Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

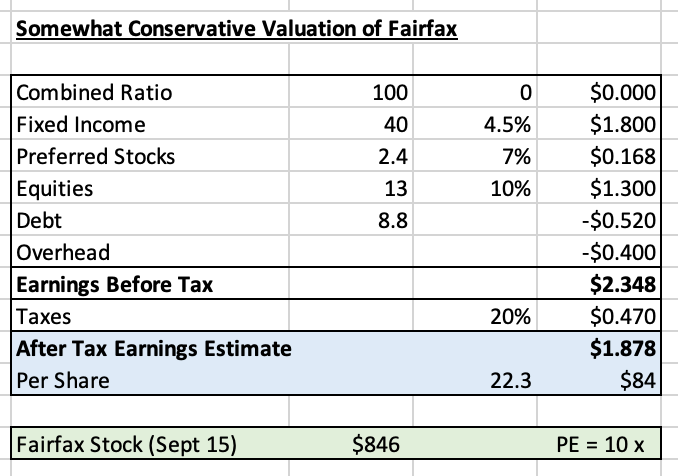

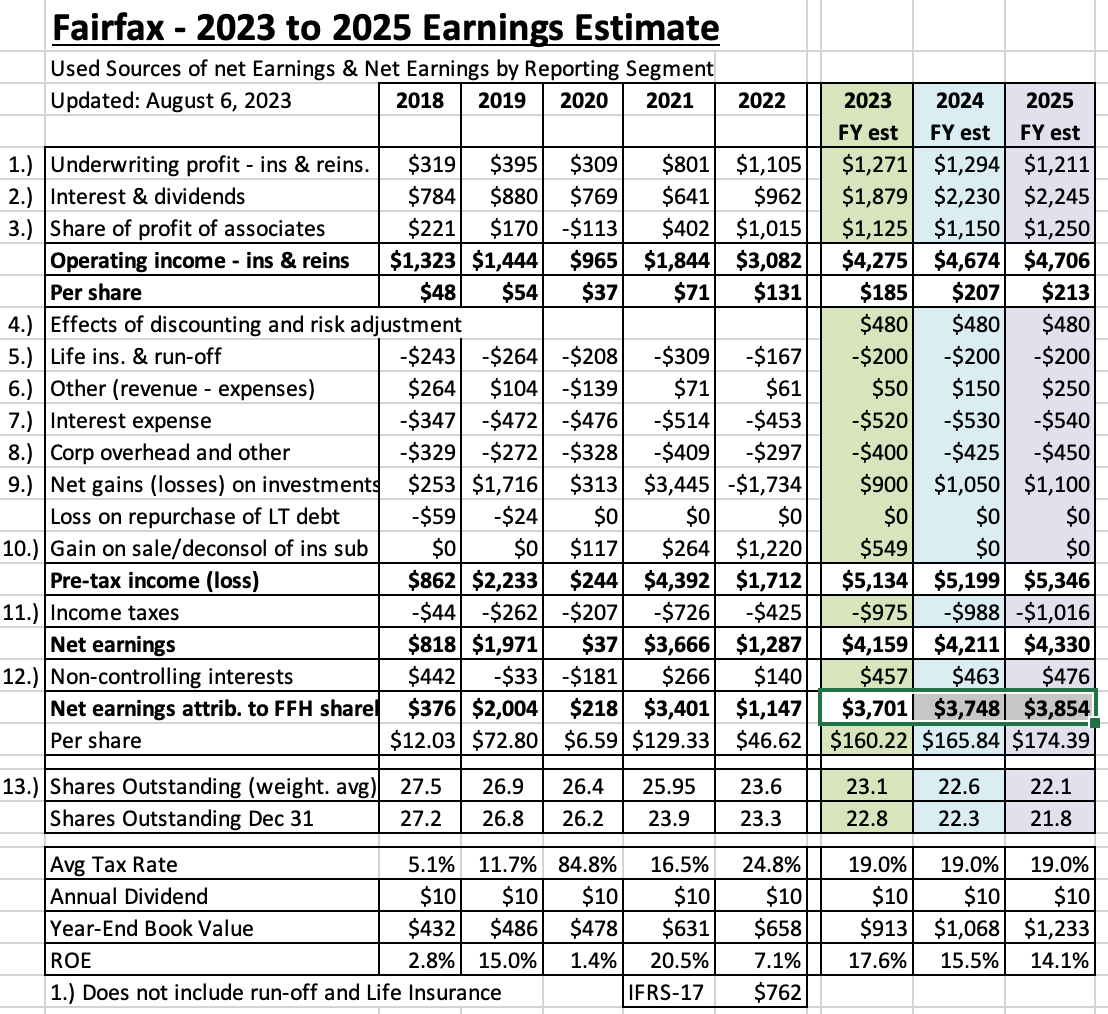

@StubbleJumper Yes, i agree that @Munger_Disciple and i are both coming at this from very different perspectives. But sorry, i can’t reconcile the two estimates - they are simply too far apart. They both can’t be right (or even close). If Fairfax earns $160/share each of the next three years there is no way the shares are worth anything close to $845/share today. Anyways, i love the debate. But time to get some sleep

-

To help investors value a stock, Warren Buffett tells the story of Aesop: "a bird in the hand is worth two in the bush." According to Buffett, investors need to determine 3 things: How many birds are in the bush? When are you going to get them out? How sure are you? The prevailing interest rate is also important: If interest rates are 15%, then two birds out in 5 years makes sense. If interest rates are 3%, then two birds out in 20 years makes sense. ----------- @Munger_Disciple Thanks for taking the time to put together an earnings estimate for Fairfax. It is great to get different perspectives. When I read your estimate above I immediately thought: "two birds in the hand are worth one in the bush." Of course, I know this was not what you are trying to say. But that was my take-away from your estimate. Let me explain. Let's start with your estimate: Now let's pivot to my current estimate for 2023. My current estimate is Fairfax will earn $160/share in 2023. We are almost 9 months into the year. Yes, something bad could happen. But something good could also happen. My view is the tail risks to my forecast (too high or too low) are about equally distributed. So I think $160 is a reasonable number. What about 2024? I am at earnings of $166/share for 2024 and $174 for 2025. I think my 2024 and 2025 estimates are mildly conservative. Let's compare out two numbers: You are at $84/share and I am at $160/share. You are 1/2 of my number. That is a big difference. So what explains the difference? Let's compare our estimates. 1.) Underwriting: Your CR is 100 and mine is 94.5 for 2023 and 95 for 2024. Your rationale: You say Warren Buffett's goal is 100. My rationale: That is where Fairfax is currently tracking (the last 3 years). Yes, we likely are late in the hard market. But everything I read suggests the hard market is likely to continue into 2024. Reinsurance (property cat) just started its hard market. Will Fairfax's CR trend higher in the coming years? Probably. I am modelling 94.5, 95 and 95.5 from 2023-2025. Over time, as I get new information I will adjust accordingly. Bottom line, Fairfax is tracking to earn $1.27 billion in 2023. Taking that to zero today and every year into the future just seems bizarre to me. PS: Warren Buffett also thinks float is better to have than an equal amount of equity. 2.) Fixed Income: $40 billion earning 4.5%. We are pretty close here. The difference is compounding. My guess is the fixed income portfolio will grow in total size at 8-10% per year the next couple of years: Top line growth: increased premiums (currently running at 8%) will grow float GIG acquisition will boost total investments Earnings: 4.5% yield will deliver earnings of $1.8 billion pre tax My point is the $40 billion will likely be $50 billion by the end of 2025. I also think the yield will be closer to 5% in 2024. Bottom line, ignoring the power of compounding gives you a lower number here. 3.) Preferred stock $2.4 billion = $170 million. I don't break out preferred stock as a separate line item. Let's assume we are on the same page here (it is a small number) 4.) Equities/derivatives. You are $13 billion at 10% = $1.3 billion. We are off quite a bit here. My tracker has this bucket with a value of $16.9 billion today. This includes some preferred stock ($850 million). I also value the FFH-TRS at notional ($1.6 billion). For this bucket I am at $2.4 billion for 2024 and growing in future years: Mark to market gains on portfolio of $8 billion = $800 million (10%). The FFH-TRS is driving this bucket (every $100 move in FFH = $200 million). Dividends = tracking around $140 million per year (includes preferred stock) Share of profit of associates on portfolio of $6 billion = tracking around $1.15 billion. Yes, close to 20%. This is a build of the current trend of the companies included in this bucket, driven by Eurobank. Associates - YOY change in fair value vs carrying value = $100 million. Although not captured in book value, this is value creation for shareholders. Operating companies (Recipe, TCI, Dexterra etc) pre-tax earnings: $150 million. Investment gains (sales/revaluation) = $250 million (lumpy) Let's take $170 million off my number to account for preferred stock already counted in 3 above. That brings my equity number to $2.23 billion. What will cause my number to fall by $900 million to your number of $1.3 billion? An economic depression? I think my equity/derivative number is going to grow by 10% per year. Like underwriting, we are miles apart here. 5.) Corporate + Interest expense = $400 + $520. We are the same here. Summary: Two buckets explain most of the difference in our forecasts: Underwriting: you are $1.2 billion below me Return equity/derivative portfolio will deliver: you are $900 million below me It looks to me like you are also assuming Fairfax stops growing today: assets, liabilities, equity. Fairfax will likely grow its assets significantly in the coming years (organic growth + earnings reinvested). Growth in float will also increase liabilities. And shareholders equity will be increasing (earnings). The power of compounding at Fairfax could be significant the next couple of years (larger in size than anything we have seen). My current estimate has Fairfax earning $3.7 billion in 2023 and a total of $11.3 billion 2023-2025. That is more than 50% of current shareholders equity. It is a huge number. This is likely coming in the next 10 quarters (2 have already been delivered) - not the next 10 years. How many birds are in the bush? $3.7 billion per year and growing. When are you going to get them out? One is coming every year (a little plumper). How sure are you? Its in line of sight. Today, Fairfax shareholders currently have one bird firmly in one hand (2022) and the second bird is just about to land in the second hand (2023). The third one is getting ready to take flight. It looks to me like your analysis assumes away 1/2 of the birds - it just pretends they don't exist. Hence my analogy of "two birds in the hand are worth one in the bush" kind of logic. What is the major flaw with my estimates? Am I being way too optimistic? Perhaps. But my problem the past 3 years is I have been way too pessimistic with my forecasts - they have consistently been way too low. I lean heavily on what I think i know today. I only go out max 3 years with my forecasts. And I admit my year-3 forecast is not as clear as my year-1. As new news comes in I update my forecasts. Quickly. If bad news starts to pour in I will take down my estimates. Same if the opposite happens and good news comes in - I'll take up my estimate. So far, I have only been making upward revisions. Another flaw with my forecasts is I do not incorporate compounding in very well. So my estimates in 2024 and 2025 for asset growth is too low. Higher assets likely means higher earnings. This is a big reason I think my forecasts are mildly conservative (overall). 20% growth in ROE is a double in 3.6 years (about). I think Fairfax might be able to do that. Looking out 4 years, a double in shareholders equity should result in much higher earnings - Fairfax's track record with capital allocation has been excellent since 2018. Soft market in insurance? Bear market in stocks? Of course both will happen at some point in the future. Just like they have in the past. And good companies will benefit. And bad companies will fall by the wayside. P/C insurance was in a soft market from 2014-2017. In the last 6 years we have had 3 bear markets in stocks and the biggest bear market ever in bonds. Over the past 3 years Fairfax has thrived. And they didn't have the earnings/cash flow they do now. My guess is Fairfax will be just fine. But I remain open minded.

