Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

The situation in Canada is frightening. The more i think about it, the more our situation is beginning to parallel the US in 2006 or 2007. The key is ‘higher for longer.’ If rates stay around current levels for the next year i think we will see the beginning of big problems in the housing market in Canada. The cracks are there already. Higher for longer, if it happens, means our mortgage market today is just like the wacky mortgage market the US had in 2005-2007. People don’t see it… the real estate market here is definitely giving off ‘Big Short’ vibes right now. Maybe i need to go to a local strip club and do some proper research. I was listening to a local real estate podcast (the Tom Storey show) and the guest realtor they had on said repeatedly “we all know real estate prices only go up.” She sounded like a nice lady… reminded me of ‘its just a gully.’ The issue was crazy low teaser rates… these allowed people to buy a house to live in they could not afford. But why let a good thing go to waste? Many Canadians became real estate ‘investors’ and started buying multiple real estate properties as well. The big difference in the US and Canada is the crazy low low teaser rates in Canada have been available for a decade. This has allowed fortunes to be made on real estate in a very short period of time. I have been one of the winners (although i now rent - i cashed out my winning ticket in 2021). Canada’s entire economy became focussed on one asset class: real estate (as a % of GDP). And Canadians are obsessed with real estate. Low teaser rates for a decade have blown a real estate bubble of epic proportions. In Canada when people buy a house it is usually done with a mortgage that has a variable interest rate (changes immediately when rates change) or a 5 year fixed interest rate. I think amortizations can be a max of 30 years. For 40 years, a variable rate mortgage was a winning horse - for these borrowers interest costs kept falling every year. During covid variable rate mortgages dropped below 1%. More risk averse Canadians take out a 5 year fixed rate mortgage. These also fell over 40 years and bottomed at 1.39% during covid. As interest rates fell for 40 years straight, well house prices have done the opposite and gone straight up for close to 20 years. Guess how much house you can ‘afford’ if you pay under 1.5% on your mortgage? House prices in Canada experienced their blow off top in Feb and March of 2022. The increase has been epic. Today a 5 year fixed rate mortgage is about 6.2%. Variable rate mortgages are higher than this. ‘Higher for longer’ means any Canadians who have an oversized mortgage (there are more than a few) are screwed. So where is the carnage? Everything looks ok? Most of the variable rate mortgages have a uniquely Canadian twist… they are called ‘adjustable’. If interest rates go higher the borrower can pay more in interest and less in principal - but the total mortgage payment does not change. To make the math work, the amortization period is extended. Lots of variable rate mortgages in Canada now have 40 or more year amortizations (yes, when 30 is the max) and some are as high as 70/years. Some of these mortgages are so far offside that the total mortgage payment is no longer covering all the interest costs - the mortgage balance is actually increasing for these loans. Here is where the story gets interesting. All mortgages in Canada will reset every 5 years (variable and fixed rate). That means about every year 20% of all mortgages will be up for renewal. This is when everything gets ‘trued up’ - total payment and amortization. Of course, 6.2% is NOT generally workable if you have a large mortgage. So ‘higher for longer’, if it lasts, is a death sentence for Canada’s housing bubble. But it will take another year or so to become more apparent. Investors are starting to cry uncle. Since about 2015 most real estate purchases in Canada for ‘investing’ were already cash flow negative - even at the low ‘teaser’ mortgage rates. House prices were going up 6-8% per year. Being mildly cash flow negative was simply a cost of doing business. At 6.2% today investors are getting taken out behind the woodshed - their monthly costs and losses have mushroomed in the thousands of dollars. The icing on the cake is, in Vancouver and some parts of Toronto, landlords can’t raise their rent much (Vancouver allowed a rent increase of 1.5% in 2022 and a 2% rent increase in 2023). And the price appreciation has stopped. So investors are screwed. But they are a hardy lot. And, after all, interest rates WILL come back down. Canadian housing ONLY goes up. What is a rational investor to do? Buy and hold. Hang in there. Well, losing thousands of dollars every month eventually works it magic. Like a splash of cold water on the face, ‘investors’ are starting to - well - run out of cash to burn. Not surprisingly, we are seeing higher rates hit the investor part of the market first. For sale inventory is starting to build - and about 50% of it appears to be from investors. Where this gets interesting is where we go from here. If inventory continues to build and we start to see prices fall 10%. If you are an investor and you are deeply cash flow negative AND real estate prices start to correct lower… you are worse than screwed. Now you risk getting wiped out financially. Leverage is a bitch when it goes against you. Within the investor segment, the condo pre-sale market could get very ugly in the coming year. Lots of ‘investors’ put down a deposit years ago on a unit that they intended to flip at a much higher price once it was completed. This strategy was a license to print money for years. These ‘investors’ can’t now sell the unit when it comes to market as the selling price is going to be below their agreed to purchase price so they will lose their deposit (or more). And they can’t buy the unit either - they do not quality for a mortgage at 6.2%. Lots of people own multiple units like this. A legal shitstorm in the making. For borrowers who live in their residence this whole thing gets complicated. Canadians are very resilient at finding solutions - so i am not sure how it plays out here. Other than mortgage payments are going through the roof for those carrying large mortgages. But it will take a few more years to fully play out. The big banks will work with mortgage holders. They will extend amortizations to take the sting away a little. The Liberal government will also likely try and do something. So perhaps we muddle through. ‘Higher for longer’ will be the key of how this plays out. But the storm clouds are forming. And it looks like it might actually pick up enough speed to become a hurricane…

-

Great discussion. Some thoughts: - where are the body bags hiding from the spike at the long end of the curve? Wo are the big losers here? What should be avoided? - how high could the yield on the 10 year go? 5% or higher? - does the US 10 year treasury set the value of all other investments? - if so, what is the move higher in the 10 year treasury tell is about other asset classes? - i am a total return investor. I don’t really care where it comes from. For me, the most interesting development in 2023 is the resilience to higher interest rates in the US. Its like higher rates don’t matter. Businesses (issued debt and locked in low rates for a few years) and consumers (locked in low rates on 30 year mortgages) in the US both made smart decisions during covid so higher rates are not affecting many. And governments aren’t interest rate sensitive (with spending). At least thats the case today. What happens in the US matters in the rest of the world. Other part of the world are much more sensitive to higher rates (like Canada). I know we are supposed to ignore macro. If interest rates at the long end of the curve continue their march higher I think we will get some wonderful opportunities to ‘buy low.’ Because, contrary to what we have learned in 2023, interest rates really do matter. A lot. Where will the opportunities come from? No idea right now. And that is one of the things i love about investing. The value (optionality) of having a little cash on hand is going up. And you are getting paid 5% while you wait. Cash as an investment is looking very good to me today (for a part of ones portfolio).

