nwoodman

-

Posts

1,891 -

Joined

-

Last visited

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by nwoodman

-

FFS. Hopefully a Cramer x10

-

I finally got around to pulling together some notes for Strathcona (attached). Thanks, @SafetyinNumbers. This was another constant reminder of what Fairfax has been up to over the last seven years. I am truly impressed with what Adam Waterous has pulled together—a textbook roll-up. No wonder Prem was so full of praise in the Annual Report. "We met Adam Waterous and the team at Waterous Energy Fund (“WEF”) in 2018. After a storied 27-year career in energy in Calgary, Adam was raising money for a fund to invest in and consolidate sub-scale, long life oil and gas businesses and assets in Canada. We were impressed by Adam’s focus on long term returns on capital. The WEF team had extensive experience in investing in oil and gas and Adam had built Waterous & Co, starting in 1991, into the largest oil and gas M&A firm in the world before selling it to Scotiabank in 2005. We invested $129 million which is currently valued at approximately $290 million through a stake in publicly traded Strathcona Resources. WEF built this company from scratch over 7 years into Canada’s 5th largest oil company producing close to 200,000 barrels per day of long life, low cost, very profitable oil. We then committed another $750 million to WEF’s next fund. The WEF team has already deployed a total from the fund of $323 million for a controlling stake in Greenfire Resources, a publicly traded oil company located in the Athabasca region of Canada. WEF’s latest investment is another business with long life (even longer than Strathcona!), low decline assets producing approximately 20,000 barrels per day that is Canada’s 11th largest oil company by proved plus probable reserves. In every respect, Adam has proven an outstanding Fairfax partner." Between Strathcona and WEF III, they probably have $1.5-2bn of IV in the making. I didn't have time to dive into Greenfire Resources, but given the pedigree of previous investments, you know it is going to make sense. I have no crystal ball on oil prices, but I think it is a good use of insurance float and consistent with the "100-year company" aspiration. Strathcona Resources Overview.pdf

-

+1. I plan to read it again, but on my first pass, I was struck by how certain sections felt like direct responses to questions raised here as well. It also conveyed a real sense of scale. I think it’s hard to reach any conclusion other than Fairfax isn’t just a solid insurance company—it’s a global powerhouse with $70B+ in assets, elite underwriting, and an investment portfolio stacked with long-term compounders. Still very cheap, in my opinion, and I can see why they remain confident in the TRS position. No idea where the share price will be in the short term but this will be a $US100B+ company within a decade.

-

Try not to follow the political threads too much so hopefully this is the right place. Another masterpiece by our very own Dave Rowe (@roweafr).

-

Thanks . Both interesting developments.

-

Thanks for this. These guys seem right up my alley, might have to do some work. Seems pretty cheap on a NAV basis at first pass. A couple of paras jumped out at me: “In a capital-intensive industry like oil and gas where capital is typically the largest expense, excluding DD&A in analyzing a company's profitability is akin to excluding the cost of the players on an NHL team. As aresult, popular Wall Street metrics which exclude DD&A such as "DACF" or "EBITDA" are four letter words in Strathcona's offices. Instead, we focus on post-DD&A metrics such as Operating Earnings, which reflect the profitability of the business after accounting for the very real capital costs required to maintain current earning power.” “In a capital-intensive business such as oil and gas, the value of existing production can quickly evaporate due to poor go-forward drilling returns, just like large production bases can quickly form from small ones if capital is profitably deployed. In the case of Strathcona, our future investment opportunity ($31.2 billion of future development capital on a 2P reserves basis) dramatically outweighs our current PDP PV-10 ($6.1 billion). To invest based on the latter instead of the former is a little like choosing a spouse based on who will be most fun on the honeymoon instead of the marriage... what starts with bliss can end in misery.” Edit: This is the very sort of long life asset that Fairfax should be investing in. Would happily see them own 20-30%.