-

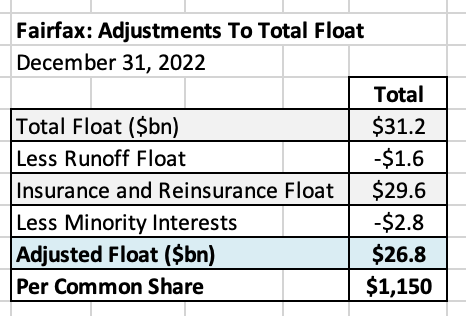

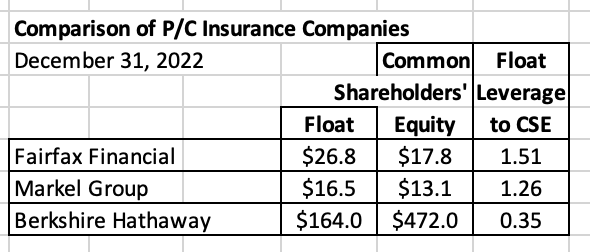

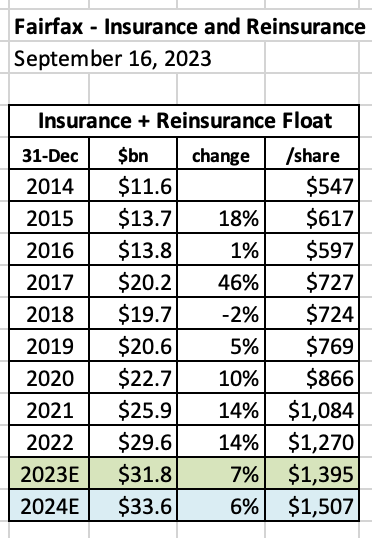

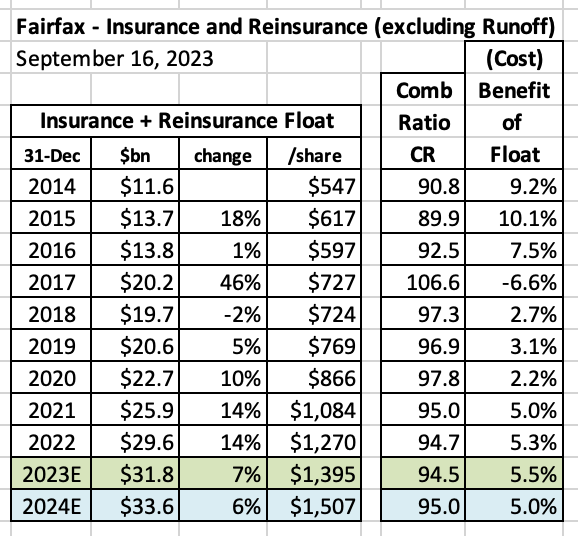

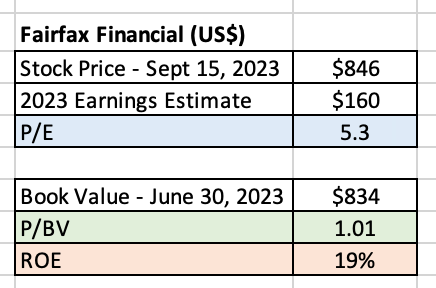

Fairfax Financial and Float - A Deep Dive In my last post i reviewed P/C insurance float, largely through the writings of Warren Buffett - a pretty knowledgeable guy on the subject. In this post we are going to pivot and apply what we learned to Fairfax Financial. Fairfax and Float: Summary of the topics we will explore: A short review of financial leverage Size of float Leverage provided by float Growth of float Cost of float Returns achieved on float Summary ---------- A short review of financial leverage Balance Sheet: Assets = Liabilities + Equity To grow (increase assets) a company can issue a liability like debt (borrow) or equity (shares). Borrowing (a liability) is simply a way to use ‘other peoples money’ to finance growth / business activities. Using borrowed money to grow/invest is a financial strategy referred to as leverage. Why use leverage to grow? To increase the return on equity. If equity stays constant but a firm can grow assets, which in turn grows earning, that will result in higher return on equity. What is the rub? There is a cost to borrow, which is the interest rate charged on the loan. And today, with interest rates elevated, the cost is very high. What does this have to do with P/C insurance companies? P/C insurance companies are unique animals. Through the course of their business operations they generate something called float. Float is the money held by insurance companies when they receive premiums that has not yet been paid out to claimants. Like debt, float is ‘other peoples money’ so it is technically a liability. Like debt, float can be used to purchase investments on the asset side of the balance sheet. The investments purchased with float will then grow total earnings, which results in a higher return on equity for the company. Growing float (L) = growing investments (A) = growing earnings (E) = higher return on equity (ROE). What is the rub? There is a cost to float and it is determined by underwriting (combined ratio). If an insurer is able to generate an underwriting profit over time, the cost of float is free (actually better than free… the ‘cost’ is a benefit). So P/C insurance companies have the ability to use float (leverage) as a low cost way to boost return on equity (ROE). Let’s now see how all of this applies to Fairfax. ---------- How much float does Fairfax have? At December 31, 2022, Fairfax had $31.2 billion in total float. However, to make our analysis more meaningful, we need to make 2 adjustments to this number: Remove float from runoff - Fairfax separates runoff when reporting underwriting results so to be consistent we will remove runoff float from our analysis. So in this post we will only be looking at float for insurance/reinsurance at Fairfax. remove minority interests - small amounts of Allied World, Odyssey, Brit and International are owned by minority shareholders. We also adjust float to account for this. By removing the share of float that accrues to minority shareholders we are left with the amount of float that accrues to Fairfax’s common shareholders, which is really the number we care about. After making the 2 adjustments outlined above, at December 31, 2022, Fairfax had $26.8 billion in float working for common shareholders (i am going to call this ‘adjusted float’ in the remainder of this post.) Adjusted float was $1,150/share. Given the growth in Fairfax’s insurance business in 2023, ‘adjusted float’ today is likely well over $1,200/share. Of interest, Fairfax’s share price closed at $846 on Friday (Sept 15). Now that we know the size of Fairfax’s float, let’s now look at it in relation to Fairfax’s total balance sheet. ---------- What is the leverage provided by Fairfax’s adjusted float? Common shareholders’ equity at Fairfax was $17.8 billion at Dec 31, 2023. As we just learned above, adjusted float is $26.8 billion. Float is 1.5 x bigger than common shareholders’ equity. The leverage is 1.5 times (adjusted float of $26.8 / common shareholders’ equity of $17.8). That means every 1% gain just from float will result in a 1.5% gain in common shareholders’ equity (ROE = 1.5%) So if float delivers an 8% return to Fairfax that will boost common shareholder’s equity by 12% (deliver an ROE = 12%) all by itself. How does Fairfax’s adjusted float and leverage compare to other P/C insurance companies? Fairfax (at 1.51 times) has more leverage from float than Markel (at 1.26 times). For interest, I also included Berkshire Hathaway. Leverage is much smaller for Berkshire Hathaway (at 0.35 times) compared to Fairfax and Markel and this makes sense given the significant growth of BRK’s non-insurance businesses over the years. Note: my float number for Markel above is an estimate. Markel does not provide a float number. Float isn’t even mentioned in their annual report, which seems strange given its importance to the returns of the company. ---------- How much has total float grown in recent years at Fairfax? Please note, in this section we will use the float numbers for insurance/reinsurance (runoff is excluded). However, i did not separate out minority interests. It would have been a lot of work and it wouldn’t have materially changed the conclusions (the growth numbers) - which is what we care about here. The float of insurance/reinsurance at Fairfax has been growing rapidly for many years: 2014 to 2022 (8 years): total float grew 155% or at a compound growth rate of 12.4% per year. 2015-2017 growth was fuelled primarily by acquisitions (Brit, international, Allied World). 2020-2022 growth was fuelled primarily by organic growth (hard insurance market). 2023 and 2024 should see solid growth in float driven by continuation of the hard market and the GIG acquisition. The management team at Fairfax has done a fantastic job of growing float over the past 8 years. And the prospects for continued growth are strong. What is the cost of float? What is the trend? Like borrowing money, float is a liability. Like all leverage (i.e. debt), float can be both good or bad - and this depends on the cost paid over time to hold the float. The ‘cost’ of float is measured by looking at underwriting results and the combined ratio. Fairfax excludes runoff when it reports underwriting results and the combined ratio (CR) so we can use their numbers in this section. Summary: From 2014-2022 the CR averaged 95.7 From 2018-2020 the CR ticked higher and averaged 97.3 From 2021-2022 the CR ticked lower and averaged 94.7 For 2023 my current estimate for the CR is 94.5 Fairfax has consistently earned an underwriting profit on its adjusted float. That is a big deal. It means that is has been able to secure $26.8 billion in adjusted float on very favourable terms. In fact the ‘cost’ of float is better than free - it is a benefit. I know, that is crazy - but it is true. This is why Buffett has said in the past that he views float as being more valuable than a similar amount of equity. That statement is a real mind bender. What is driving the improvement in the combined ratio? My guess is two factors are driving the improvement: The hard market in insurance (that began in Q4, 2019) resulting in higher prices and better terms and conditions. Slow incremental improvement in the quality of Fairfax’s collective insurance businesses (resulting in better underwriting) driven by Andy Barnard and the leaders of the various insurance companies. So float has been growing at 12.4% per year for the past 8 years. And the ‘cost’ has actually been better than free - a ‘benefit’ - over the same time frame. But the story gets even better. Why? Return. ---------- What is the return Fairfax has been earning on its float? Fairfax has $26.8 billion in adjusted float that is fully invested and earning a return for Fairfax shareholders. For reference, the total investment portfolio at Fairfax was about $55.5 billion at Dec 31, 2022. Adjusted float of $26.8 billion represents 48% of total investments. It is significant. In this section we are going to look at Fairfax’s return on total investments (a number we have a fair bit of confidence in). We are not going to try and break out Fairfax’s returns specific to float (which is a part of total investments). Again we are coming at this analysis at a very high level. If we subscribe a lower than average return to float (by assuming it is more skewed to short term fixed income investments) we would then need to attach a much higher return to Fairfax’s non-float investments to get to the correct average number. Instead, we are going to keep our analysis simple and use Fairfax’s average return on total investments as a very rough estimate for what is being earned on adjusted float. From 2018-2022, Fairfax’s return on total investments averaged about 5.1% per year. Not surprisingly, the big drag was the fixed income portfolio. Fairfax’s interest and dividend income (a reasonable proxy for the return on the fixed income portfolio) delivered an average return of about 2.3% from 2014-2022. Today? In 2023, Fairfax is tracking to earn an 8.6% return on its total investment portfolio. That is 69% more than the average of 5.1% of the past 5 years (2018-2022). That is a meaningful increase (big understatement!). What are the biggest drivers of the increase in total return? Interest and dividend income, which is estimated to deliver a return of 4.5% in 2023. My current guess is interest and dividend income will increase to about 5% in 2024, which is more that double its run rate from 2014-2022. Equity markets have also rebounded YTD in 2023. Since 2018, very good capital allocation decisions - with the benefits increasingly showing up in reported results. What about future returns? Fairfax has extended its fixed income portfolio from 1.2 years at Dec 31, 2021 to 2.4 years at June 30, 2023. This locks in higher interest rates for the next couple of years. It seems reasonable to expect the management team at Fairfax to continue to make good capital allocation decisions. Bottom line, Fairfax looks well positioned to continue to deliver strong investment returns moving forward. My current estimate has Fairfax earning a return of more than 8% on its investments in each of 2023, 2024 and 2025. Ok. Let’s try and summarize everything. ---------- What have we learned about Fairfax and its float? ‘Adjusted float’ is $26.8 billion. It has been compounding at better than 10% per year for the past 8 years. ‘Cost’ of float is actually a benefit and the benefit has increased in recent years. The average return Fairfax is earning on its total investments is currently tracking to be 8.6% in 2023, up from an average of 5.1% from 2018-2022. When looking at float, all three of the most important metrics are moving to the benefit of Fairfax and its shareholders. It is large and increasing in size. It is being obtained at a very favourable cost - better than free. And the return being achieved on its investments has spiked and the higher number looks sustainable. So how does float fit into Fairfax’s valuation today? This is where things get interesting. Fairfax’s stock is trading today at $846 which is about the same as book value ($834 at June 30, 2023). Mr. Market is saying that Fairfax is worth a little more than book value = common shareholder’s equity = $19.4 billion at June 30, 2023. Mr Market appears to be assigning little value to the adjusted float that Fairfax has of $26.8 billion ($1,150/share) at Dec 31, 2022. Assigning a very low value to adjusted float might have made some sense when interest rates were very low. But in the current environment, where interest rates are high and likely to stay high, this makes no sense. This perhaps explains why Fairfax trades at a PE of 5.3 x 2023E earnings (my current estimate of $160/share). Perhaps Mr Market does not yet appreciate how large the increase in earnings from adjusted float is likely to be in the coming year(s) and the impact that will have on ROE at Fairfax (at 1.5 x leverage). What did Fairfax have to say about float in its most recent annual report? Fairfax 2022AR: “For our stock price to match our book value’s compound rate of 17.8%, our stock price in Canadian dollars should be $1,375. And our intrinsic value exceeds book value, a principal reason being that our insurance companies generate huge amounts of float at no cost. This is the reason we continue to buy back our shares as we continue to think they are very cheap.” Fairfax has resumed buying back stock in August and September.