-

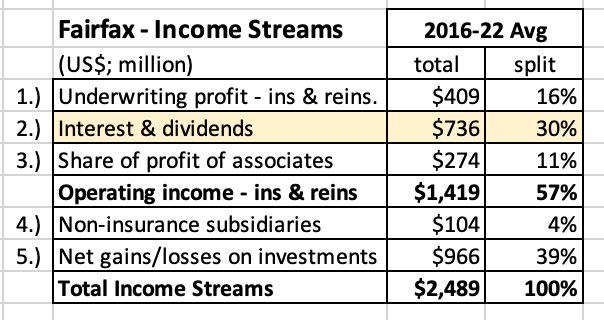

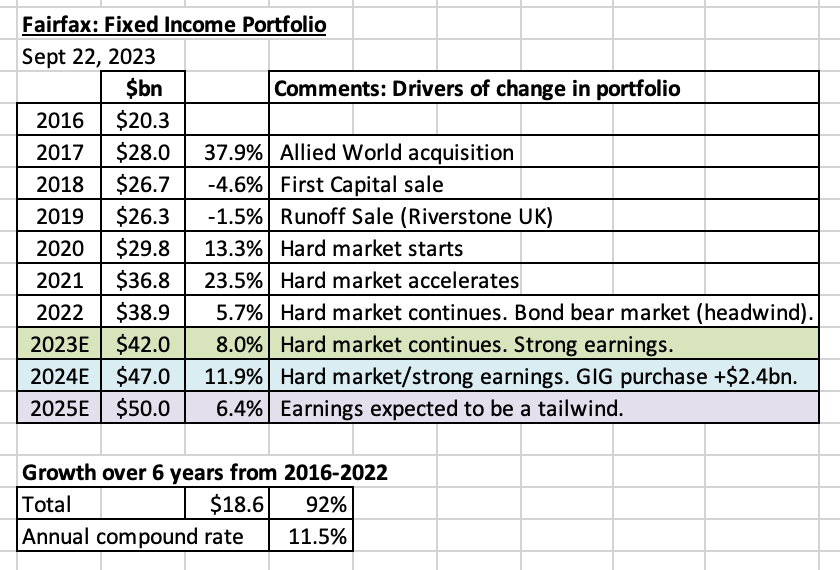

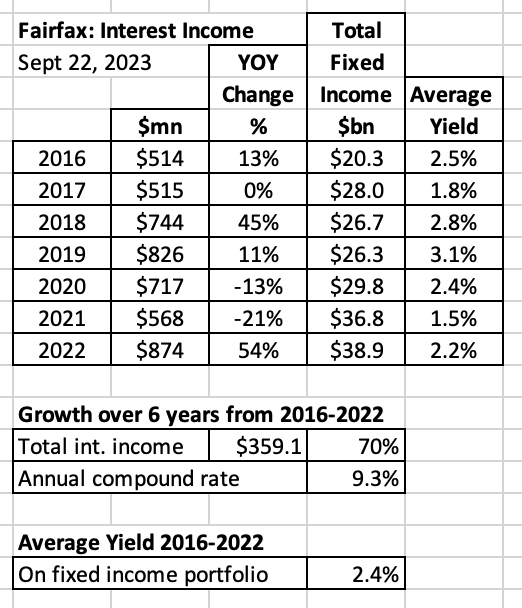

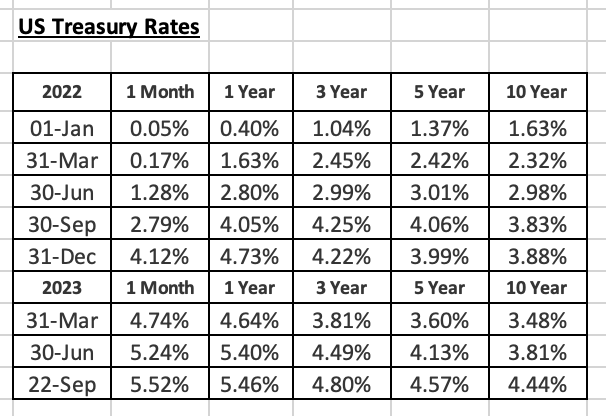

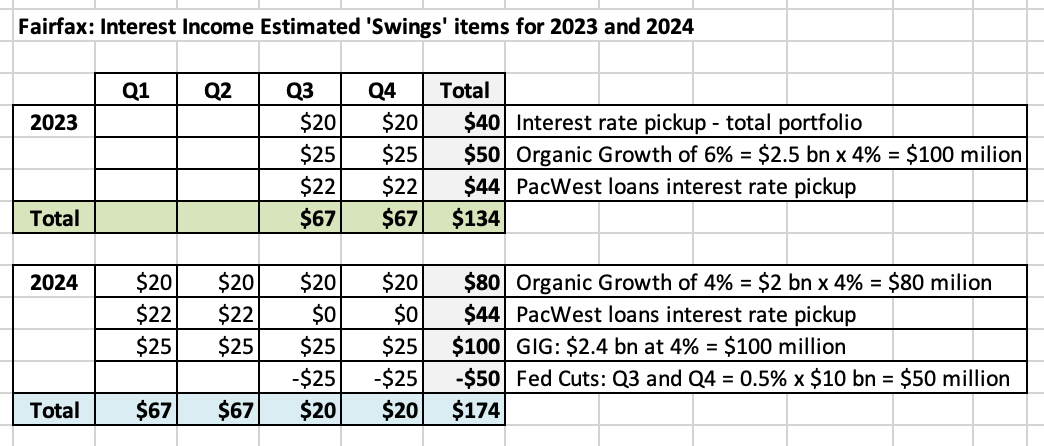

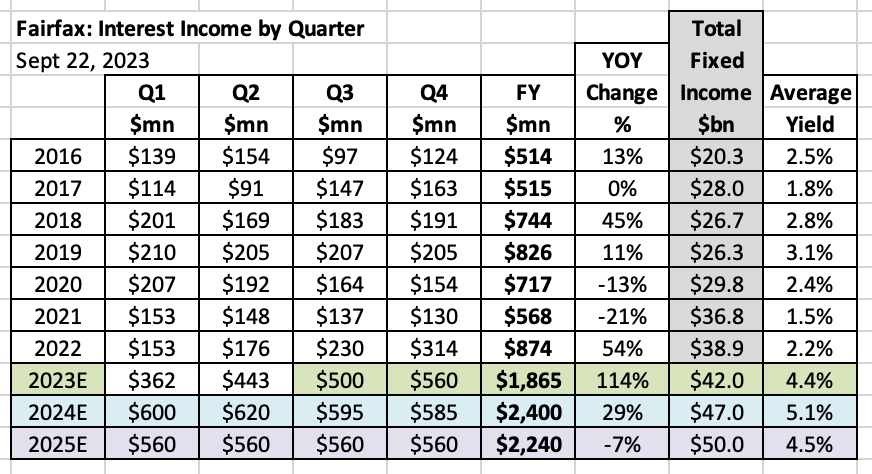

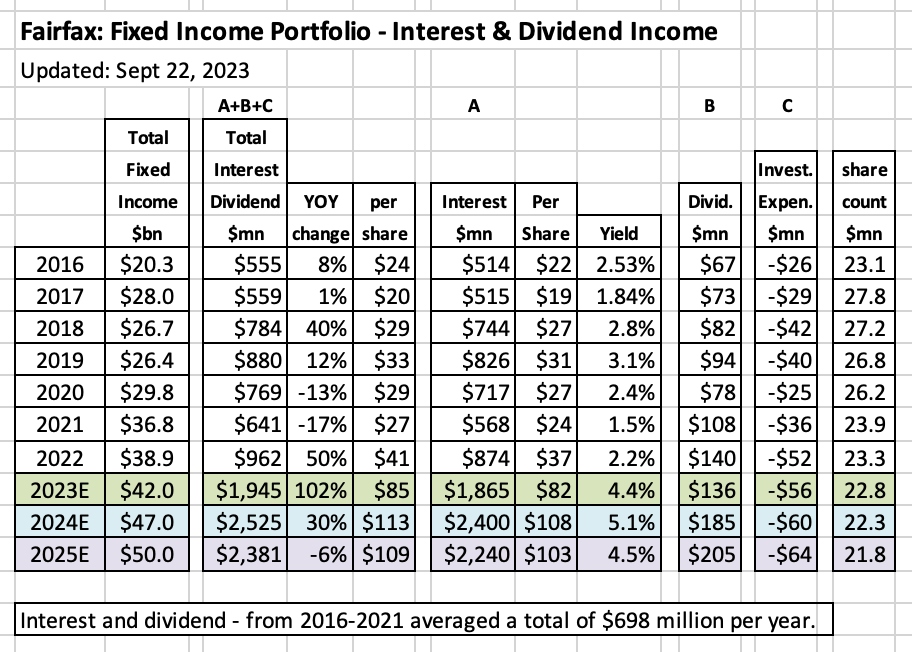

2023 Interest and Dividend Income - Earnings Update The key to forecasting is getting the ‘big rocks’ right. From an earnings perspective, there is no more important item to Fairfax today than interest and dividend income. From 2016-2022, this one ‘bucket’ represented a total of about 30% of Fairfax’s various income streams. With ‘higher for longer’ increasingly becoming the new reality for interest rates, interest and dividend income will likely increase in the near term to represent close to 40% of Fairfax’s various income streams. If we can get can get our estimates for this part of earnings modelled properly we should be well on our way to coming up with a quality earnings estimate for the company as a whole. Interest and dividend income is quite simple. It is relatively easy to calculate. It is usually not very volatile quarter to quarter. And it is pretty predictable, looking out a couple of years. This is why interest and dividend income is considered the highest quality source of earnings for an insurance company. Bottom line, interest and dividend income is important to Fairfax (and investors) because of its size, growth and its quality. Interest and dividend income - components Fairfax reports ‘interest and dividend income’ as a line item on its Consolidated Statement of Income. It is made up of three parts: Interest income: received from the fixed income portfolio (cash, short term investments, bonds, derivatives and other invested assets) Dividends: received from equity portfolio (common and preferred stocks) Investment expenses: paid to Hamblin Watsa When looking at ‘interest and dividends’ for Fairfax, dividends now represent less than 10% of the total. Interest income represents more than 90% of the total, so this is what we are going to focus on. Before we do the deep dive on interest income at Fairfax, let’s step back a look at the big picture. ————— What did we learn in financial markets this week? Like a splash of cold water to the face, financial markets are waking up to the likelihood that interest rates are not coming down any time soon. At the longer end of the curve, despite the big move that has happened over the past month, bond yields look like they could be headed even higher. What is ‘higher for longer?’ Higher for longer is the realization from financial markets that the Fed will likely need to keep interest rates elevated well into 2024. The Fed met this week and they delivered this message loud and clear. US economic growth continues to surprise to the upside. Employment is strong. Oil is back over $90. Although it has come down, inflation remains stubbornly high. Further out on the curve, bond yields have reached new cycle (16 year) highs. Financial markets are likely saying they don’t think higher interest rates are going to cause a recession - the economy can handle higher interest rates. The current supply / demand situation also suggests rates further out on the curve might go even higher: issuance (supply) of longer dated treasuries has increased while demand remains muted and this has pushed prices lower (and yields higher). This supply/demand dynamic is expected to persist in 2H 2023. What were financial markets thinking at the end of 2022? At the end of 2022, financial markets were expecting a recession in 2023. And it was expected the Fed would be cutting the Fed funds rate by 100 basis points in 2H 2023. Financial markets were completely wrong in December 2022. Today, they are now expecting Fed fund rate to peak near 5.5% in January 2024. And from there to slowly drift a little lower but to still be over 5% in July of 2024. Yes, financial markets could be wrong again. Bottom line, ‘higher for longer’ appears to be what has been getting priced into financial markets in recent weeks. Source: https://x.com/asif_h_abdullah?s=21 What does all this mean for Fairfax? ‘Higher