-

Thanks @Hoodlum for pointing this out. It is an intriguing possibility. In pulling together some notes (attached) on AGT, it was not lost on me that they privatised AGT at pretty much the lows. It is a much better business today, and I wouldn't be surprised if margins improved due to some of their moves up the value chain. Apart from the apparent value investing bias to these ag-companies, I wonder if Fairfax finds something thematically appealing. In the notes, I have tried to touch on this but haven't quite figured out whether there is an angle they see that I am missing. I guess they are long life and consistent with the 100-year company thesis, bottom rung of Maslow's hierarchy etc AGT Foods Overview.pdf

-

This is really important, and I was thinking exactly that on my dog-walk this morning. For them to forward forecast 15% returns on Tangible Book, they must be pretty confident in something a little higher. Also means there was no skeleton’s in Hellenic’s closet. Well played Eurobank team.

-

Brief MS coverage of the results. They increased their PT to €2.77. Pretty conservative IMHO but consistent with European peers. Given Eurobanks management and growth prospects I think comps are not that useful. EUROBANK_20250227_1758.pdf

-

Eurobank results are out. Impressive! Maybe this deserves to trade closer to €4 than my PT of €3. https://www.eurobankholdings.gr/-/media/holding/omilos/enimerosi-ependuton/enimerosi-metoxon-eurobank/oikonomika-apotelesmata-part-01/2025/fy-2024/4q2024-results-pr-en.pdf FY2024 Key Financial Highlights: • EPS: €0.39 • Net Profit: €1,448m (Adjusted Net Profit: €1,484m) • Return on Tangible Book Value (RoTBV): 18.5% • Tangible Book Value (TBV) per share: €2.31 (up from €2.07 in 2023) • 50% Payout Ratio: • Cash Dividend: €0.105 per share • Share Buyback: €288m • Loan & Deposit Growth: • Performing loans grew by €3.9bn (+10%) • Deposits increased by €6.2bn • Net Interest Income: €2,507m (+15.3% YoY) • Net Fee & Commission Income: €666m (+22.4% YoY) • Total Capital Adequacy Ratio (CAD): 18.5% • CET1 Ratio: 15.7% • Non-Performing Exposures (NPE) Ratio: 2.9% (down from 3.5%) • Provisions over NPEs: 88.4% Regional Contribution: • SEE (Southeastern Europe) Contribution to Profits: 48% • Bulgaria: Adjusted Net Profit of €208m (+9.6% YoY) • Eurobank Cyprus: Adjusted Net Profit of €210m (+5.1% YoY) • Hellenic Bank: Contribution of €275m • SEE Core Pre-Provision Income: €800m (+53.1% YoY) • SEE Core Operating Profit: €739m (+58.9% YoY) 2025-2027 Business Plan: • Sustainable RoTBV Target: ~15% • SEE Contribution to Core Profit: Expected to increase to 55% by 2027 • Cumulative Payout: Expected to double vs. 2022-2024 • Loan Growth Target: ~7.5% CAGR • Wealth Management Growth Target: ~15% CAGR • TBV per Share Growth: Expected to increase by ~40% by 2027 Key Financial Targets for 2025-2027: Metric 2025 Target 2027 Target Core Operating Profit ~€1.7bn ~€1.9bn RoTBV ~15.0% ~15.0% TBV per Share ~€2.55 ~€3.20 Payout Ratio ≥50% ≥50% CET1 (post-payout) ~15.8% ~16.0% Key Takeaways: • Eurobank exceeded expectations in FY2024, delivering strong earnings and robust growth in loans and deposits. • The 50% payout ratio aligns with the bank’s commitment to rewarding shareholders. • The 2025-2027 business plan focuses on sustained profitability, regional expansion, and increased shareholder returns. • The integration of Hellenic Bank and acquisitions like CNP Insurance are expected to drive further growth.

-

I do enjoy the internet at times.

-

@StubbleJumper is/was like mind expanding drugs for me. One of a kind and super smart. Hope he is doing well. Great to read one his old posts, thanks @charlieruane reminds me to go back and read earlier posts on a number of topics. “There is gold in them there hills.”