-

Because Fairfax has extended duration to 2.4 years I don't think where interest rates go in 12-24 months matters all that much anymore. My view is the management team will navigate their way though it - just like they have since 2018. Extreme volatility has been very good for the team at Hamblin Watsa and Fairfax shareholders. Active management is able to take advantage of the extreme dislocations when they happen. The $2 billion PacWest loan purchase (expected to deliver a total return of 10%) being the most recent example.

-

Comments on status of hard market from CEO of Arch Capital on their Q2 call (July 27): “We often refer to the insurance clock developed by to help illustrate the insurance cycle. You can find the clock on the download cap for this webcast or on our corporate website. If you can't do the clock right now, just picture a traditional clock dial. For some time, we've been hovering at 11:00, which is one we expect most companies in the market to show good results as rate adequacy improves and loss trends stabilize. “Last year, a popular topic on earnings calls was whether rate increases were slowing or what the rates were even decreasing. These are classic signs of the clock hitting 12 when returns are still very good, but conditions begin to soften. Yet here we are in mid-2023 and conditions in most markets remain at 11:00. We've even checked the batteries in the clock and they're just fine. The clock isn't broken. It's just that the current environment dictates an extended period of rate hardening. “So what's sustaining this hard market? Well, I believe it's a relatively simple combination. Heightened uncertainty is driving an imbalance of supply and demand for insurance coverage. Since this hard market inception in 2019, we've had COVID to war in Ukraine, increased cat activity and rising inflation, all of which create significant economic uncertainty. Underwriters have had to account for more unknowns. Beyond those macro factors, industry dynamics also play a role in sustaining the hard market. Generally, in adequate pricing and overly optimistic loss trend assumptions during the soft market years of 2016 through 2019 have led to inadequate returns for the industry. “The impact of these factors should cause insurers to raise rates and purchase more reinsurance in a capacity-constrained market with limited new capital formation. Put it all together, and it may be a while before the clock strikes 12 and we begin to move beyond this hard market.”

-

Food for thought for those who are convinced the hard market in insurance HAS to end soon. Imagine a world where Fairfax continues to grow top line insurance by 8% in both 2023 and 2024 (further increasing float). And interest rates remain higher for longer. That is probably a reasonable base case today.

-

US P&C Insurance Market Report: Profitability to remain elusive in 2023 - https://www.spglobal.com/marketintelligence/en/news-insights/research/us-pc-insurance-market-report-profitability-to-remain-elusive-in-2023