for longer’ is a big deal for Fairfax. They have a $40 billion fixed income portfolio. As we discussed, interest and dividend income is already the largest driver of earnings for Fairfax. So an already big number is going to get even bigger. The fixed income portfolio of Fairfax has a very short average duration of 2.4 years at June 30, 2023. This means a significant amount of their portfolio continues to mature each quarter. Compared to all other P&C insurers (not named WR Berkley - who is also at 2.4 years), Fairfax is able to reinvest a significant portion of their fixed income portfolio at still increasing interest rates. This means the quarterly run rate for interest income will likely continue to move meaningfully higher in the coming quarters. As a result of ‘higher for longer,’ estimates for interest and dividend income for Fairfax will need to be updated - yes, it is going higher. And given the importance of interest and dividends, this means earnings estimates will also need to go higher. Analysts are going to feel like they are living their own version of the movie Groundhog Day. However, we will not wait until Fairfax reports Q3 results to ‘discover’ what we already largely know - we are going to update our forecast for interest and dividend income in remainder of this post. —————- Interest Income - a deep dive Two items drive interest income: The size of the fixed income portfolio The average yield earned on the investments held in the portfolio How big is the fixed income portfolio at Fairfax? The fixed income portfolio at Fairfax increased in size from $20.3 billion in 2016 to $38.9 billion in 2022. The total increase was 92% and the annual compound growth rate was 11.5%. My forecast is for the size of the fixed income portfolio to: increase 8% in 2023 to $42 billion. This will be driven by growth in premiums from the continuing hard market. It will also be driven by earnings, some of which will likely be reinvested in fixed income securities. The continuing bear market in longer dated bonds is a small headwind (as the value of these securities fall). increase 12% in 2024 to $47 billion. Similar to 2023, this will be driven by the hard market and growth in earnings. The closing of the GIG acquisition will add $2.4 billion to fixed income portfolio. This may happen in Q4 of 2023. increase 6.4% in 2025 to $50 billion. This is a very rough number. Strong earnings are expected to be a tailwind. We will fine tune this estimate when we get into 2024 as we get more information. Bottom line, we are seeing strong growth in the size of the fixed income portfolio at Fairfax and this should continue moving forward. How much did Fairfax earn on its fixed income portfolio? A look back. Total interest income at Fairfax increased from $514 million in 2016 to $874 million in 2022. The total increase was 70% and the annual compound growth rate was 9.3%. The average yield on the fixed income portfolio from 2016-2022 was 2.4%. Yes, that is a low number. From 2016, Fairfax has been positioned very conservatively with their fixed income portfolio (high quality and low duration). Green shoots: in 2022, interest income was $874 million, an increase of 54% over 2021. This was a new record for Fairfax. Active management matters again - duration and credit quality One of their best investment decisions ever: in Q4, 2021 Fairfax shortened the average duration of their fixed income portfolio to 1.2 years. They also shifted to holding mostly government bonds. Of note, in Q4 of 2021, Fairfax sold $5.2 billion in corporate bonds at a yield of 1% and realized a $253 million gain (these bonds were purchased in March/April of 2020 when credit spreads blew out due to covid). And in 2022, the fed moved to aggressively moved to increase interest rates which unleashed hell on bond (and stock) markets. Of course, with their fixed income portfolio sitting at 1.2 years average duration, Fairfax avoided billions in losses on their fixed income portfolio. This positioning also allowed Fairfax to quickly benefit from much higher interest rates. Interest income bottomed out in Q4 2021 and has been relentlessly moving