-

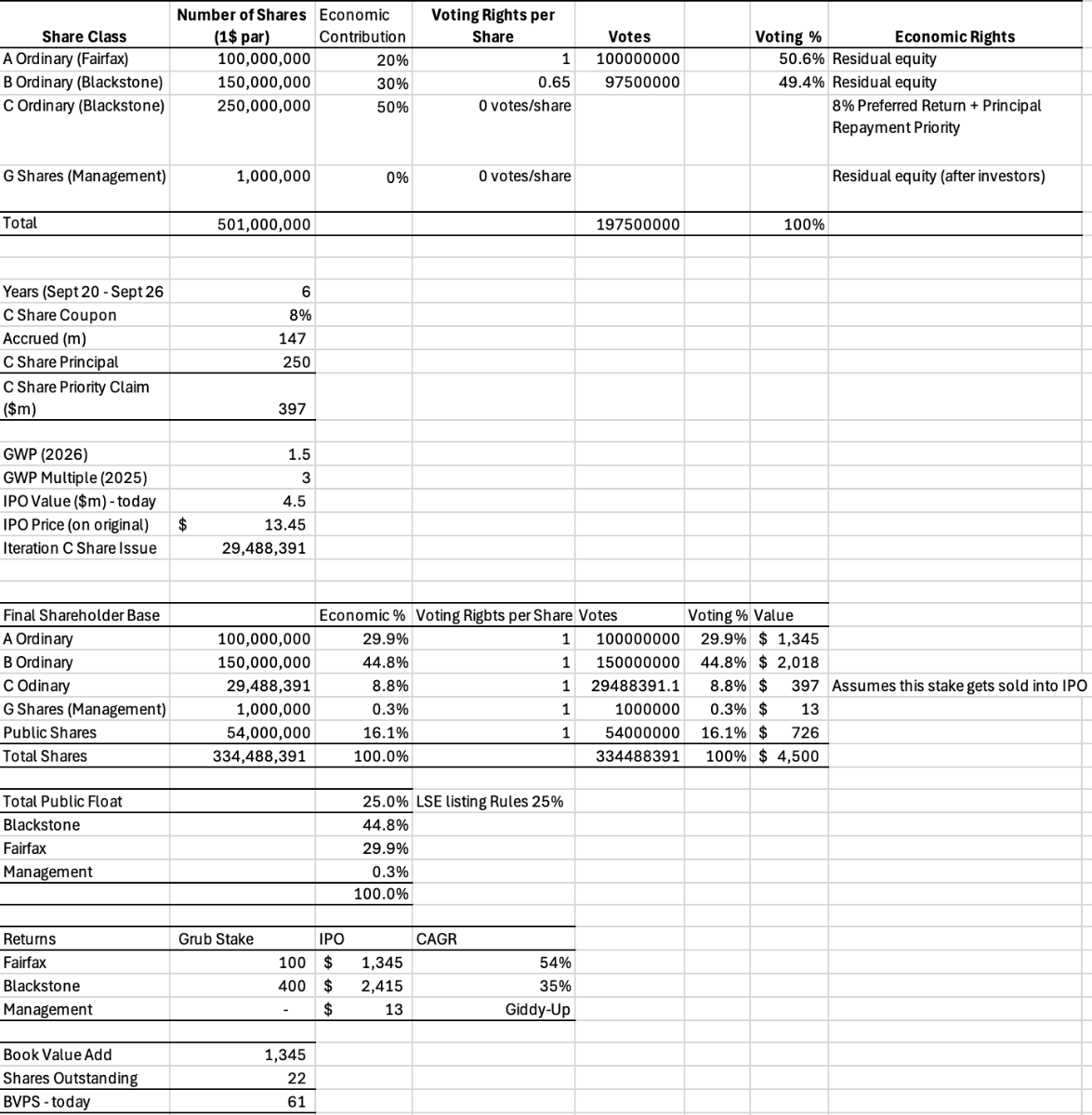

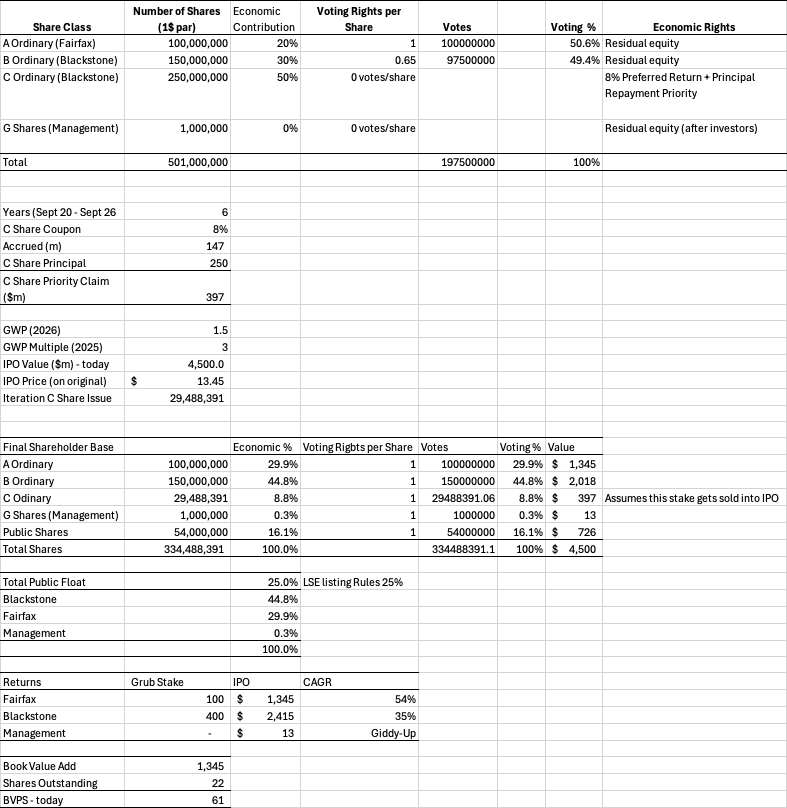

True, it also depends on the dilution of shares issued to the public. My quick read is that you need 25% in public hands to meet LSE listing requirements. In the numbers above I have assumed that Blackstone retains all their B shares and only sells the shares issued to cover what’s owing on the C’s. They may choose to sell some of those into the IPO. So lots of assumptions, IPO price, timing, dilution etc but I think you can conclude it will be a decent bump to book value at some point. In pulling together the notes, it did strike me that this is getting long in the tooth for a Blackstone investment (5-7 years on average), so I wouldn’t be surprised if they run it for a year or so under its own structure with an IPO 2026/2027. This is consistent with the view you had in your Substack article.

-

Just on Ki, some clever posters above posited that Ki might well be another serious home run, but yet flagged, we might be surprised at our fractional share, given Britt trained the model. I have some thoughts in the note attached, and I agree with both points of view. This will likely be a 40-50% CAGR over 6 years, and we got to do it with a Gorilla. Not sure how you even handicap a successful Blackstone partnership. Thanks, @SafetyinNumbers, for all the links you put in your Substack; my notes are far too lazy for that, hence notes. Currently, 3.5 GWPS premium is my baseline, but +/- 20% is down to the vagaries of the market. Great business, but what value have they created by working this through + being a partner that delivers for Blackstone? Ki Insurance Overview.pdf

