Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

@AlwaysDay1 my writing is a little unclear at times… i am saying 2 things will likely bump interest and dividend income to over $500 million in Q3: 1.) incremental interest earned from $1.8 billion PacWest portfolio 2.) incremental interest earned from bonds that mature and are rolled over at higher maturities

-

@LC here is my logic. 10% on $1.8bn = $180mn. But we need to net out what they were earning on the $1.8 billion previously. My guess is 5% = $90 million. So we get $90 million in incremental earnings. Some of this will be investment gains (not dividends) as the bonds were purchased at a discount. So my guess is incremental interest and dividend amount will be $80 million or $20 million per quarter. I didn’t come across the dividend amount. Please share (if anyone else knows).

-

That was the number that slapped me upside the head when i was reading… WOW!

-

Great quarter. Boring. But let’s look under the hood to see what we can learn. Here are three key takeaways: 1.) interest and dividend income = $464.6 million. This is now running at $1.86 billion/year. This does not include: - the higher interest income from the $1.8 billion in PacWest loan portfolio. This closed late in Q2. My guess is this will add $20 million per quarter to interest income. - as bonds continue to mature, Fairfax will be able to re-invest them at a much higher rate. My guess is Interest and dividend income for Q3 will be above $500 million. That would put it at $2 billion per year. That is $86/share. Fairfax is trading at 9.4 x estimated annual interest and dividend income. Holy shit Batman! 2.) combined ratio = 93.9. This was an elevated quarter for catastrophe losses… so this is a very good result. What happened? “…prudent expense management and decreased catastrophe losses.” Reading that in a Fairfax press release is music to my ears. Fairfax said they were decreasing Brit’s exposure to catastrophes and it appears we are seeing the benefits of this play out (probably company wide). My thesis is Fairfax has been slowly improving the quality of their insurance businesses for the last decade (under Andy Barnard’s leadership) and results this quarter support this idea. And how about Allied World’s CR of 91%… this sub looks like it has supplanted Odyssey as Fairfax’s top performing insurance sub. 3.) interest rates spiked late in Q2. We knew Fairfax was going to take a hit on their fixed income holdings in the quarter and now we know the number: a loss of $405.3 million. But this is a great thing for Fairfax. Their balance sheet has completely digested the spike in interest rates we have seen over the past 6 quarters. This is a big deal. Higher interest rates are a big tailwind for Fairfax. Their fixed income portfolio is still pretty low duration (2.5 years at the end of Q1). So lots of bonds will be rolling off every quarter. And Fairfax will now be able to reinvest at much higher rates, locking it in for years into the future. I hope we learn on the conference call what the average duration of the fixed income portfolio was at the end of Q2.

-

@OCLMTL welcome to the wild side (posting). Thanks for sharing your thoughts. I agree with you that the current valuation makes no sense… even with the big move in the share price. we are learning a few things: 1.) Fairfax shares got stupid cheap. So everyone’s starting/reference point is wrong. 2.) The phenomenal growth in the insurance companies over the past decade spiked the earnings power of the company - but low interest rates and Fairfax’s strategy of going low duration hid this increase in earnings power for a couple of years. 3.) the execution by the team at Fairfax is still being grossly under appreciated. Especially what they did with their fixed income portfolio. The spike in earnings is happening. It is sustainable. But few understand or believe. 4.) Investment professionals are still in denial. Its almost like a badge of honour in the industry to say ‘i haven’t followed Fairfax for the past five years’ and then they follow it up with ‘oh, and don’t invest in that company… its a mess.’ Meanwhile their clients portfolios underperform. Psychology is such an important part of investing. I was talking to a family member about Fairfax tonight (they are way up on their investment) and they asked me if it was time to sell and lock in crazy big gains? I said ‘forget how much you are up for a second. You own a well run company and it is trading at 5.5 x earnings and its future prospects are very good. What do you think you should do?’ They got a blinding glimpse of the obvious - they decided to stay invested. I probably should have told them to stop looking at the stock price every day… hard when it keeps hitting fresh all time highs.

-

@Maxwave28 your understanding is correct. When i do my updates i use the old accounting logic as much as possible. And 4.) becomes a plug kind of number. We will learn more about IFRS 17 when Fairfax reports tomorrow. My expectation is it will impact 4.) My hope is, over time, we will slowly learn what drives 4.) and how much (like changes in interest rates). So we can make educated guesses in models. Right now i feel like i am flying a little blind. I am not concerned.

-

@steph you are welcome. I learn so much from other posters… and what i learn usually makes its way into my future posts. This is a great community. We are very lucky right now. I have been following Fairfax for about 20 years. Only 2 other times has the set up looked as favourable as it does today: 2003 (short attack) and 2006/07 (short attack when they were sitting on giant CDS position). We all need to thank the gods for how everything with Fairfax has played out over the past 33 months. It has been a crazy wonderful ride. And the stock still trades well under 6 x 2023E earnings. Nuts.

-

@nwoodman great comment. But i would take it a step further. I think Fairfax has been winnowing the vast collection of contacts they have. I think they know today who the top performers are. And the top performers are the ones getting the cash. And this has been happening for a few years. How will we know? Future results… when they keep surprising to the upside.