higher every quarter since then (more on this below). In 2022 Fairfax began extending duration to 1.6 years. And in 1H 2023 average duration has been increased further to 2.4 years. This is locking in higher rates for years into the future. ‘Higher for longer,’ with yields on longer dated treasuries hitting 16 year highs this month, Fairfax has a wonderful opportunity to extend duration even more. This will be something to watch for when Fairfax reports Q3 results. Quality management: lead by Brian Bradstreet, the fixed income team at Fairfax/Hamblin Watsa has been executing exceptionally well in recent years. This is not surprising - their track record over the long term has been outstanding. Another misunderstood and under appreciated part of Fairfax. The move in US treasuries over the past 7 quarters has been epic - and that is not hyperbole. Fun thought exercise Can we estimate how much of Fairfax’s $40 billion fixed income portfolio is ‘maturing’ each quarter and what the pickup in yield is when the proceeds are reinvested at todays much higher rates? Let’s assume $2.5 billion is maturing each quarter and the yield pickup is 2%. If close to accurate, this suggest interest income should continue to grow at $50 million each quarter over the prior quarters number. And this should continue for the next couple of quarters. What to board members think? Too high? Forecast for fixed income for 2023, 2024 and 2025 Given the importance of interest income to the Fairfax story we are going to get into the weeds a little bit more. Because so much has changed so fast over the past 24 months, historical numbers are pretty much useless to use on their own to estimate interest income. This is why most analysts have been so wrong with their earnings estimates for Fairfax over the past year. They are primarily using historical numbers to estimate interest income. In another couple of quarters, once interest income ‘normalizes’ then the analysts earnings estimates will better reflect reality. To build an accurate forecast for interest income we do need to start with historical numbers, as they provide a valuable baseline. But we need to use quarterly numbers. And then we need to overlay the new news (I call these ’swings’): interest rate pickup - for bonds maturing each quarter which are then reinvested at much higher rates. Let’s assume $20 million per quarter. Likely way low. Is $50 million more accurate as per my numbers above? To be conservative let’s assume there is no interest rate pickup in 2024; my guess is there will be some in Q1. organic growth - this is growing the size of fixed income portfolio. Let’s assume an increase in the size of the fixed income portfolio of $2.5 billion x 4% = $100 million per year = $25 million per quarter. new business - interest rate pickup: PacWest loans are expected to deliver a 10% total return. Some of this gain will be price. It seems reasonable to assume the yield pickup will be about 4% or 5% = $90 million per year = $22 million per quarter, starting in Q3, 2023. new business - increase in fixed income portfolio: when it closes the GIG acquisition will add another $2.4 billion to the fixed income portfolio. Let’s assume an interest rate of 4% = $100 million per year = $25 million per quarter. Let’s start this in Q1 2024. If the deal closes in Q4, as expected, we can move this forward a quarter when we do out next update. Fed rate cuts - let’s build in 2 rate cuts from the Fed in 2H 2024. Let’s assume this cut impacts $10 billion by 0.5% = $50 million annual decline = $12.5 million per quarter. To be conservative lets go with a decline of $25 million per quarter. The key here is to try and understand what the largest drivers of change are and to do a very rough estimate of the impact. Bottom line, doing our estimate by quarter should add a lot of accuracy to our quarterly and annual estimates. Step 1: Understand interest income swings by quarter Below I have tried to capture the big ‘swings’ that will impact interest income moving forward. By breaking down the impact by quarter we now have a rough number we can add to our baseline numbers. Please note, it is important