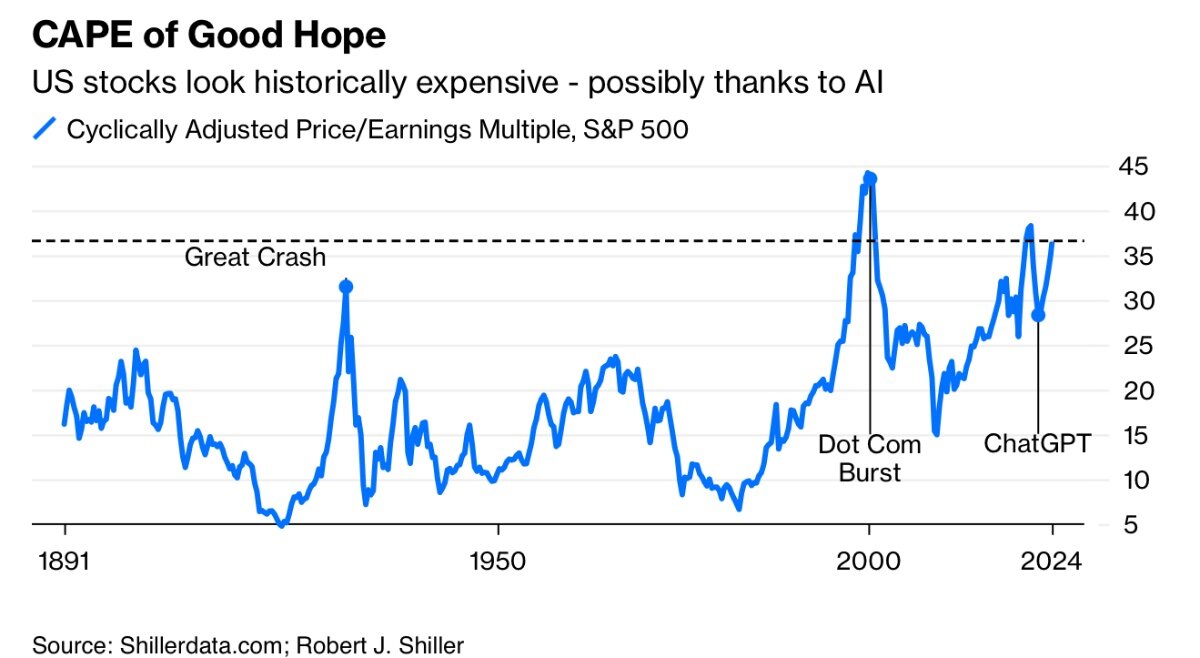

Some intriguing graphs in Bloomberg today. Hardly an inspiring outlook for the major US indexes, especially if there is a corporate tax hike in the offing. Cap gains tax increase would be a double whammy.

-

Movies and TV shows (general recommendation thread)

nwoodman replied to Liberty's topic in General Discussion

A couple of episodes into Disclaimer on Apple TV+. A good cast and intriguing story so far. A cut above the usual dross.

-

Hopefully in philosophical terms too. That lifeboat’s size and destination holds no appeal.