-

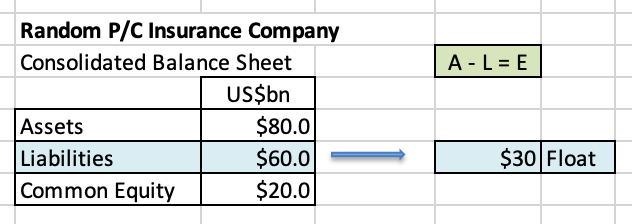

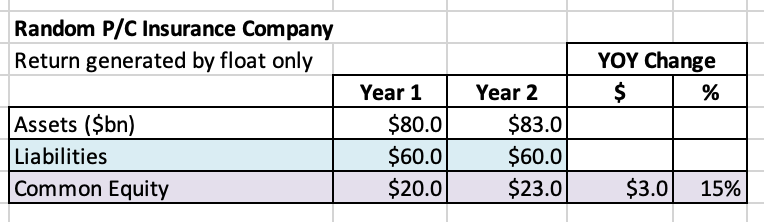

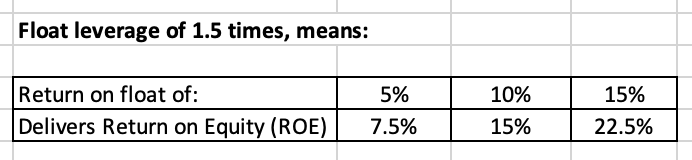

Like Indiana Jones, today we are going to set out on an adventure in search of long lost treasure. Something that most investors appear to have forgotten about. What do the legends tell us? Does it really exist or is it just a myth? What am i talking about? P/C insurance float (I’ll just call it ‘float’ moving forward). Float is such a big (and important) topic we are going to tackle it in two posts. The first post (below) will focus on the theory - what it is and why P/C investors should care. The second post will then apply the theory to today using a real company - Fairfax Financial. My plan is to have the second post completed and out on Sunday. Ancient history Thirty years ago, talking about float was all the rage for P/C investors. Read old articles on investing in P/C insurance companies and a discussion of float will usually be front and center. And the champion of float from that era was, of course, Warren Buffett and his company Berkshire Hathaway. So what happened? Why has float apparently settled into into the dustbin of history and become a relic of the past? Due to competitive insurance markets, industrywide underwriting profit has remained illusive for the past decade. At the same time, top line organic growth slowed to a crawl. Returns on investments fell: P/C insurers put most of their investments into fixed income instruments. In their battle with deflation, global central banks took interest rates all the way into negative territory. The US 10 year treasury traded at a yield below 0.60% in August of 2020 and traded with a yield below 1.5% for much of 2021. S&P Global: US P&C Insurance Market Report Float lost its value Breaking even on underwriting for a decade while returns on investments plummeted made having float far less valuable than at any point in recent history. Another smaller factor: over the years, P/C insurance has become a much smaller part of Berkshire Hathaway’s business model. What did Buffett have to say about float in his 2022 letter to shareholders? Float is mentioned 4 times in one short paragraph - telling investors to go somewhere else if they wanted to learn more. Does this sound important to you? So ‘float’ also lost its biggest cheerleader. Does this mean… Float is dead? Long live float? No, of course not. Just because float is no longer appreciated (or followed) doesn’t mean it doesn’t matter. In fact, for those paying attention, the world has changed again. The conditions that made float a big deal 30 years ago have returned: Insurance has been in a hard market since about Q4 of 2019 - above average insurance companies are seeing improving underwriting results (cost of float) and significant top-line growth (supply of float) over the past four years. Global central banks now have an inflation fight on their hands - and ‘higher for longer’ is becoming the new mantra for interest rates. Fixed income yields have spiked higher across the curve. The 10 year US treasury closed today with a yield of 4.32%, a level where it last traded at in 2007. As a result, returns on float are improving greatly. Both of these developments make having float today extremely valuable. Except remember… pretty much everyone has forgotten about float. What’s old will be new again. Well, my guess is this is about to change. I think investors are going to get interested in float again. What is going to cause the change? A new generation of investors are about to discover something Warren Buffett hit on when he bought National Indemnity back in 1967: float, under certain conditions, can be a license to print money. Those ‘certain conditions’ have returned. And in recent years some insurance companies have started up the printing presses and are now starting to print money. More than anyone imagined possible. ========== P/C insurance float: the basics Let’s first do a quick review of float. Float is deceptive. It is kind of like compound interest as a concept. It is easy to define but very hard to actually understand. Who better to teach us about P/C insurance float than the old master, Warren Buffett himself. Float: the basic building block to use to evaluate a P/C insurance company Back in the 1990’s, Warren Buffett was using P/C insurance as the core engine to drive Berkshire Hathaway’s profit growth. GEICO was purchased in 1996 and General Re was purchased in 1998. Given P/C insurance’s importance to Berkshire Hathaway shareholders, Buffett provided the following as a guide to help them understand P/C insurance as an investment. BRK 1998AR: “With the acquisition of General Re — and with GEICO’s business mushrooming — it becomes more important than ever that you understand how to evaluate an insurance company. The key determinants are: 1.) the amount of float that the business generates; 2.) its cost; and 3.) most important of all, the long-term outlook for both of these factors.” Well, Warren appears to be saying float is the most important thing to understand when evaluating an insurance company. Interesting, given how little press float gets today from analysts and investors. What is float? BRK 1998AR: “To begin with, float is money we hold but don't own. In an insurance operation, float arises because premiums are received before losses are paid, an interval that sometimes extends over many years.” Float is money a P/C insurer has that it can use to invest. It is an asset but it is a liability (not equity). It is kind of like a very sticky deposit at a bank (a deposit is also a liability for the bank). Because float is a liability, it is also leverage. Like all leverage (i.e. debt), float can be both good or bad - and this depends on the cost paid over time to hold the float. What is the cost of float? BRK 1998AR: “Typically, this pleasant activity (the insurance business) carries with it a downside: The premiums that an insurer takes in usually do not cover the losses and expenses it eventually must pay. That leaves it running an "underwriting loss," which is the cost of float. An insurance business has value if its cost of float over time is less than the cost the company would otherwise incur to obtain funds. But the business is a lemon if its cost of float is higher than market rates for money.” Underwriting determines the ‘cost’ of float. This point is critical. Over time, if an insurer can produce an underwriting profit on its insurance business that means the cost of its float is actually a benefit - that is better than free. That means the insurer is actually getting paid to hold the float. This is far better than ‘the cost the company would otherwise incur to obtain the funds.’ Float is a pile of money that an insurance company can actually earn two income streams from: underwriting (if float is obtained at a benefit) and investing. Sounds like Buffett was on to something. To summarize: according to Buffett, a good P/C insurance company: Has a large amount of float Is a good underwriter - is able to generates the float at a favourable cost (ideally a benefit) Has a good long term track record - of both growing float and as a solid underwriter Buffett’s secret sauce: P/C insurance float Buffett’s genius has really been two pronged: Use P/C insurance float as an ever-increasing low cost (free) source of capital/leverage used to push profits even higher. These growing profits were then continuously reinvested into great companies/equities (outside of insurance) that have also become compounding machines over time and pushed profits even higher. OK. So there is a quick review of float, explained with the help of Warren Buffett. To help us understand float even better, let’s look at it now from a balance sheet perspective. ========== Float and the balance sheet Let’s create an imaginary insurance company - called Random P/C Insurance Co - and create a fictitious balance sheet. Our company has $80 billion in assets, with $60 billion in liabilities and $20 billion in common shareholders’ equity. Of the total liabilities of $60 billion, float is $30 billion. The summary of the balance sheet is below: We are also going to assume common shareholders’ equity = book value. We are going to make up more numbers below. We are using numbers that make our calculations easy. Please don’t focus too much on the exact numbers. Instead, focus on the information they are trying to convey - especially about leverage. Cost of float Let’s assume our insurance company is a slightly above average underwriter with a combined ratio (CR) of 96 - this translates into a ‘benefit’ of float (better than free - our company is actually getting paid to hold their float). Return on investments (which includes float) Let’s assume our insurance company is above average in terms of the return it earns from its total investments (which includes float) - let’s assume it earns 8% on average. We are also going to assume there are no taxes. The return of Random P/C Insurance Co When we put the two together we get: Benefit of float (CR of 96) Return on investments = 8% Let’s assume Random P/C Insurance Co earns a total return of 10% on its float. This means our insurance company is earning the following: $30 billion float x 10% = $3 billion. Can we calculate the actual leverage provided by the float? Yes. Total earnings from float of $3 billion will flow though the income statement and increase retained earnings, which will then flow though to the balance sheet and increase both assets and common shareholder equity by $3 billion. So a return from float of 10% results in an increase in common shareholders' equity of 15%. The leverage can be calculated as follows: total float / common shareholders' equity. In our example float of $30 billion / common shareholders' equity of $20 billion = 1.5 x leverage Common equity, debt and total investments The above increase in common shareholders' equity was driven solely by float. A company is also going to generate earnings from its common shareholders’ equity - the funds provided by shareholders. Perhaps it also uses a little debt to generate more earnings. Any returns generated by its other investments (those other than float) need to be added to the numbers above. ========== Below Buffett summarizes how float fits into the big picture Berkshire Hathaway 1995AR: “In more years than not, our cost of funds has been less than nothing. This access to "free" money has boosted Berkshire's performance in a major way. “Any company's level of profitability is determined by three items: 1.) what its assets earn; 2.) what its liabilities cost; and 3.) its utilization of "leverage" - that is, the degree to which its assets are funded by liabilities rather than by equity. “Over the years, we have done well on Point 1, having produced high returns on our assets. But we have also benefitted greatly - to a degree that is not generally well-understood - because our liabilities have cost us very little. An important reason for this low cost is that we have obtained float on very advantageous terms. The same cannot be said by many other property and casualty insurers, who may generate plenty of float, but at a cost that exceeds what the funds are worth to them. In those circumstances, leverage becomes a disadvantage. “Since our float has cost us virtually nothing over the years, it has in effect served as equity. Of course, it differs from true equity in that it doesn't belong to us. Nevertheless, let's assume that instead of our having $3.4 billion of float at the end of 1994, we had replaced it with $3.4 billion of equity. Under this scenario, we would have owned no more assets than we did during 1995. We would, however, have had somewhat lower earnings because the cost of float was negative last year. That is, our float threw off profits. And, of course, to obtain the replacement equity, we would have needed to sell many new shares of Berkshire. The net result - more shares, equal assets and lower earnings - would have materially reduced the value of our stock. So you can understand why float wonderfully benefits a business - if it is obtained at a low cost.” Float is better than equity? This question is a bit of a mind bender. Because of its unique ‘cost’ (i.e. low cost or even a benefit), in the past Buffett has said that he views float as being better than equity. BRK 1997AR: “Since 1967, when we entered the insurance business, our float has grown at an annual compounded rate of 21.7%. Better yet, it has cost us nothing, and in fact has made us money. Therein lies an accounting irony: Though our float is shown on our balance sheet as a liability, it has had a value to Berkshire greater than an equal amount of net worth would have had.” Well, suggesting float is better than equity is perhaps a bridge too far. However, I think we can conclude that float matters a great deal. Especially today (in a high interest rate world). Conclusion OK. So now we know what float is and the key metrics to use to evaluate P/C insurers. Who should we start with? That is an easy question to answer. In our next post (coming Sunday), we will do a deep dive on float at Fairfax Financial to see what we can learn. ========== How Warren Buffett Achieves Great Returns Every Year - Advantages of Insurance Float

-

The tricky thing about inflation is just when you think you have it licked it pops higher again. At least that was the experience in prior inflationary episodes. Central banks are starting to look and sound like they think they have inflation licked. I am not so sure. Here in Canada we have record government spending.. that continues to increase. We also have a severe housing shortage so all levels of government are now rallying to try and get more housing units built (yes, at the same time the Bank of Canada is trying to slow housing). Rental prices continue to increase (at least in Vancouver) driven by record low vacancy rate. Minimum wages in almost all jurisdictions are up meaningfully year over year. Wealth effect has minted millions of millionaires (housing bubble) over the last decade - these people continue to spend. Much higher interest rates is spiking interest income of savers (like my mother-in-law) and that new meaningful income stream is leading to increased spending. Oil spiking is now feeding through to increases at the gas station…. In my province we are building a massive hydro dam in the north east of the province. We are building two large pipelines (one to Vancouver and the other to Kitimat) thousands of miles long at something like triple the original cost. A LNG facility is being built in Kitimat. The Province is also doing a massive rebuild of the infrastructure destroyed by record flooding 2 years ago (all over the province). Forest fires just wiped out hundreds of expensive houses in the interior - now those all will get rebuilt. Oil and gas and mining is all doing well. I could go on and on. This is just my long winded way of saying that i agree with you. This suggests to me we might see higher for longer when it comes to interest rates. Like perhaps well into next year. And if inflation actually pops again perhaps we see central banks actually tighten even more. I really have no idea. So no strong conviction. But it is super interesting…