-

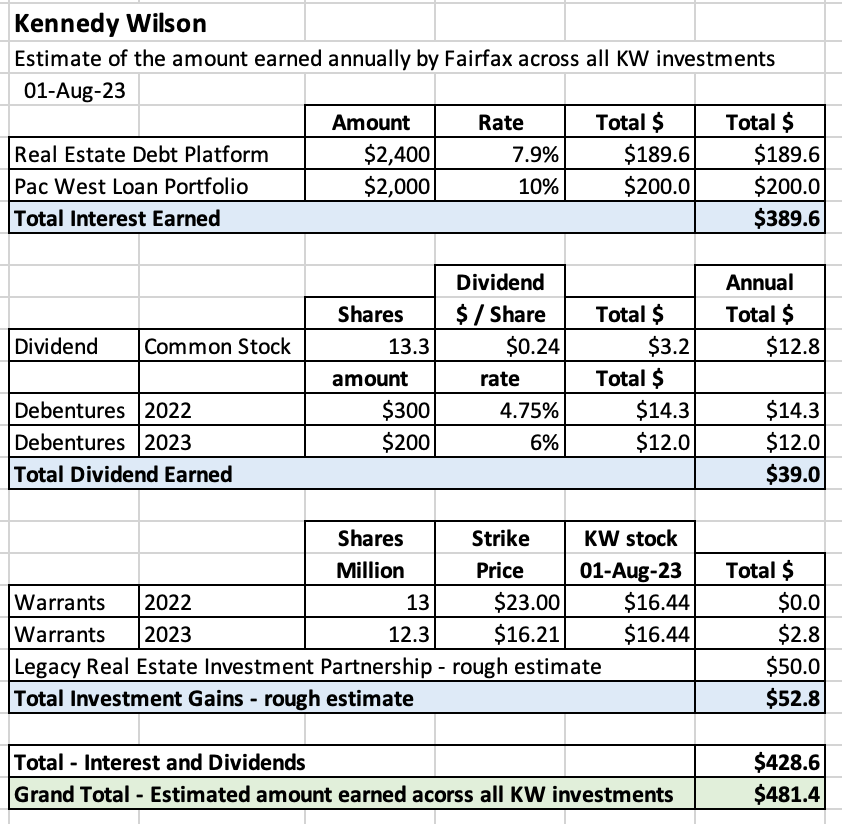

Kennedy Wilson is a misunderstood and underappreciated part of Fairfax’s investment portfolio. Most investors think of Kennedy Wilson through the lens of an equity holding. Looking at the performance of KW’s stock price the past 5 years… what a dog! Woof! KW shares were trading around $21.40 five years ago and today they closed at $16.44/share. What a terrible investment by Fairfax. Right? Wrong. Kennedy Wilson has been one of Fairfax’s best investments. What is wrong with the analysis above? It completely misses the point of WHY Fairfax is invested in Kennedy Wilson – it is to tap into Kennedy Wilson’s extensive global real estate expertise. First, let’s do a quick review. Fairfax began its relationship with Kennedy Wilson in 2010. A very successful real estate investment partnership has recently blossomed to now include a significant real estate debt platform. Over the past 3 years, Kennedy Wilson has become a much more important part of Fairfax’s investment portfolio. The partnership now includes both equity and fixed income investments: 2010: $100 million direct investment in Kennedy Wilson stock 2010: Real estate investment partnerships 2020: Real estate debt platform 2022: $300 million debenture (4.75%) 7-year warrants for 13 million common shares with strike price of $23. 2023: Purchase of $2.3 billion in real estate loans from PacWest 2023: $200 million debenture (6%) 7-year warrants for 12.3 million common shares with strike price of $16.21 Roughly, how much does Fairfax currently earn annually from its different investments with Kennedy Wilson? My very rough estimate is around $481 million. Fairfax has about $5.7 billion invested with Kennedy Wilson so this represents about a 8.4% annual rate of return for Fairfax (mostly interest and dividends). Of this total, about $429 million is interest and dividends. The PacWest loan transaction just closed so the incremental earnings from this investment will start to show in the interest and dividend income bucket starting in Q3. The expansion of the relationship with Kennedy Wilson provides another good example of how Fairfax over the last 5 years has been: Leveraging and expanding existing, successful, long-term partnerships Methodically diversifying their investment portfolio - in this case into real estate The result is yet another new, growing, significant and steady stream of earnings for Fairfax. ————— What is the timeline of Fairfax’s various investments in/with Kennedy Wilson? Started in 2010 Kennedy Wilson (KW) stock initial equity investment was US$100 million (9% of company) today position is worth $200 million (13.3 million shares x $14.98/share) current annual dividend of $0.96 = 6.4% yield = $12.8 million in dividend income per year Wade Burton is on the board (along with Stanley Zax, who sold Zenith to Fairfax in 2010) investment partnership: started with $278 million in 2010 Prem’s 2022 letter: “we have invested $1.2 billion alongside with them in real estate, have received cash proceeds of $1.1 billion and still have real estate worth about $570 million. Our average annual realized return on completed projects is approximately 22%.” Expanded in 2020 Launched a real estate debt platform: to pursue first mortgage loans secured by high-quality real estate in the Western U.S., Ireland and the U.K. 2020 = initial amount of $2 billion 2022 = increased to $5 billion Prem’s 2022 letter: “$2.4 billion invested through Kennedy Wilson in well-secured first mortgages, primarily on high quality residential apartment buildings, at a floating rate (currently 7.9%)” = $190 million in interest income. Expanded further in 2022 2022: KW perpetual preferred equity investment = $300 million pays an annual dividend of 4.75% = $14.25 million includes 7-Year warrants for 13 million shares at strike price of $23/share. Expanded further in 2023 PacWest debt purchase of $2.3 billion: KW is buying loans at a discount for $2.1 billion, of which Fairfax is buying $2 billion (95%). Fairfax is also assuming $1.7 billion in future funding obligations. Average loan to value is 51%. More than 70% of the loans relate to multifamily or student residences; the remainder are a mix of industrial, hotel and life sciences office property projects. Fairfax expects the average annual return to exceed 10%. Remaining term to maturity is 1.7 years, with some loans carrying extension rights (max 2 years). 2023: KW perpetual preferred equity investment = $200 million pays an annual dividend of 6% = $12 million includes 7-Year warrants for 12.3 million shares at strike price of $16.21/share. Ownership of stock: Kennedy Wilson has 139.4 million shares outstanding Fairfax owns 13.3 million = 9.5% Fairfax also owns warrants: 13 million at $23 12.3 million at $16.21 If Fairfax exercises all warrants it would own 38.6 million shares = 23.4% (164.7 total) Fairfax is getting paid 4.75% and 6% while waiting for the warrants to get in the money (they have seven years). What does Fairfax see in Kennedy Wilson? Prem’s comment from the 2022 press release from Kennedy Wilson announcing the PacWest transaction: “We are pleased to make this new investment in Kennedy Wilson and to build on our outstanding partnership that dates back to 2010,” said Prem Watsa, Chairman and CEO of Fairfax. “We believe in their global business model, the strength of their high-quality, income-generating assets, and their best-in-class management team.” https://ir.kennedywilson.com Q4 2022 Investor Presentation: https://ir.kennedywilson.com/~/media/Files/K/Kennedy-Wilson-IR-V2/reports-and-presentations/presentations/q4-2022-investors-presentation.pdf ————— Interesting trivia point: Bill McMorrow (CEO and Chairman of KW) was the genesis behind Fairfax's investment in Bank of Ireland in 2011. Fairfax made around $1 billion from that one investment. Thank you, Bill! (see Prem's comments below from 2011AR) ————— 2020: Kennedy Wilson and Fairfax Launch New $2 Billion Real Estate Debt Platform https://ir.kennedywilson.com/news-events-and-presentations/press-releases/2020/05-14-2020-105955816 “Kennedy Wilson and Fairfax first invested together in 2010 when the two companies acquired $250 million of real estate assets, including real estate secured loans and real property. Over the past decade, the companies have partnered on $7 billion in aggregate acquisitions, including over $3 billion of real estate related debt investments. In addition, Fairfax currently has an equity ownership interest in Kennedy Wilson of approximately 9%.” 