-

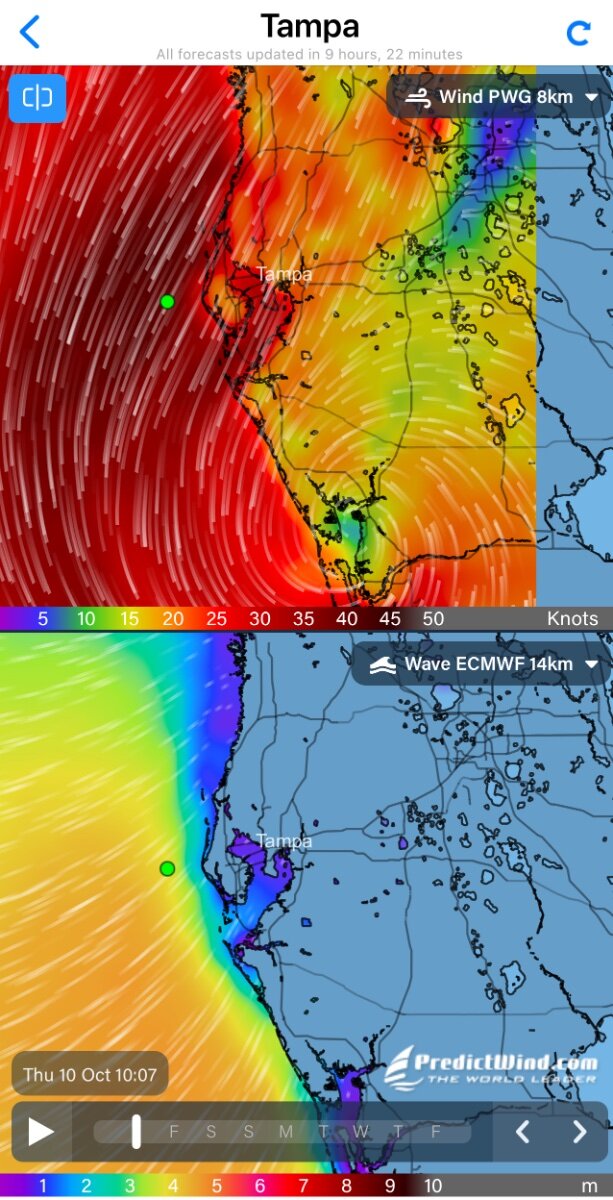

Bad, but could have been a lot worse. Devil will be in the detail. Just glad that this particular enviro bomb got diffused to Cat 3 at landfall and trajectory and wind direction made for offshore where it mattered. A bit further north….

-

A couple of thoughts: (1) Brian Bradstreet you absolute legend. (2) Did any of their competitors reach for yield? This may be the underpinning of a continuation of the hard market regardless of the cats. Taken together it must be a very high probability, even for the worst possible reasons.

-

Good, all things being equal they should be chipping away this month too. Stupid on my part, but it’s like some arcade game, can they get the share count to 20m at low multiples before they make the TSX60. This period reminds me of buying Berkshire at book in 2011 when you had a high probability IV was growing by at least 1% per month, that return was locked you just didn’t know if your return was going to be higher.

-

. True, I am sure if we put in the work there we could demonstrate a negative correlation between “gas bagging” and performance. Thank goodness Prem has been not been doing the rounds like he was a few years back. Coming back to the book, that is what struck me about the early years of Fairfax, “let the results do the talking”.

-

It's never just one thing, but Allied World may have been one of those "sliding door" moments for both companies.

-

Lot of scalps in the low 30b’s to take out. It’s probably inconsequential, for the moment, but fun to watch. https://companiesmarketcap.com/canada/largest-companies-in-canada-by-market-cap/

-

Agree. A feeding frenzy of “advice” does spring to mind

-

I was probably channeling your article in my comments above. Given so much good writing by others it is rare to have a unique view on Fairfax, well done again.

-

DeVocht now claims that the advice he received, geared mainly toward minimizing taxes, was negligent and failed to take into account his level of financial sophistication. His Tesla investment strategy involved loans from a Royal Bank margin account. Not sure about Canada but but by Australian standards he would have crossed over into “Sophisticatd Investor” status at around around $2.5m mark. To qualify for margin and play the game at the level he was to get to $460m he would have had to be qualified as an SI. I doubt RBC will be losing much sleep unless there was there was some shenanigans with the IHC angle or the ” charitable donation”. An asset test for investment sophistication is a useless proxy that is self evident.

-

Not a bad attempt, even if it is by an Australian https://www.firstlinks.com.au/warren-buffett-lost-edge-20-years-ago

-

I think it is a sweet spot for proficient float based allocators. It would be interesting to inflation adjust Berkshire and see what they managed to compound in the $US25->100bn range. Different times of course but lots of deals in the $1-5bn space for the prepared mind and that is without taking EM into account.