-

Timely article from Mauboussin at MS entitled Probabilities and Payoffs: The Practicalities and Psychology of Expected Value (attached). Nothing new for the value investors here, but it did get me thinking about why I am happy with concentrated positions in Berkshire and Fairfax. Everyone’s risk tolerance is different but for me the key touch points in the article are: Fairfax Thinks in Expected Value Terms • Investing success is about payoffs, not just probabilities—Fairfax inherently applies this through its insurance and investment approach. • They take asymmetric bets—protecting the downside while positioning for large potential gains. Internally Diversified, Reducing Risk (the big one for me) • Insurance float provides stable capital for investing. • Investment portfolio spans equities, fixed income, and alternative assets. • Global presence and non-insurance subsidiaries offer further diversification. Aligned with Kelly Criterion & Position Sizing • If an investment has an edge, capital should be allocated accordingly—but not overbet. • Fairfax’s focus on capital preservation ensures it avoids wipeout while allowing compounding. Embracing Volatility While Managing Drawdowns • Hedging and contrarian investing have helped them profit in downturns (e.g., 2008). Sometimes this has come with opportunity cost but overall no significant capital loss. • Low correlated leverage prevents forced asset sales during stress periods. Even when seemingly cash strapped they have a remarkable ability to pull a deal together via their extensive and ever growing network. Final Thoughts • Risk management is their business, making them an ideal concentrated bet. • Their ability to capitalize on market inefficiencies aligns with a long-term compounding strategy. • Tax is a consideration for me, so an acceptable return while leveraging an unrealised tax liability works well for me. I think Prem’s aspiration to build the 100 year company along with the tenure of key personnel and the resultant culture are key factors for me. The article is worth a read, just to reinforce probabilisitic reasoning. Authors: Michael J. Mauboussin – Head of Consilient Research at Counterpoint Global, Morgan Stanley Dan Callahan, CFA – Member of the research team at Counterpoint Global, Morgan Stanley Mauboussin is well-known for his work on decision-making, behavioral finance, and the application of probability and expected value in investing. His background makes this report particularly relevant for investors who focus on risk management, capital allocation, and probabilistic thinking. article_probabilitiesandpayoffs.pdf

-

These are important points, and the second one is something I’ve been thinking about a lot since the CC. This deal gives a glimpse into the kind of earnings power that comes from shifting a portion of the fixed-income portfolio from safe treasuries into higher-yield corporates. They have been telegraphing this intent for a couple of years now. I’m not saying that shift has fully started yet—you probably need some real stress in credit markets for that to accelerate—and even then, it’s only ever going to be a portion (maybe 25% at most?) of the FI portfolio, given RBC constraints and regulatory capital rules. That said, it illustrates how much earnings power can change under these conditions. As you pointed out, it’s easy to be anchored to a decade of low rates, but these yields aren't necessarily outliers in an HFL (higher-for-longer) environment. I still don’t think that kind of optionality is being priced in. If Fairfax continues to lean into private credit and structured high-yield deals like this, the long-term earnings profile of the fixed-income book could look very different from what the market is currently expecting.

-

MS with a breakdown by non-life insurance sector. It looks like Digit’s speeding ticket is still intact INDIA_20250214_1507.pdf

-

MS with a positive spin (see attached) “The broad market is drawing down rapidly as the bid has faded despite improving fundamentals. While catching the bottom is difficult, we think buying Indian equities could prove rewarding.” INDIA_20250217_1001.pdf

-

Thanks @Viking. Agree with all your points. There is a degree of sophistication to the way Fairfax is going about things that I wish I had appreciated more. There is also a frankness in the CC’s that is quite refreshing “Peter Clarke Right. Yes, no, that's -- the TRS on Fairfax, that's strictly an investment for us. We put it back on in 2021 or thereabouts and it's performed extremely well and we think it will continue to perform very well. As we said, we can see strong underwriting results going forward. Our interest in dividend income is strong, our associate income is strong. But we feel we'll be able to continue to compound book value at a very high rate or acceptable rate, and our share price will follow. You know, we're not trading at a high multiple if you look at our peers and so for us, it's still an investment, we very much like.” The thing that make’s my head spin a little is their short and medium term opportunity set. $835m of timeshare financing at an aggregate >10% was not on my bingo card for January. For a while I have felt they have/perceive more opportunities than they have available cash. Just hope they don’t get over their skis but so far, so good.