2022: Kennedy Wilson Announces $300 Million Perpetual Preferred Equity Investment From Fairfax Financial https://ir.kennedywilson.com/news-events-and-presentations/press-releases/2022/02-23-2022-211613501 “Kennedy Wilson and Fairfax began their relationship in 2010 when Fairfax made a $100 million equity investment in Kennedy Wilson. Over the past decade, the companies have partnered on $8 billion in aggregate acquisitions, including approximately $5 billion of real estate related debt investments. Fairfax currently has an equity ownership interest in KW of approximately 9%.” ————— 2023: Fairfax Financial Partners With Kennedy Wilson to Acquire Loan Portfolio From Pacific Western Bank, Makes Additional Equity Investment in Kennedy Wilson https://www.fairfax.ca/press-releases/fairfax-financial-partners-with-kennedy-wilson-to-acquire-loan-portfolio-from-pacific-western-bank-makes-additional-equity-investment-in-kennedy-wilson-2023-06-05/ Kennedy Wilson’s Press Release https://ir.kennedywilson.com/news-events-and-presentations/press-releases/2023/06-09-2023-110020523 “The acquisition of this Loan Portfolio from Pacific Western Bank highlights Kennedy Wilson’s historic ability to find off-market transactions during periods of uncertainty, move with speed, and build on our successful track record of investing through all real estate cycles,” said William McMorrow, Chairman and CEO at Kennedy Wilson. “The foundations of Kennedy Wilson are our deep relationships, our reputation as a great partner, and our strength in being nimble when opportunity arises; all of which came into play with this loan portfolio acquisition.” ————— 2022AR Prem: “Since we met Bill McMorrow and Kennedy Wilson in 2010, we have invested $1.2 billion alongside with them in real estate, have received cash proceeds of $1.1 billion and still have real estate worth about $570 million. Our average annual realized return on completed projects is approximately 22%. We also own 10% of the company. More recently we have been investing with Kennedy Wilson in first mortgage loans secured by high quality real estate in the western United States, Ireland and the United Kingdom with a loan-to-value ratio of 60% on average. At the end of 2022, we had invested in $2.0 billion of mortgage loans in the U.S. at an average yield of 8.1% and an average maturity of 1.7 years, and in approximately $350 million of mortgage loans in the U.K. and Europe at an average yield of 6.0% and an average maturity of 2.5 years.” “The combination of interest and dividends and profit from associates accounted for a 3.7% return on our portfolio in 2022, the highest return in the last five years (average 2.5%). We expect to earn these returns in 2023 as well, partly because we have $2.4 billion invested through Kennedy Wilson in well-secured first mortgages, primarily on high quality residential apartment buildings, at a floating rate (currently 7.9%).” ————— 2013AR: “The KWF LPs are partnerships formed between the company and Kennedy-Wilson, Inc. and its affiliates to invest in U.S. and international real estate properties. The company participates as a limited partner in the KWF LPs, with limited partnership interests ranging from 50% to 90%. Kennedy-Wilson holds the remaining limited partnership interests in each of the KWF LPs and is also the General Partner. For the KWF LPs where the company may exercise veto rights over one or more key activities, those partnerships are considered joint ventures under IFRS 11. Where the company has no veto rights over key activities, the company is considered to have significant influence under IAS 28. The equity method of accounting is applied to all of the KWF LPs.” ————— 2011AR Prem: “I have attended the Berkshire Hathaway shareholders’ meeting since there were only 200 shareholders in attendance about 30 years ago. I still find I learn something each year from Warren and Charlie. At the meeting in 2010, I met Bill McMorrow through Alan Parsow, who is a money manager based in Omaha and a great friend. Bill founded Kennedy Wilson, a real estate services and investment company, in 1988, and he now owns 26% of the company. As a result of this meeting, we invested $100 million in a Kennedy Wilson 6% preferred convertible at $12.41 per share, and later purchased $32.5 million of a 6.45% preferred convertible at $10.70 per share and 400,000 common shares at $10.70 per share. Fully diluted we own 18.5% of the company. In 2010 and 2011, we also invested $290 million in several real estate deals with Kennedy Wilson in California, Japan and the U.K. – deals at significant discounts to replacement cost and with excellent unlevered cash on cash returns, in which Kennedy Wilson is the managing partner and a minority investor. We are thrilled to be partners with Bill and his team, who always focus on the downside and have the expertise to manage these investments and finally harvest them. You never know what you will find at a Berkshire meeting!!” “And there is more to the McMorrow story. While Bill was negotiating the purchase of some real estate loans from Bank of Ireland, he was really impressed with Ritchie Boucher, the Bank’s CEO. Bill introduced Ritchie to us, and we too were very impressed. With the help of our friends at Canadian Western Bank, one of the best banks in Canada, we thoroughly reviewed the opportunity and then quickly formed an investment group with Wilbur Ross, Mark Denning from Capital Research and Will Danoff at Fidelity, which purchased $1.6 billion of Bank of Ireland shares on a rights issue (Fairfax’s share was $387 million).”