-

-

Just finished this one, thanks @glider3834for the lend. The three commentaries by Roger, Andy and Brian were superb. I figured we are among friends so reproduced them below. Even though these were penned nearly 15 years ago, what struck me is the continuity of thought. 1. Roger Lace For three years, day in, day out, Prem analyzed what companies were really worth: industrials, financials, every kind of business in Canada and the United States. He found it more like fun than work; he worked as much for the love of the game as for the money. He also made a number of lifelong friends, while never losing the chance to have a one-on-one training session with his mentor, John Watson. Such was the pleasure that, in 1977, he passed up a chance to take over as director of research for the lesser job of managing money for pension funds. His immediate superior was Tony Hamblin; Roger Lace and Brian Bradstreet were colleagues. “I'm sure there were a few guys who just said they were value guys because they had to, whereas Prem felt strongly about it. John Watson worked me over in the formal sit-downs, but Prem worked me over pretty heavily in the daily chatter by the water cooler and in the office. I was kind of neutral initially, a bit resistant, and he won me over by his rigorous, analytical approach. Where was Graham wrong? he kept asking, and since I couldn't find anything wrong, I was sold. I guess I would have to ask myself if that was Graham's doing or Prem's ability to convince people. Prem was very outspoken, very enthusiastic, and he had an almost evangelical feeling about value investing. He was so outspoken and had so much conviction that I think some people got tired of hearing about it. But not the true believers like myself and Brian Bradstreet. We bad to do a lot of internal and external presentations as analysts. Prem pounded the table and did not take opposition lightly. Over the years, I suspect, a few people probably took him aside and said, "Hey, you're coming on a little too strong here," because he became a very good listener. He took his persuasive powers and learned to point people in the right direction without being too heavy-handed. Once we got into portfolio management, Prem in particular wasn't one to modify his views in any way, and he took some pretty big positions in some pretty unpopular areas. I was of the same mindset, but I'm the type of guy who would rather switch than fight. If my superiors put their foot down, I went out of the room with my tail between my legs and did what I was told. Not Prem. There were more and more guidelines and policies laid down from higher levels, but in the rare instance that you felt there should be some leeway, you were allowed to take it to the CEO or certain members of the board. It was almost a joke because every other day, it seemed, Prem would be marching up to the boardroom to argue about the smallest details. And they always gave in, which was quite amazing.” Roger Lace 2. Andy Barnard In its early years, Odyssey Re began as a loose confederation of separately capitalized companies. In 2000, after the purchase of TIG Re, we restructured Odyssey onto a single, consolidated platform. Because of the numerous acquisitions from which Odyssey Re was created, the market was somewhat confused during this time as to what exactly was included in Odyssey, and what had been removed. “In 2001, we took the company public in an IPO. Going public was a very helpful way for the company to communicate to the marketplace a new coherent identity and establish our brand awareness. In September 2001, the 9/11 attacks accelerated the hardening in the market that had begun to take place late in 1999. We had created a much more compelling platform by having one company with a billion dollars of capital and branches around the world. These steps allowed us to participate very effectively in the hardening market. We went from writing about $150 million of premium when we started in 1996, to about $1 billion at the time we went public, to $2.5 billion three years later. The business that we wrote during this period has been very profitable. Odyssey has certainly defied its skeptics. The various pieces we acquired and stitched together over the years had all been challenged companies at the time Fairfax acquired them for discount prices. The team at Odyssey engineered a remarkable turnaround, which confounded those who believed it was not possible to turn around struggling operations. We went public at $18 a share; Fairfax took us private eight years later at $65. We grew our book value over this period at more than a 20% compounded rate - one of the best records in the industry. Prem sees the best in everyone. He is generous spirited with a wonderful sense of humour. His analytic mind grasps the essential details of business quickly, yet he's an extraordinarily warm person with a remarkable ability to connect. He's got a unique combination of exceptional qualities that drive the culture at Fairfax.” Andy Barnard 3. Brian Bradstreet Brian's worry had become focused on a seemingly esoterie matter, reinsurance recoverables. Simply put, because Firfax's insurance companies had laid off a large portion of their risk to a host of reinsurance companies, as is standard insurance company practice, their ability to pay claims in full was contingent on the ability of those reinsurers to pay the reinsurance they had provided. By 2004 those reinsurance recoverables totalled over $8 billion. “When I looked at that, I got scared. The more I looked into those reinsurance companies, the more scared I got. The investment markets were bubbly. There was a lot of crazy risk-taking. We ourselves on the fixed-income side were being offered Ponzi-type stuff that came with an AA or AAA rating. So I began to fear that the reinsurance companies we were relying on to pay us might buy this junk and get into trouble and we wouldn't get paid. That would bor us right out of the water: And so I asked, How can we protect ourselves? With the help of our analysts, I started researching all these reinsurance companies to see how mary treasury bonds they did or didn't own. If they owned a lot, I could rest easy. If they didn't own a lot, that meant they might not be able to pay us. What we found was that pretty well all of them, including the best of them like AIG, were taking enormous risks. That was our initial screening. Then we started to dig more, company by company, and we realized they owned all these asset-backed, mortgage-backed, high-yield bonds, which were pronounced as safe as treasury bonds but were in fact pure risk. One way to protect ourselves was to buy credit default swaps (CDSs), which were just appearing on the market around this time. They were basically bankruptcy insurance on the reinsurers. But I soon realized that we couldn't buy enough contracts on enough reinsurance companies to be diversified and fully protected. Then it occurred to me, Why don't we buy protection on the companies that are standing behind what the reinsurance companies are buying? If I was worried about the high-risk mortgage business, for example, why not bury insurance on the mortgage insurers in the United States? So we did. The next step was to buy insurance on the mortgage-lending companies like Fannie Mae and Freddie Mac, which were supposed to be government-backed but weren't in legal terms. Fannie Mae, for example, had $80 of exposure for every $1 of common equity, so it was a very good bet to fail. We bought our first contracts in 2003 and our last ones in December 2007. We just kept buying more and more, first five-year, then seven-year, because they were so cheap. By the end of 2006 we had invested $276 million in CDSs that the market valued at $72 million. At any other place I would have been kicked out on the street. Not here though. I remember going into an investment committee meeting where Prem asked, "What's the best idea we've got?" Francis Chou, who's a pretty shy guy, piped up, "Buy more credit default insurance." I didn't have the guts to say it.” Brian Bradstreet