to get these estimates approximately right. Some will be high. Other will be low. Collectively, they will should be close. Step 2: Build our annual forecast by quarter Together with our baseline (historical) numbers, we used the ’swings’ above to help us come up with our new forecasts for the remainder of 2023 and for 2024 and 2025. Note, i did take my ‘swings’ numbers above down a little for each quarter - to add some conservatism. My new forecast for interest income for Fairfax is: $1.865 billion in 2023, a YOY increase of 114% $2.4 billion in 2024, a YOY increase of 29% $2.24 billion in 2025, or a YOY decline of 7% This results is a portfolio yield of: 4.4% in 2023 5.1% in 2024 4.5% in 2025 The total number of $2.4 billion for 2024 looks high (just because it IS a huge number). But the portfolio yield of 5.1% looks reasonable (remember the Kennedy Wilson portfolio is about $4 billion and it is yielding around 8%). But these numbers are where my logic and math takes me so that is what I will go with for now. As new information comes in (or I discover errors in data to logic) I will update my forecasts. Important: this is my first stab as this kind of detail. So there will be errors. Please let me know where my logic is wrong so I can make the estimate better over time. Discussing/debating the assumptions/logic with others on the board is when the learning really happens. Thank you in advance Interest and Dividend Income Coming full circle, let’s now overlay our new estimate for interest income into our estimate for interest and dividend income. My new forecast for interest and dividend income for Fairfax is: $1.945 billion in 2023, a YOY increase of 102% $2.525 billion in 2024, a YOY increase of 30% $2.381 billion in 2025, or a YOY decline of 6% Conclusion Interest and dividend income is the most important income stream for Fairfax. It is poised to increase more than 100% in 2023 and another 30% in 2024. The driver of this increase is the fixed income portfolio. double in size: the total fixed income portfolio more than doubled in size the past 8 years from $20.3 billion in 2016 to an estimated $42 billion in 2023. double in yield: The yield on the fixed income portfolio averaged 2.4% from 2016-2022. It is estimated to come in at 4.4% in 2023 and 5.1% in 2024. A double in size combined with a double in yield is nuts. Investors are getting served up a double-double with Fairfax’s fixed income portfolio (that line will only make sense to Tim’s coffee drinkers). The story gets better. Fairfax is positioned perfectly to benefit from ‘higher for longer.’ Fairfax has an opportunity today to lengthen duration. This would then lock high interest income into 2025 and 2026. What about corporates? Fairfax has the majority of its fixed income portfolio invested in safe but lower yielding government bonds today. What if they start to move out on the curve AND at the same time shift more into corporates. That would likely result in a yield pickup of around 1.5% or 2% over governments bonds. So for all of you out there who are thinking that interest and dividend income will peak out at $2.5 billion in 2024… maybe not. ————— Dividends Dividends have increased from $80 million in 2014 to $140 million in 2022, a compound increase of 7.2% per year over 8 years. Dividends should continue to increase in the future. Eurobank would like to start paying a dividend in 2024. They have discussed 25% as a reasonable payout ratio. If this happens, Fairfax could see dividends increase by up to $75 million just from Eurobank. That would be a 50% increase to dividends. Regardless, we should see this continue to increase in the future as Fairfax grows its equity holdings and as existing holdings increase their payouts. ————— Where do i go to learn about where interest rates might be going? I follow a guy named Joseph Wang - The Fed Guy. I have been following Joseph for more than a year and he has been remarkably accurate with his projections for interest rates. Just as importantly, Joseph is a great educator. He lays out his thinking on interest rates (and the Fed meeting last week) in his most recent podcast on September 23.