-

@nwoodman thanks for posting the article. Eurobank’s guidance for EPS was increased from €0.22/share to €0.28/share. Shares closed today at €1.59/share. I am wondering if the earnings of Fairfax’s various associate and consolidated equity holdings will exceed expectations when they report on Thursday. Eurobank is the biggest, so we are already off to a great start. Recipe? Thomas Cook?

-

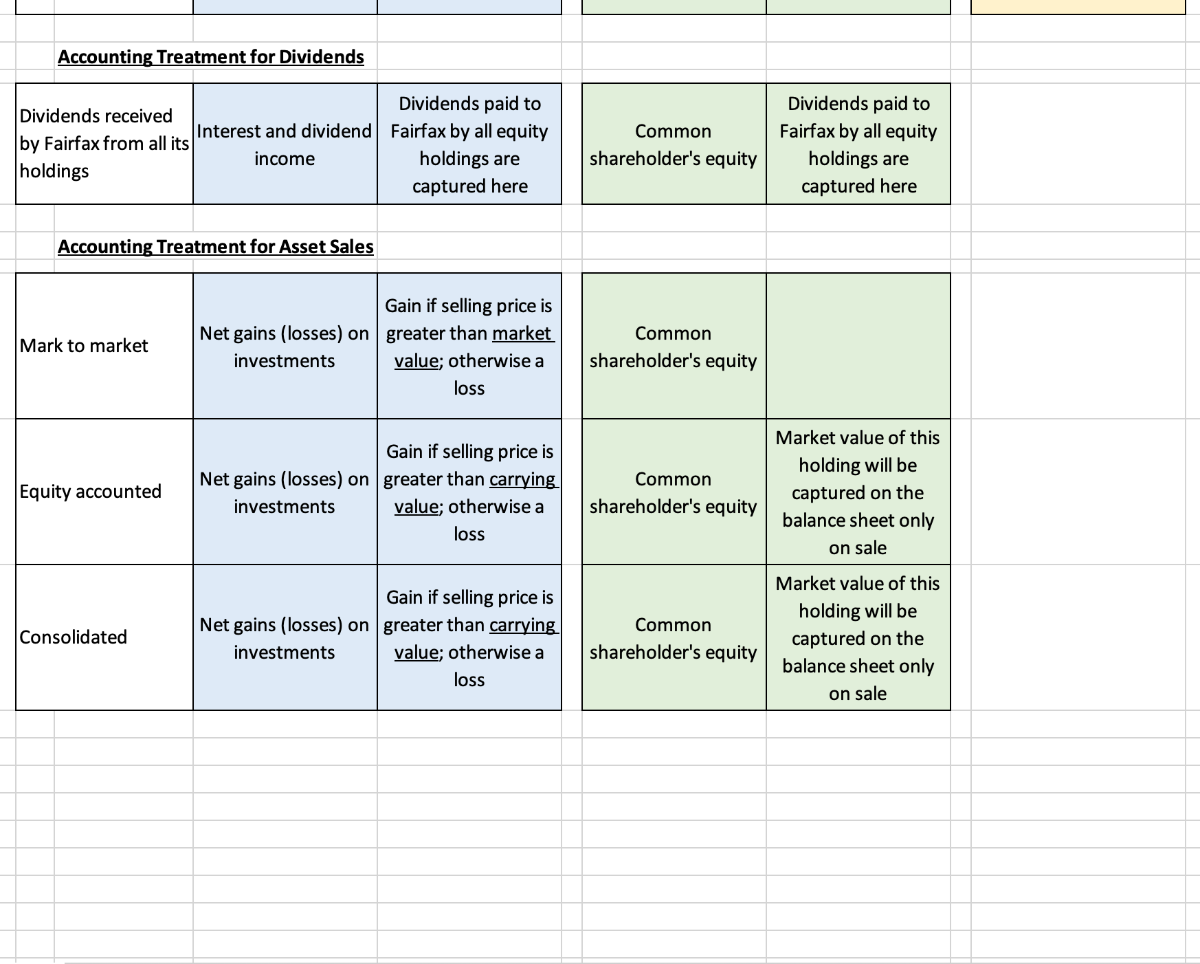

I need the help of board members. It can be confusing to understand how the business results of Fairfax's vast collection of equity holdings flows through to Fairfax's income statement and balance sheet at the end of each quarter. I have put together a 'cheat sheet' with 'rules of thumb' to help investors better understand this flow. Does this look generally accurate? What is wrong? What is missing? Can the layout be improved? Please feel free to rip it apart (you won't hurt my feelings). Comment on this thread or private message me. Thanks! PS: it is one sheet, but I copied it with two pictures so it can be more easily read.