-

@Hamburg Investor thank you for coming over to the dark side and joining CofBF. The more discussion and debate we can get the better. We are all trying to learn (and hopefully make a little money along the way). Your post above outlines a major flaw with my 3 year forecasts for Fairfax: i am likely being too conservative for 2024 and 2025. Part of this was by design. When i started at Kraft many years ago one of my first bosses taught us newbies the art of sandbagging when building a forecast (very important when your quarterly bonus payout was tied to it). On reflection i likely need to make some adjustments to parts of my 3 year forecast (i feel a little like i am getting my hand slapped by senior management - a little sandbagging was ok… but too much got you into trouble). What am i missing? Two things: 1.) capital allocation skills of Hamblin Watsa: they have been hitting the ball out of the part since 2018 when it comes to capital allocation. 2.) power of compounding - well understood by members on this board: - a 15% return per year is a double in less than 5 years. - a 20% return is a double in about 3.5 years. So yes, i need to get more realistic with my estimate for how fast investments (and returns from those bigger numbers) will be growing in the coming years. Growth of growth is the secret sauce that is now kicking in at Fairfax (due to double digit growth in insurance and investments AND improving underwriting and much higher investment returns). Today, Fairfax is delivering a 20% ROE. I think they will be able to deliver a high teens ROE over the next three years (2023-2025). I like my earnings per share estimate of $160/share for 2023. My estimates for 2024 ($165) and 2025 ($174) need to move higher.

-

@SafetyinNumbers thanks for posting. It is nice to see the backbacks happening again. I am hopeful Fairfax can keep taking out a minimum of 2% of effective shares outstanding each year - keeping the trend in recent years going. The buybacks also signal the company continues to see their shares as being undervalued. Obviously shares aren’t as cheap as prior years but the company’s earnings and prospects have improved greatly in recent years.

-

@glider3834 thanks for posting. I missed this last transaction. Great news. I was wondering if Eurobank was going to have to pay an additional premium to get over 50% and the answer is no. When they went to €2.35/share they had their ducks in a row to get +50%. Smart.

-

@glider3834 great summary. So at Eurobank’s price of €2.35/share Hellenic Bank is valued at €1 billion and it is on track to earn €260 million after tax in 2023. That looks pretty good. There are so many interesting layers to this transaction… - I think the acquisition will take up to 12 months to be approved. So Hellenic Bank will likely be a much more valuable bank when they actually fork over the money next year. Especially if interest rates stay higher for longer. - Eurobank still will not have more than 50% control. I wonder if they already have the next purchase lined up to get over 50%. - Eurobank sold the bank they owned in Serbia recently (at a pretty decent price if i remember correctly). Essentially flipped from being a smaller player in Serbia (8% market share) to being the largest player in Cypress (depending on metric being used). Proceeds from Serbian sale (70% of €280 million) will pay for a chunk of the Hellenic purchase. Looks like good strategy and good capital allocation. The management team at Eurobank has been executing well for years.

-

@hardcorevalue i am not sure how long you have followed Fairfax India. The stock has just had an amazing run higher from $9.65/share a year ago to over $14/share recently. Yes, since December the stock has moved mostly sideways. I have followed Fairfax India for years. I have no idea how the stock trades. I do think Fairfax India has an exceptional management team. They continue to make good decisions and build value for shareholders. I own some shares (not a big position). Where will the stock go from here? I have no idea. But my guess is in 5 years time shareholders will probably do well (from current levels) - and possibly very well. But week to week or month to month (and perhaps year to year) the sideways movement is hard to make and sense of (for me anyways). So i don’t try.