-

Strictly from a financial perspective, we all should be praying for a couple of bad hurricanes. Small hit to short term results. But it would likely extend the hard market another year of two - resulting in higher for longer profits (price increases and better terms and conditions). I think much of what people are discounting into their models when valuing Fairfax is too pessimistic and one sided. Because each risk has a corresponding opportunity. Discounting the risk and not adding back some of the opportunity is not being conservative. That makes no sense to me.

-

@Haryana yes, my July 11 comments was discussing my holdings of Fairfax and Fairfax India. At the time i was 100% Fairfax and 0% Fairfax India. And yes, at the time, i had other investments. Sorry for the confusion.

-

@Haryana to be clear, i did not move from zero to 30% cash. I always have a cash balance that i flex up and down depending on the opportunity set. My ‘way overweight’ position in Fairfax has not changed the past couple of months - I continue to think the stock is still wicked cheap (despite hitting all times highs). ————— Posted on Tuesday: “Cash. It has been a great year. Time to get more defensive. Lock in gains. Back up to 30% cash. Get paid close to 5% risk free to sit in the weeds and wait and see what Mr Market pukes up next. The move higher in bond yields is what i am watching right now. How high can they go?” “i am not turning bearish. Or bullish.”

-

When it comes to pay, you get what you are able to negotiate. If you have leverage, you earn more. If you have no leverage you earn less. From my perspective, there is no ‘right’ or ‘wrong’ amount. In a tighter labour market, like today, it makes sense labour has a little more leverage (in general) and therefore will attempt to extract more. No idea how it all plays out.

-

Balanced summary of how messed up Canadian / Indian relationship is. - https://www.theglobeandmail.com/opinion/article-the-real-reasons-canadas-relationship-with-india-is-broken/#comments

-

This graph illustrates beautifully the difference in the impact of rising interest rates on home owners with a mortgage in Canada and the US. Canadian mortgage holders are being impacted much more quickly than those in the US. And that makes perfect sense given borrowers here have interest rates that are variable or fixed for only 1 year, 2 year, 3year, 4 year or 5 year (mortgages can be amortized for up to 30 years). Current mortgage rates in Canada are now about 6.2% for a 5 year and higher (for shorter terms). So every year about 20% of borrowers in Canada are now resetting to 6.2% or higher from their old rate which is probably around 3% = double the interest cost. Hard to see how this does not have an impact on consumer spending / the broader economy over time. The key is how long interest rates stay elevated. On that front, inflation surprised everyone and ticked higher again a couple of days ago. Source: https://x.com/asif_h_abdullah?s=21

-

@Sweet i am not sure the names you are speaking of. Note, i am after 15-20% per year returns over the next year in the sector (not 100% in 12-24 month type returns). I follow Suncor closely. With their windfall profits from energy the past 2 years they have been: 1.) paying down debt aggressively. 2.) buying back stock aggressively (i think 6 or 7% of shares outstanding per year) at very low prices. 3.) paying a good dividend (4.4% yield today). In another 6 months or so they will likely hit their net debt target. At that point, most of the free cash flow will go to share buybacks and probably a higher dividend The company recently announced a 10% reduction in total workforce that will save it about $400 million per year. The new CEO is laser focussed on making Suncor a simpler, more focussed company. He also looks to be VERY shareholder friendly. Bottom line, i think there are some pretty compelling opportunities in the energy sector (still). Not as cheap as 2020. But the comlanies are in much better shape (their balance sheets). And the outlook for energy is also much better - oil is at $90 and my guess is it goes higher from here. OPEC (Saudi’s) appear back in control of the oil market. The US has played its SPR card. I’m not a conspiracy guy… but the Saudi’s and Biden/Democtrats clearly hate each other. What will higher oil prices do you Biden’s chances of reelection in 2024? I think the Saudi’s are VERY motivated to keep prices high for the next year. Russia probably as well - want to get the upper hand in the Ukraine war? Get Trump elected. Geopolitics sometimes matters.

-

You can’t make this stuff up. We haven’t even reached peak coal usage yet. Peak oil or gas? Global Coal Use Set to Stay at Record Levels This Year, IEA Says “Lower natural gas prices in the US are also encouraging a move away from coal, the IEA’s report said.” https://www.bloomberg.com/news/articles/2023-07-27/global-coal-use-set-to-stay-at-record-levels-this-year-iea-says

-

This post was the first made on this thread back in 2020. @james22 freaking brilliant call. Just as relevant today? Eric Nutall is not my favourite oil analyst… but i do like his chart (i prefer Arjun Murti and Josh Young).

-

I heard this on a podcast a while back (not sure which one). I did a quick search online and found the following article: “For a typical wood-frame condo development in Vancouver, the fees represent 29.25 per cent of the unit’s final purchase price.” - https://biv.com/article/2023/07/government-fees-inflate-risk-uncertainty-bc-builders#:~:text=Municipal fees account for the,is attributed to regional fees. “Government fees imposed on a project can range from those that cover infrastructure-related needs (DCCs and development cost levies), community contributions that will offset density (CACs), a federal goods and service tax (GST), building and development permits, property transfer taxes and the speculation and vacancy tax. “ In Vancouver, there is also the additional empty homes tax and a public art fee, according to a February 2023 Urban Development Institute, Pacific Region report. “The total cost of government fees represents 32.72 per cent of rent that the end-user pays in a typical wood-frame, purpose-built rental development in Vancouver. “Municipal fees account for the majority of this total at 44.27 per cent; federal and provincial fees account for 28.39 and 24.15 per cent, respectively. The remaining 3.18 per cent is attributed to regional fees. For a typical wood-frame condo development in Vancouver, the fees represent 29.25 per cent of the unit’s final purchase price.”