-

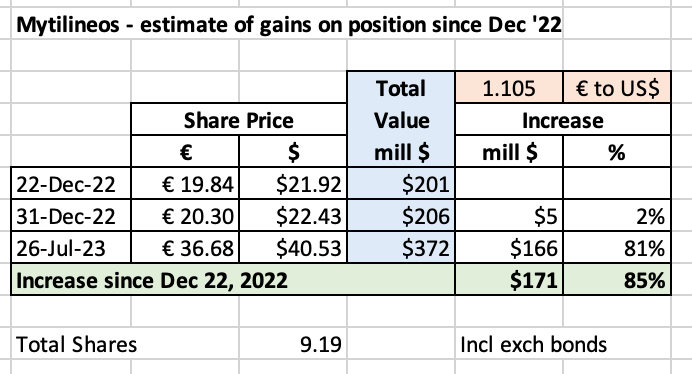

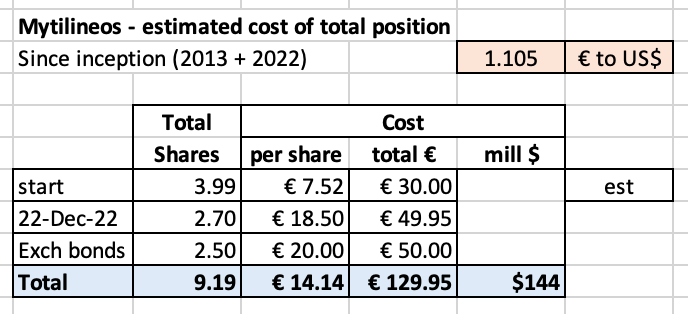

Mytilineos shares have been on a tear in 2023. Here is an short update of what it means for Fairfax. Who is Mytilineos? Ticker: MYTIL.AT (trades on the Athens stock exchange) Stock price: $36.68 (July 26, 2023) Market cap: €5.07 billion Dividend = €1.24 = 3.4% From the company’s web site: “MYTILINEOS Energy & Metals is a global industrial and energy company covering two business Sectors: Energy and Metallurgy. The Company is strategically positioned at the forefront of the energy transition as an integrated utility, while already established as a reference point for competitive green metallurgy at the European and global level. It has a consolidated turnover and EBITDA of €6.35 billion and €823 million, respectively, and employs more than 5,442 direct and indirect employees in Greece and abroad.” Corporate presentation Jun 2023: https://www.mytilineos.com/media/k5lj10q0/corporate_presentation_june_2023.pdf How much of Mytilineos does Fairfax own? Fairfax owns 9.19 million shares (including the exchangeable bonds) with a value of $372 million. This makes the company a top 15 holding in Fairfax’s equity portfolio. Fairfax made its first investment in Mytilineos in 2012 or 2013 (€30 million stake). In November of 2022, Fairfax owned 3.99 million shares. In December 2022, Fairfax more than doubled their stake: they purchased 2.7 million shares at €18.50. they purchased exchangeable bonds that gives them the right to buy another 2.5 million shares at €20. Fairfax is now the second largest shareholder. How has the investment performed since Fairfax added to their position in December, 2022? Fairfax’s position is up $171 million or 85% over the past 8 months. ————— October 21, 2013: Canada's Fairfax buys Mytilineos stake in second bet on Greece https://www.reuters.com/article/us-greece-fairfax/canadas-fairfax-buys-mytilineos-stake-in-second-bet-on-greece-idUSBRE99K05H20131021 December 13, 2022: Fairfax becomes the 2nd largest shareholder in MYTILINEOS https://www.mytilineos.com/news/company-news/fairfax-becomes-the-2nd-largest-shareholder-in-mytilineos ---------- Estimated cost to Fairfax of total position (very rough) My estimate below of €14.14 is likely high. It does not include dividends, which Mytilineos has paid since 2018. And my estimate of €7.52 for the initial 3.99 million shares is a guess. Given the large size of the position, Fairfax will likely give us the correct number in a future annual report.

-

I don’t even know where to begin. $50? Really? But hey, if a $50 fee is keeping idiots like that off this board… well, that is priceless!

-

Timely lessons from Buffett's 1999 Fortune article

Viking replied to LearningMachine's topic in Berkshire Hathaway

@LearningMachine great trip down memory lane. Thanks for posting. Lots about investing has not changed much. For small investors, costs have come way down. And much better information is available. What hasn’t changed with small investors? If i had to pick one thing it is probably psychology… still making the same mistakes. -

As i mentioned in my previous post, the closing of the Gulf Insurance Group (GIG) deal (Q4?) - boosting Fairfax’s ownership to 90% - will be an important growth driver of Fairfax’s 2024 results. GIG recently updated their web site. They added a bunch of new information. Below is the link to a 40 page report that provides a great overview of the company. - https://www.gulfinsgroup.com/Frontend/EN/GIG-Corporate-Profile-ENG.pdf?download=false Here are the financial highlights (2022): Net premiums written = $1.7 billion Underwriting surplus = $164 million Total Investments = $2.4 billion Shareholders equity = $748 milion Net profit = 125 million (Q1, 2023 = $34 million) The purchase price of the 46% owned by Kipco is $860 million. However, the true cost to Fairfax is far less, due to the time value of money. Fairfax will pay $200 million at close and then 4 annual instalments of $165 million. If we use an 10% discount rate, the cost to purchase Kipco’s stake when it closes in Q4 is closer to $700 million ($200+$149+$134+$120+$108). This is a good example of solid capital allocation on the part of Fairfax. They are paying a premium for quality. That is interesting. They are also playing the long game with this purchase as it is a very strategic purchase for them that solidifies their presence in the MENA region. It is also anther example of using their current robust cash flow to take out a partner in a business they understand very well.