-

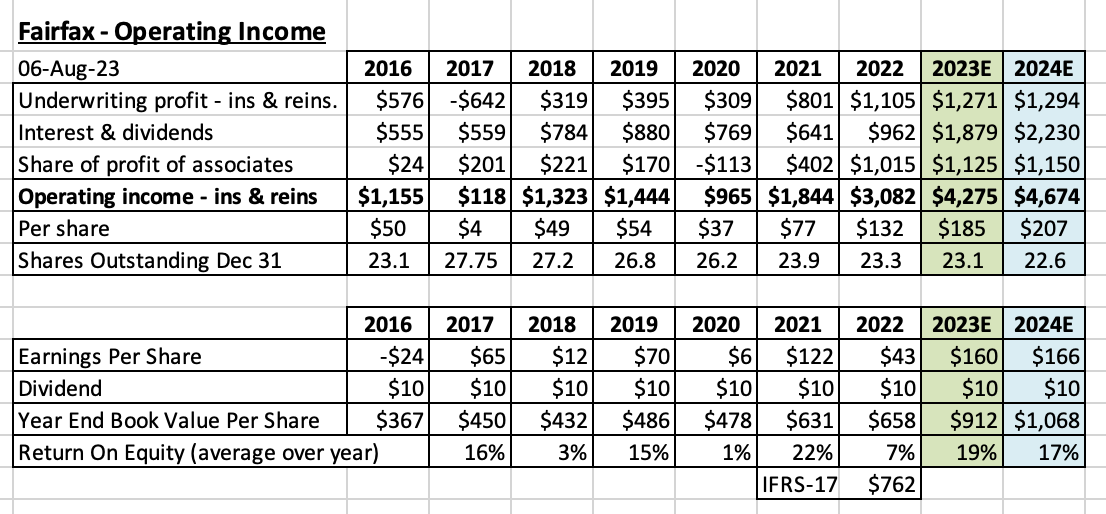

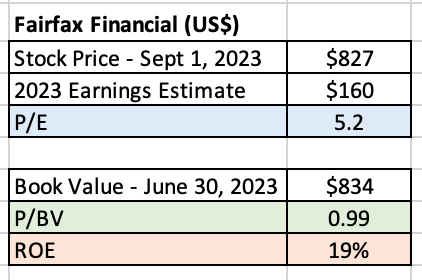

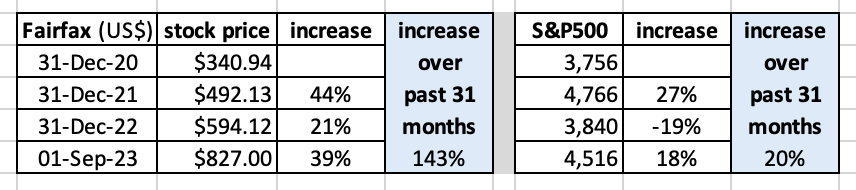

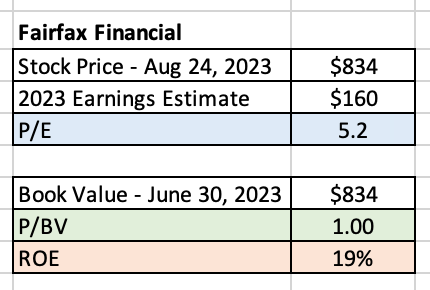

What is the best way to value Fairfax today? Peter Lynch: “What possible assurance do you have that (a stock you own) will go up in price? And if you are buying, how much should you pay? What you’re asking here is what makes a company valuable, and why it will be more valuable tomorrow than it is today. There are many theories, but to me, it always comes down to earnings and assets. Especially earnings.” One Up On Wall Street ---------- Fairfax has been an exceptionally difficult company for investors to value for the past three years. And especially right now (given the sharp rise in the stock price). Even investors who have followed the company closely for many years are having a hard time. New investors don’t stand a chance. Mr Market is saying Fairfax has a fair value today of $827/share (that is where it closed Sept 1, 2023). I think the stock is still wicked cheap. Others on this board feel the stock is only mildly cheap. What is the fundamental problem? There is no consensus of what level of earnings the collection of assets that Fairfax currently owns can deliver on a regular basis moving forward. Or what to expect for the next 3 to 5 years. Most investors prefer to use book value as their primary tool to value Fairfax. It is an insurance company after all. And using book value is supposed to be the proper way to value an insurance company. Using book value also conveniently allows an investor to largely ignore earnings (coming up with an estimate). And given the lack of consensus around earnings for Fairfax… well isn’t that a good thing? Well, easy and good are not the same thing. What is the best way to value Fairfax today? Just like any job, we need to pick the right tool. To do this we need to answer the following question. Is Fairfax an insurance company or a turnaround play? No, this is not a trick question. The answer, of course, is that Fairfax today is both. But we are talking here about how to value Fairfax as a company. My view is that today Fairfax should be valued primarily through the lens of a turnaround play. Not as an insurance company. Does it make that much of a difference? It makes a huge difference. Using book value (P/BV and ROE) to value insurance companies with relatively consistent financial results over a 5 or 10 year period makes a lot of sense. But using book value (P/BV and past ROE) as the primary measure to value a turnaround like Fairfax makes little sense especially when they are still in the middle of the earnings part of the turnaround. The problem with book value (P/BV and ROE) is it is a ‘rear view mirror’ valuation measure - it does a great job of telling you what has happened. And for lots of insurance companies what ‘has happened’ is likely to continue to happen in the future. So using book value (P/BV and ROE) as a primary valuation tool makes sense. But for a turnaround like Fairfax, where a massive amount of change is happening - which is leading to much higher earnings - focussing primarily on the past is going to mess investors up. It is going to cause them to way under estimate future earnings. This in turn is going to cause them to under value the company. And that is going to lead to poor investment decisions. A lot of investors who follow Fairfax are probably wondering how they missed the big move in the stock over the past 31 months (since Jan 1, 2021). My guess is the key issue is too much ‘rear view mirror’ analysis and not enough ‘looking out the front windshield’ analysis. The difference between valuing a stodgy insurance company versus valuing a turnaround. How should an investor value a turnaround? Let’s look to Peter Lynch for some insight. Peter Lynch loved turnarounds. It was one of the 6 buckets he used to classify his stock investments. Classifying stocks properly at the beginning of the process is critical. Because the classification determined the proper method to use to analyze the stock. To value a turnaround it is critical to: First, understand what went wrong. Second, confirm that whatever went wrong has indeed been fixed. Third, focus in on evaluating the assets and estimating the trajectory of future earnings. What went wrong at Fairfax? Fairfax has three economic engines: insurance, investments - fixed income and investments - equities/derivatives. Fairfax’s insurance business has been a solid performer over the past decade. And their investments - fixed income economic engine has also performed well. The issue at Fairfax was the investments - equities/derivatives engine. The good news for Fairfax was the solution to their poor performance was fully within their control. They just needed to stop doing some really dumb things (putting it politely) in one part of the company. What was the fix? To right the ship in the equities/derivatives engine, Fairfax did a few things: 1.) end the equity hedge/shorting strategy. The equity hedge positions were exited in late 2016. The final short position was sold in late 2020. Done. 2.) make better equity purchases. This started in 2018. Done. 3.) fix poorly performing equity purchases from 2014-2017. This started in 2018 and looks like it was completed in 2022. Done. But Fairfax didn’t stop here. They did even more: 4.) since 2020, they have made at least one brilliant decision each year: Late 2020/early 2021: initiated the FFH total return swap position, giving exposure to 1.96 million Fairfax shares at $373 share (resulting in a $900 million pre-tax gain to date) Late 2021: buying 2 million Fairfax shares at $500/share (book value is currently $834/share and intrinsic value is likely well over $1,000). June 2022: sale of pet insurance business for $1.4 billion (resulting in a $992 million after-tax gain). And the insurance gods have also been smiling on Fairfax: 5.) a hard market in P&C insurance started in Q4, 2019. And it looks like it will continue into 2024. And if all that wasn’t enough, the macro gods also decided to smile on Fairfax, delivering to the company their biggest gift yet: 6.) after dropping interest rates to close to zero in late 2021 they pivoted and spiked rates to more than 5% in 2023. Fairfax navigated their $38 billion fixed income through the treacherous storm perfectly - and the gold ($billions) is literally raining down today. So Fairfax not only stopped doing dumb things, they also started hitting the ball out of the park. At the same time both the insurance and macro gods started smiling on the company. Each of these things on their own has causing earnings to grow significantly over their historical trend. Stacked one on top of the other - well earnings have exploded higher. In short, the turnaround at Fairfax that began back around 2018 now looks complete. But importantly, the lift to earnings will likely take a few more years to fully play out. What is happening to earnings at Fairfax We are going to focus on operating income given this is considered the high value part of earnings for an insurance company. Operating income averaged $1 billion ($39/share) each year for 5 years from 2016-2020. From this base it has: Doubled to $1.8 billion in 2021. Tripled to $3.1 billion in 2022. Is on pace to quadruple to $4.3 billion in 2023. Is estimated to be $4.7 billion, or $207/share, which would be a quintuple from $39/share (average from 2016-2020). How would an investor focussed primarily on book value have seen any of this coming? The answer is easy… they would have completely missed it. They probably still are. What are we learning about Fairfax’s collection of assets? Beginning as far back as 2021, investors were getting glimpses that something good was happening at Fairfax. In 2022, is was obvious that ‘new Fairfax’ had arrived - but the good news was masked in the top line results by the bear market in financial markets and the large unrealized losses in fixed income and equities. But the change was obvious to those of us who followed the company closely. In 2023, the story continues to improve. And 2024 looks even better. What we are learning is Fairfax was significantly under earning on its collection of assets for much of the past decade. But all the shackles that were holding earnings down have now been removed. Management is executing exceptionally well. For the first time in the company's history, the three economic engines are all delivering record results at the same time: insurance, investments - fixed income and investments - equities/derivatives. Investors are just starting to get a look at what the true earnings power of Fairfax is on a go forward basis. And the total number is far higher than anyone dreamed possible. So what is the valuation of Fairfax today? Board members probably wonder why I have been so focussed on earnings in my analysis of Fairfax the past two years. Well, now you know why. I view Fairfax currently as a turnaround type of investment - and a heavy focus on earnings and assets is the only rational way to analyze the company today. It’s not that I don’t pay attention to book value. I do. I just have never trusted how useful it is a tool to value Fairfax today or to help me better understand its earnings power as a company. My current estimate is Fairfax will earn $160/share in 2023. I think that is a good baseline to use for earnings moving forward. If my analysis is right then that means Fairfax is trading at a PE of 5.2 x E2023 'normalized' earnings. Yes, that is nuts. What does the future hold? Peter Lynch: “Companies don’t stay in the same category forever. Over my years of watching stocks I’ve seen hundreds of them start out fitting one description and end up fitting another.” One up on Wall Street Over the next couple of years we will all come to better understand Fairfax. And what its collection of assets are capable of delivering. What the true ‘normalized’ earnings power of the company is. At that point in time, the turnaround will long be over. And Fairfax will revert to being another predictable, boring old insurance company. And at that time, the valuation metrics (like book value, P/BV and ROE) generally used for valuing boring old insurance companies will again be appropriate to use for Fairfax. If Fairfax is able to deliver strong earnings growth in the coming years the much improved results will slowly get baked into its historical numbers. That is when more traditional insurance investors will start to 'discover' how well managed Fairfax is. And how cheap the stock is. As this process plays out the P/BV multiple will likely expand significantly from 0.99 today to something more in line with peers, perhaps north of 1.3 (perhaps higher). ————- Another reason Peter Lynch liked turnarounds: Peter Lynch “The best thing about investing in successful turnarounds is that of all the categories of stocks, their ups and downs are least related to the general market.” One Up on Wall Street Fairfax is up 143% since January 1, 2021. S&P500 is up 20%. Fairfax’s outperformance over the S&P500 over the past 31 months has been an amazing 123%. Yes, that Peter Lynch is one smart dude. ————— Peter Lynch on Turnarounds “These are stocks that are battered down or they are hated companies, or they have been forgotten about. They are depressed in price but you have determined some one thing or a few things that have the potential for reversing this company’s fortunes independent of the industry getting better, or the economy getting better. “You always have to do a balance sheet check on any company. This includes turnarounds. Do they have enough cash to make it through the next 12 months or the next 24 months? Do they have a lot of debt that’s due right now? These are important questions to answer. “Make sure you understand and believe in the plan to restore corporate profits. It is all internal. They are doing something, either a new product, new management, cutting costs, getting rid of something. Something inside the company that allows them to improve themselves. “Lots of turnarounds never happen, but a few winners can make up for a lot of losers. What’s important is to wait for the actual evidence of the turnaround occurring, not just the symptoms. (With) the turnaround, you have plenty of time. So just don’t buy on the hope. Wait for the reality. Turnarounds are so big it is worth waiting to get some real evidence.”

-

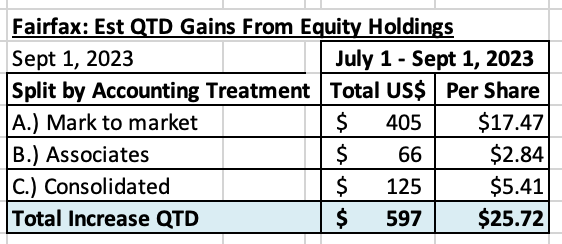

Fairfax's equity holdings (that I track) are up about $597 million so far in Q3 (9 of 13 weeks = 69%). Shaping up to be another quarter of solid performance. Split by accounting treatment can be seen below. I have attached my Excel file if you want a closer look. Top Movers? All up this quarter: Thomas Cook India = $156 million FFH TRS = $154 million Eurobank = $110 Broad based gains: 6 different equities are up more than $20 million Stelco = ($43) million: the largest decliner Fairfax Sept 1 2023.xlsx

-

Lots of insurers are still sitting on large losses in their bond portfolio. The underwater fixed income securities are held in their held to maturity bucket so the losses have not flowed through the income statement. And the company line is ‘we will hold to maturity so it does not matter’. And that, of course is stupid. And makes no sense. Of course there are significant costs today for all companies that were buying fixed income duration in 2020 and 2021. Saying ‘it doesn’t matter’ is just a crafty psychological trick. So you buy a 4 or 5 year bond in 2020 or 2021 at a 2.5% yield. Yes, an insurer can hold this bond to maturity. But you hold a fixed income instrument to make money. 1.) what is the real yield on all these bonds? With inflation running 4 or 5%? You are losing money (in terms of purchasing power) on a significant part of your fixed income portfolio. For years. These losses/positioning matter (just ask the ratings agencies). 2.) what is the opportunity cost? If you have a long duration portfolio of 4 or 5 years you also have a limited ability to reinvest at much higher rates. This also means earnings for these insurance companies are messed up. If you don’t book the loss today, it effectively means your earnings in prior year periods is overstated. There is no free lunch. This also means historical ROE’s from most recent years are overstated. In the current environment of much higher rates, Fairfax is a huge winner. Because of the actions of its management team. Their management of their fixed income portfolio has been best in class - and it is not debatable. My current estimate is Fairfax is tracking to deliver a return of 8.6% on its $56.5 billion investment portfolio in 2023 and better than 8% in both 2024 and 2025. That is going to blow insurance peers out of the water. Yes, Fairfax’s stock continues to trade at a severe discount to peers. Efficient markets once again demonstrating how inefficient they can be at times.

-

@gary17 i have a question for your. Lets pretend Fairfax delivered an ROE of 15% per year on average for the past 5 years. This year they are on track to deliver an ROE of around 19%. Prospects for 2024 and 2025 look good (mid teens ROE). What multiples (PE and P/BV) would be reasonable to pay today?