-

My guess is the Canadian big banks will be fine. Unless we have a bit of a crash in the housing market (driven by economic recession - and an increase in unemployment). Not likely, from my perspective but possible. I think the big Canadian banks are cheap. They are a regulated oligopoly - they have morphed into a utility type of investment. For example, the returns for investors (as a basket) have tracked close to the dividend yield for the past 5 years. At current prices (20% off highs) probably a decent entry point - unless Canada has a hard landing like the US in 2008. Part of the challenge today is the data on housing is very poor. The lending process is a mess. The pandemic turned everything on its head. The government (federal and provincial) have been asleep at the wheel in terms of spike of permanent / nonpermanent residents. Taxes (as a % of selling price) on a new build has gone from 10% eight years ago to 30% today (didn’t matter when prices were going up 8% per year. Zoning (controlled my minipitailites) is archaic and driven by NIMBY - not in my backyard. Oh, and interest rates are about 6.25% and new buyers have to have the income to qualify at and 8.25% rate (called a stress test). The average price of a detached house in greater Vancouver is $2.4 million. The average price for a condo/apartment is $800,000. The average salary in Vancouver is $69,000 (25% of this will go to income taxes). At a 8.25% qualifying mortgage rate the math doesn’t work (my attempt at humour).

-

@SharperDingaan you highlight the thing i have never understood. How can Canada have a housing crisis (driven partly by lack of supply) when it was in a multiyear construction boom of epic proportions? I hope that you are right and there are a lot of units sitting empty that will now be put now to productive use.

-

@John Hjorth despite my post above, i am optomistic. The fact we have a crisis (in Vancouver/Toronto) the politicians now have the cover they need to do what needs to be done. Vancouver had lots of land… we just need to densify the downtown areas (imagine if Manhattan or downtown Copenhagen only allowed single family homes to be built with big yards?). And we are beginning to see real change and my guess is we are just getting started: - zoning rules have changed in Vancouver from a single family bias to a multi family bias. - Federal and provincial governments are implementing new policies to try and stimulate supply of multifamily buildings @SharperDingaan i never thought about the supply of workers shifting from building condos to building affordable multifamily units (being encouraged by governments). perhaps the pivot can happen a little more quickly than i initially thought. Address is also from the demand side: This is the quicker way to address the problem. My guess is we also will get a slowdown in the number of foreign students/immigration/foreign workers. As better information/stats becomes available the federal/provincial governments are going to be forced to do something - or they will likely get hammered in the next election. Who loses? My guess is the people who have too much debt. So anyone who bought in the past 5 years and are carrying a big mortgage. Maybe 10% of homeowners today, so in the big scheme of things not a big number. The fundamental issue is prices are simply too high. IF interest rates stay elevated, my guess is we will see price slowly come down (over a couple of years. Maybe 10 or 15% in nominal terms. Factor in inflation and you get a 25% correction in real terms over a 3 year period. Nothing catastrophic. The market will find a new equilibrium.

-

I think the last true hard market in PC insurance was around 2004. That suggests the insurance cycle can run in a 20 year cycle from hard to soft and back to a hard market. At the same time, you also have an interest rate cycle. Interest rates peaked in 1980 and the trough was 2020. That 1/2 cycle in rates was 40 years. What does this tell us about how to value Fairfax today? I am pretty sure the two are linked. But i have no idea how to overlay that linkage to how i value Fairfax. Perhaps management is the key. Good management teams will usually thrive over time. Bad management teams will usually struggle/fail. And cycles will happen like they always do.

-

My understanding is the move in bond yields the past month or so is being driven primarily by supply / demand dynamics. Supply is vastly outstripping demand. And I think this is expected to continue the rest of this year. Higher interest rates. Oil over $90. Something to monitor... Historically speaking, if this lasts for any length of time, it usually starts to create some stress. And I am in Canada, and high interest rates are a completely different animal here - this is like impacting my assessment big time.

-

Cash. It has been a great year. Time to get more defensive. Lock in gains. Back up to 30% cash. Get paid close to 5% risk free to sit in the weeds and wait and see what Mr Market pukes up next. The move higher in bond yields is what i am watching right now. How high can they go? i am not turning bearish. Or bullish.

-

@Crip1 well said. What are your thoughts about the interplay between underwriting profit and investment returns? Are they linked? Can we put numbers to each? At the end of the day, publicly traded P/C insurance companies need to make a 8-10% ROE over time. The CEO’s want to hit their bonus payouts and also keep their jobs. As a result, i think CR and investment results are linked. Let’s assume fixed income yields stay at the elevated levels we are seeing today. Can a 100 CR get a company to a 10% ROE? Maybe Fairfax today because of the leverage they have with float. But i think most P&C insurers would struggle to deliver an ROE of close to 10%. Given most have taken a capital hit on their fixed income portfolios due to rising interest rates i just don’t see a big or rapid turn to a soft insurance market. Bond yields are still too low. And insurance companies lots of near term risks they need to build into their models when pricing (elevated catastrophe losses, reinsurance costs, inflation etc).

-

@Munger_Disciple to be clear, i may have a lot of conviction in my estimate for 2023. I have never said any estimate is ‘in the bag’. That, of course would be idiotic. As we move to 2024, the estimate gets less clear. 2025 even less. And i don’t even attempt to forecast 2026 as there are too many moving parts. You have built an estimate… i have built an estimate. We both have provided our logic. Discussing the build is how we learn. I appreciate the opportunity to debate. ————— Below is what i said in my response to you two days ago What is the major flaw with my estimates? Am I being way too optimistic? Perhaps. But my problem the past 3 years is I have been way too pessimistic with my forecasts - they have consistently been way too low. I lean heavily on what I think i know today. I only go out max 3 years with my forecasts. And I admit my year-3 forecast is not as clear as my year-1. As new news comes in I update my forecasts. Quickly. If bad news starts to pour in I will take down my estimates. Same if the opposite happens and good news comes in - I'll take up my estimate. So far, I have only been making upward revisions. Another flaw with my forecasts is I do not incorporate compounding in very well. So my estimates in 2024 and 2025 for asset growth is too low. Higher assets likely means higher earnings. This is a big reason I think my forecasts are mildly conservative (overall).