-

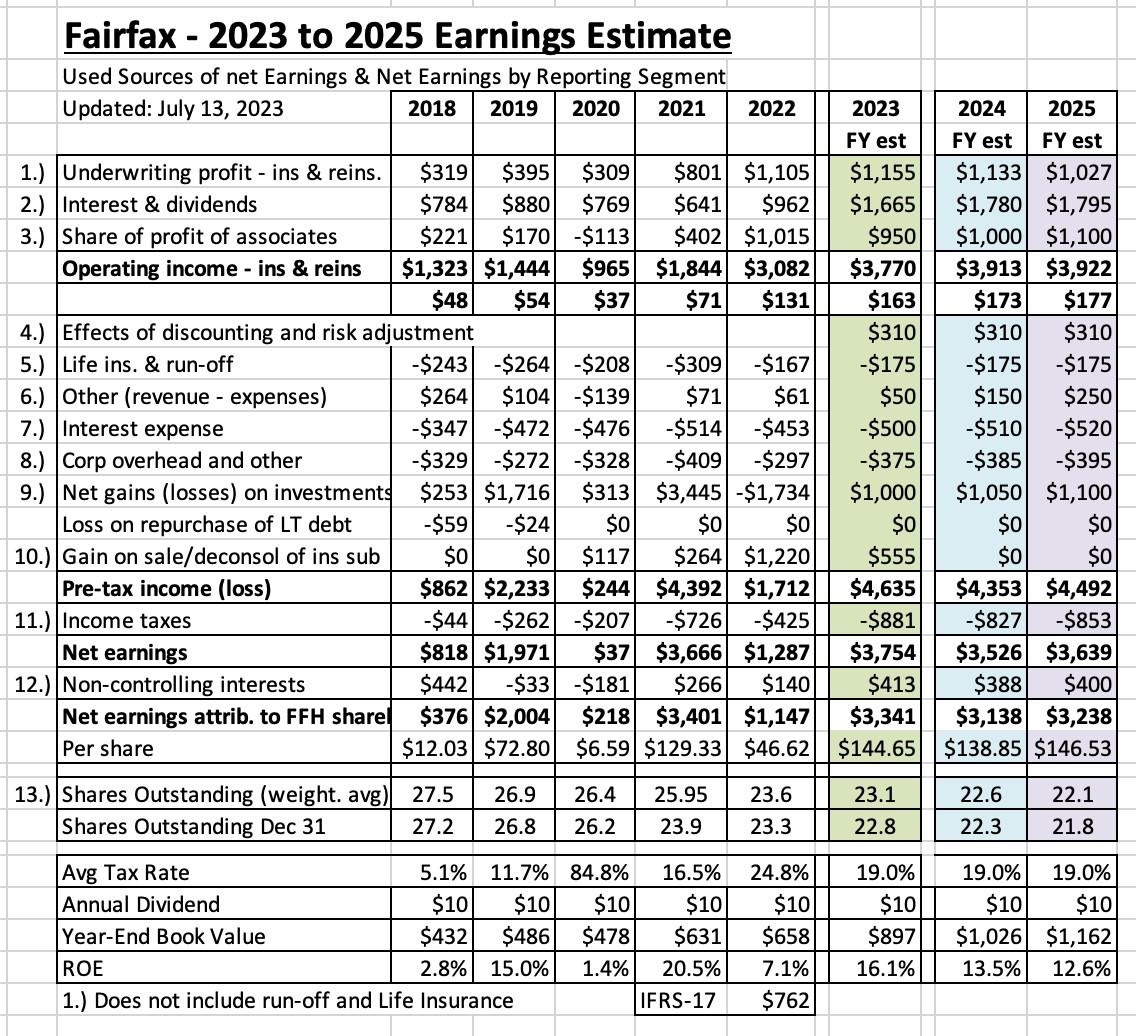

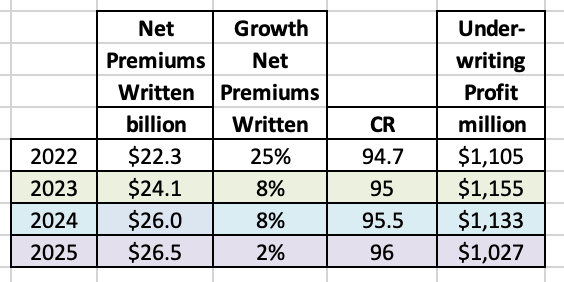

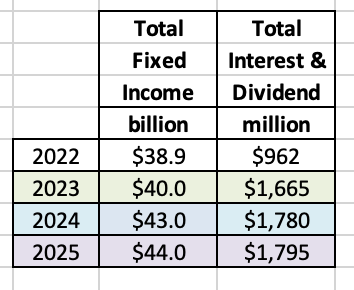

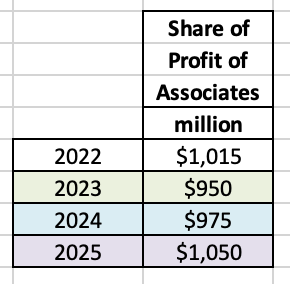

As we begin Q3, this is a good time to update earnings estimates for Fairfax for 2023. And look ahead to 2024. I am also going to take a stab at 2025. I don’t like to go much beyond 2 years with earnings estimates - there are simply to many moving parts. But it useful to get a three year view on earnings to better be able to value the stock price today - so lets give it a shot. My first big learning has been: the GIG acquisition is going to be a material development for Fairfax when it closes. I need to get up to speed with GIG (I may need to revise my estimates below). Please chime in with your thoughts. Too optimistic? Too pessimistic? Any thoughts on what GIG is going to deliver? What important things are missing? Please get into the weeds. Conclusion: Let's skip ahead to the conclusion. My estimate is Fairfax will earn about $140/share, on average, over the next three years. I consider this to be a mildly conservative estimate - what i mean by that is i think it is more likely that earnings will come in higher than lower. The big ‘miss’ with my estimates is capital allocation. We don’t know much of what the management team at Fairfax is going to do with all the earnings (around $3.2 billion) coming each of the next 3 years. Looking at the last 5 years, the management team has been best-in-class with capital allocation. My guess is they will continue to make good decisions (on balance) and this will benefit shareholders - providing a tailwind to my forecast. I am also assuming interest rates remain roughly at current levels. Of course this will not be the case. But if rates rise - or go lower - Fairfax will have lots of puts and takes. I am also forecasting no impact from IFRS 17 (as I have stated before, I am still learning how this accounting change affects Fairfax’s reported results over time.) I love the following 8-year snapshot of Fairfax. It communicates really well the dramatic transformation that has happened at the company beginning in 2021. It is a pretty amazing story. What are the key assumptions? 1.) underwriting profit to be flat to slightly down. Estimates for both premium growth and CR are conservative. When the GIG transaction closes (Q4?) Fairfax will be getting a big boost to its insurance business. I think GIG might be adding $1.8 billion to net written premiums. GIG is the driver to top line growth of 8% in 2024. If the hard market continues into 2024 then top line growth at Fairfax will likely be +10%. I am forecasting Fairfax’s CR to increase from 94.7 in 2022 to 96 in 2025. Do I think this will happen? No. My guess is they will continue to deliver a 95 CR - until I learn something that tells me something new. The hard market will end at some point. But do things quickly turn ugly? Probably not, but not sure. 2.) interest and dividend income: Will increase modestly. Extending the average duration of the fixed income portfolio to 2.5 years largely locks in these numbers. Tailwinds: GIG: will add about $2.4 billion to total investment portfolio. At estimated total return of 4.5% = $110 million. I expect the majority of this would be interest income. PacWest loans: $100 million incremental ($200 million total) to interest income? Half in 2H, 2023 and half in 1H, 2024. Eurobank: likely dividend starting in 2024 = $60 million? Headwind: Short term treasury rates likely come down lowering interest on cash/short term balances. 3.) Share of profit of associates: Will increase modestly. It fell in 2023 because of the sale of Resolute Forest Products - who contributed $159 million in 2022. GIG purchase will subtract $80 million in 2024 (same as what is built in for 2023). growing earnings at Eurobank and Poseidon/Atlas will power this higher. My estimates for Stelco and EXCO are very conservative (a combined total of $110 million per year). 