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

Nice, cruisy setlist . Made me go looking for Donna Leake’s latest, funny how musical suggestion works. -

Cheers, PDF attached. Summary as follows: 1. Massive Newbuilding Programme: Seaspan has placed orders for 70 container ship newbuildings, delivered at a rate of one per week, to be completed by early 2025. This significant expansion is driven by demand, and the company is on track to finalize 32 additional newbuildings in 2024. Out of these, 23 vessels will remain under Seaspan's ownership. 2. Fleet Size and Capacity: By the end of 2024, Seaspan’s fleet will comprise close to 200 vessels with a combined capacity nearing 2 million TEU (twenty-foot equivalent units), making Seaspan one of the largest independent tonnage providers in the industry. 3. Diversification into Car/Truck Carriers: In addition to its container ships, Seaspan has diversified into the car/truck carrier market, ordering six newbuildings for Hyundai Glovis, set for delivery in 2026. 4.Fuel Flexibility and Retrofits: Seaspan is investing heavily in fuel innovations, particularly LNG and methanol. It is currently retrofitting five of its existing vessels, converting them to methanol dual-fuel, at a cost of $20 million to $25 million per retrofit, compared to the price of a newbuild at around $150 million to $160 million. This retrofit project, involving ships chartered to Hapag-Lloyd, is part of a broader fuel strategy, with Seaspan expecting to have between 50 and 60 LNG dual-fuelled vessels in its fleet. 5.New Investments in Dual-Fuel Technology: Seaspan is also pursuing ammonia dual-fuelled container ships, with approval for a 3,000 TEU feeder ship that can scale either way. These initiatives demonstrate the company’s commitment to greener shipping options while balancing financial sustainability. 6. Financial Discipline: COO Torsten Pedersen emphasized that Seaspan does not sign newbuilding contracts without charter agreements already in place, ensuring the company does not take unnecessary financial risks. This approach helps the company mitigate tail-end risk while staying agile in a fast-changing market. What is a Feeder Ship? A feeder ship is a smaller vessel used to transport containers between smaller ports (often referred to as "feeder ports") and larger ports (known as "hub ports") that serve as main shipping destinations for large, ocean-going vessels. Feeder ships typically have a smaller capacity, usually ranging between 300 TEU to 3,000 TEU, compared to the much larger container ships that can carry tens of thousands of TEUs. Feeder ships are an essential part of the global shipping network, as they help consolidate cargo from smaller ports, moving it to larger ports where the goods can be transferred to bigger vessels for international or long-haul shipping. Similarly, they are used to distribute containers from large hub ports to smaller, regional destinations. This feeder system allows for cost efficiencies by concentrating large amounts of cargo at central hubs while still ensuring access to smaller ports that cannot accommodate larger vessels. Inside Seaspan Understanding major newbuilding investments and what comes next TradeWinds.pdf