-

When it comes to housing, Canada is facing the perfect storm. 1.) First we blew a housing bubble that is probably bigger than the the US housing bubble that popped in 2008. So we have crazy high prices. 2.) All mortgage rates here are variable, with crazy low teaser rates. Those teaser rates are now resetting, with most resetting in 2024 and 2025. The parallels with US housing in 2006-2007 are frightening. 3.) Bubble high real estate prices + 6% mortgage rates = $3,000/month to rent a one bedroom. That is the math for a new investor. Rents on new rental units coming to market have doubled in the past 2 years. 3.) Rents in Vancouver are controlled by the government. Same for older housing stock in Toronto. So in the same building two of the exact same units can rent for $1,500/month and $3,000/month. So no renters can afford to move today - your rent is going to double if you do. The rental market is effectively frozen. 4.) Supply always has been tight and vacancy rates in Vancouver and Toronto have always been extremely low (2% or less). 5.) Demand - the number of international students has increased in recent years from a run rate of 200,000 per year to about 800,000 today. The net add has been 600,000. Why the increase? International students pay up to 6x the amount for tuition compared to a Canadian student. International students are driving the budgets of universities now. The provincial/federal governments usually fund education but international students have now become the golden goose for most institutions. Provinces and feds love it because they can spend $ on other priorities. Of course, no one asked if we have the housing to support an increase of 600,000 people. - the Federal government also decided recently to boost immigration to 500,000 per year. GDP/capita has been falling for years in Canada. Fix? More people. Total GDP grows (easy way to paper over the problems under the surface). - temporary foreign workers. We also have a shortage of workers so we have also been bringing in 200,00 or so foreign workers each year. When you add the three together… Stats Canada just admitted they have undercounted the number of new people coming to Canada by 1 million people. 6.) Supply. The Bank of Canada is trying to slow the economy to get inflation under control. How? Higher interest rates. This lowers activity in interest rate sensitive parts of the economy, primarily housing. And it is working. New building permits are down a lot. New construction is slowing. Fewer units will be coming to market looking out a couple of years. So we have a really messed up situation. Market was already super tight. Supply is constrained. Demand is through the roof and growing - the governments are not changing any of the rules (students, immigration, foreign workers) - at least as of today. Housing looks like it is going to be the dominant issue in this country moving forward.

-

Below are a few quotes from the article. The tide is going out in Canadian real estate and we are beginning to understand who has been swimming naked. The additional problem for real estate investors in Vancouver is rent increases are dictated by the provincial government (2% in 2023, 1.5% in 2022). Older housing stock in Toronto is rent controlled (i think). If rates stay high (which is what it looks like) a lot of ‘investors’ in Vancouver/Toronto are going to learn that leverage can be a bitch: 1.) much higher interest rates - variable rate mortgage 2.) falling housing prices 3.) limited ability to increase rents “The problem facing Canada’s real estate investors, whether they’re buying a new property or they have a floating-rate mortgage on one they already own, is that the math simply doesn’t work at today’s interest rates. Modeling by the Bank of Montreal shows that in Toronto, anyone using a mortgage with a standard 20% down payment to buy a rental property at today’s prices, charging today’s rents, would be signing up to lose about C$1,000 (roughly $738) each month. These cashflow calculations have been negative since 2016, but investors were generally willing to overlook that because part of those payments were paying down the mortgage’s principal, thus building equity in the investment. But in the last year, the cashflows have gone so deeply negative, it even offsets those equity gains, the BMO modeling shows.“ “Rental amounts aren’t going up fast enough to cover for the huge increase in interest rates,” he said. “Effectively what we do is we flush out all the people who are holding their breath. That’s what we’re starting to see here.”

-

For those who are looking to follow oil more closely the podcast below is done daily with different guests. Some are quite good. I wonder if oil is going to be the big story for the rest of 2023. If oil keeps going higher and busts through $100 it is going to have significant consequences on some things. Like inflation. And interest rates. Higher for longer is looking more and more likely every day. Up here in Canada, i think we might be seeing things starting to crack in the economy due to higher interest rates. We have had a monster housing bubble and everyone here has essentially what is a variable rate mortgage with a teaser rates that all going to reset over the next 30 months. Borrowers are going from 3ish % to over 6% when they renew. A segment of the population is screwed (those who bought high in recent years and have a big mortgage). It is worse for investors (who bought recently). In Vancouver, the rental market is rent controlled. So your mortgage skyrockets higher and the government allows you to increase rent a maximum of 2% in 2022. Housing inventory is starting to move higher in Toronto and Vancouver - this will be something to watch in the coming months. My favourite line in the video below was something like “i got duped by the fallacy of peak oil decades ago. The new fallacy that will be disproven in another decaade? That demand for oil will peak soon.” If you watch the video start at the 7 minute mark…

-

@blakehampton If you haven’t, I would read Chapter 8 of the Intelligent Investor. “Does the current economic situation particularly stand out to you, or is a mass feeling of uncertainty simply inevitable when it comes to markets?” Volatility is your friend. Especially if you are young. I think people in their 40’s are young (in investing years). If you are young you should pray for armageddon. Falling stock markets are a gift. The bigger the decline the better. You buy more with the same amount of dollars. When you are really old, that is when you want strong equity markets. Of course you are not going to be able to time the bottom. My point is, on big declines, find money (bring forward contributions - borrow short term from family etc). Buffett suggests you should buy stocks like you buy groceries - lower prices are better. Training your brain is one of the keys to successful investing. Watch CNBC less. Read @dealraker posts about buy and hold. http://csinvesting.org/wp-content/uploads/2012/07/mr-market-by-ben-graham_final.pdf