4.) Effects of discounting and risk adjustment (IFRS 17). Interest rate changes drive this bucket. I need time to learn how much. Given I am forecasting interest rates to remain about where they are today I am leaving this number the same over the forecast period. 5.) Life insurance and runoff. This combination of business lost $167 million in 2022. I am forecasting this bucket to lose $175 million in each of the next three years. We should expect Eurolife to grow its earnings nicely over time. 6.) Other (revenue-expenses): improving results from consolidated holdings. In the near term, perhaps we get write downs in both Boat Rocker and Farmers Edge. Recipe should deliver solid and growing earnings of better than $100 million per year. Earnings at Dexterra are growing again. AGT is a sleeper holding. Grivalia Properties is in its peak investment phase; earnings should grow nicely looking out a year or two. This bucket could really start to shine through for Fairfax in the coming years. 7.) Interest expense: modest increase. 8.) Corporate overhead and other: took the average of last 3 years and added 10% 9.) Net gains on investments: This is a wild card. My estimates assume: mark-to-market equity holdings of $7.8 billion increase in value by 10% per year = $800 million. there is a small bump of $200-$300 million per year in additional gains (equities and fixed income). Total return on investment portfolio is: 2023 = 7.5% 2024 = 6.8% 2025 = 7.0% (I get this by adding up the following line items: 2.) + 3.) + 6.) + 9.) and divided the total by the value of their investment portfolio). These percent returns, while high compared to recent years, are hardly heroic given Fairfax is currently earnings about 4% on their fixed income portfolio. 10.) Gain on sale/deconsol of insurance sub: this is where I put the really large monetizations. 2022 was the sale of pet insurance and Resolute. 2023 was the sale of Ambridge and the purchase of GIG (resulting in a write up of the existing holding). I am building in nothing for 2024 and 2025 and this is highly unlikely. We likely will get a Digit IPO at some point over the next year and this could result in a significant gain for Fairfax. We could get an event that triggers a revaluation of Eurobank (carrying value is currently $500 million below market value and this will likely widen significantly in the coming years). We could see an AGT IPO. Fairfax is likely to sell another large holding for a significant gain. Bottom line, this is probably where I will be most wrong with my forecast. Developments here will have a material positive impact to Fairfax’s reported results (earnings and book value). 11.) Income taxes: estimated at 19% 12.) Non-controlling interests: estimated at 11% (not really sure) 13.) Shares Outstanding: reduced by 500,000 per year. This is in line with a normal year from Fairfax. It would not surprise me to see Fairfax do one more big repurchase to take advantage of the low share price while it lasts.

-

Thanks for giving me my belly laugh for the day i really appreciate it!

-

@glider3834 thanks for all the links to articles that you post. You are quite the blood hound finding interesting and important developments that are relevant to Fairfax. i agree, Cypress is a region to watch (quite profitable). I have been very impressed with capital allocation decisions made at Eurobank over the past few years. I think they were short duration on their fixed income portfolio at the end of 2021 (sound familiar). The purchases of the stakes in Hellenic Bank (you posted) were a steal. And the sale of the Serbian assets (in a non-core market) at a good price looks smart amd well timed (provide the funds to growth in Cypress, a core market). Scale really matters in banking. And it is becoming even more important. The big boys really do have massive advantages over smaller players. Makes sense we should see alot of consolidation in the coming years. Should benefit the big boys.