-

@newtovalue yes, my estimate for the investment portfolio is low and probably way low: 2023 = $56.5 billion 2024 = $57.5 billion 2025 = $58.5 billion When the GIG acquisition closes that will cause a material increase to the investment portfolio. Continued organic growth in insurance will help as well. And as earnings roll in each quarter and are reinvested (further growing insurance and non-insurance buckets). My estimates are pretty dynamic… constantly changing as we get new information. Some numbers will be high and others low. My goal is to get the direction and total reasonably close. So far most of my estimates have been too low and often by quite a bit. So i took things up a fair bit with my last set of revisions. We will know more when Fairfax reports Q3.

-

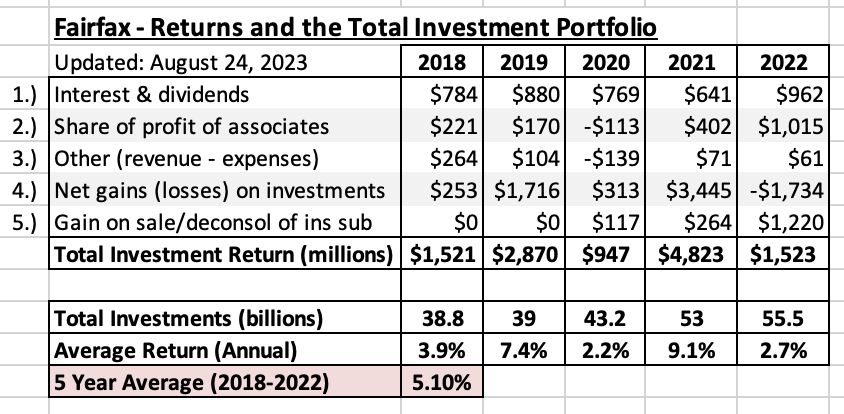

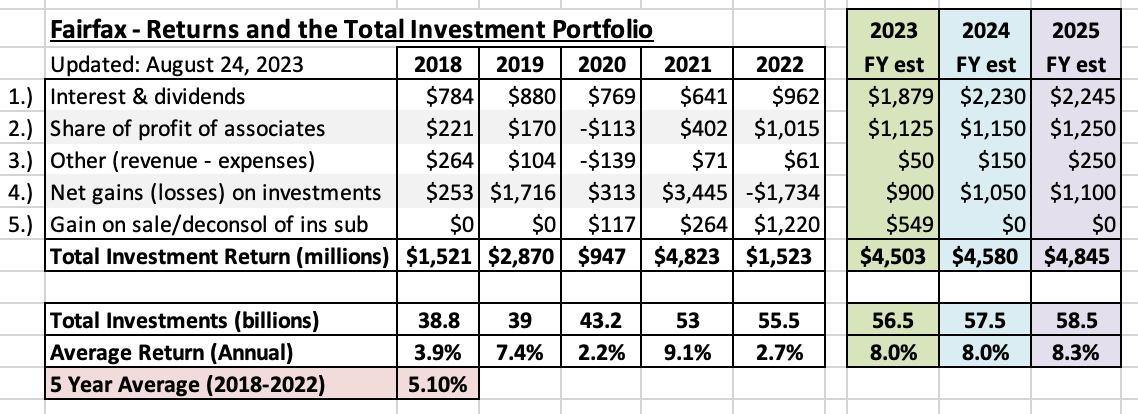

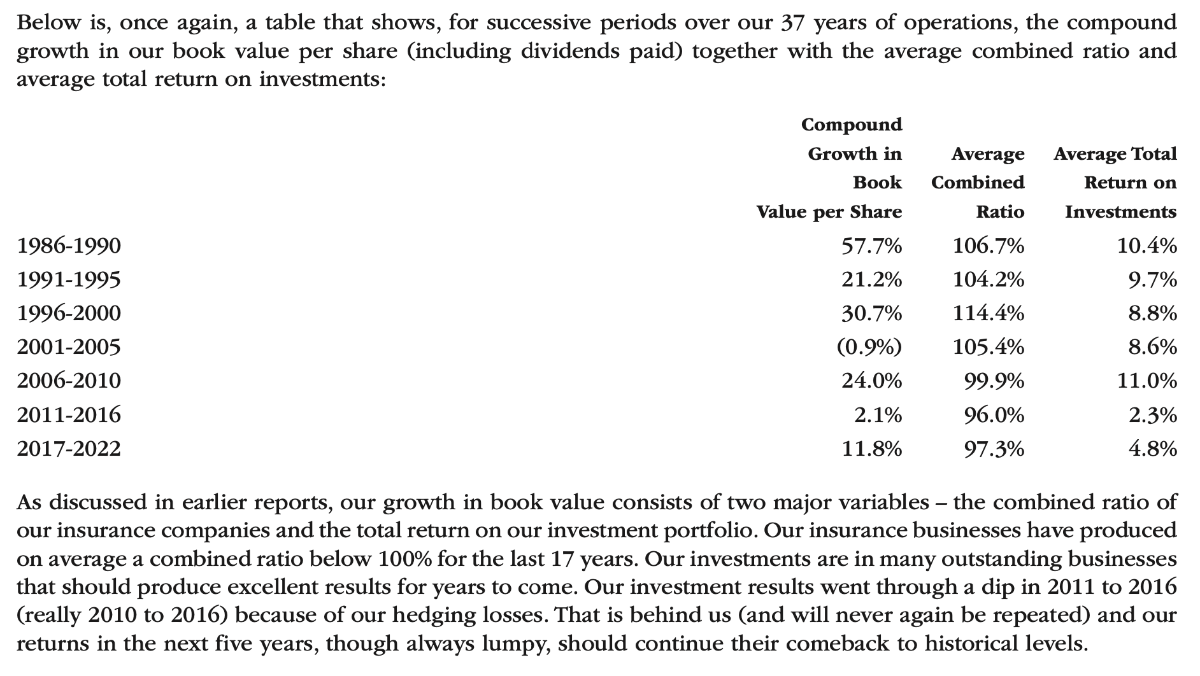

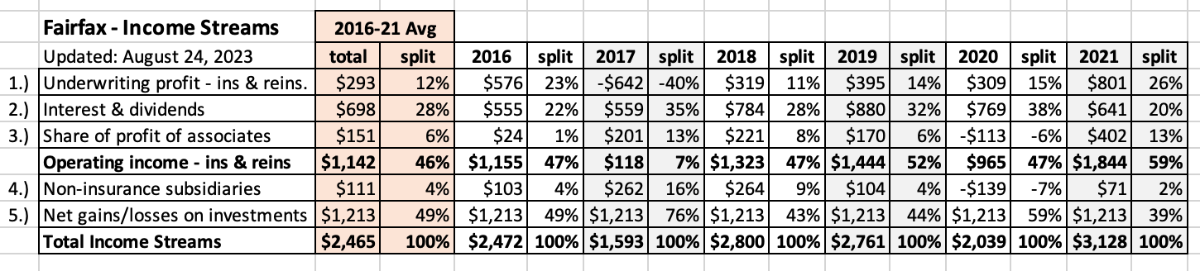

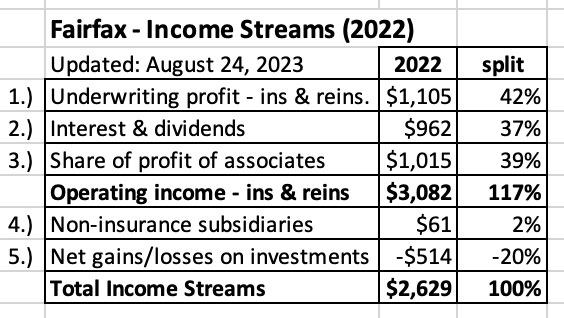

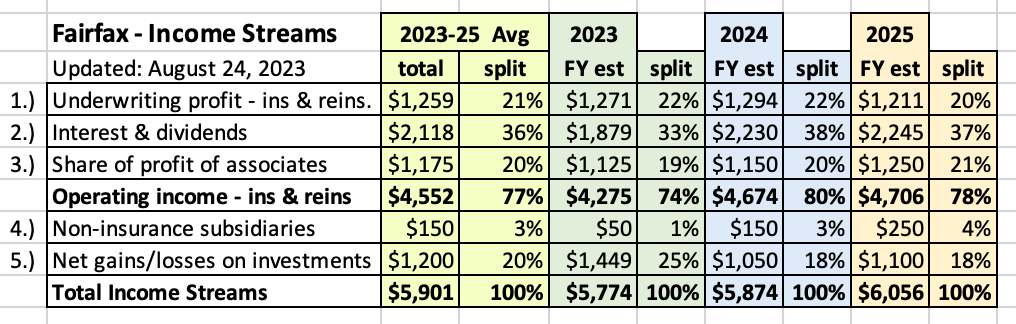

Fairfax’s $56.5 Billion Investment Portfolio: What Will It Earn in 2023 to 2025? Fairfax has two income sources that drive earnings and growth in book value: underwriting and investments. Given their business model (use insurance/float to invest in non-insurance companies) about 20% of their income comes from underwriting and 80% of their income comes from investments. Given its outsized importance to Fairfax, let’s dig into Fairfax’s investment portfolio and try and determine what sort of return it will be able to generate moving forward. This will give us great insight into what Fairfax will earn. And this will enable us to better understand Fairfax’s current valuation. How big is Fairfax’s investment portfolio? It is about $56.5 billion or $2,435/share. Has it been growing in size? Yes. From 2018 to 2022 it increased: in absolute terms by 9.4% per year. per share by 13.5% per year. What is the split today? Fixed income = $40 billion (71%) Equities/derivatives = $16.5 billion (29%) What did Fairfax earn on its total investment portfolio in the past? Prem provided this information in his letter in the 2022AR (attached at the bottom of this post): From 1986-2010, Fairfax earned an average of 9.7% on its investment portfolio. For the first 25 years of its existence, Fairfax’s secret sauce was its return on its total investment portfolio. In aggregate it was very good. From 2011-2016, Fairfax earned an average of 2.3% From 2017-2022, Fairfax earned an average of 4.8% 2010-2020 was a lost decade for Fairfax shareholders. The issue was not the insurance side of the business. The investment side of the company completely messed up (the equities/derivatives part). The big mistake was the equity hedge/short position. There were also lots of poor equity purchases from 2014-2017. Let’s focus on the last 5 years. What Fairfax did 10 years ago is interesting. What they did the past 5 years is much more helpful in understanding the current situation. (Please note, I am not sure of the exact build that Prem used to get to the averages that he put in his letter in the 2022AR. My build is outlined below. There will be differences. However, directionally, the comparisons should still be useful.) From 2018-2022, Fairfax earned an average of 5.1% from their investments (my build is detailed below). Let’s overlay what happened in financial markets over this same time period: historically low interest rates from 2018 to the middle 2022 - this killed returns in the fixed income portfolio for much of the 5 year period. 3 different bear markets in stocks: 2018, 2020 and 2022. historic bear market in bonds in 2022. Given the significant headwinds in financial markets from 2018-2022, the fact that Fairfax was able to deliver a total return of 5.1% each year (on average) is actually pretty impressive. What happened? Hamblin Watsa started to get their investing mojo back. Note: IFRS: I am ignoring for now ‘Effects of discounting and risk adjustment’ = about $480 million to June 30, 2023. What did the management team at Fairfax do from 2018-2022? Internal: Ended equity hedge/shorting strategy. The final short positions (closed out in late 2020) resulted in total losses of $624 million from 2018-2020, or an average of $208 million over each of the three years. The equity holdings from 2014-2017 have mostly been fixed. Beginning in 2022, and lead by Eurobank, these holdings have gone from being a headwind to earnings (losing hundreds of millions every year in total) to now being a tailwind (making hundreds of millions every year in total). That is likely an improvement (swing) of +$500 million per year (my numbers are very rough and intended to be directionally accurate). Since 2018, new equity investments have been very good. They are, in aggregate, performing very well. These holdings are a growing tailwind to earnings. Chug, chug, chug. External: Interest rates bottomed in late 2021: Fairfax sold $5.2 billion in corporate bonds (yielding 1%) and bought short term treasuries and reduced average duration to 1.2 years. Interest rates spiked in 2022 and into 2023: average duration has been extended to 2.4 years. I think they bought some Canadian corporate bonds in Q2, 2023... Covid bear market 2020: got exposure to 1.96 million Fairfax shares at $373/share. Bought back 2 million Fairfax shares in late 2021 at $500/share. Bear market 2022: spent billions buying more of companies it already owned often at bear market low prices. The investment team at Fairfax has been putting on a clinic on the benefits of active management over the past 3 years. The extreme volatility we have seen the past three years has actually been a big tailwind to Fairfax and its investment portfolio. This begs the question: would Fairfax perform better in a ‘safe’ environment or in a ‘shit storm’ environment? Over the medium term (3 year time horizon), i think they would actually do better in a ‘shit storm’ environment. Especially when you include the $3.7 billion in net earnings (much of it from high quality sources that could be reinvested opportunistically) that is likely to be rolling in each year moving forward. That would be ‘buy low’ on steroids. We are going to come back to this point later. But we are getting ahead of ourselves a little. How do things look in 2023? Both equities and fixed income are poised to deliver very good results moving forward - and the table is set for this to last for years into the future. This is the part that most investors still do not get. Why? The significant ‘internal’ drags that were holding down Fairfax’s returns from 2018-2022 are gone. And significant new tailwinds have emerged. Equities: No more losses from the equity hedge/short trade. The equity purchases from 2014-2017 are now delivering very good returns. The equity purchases from 2018 to date continue to performing well. Importantly, Fairfax boosted their stakes in many companies they already own at bear market low prices. This will be a tailwind for future earnings. Covid headwinds have flipped to tailwinds at Recipe, Thomas Cook and BIAL. Bottom line, the underlying earnings power of Fairfax’s $16.5 billion equity portfolio is finally fully delivering on its potential. It was already doing much better in 2022. All an investor had to do was look at share of profit of associates, which spiked to over $1 billion in 2022, to see the transformation of the companies