-

Not sure, other than their debt raises, there aren’t too many details available on their instruments of choice, but interesting point about the FX implication. CAD would definitely help the cause . I thought you might have had a handle on who the Total Return Payer was, pretty sure you figured it was one of the Canadian Banks so I think there is a high probability it is in CAD. Anyway some notes attached, it’s definitely floating rather fixed as they have discussed a “ higher TRS expense” previously that coincided with rising rates. Fairfax Financial’s Total Return Swaps on Its Own Shares.pdf

-

While that would be awesome, surely this is at the prevailing rate, SOFR + spread. Cheap compared to IV growth, but unlikely to be locked in. I am tipping 4.75%+2%=6.75%.

-

I am a Fairfax investor, so it crossed my mind of course. Vacatia is obviously the price taker here and Fairfax didn’t have to do the deal. There needs to be enough cashflow to service the 80m of financing (unless there is a PIK provision to the note) and whatever Vacatia needs to set up their system at Berkeley to start clipping tickets. You would hope the assets were some way to this target and then Vacatia generates the rest through the overnight rental market plus some asset sprucing. In the pdf I outlined some thoughts on how it might work but it’s speculation. If it goes tits up then you hope that the Berkley assets can be sold at cost. My only other thoughts are Wade Burton’s tie ins with KW and Eurobank, he seems to like (tourism) property but as @petec said there has been a few flops or works-in-progress depending on your timing. As I said above I would love to know how this originated and whether it came via KW or an associate. Out of the blue seems unlikely but possible. Will be watching this one with great interest due to the quantum but also an insight into Wade’s deal making and risk management. In both areas I think he excels BTW. Always difficult due to the way Fairfax allocates capital to attribute a decision to one person though.

-

Indeed, as you pointed out above if it works the leverage will be pretty phenomenal albeit on $25m of equity. It will be interesting to get some color on the terms of the note, perhaps AR or at least Q1.

-

Sensex down 3,000 points in 9 days. Is it just the beginning of bear market? Quite the blow off in Indian markets. On the updside, IDBI is down 30% since its peak in July 24. At the current market capitalization of INR 775 billion, the 60.72% stake being put up for sale is worth approximately $5.42 billion USD.

-

Corrected in V3 above, it should have read Vacatia contribute their business model to the Vacatia Blizzard JV. Vacatia is definitely still a stand-alone. I also corrected the EV/Owner table on the basis that Berkley got done at $835m (Fairfax) and $25m (Vacatia)=$860m. We don't know this for sure (chance of financing outside of Fairfax), but on face value it does seem like a decent margin on safety. However I know SFA about the the timeshare industry so take it with a pinch of salt. The Vacatia business model of timeshare plus overnight rentals isn't unique but might make a real difference to legacy assets like Berkley. I guess that's Vacatia's bet and if it doesn't turn out well Fairfax flips the underlying assets. Each year Fairfaxearns $80+m so the margin of safety improves. I would love to know how this deal orginated, perhaps yet another question for the AGM. Wade Burton from the CC " Second, I wanted to discuss an investment that closed just after year-end 2024. We invested in the largest independent timeshare company in America called the Berkeley Group. Caroline Shin and her team at Vacatia are Fairfax partners here. The investment is underpinned by asset value, where we directly own 4,950 full-service vacation units mostly located in Las Vegas, Orlando, and other high-traffic vacation areas in the U.S. The opportunity here is for Caroline and her team to generate overnight rental income from the huge stock of nightly vacancies. Her experience designing Hotwire online booking software and then as an executive at Starwood is perfect for what Vacatia is trying to do with Berkeley. In fact, prior to this acquisition, her group at Vacatia made investments in five smaller timeshare assets from 2019 to 2024, and in each case, they were very successful at significantly growing EBITDA in a short period of time. The total deal was $835 million, which we funded with a $275 million five-year preferred note at 13.5%, a $365 million seven-year senior secured note at 9.5%, and $170 million mortgage warehouse loan with a five-year maturity at SOFR plus 400. The $50 million equity is funded 50% by Fairfax and 50% by Caroline and her partners. We are absolutely thrilled to be her partner on this."