-

I would much prefer Clarke to Sokol. I might be a bit naive, but Clarke’s style imbues trust, Sokol not so much.

-

It may have nothing to do with FFH, a market wide margin call would have this baby throw out with the bath water in a heart beat, just the same with Berkshire. The point is to not get called yourself called or have the stomach to sit through it even with no margin. Hence the stress testing. In a 50% off market sale, is Fairfax going to be your number 1 pick?

-

What are you listening to ? (Music thread)

nwoodman replied to Spekulatius's topic in General Discussion

Too right, yep Amy is the original Energizer Bunny. I have been hoping to see them again too. Almost got my chance a week ago as they were doing a one night new album (Cartoon Darkness) release at my “local”…..unfortunately two days after we departed for a holiday in Indonesia . Their touring schedule has been frenetic, amazed they found time to get the new album done at all. -

Just scrap booking, probably needs inflation adjustments, currency devaluation etc. but even a 75% haircut would still tell the story

-

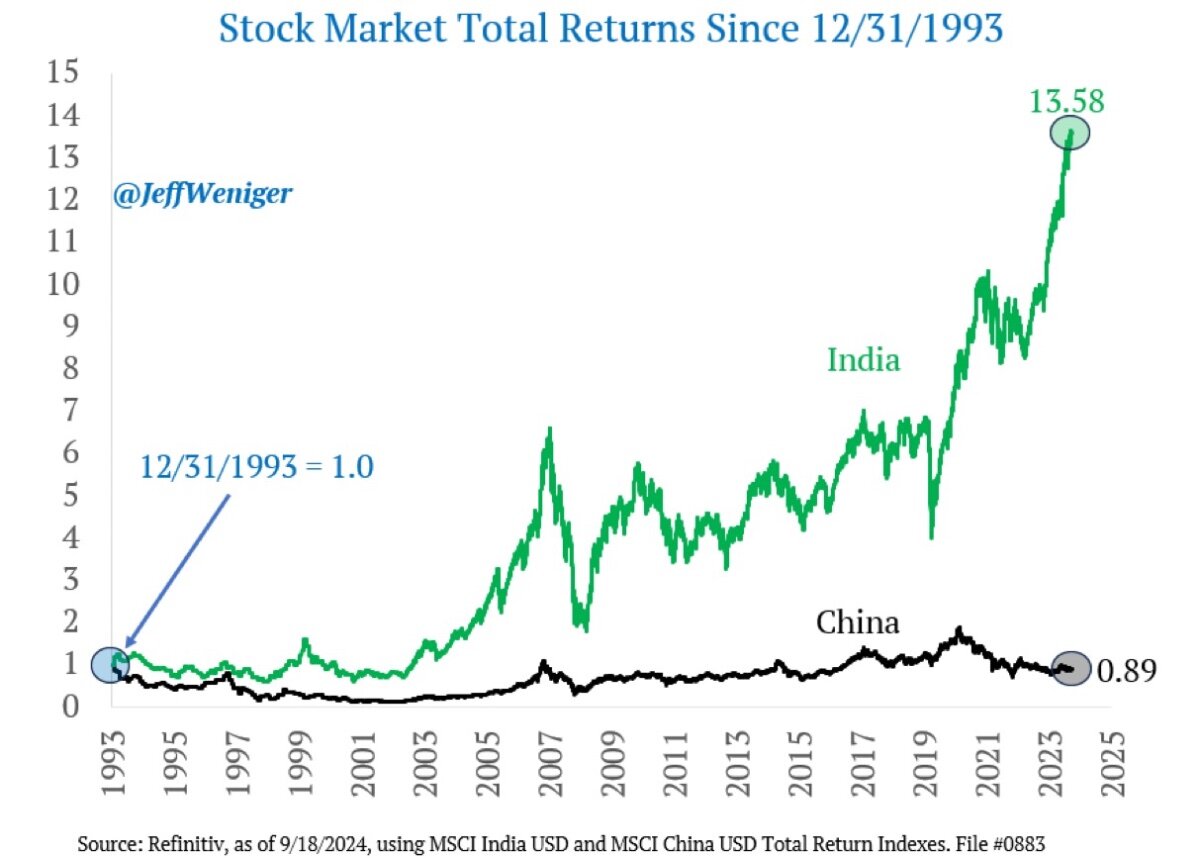

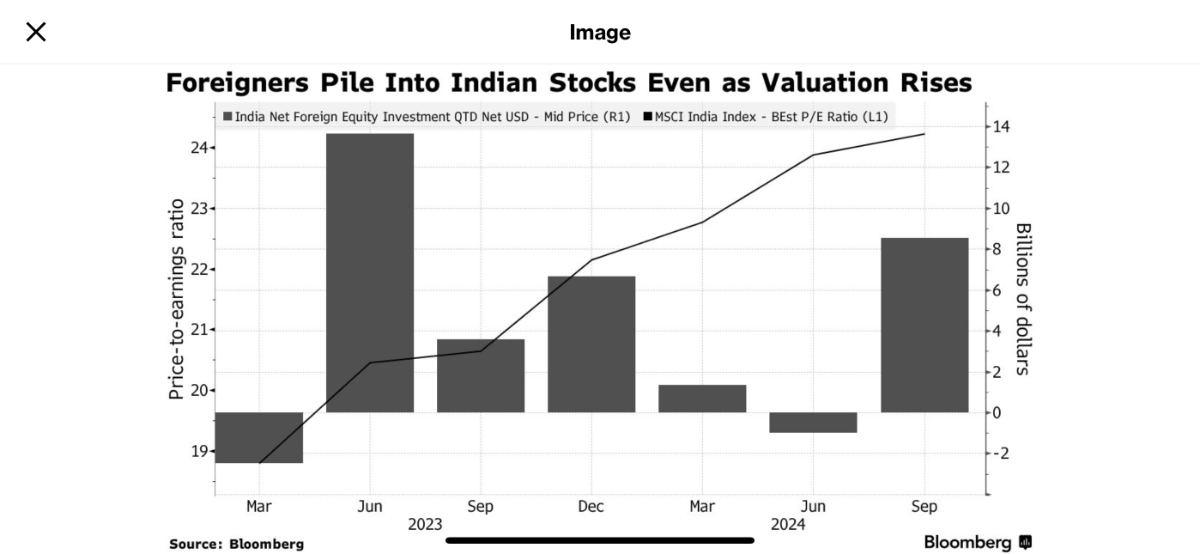

Global Money Is Chasing Indian Stocks Again as Bull Run Extends - Foreign investors have poured about $20 billion into Indian stocks this year, the largest inflow since 2020. - The MSCI India index has risen nearly 11% this year, outperforming other emerging market indices.

-

That would really raise issues with my Shitco Anonymous sponsor

-

JACK. Last held this 15 years ago. Love me some shitco action. PT $65 per share