captured in that bucket. But the improved performance in 2022 was masked by the general bear markets in bonds and stocks and the subsequent large unrealized investment losses that were reported. Fixed income: As good as the story is in equities, it is even better in fixed income. Going short duration of 1.2 years in late 2021 was, with hindsight, pure genius. Probably the best investment decision Fairfax has ever made in its history. Bond yields have since spiked higher. As a result, interest income has been spiking higher. It began picking up steam in 2022. But it has really got going in 2023. And 2024 is shaping up to be even better. And now Fairfax is extending duration. The big increases in the returns in both the equity and fixed income portfolios is now spiking the return on Fairfax’s $56.5 billion total investment portfolio. Most importantly, the increase in earnings we are seeing in the equity portfolio (to higher quality) and the bond portfolio (to longer duration) make these higher earnings durable. Ok. Enough talk. Show me the money! What is the current estimate of what Fairfax might earn on its total investment portfolio in 2023? My current estimate for Fairfax to generate an total investment return of about $4.5 billion in 2023, or a return of 8% on its total investment portfolio. Assumptions to get to $4.5 billion in 2023: We are already half way through the year in terms of reported results. And we are almost 2 months into Q3. So it is a pretty straight forward exercise to come up with reasonable estimates for the remainder of this year: Interest and dividend income was $465 million in Q2. My guess is the current run rate is over $500 million per quarter so $1.9 billion for the year looks about right. $40 billion fixed income portfolio: my estimate for average yield in 2023 is 4.5%. Share of profit of associates was $603 million in 1H. My estimate of $1.1 billion for FY is likely low. Consolidated equities was -$36 million in 1H. This should reverse in 2H, driven by Recipe, Thomas Cook, Fairfax India and other holdings, and finish the year at $50 million. Net gains on investments was $450 million in 1H. I am estimating this to finish the year at $900 million. Gain on sales = Ambridge closed in Q2 and the GIG revaluation is expected to happen in 2H. The assumptions above are hardly heroic. And they get us to an 8% return on the investment portfolio for 2023. What is the current estimate for 2024 and 2025? My forecast is for Fairfax to earn an average of 8% on its total investment portfolio in both 2024 and 2025. And I think this is a conservative number. Why? For all the reasons I outlined above: many of the tailwinds to the equity and fixed income portfolios that are just now fully flowing through to reported results and this improvement should continue into 2024, although at a slower pace. Significant net earnings rolling in: an estimated $3.7 billion per year (mostly high quality). A management team with proven best-in-class capital allocation skills. I am sandbagging my forecast for ‘net gains on investments’ for 2024 and 2025. I am going low with my estimate because, of course, i don’t know where they are going to come from. Today, the management team at Fairfax has so many good options: Buy Fairfax stock trading at 5.2PE (to estimated 2023 earnings) and 1 x BV (which is well below intrinsic value). Shift from treasuries to high quality corporate bonds that are now yielding 6% to 6.5%. Given the increase in rates further out on the curve, continue to extend duration of the fixed income portfolio. Lots of equities are trading at low valuations (the run up in the market averages YTD in 2023 was largely driven by the ‘magnificent 7). Bottom line, it would not surprise me if Fairfax delivers a return of better than 8% on total investments in each of 2024 and 2025. What if my estimate of 8% on average over the next 3 years is approximately right? An 8% return on investments equates to net earnings of about $160/share in 2023. ($160 in earnings also assumes a full year CR of 95). This level of earnings should grow nicely in the future. The stock is currently trading at $834. Book value is $834/share. An 8% average return on investments means the current share price is indeed crazy cheap - sorry to keep repeating this point… but it is what it is. So what is it investors are missing? The total earnings that Fairfax is currently delivering is so big that investors simply don’t believe it. Fairfax’s historical numbers and my estimates do not match up - not even close. It makes sense for most investors to believe that Fairfax’s numbers will revert back over time to their lower historical levels. Investors also don’t believe that the high earnings number, if it actually happens in 2023, is sustainable. So even if a big number happens in 2023, well, it will be a fluke. They say “That baby’s coming down!” Why does the number have to come down in 2024? You pick the reason: ‘Interest rates are coming way down.’ ‘An economic recession is coming.’ ‘A stock market correction in coming.’ 'In 2026 (you fill in the bad thing that has to happen).' The pushback from investors is driven mostly by either disbelief or macro concerns. Nothing to do with Fairfax and what the company is actually doing or based on the results that it is currently delivering. What is it Peter Lynch suggests that an investor should focus on when doing their research on a company? Facts and earnings. What about macro? He thinks investors who focus on macro are nuts. Here is the really interesting thing… even if all of those scary macro things happen… I think they might actually make Fairfax’s future performance even better. Heads I win. Tails you lose. I love that type of bet. ————— From Prem’s letter in the 2022AR:

-

@tnp20 I think the guest in the podcast nailed it: Xi has destroyed the confidence of foreign investors. He gave the world a glimpse into what the CCP’s end game is (and it doesn’t include foreigners). He was too early. And now he has lost the ability to take advantage of stupid foreigners (well some of them anyways - Macron still seems keen).

-

Here is some constructive feedback: 1.) my guess is Fairfax earns $160/share in 2023. That is a 5.2 PE. I expect earnings per share to grow in 2024 and 2025. So Macy’s is not cheaper today. 2.) liquidation value. My guess is if Fairfax started to sell off its many assets it would realize significant value for shareholders. Of course that isn’t going to happen so it is kind of a useless exercise. My question: is Macy’s going to liquidate parts of the company? 3.) management: the management team at Fairfax has been executing exceptionally well the past 5 years (best in class among insurance companies). They are going to be getting in the range of another $11.3 billion in net earnings over the next 3 years. I have no idea how good the management team at Macy’s is… but are they that good? 4.) insurance is in a hard market. Retail is… in a terrible market that might get worse ( although i did buy a little Aritzia recently). Sanjeev, my read is you are significantly underestimating the current earnings power of Fairfax - like many of the posters on this board. And i love it. Stocks usually climb the wall of worry. PS: i will admit i do not follow Macy’s… but i will do some reading on the weekend. Your banging of the table is what got me back into Fairfax in late 2020. And more recently you nailed META.

-