-

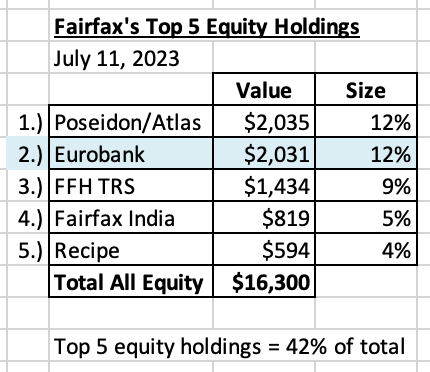

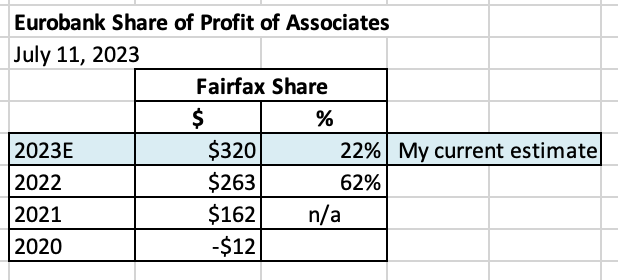

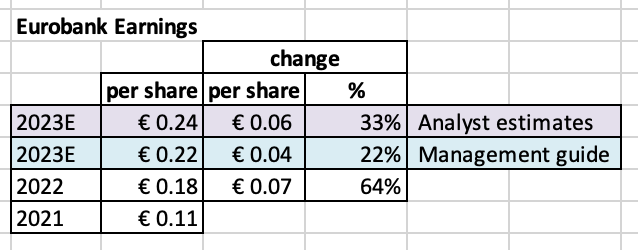

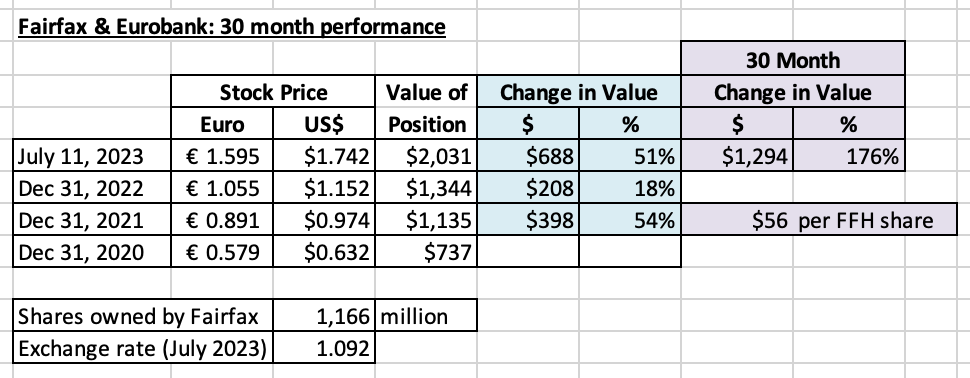

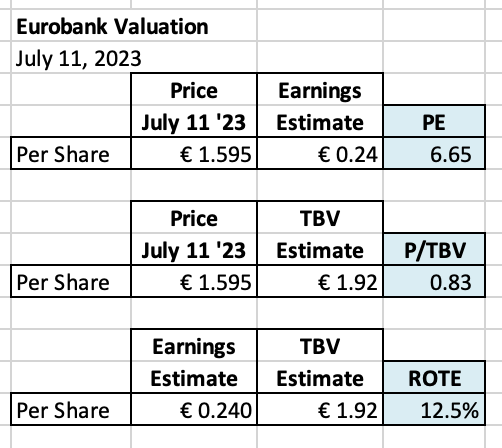

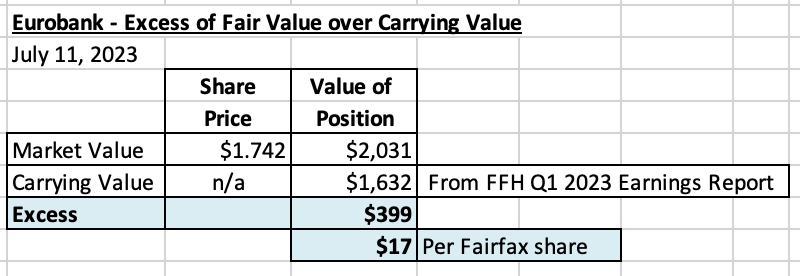

@nwoodman thank you for providing the MS report. It motivated me to write an update on Eurobank. Eurobank's stock is one again hitting all time highs (€1.595 today). It is now tied with Poseidon/Atlas as Fairfax’s largest equity holding. Time to do a review of what has been Fairfax’s best performing equity holding over the past couple of years. This review will focus on the numbers and will be mostly forward looking. Who is Eurobank? Eurobank is one of the largest banks in Greece (and the region). Its core markets are Greece, Bulgaria and increasingly Cypress. It is recognized as being one of the best managed banks in Greece. Q1, 2023 Management Presentation: https://www.eurobankholdings.gr/-/media/holding/omilos/grafeio-tupou/etairikes-anakoinoseis/2023/1q-2023/1q2023-results-presentation.pdf Of interest, Eurobank, Eurolife and Grivalia (all Fairfax holdings) are all joined at the hip. More on this in another post. Let’s start by looking at the big picture. What are prospects for the Greek economy? Greece is positioned very well right now. The Greek economy turned the corner a couple of years ago now. Tourism is booming. As is the property market. Prime Minister Mitsotakis (center-right) was just re-elected with another majority for a second consecutive 4-year term. This ensures the significant economic (pro-market) reforms to the Greek economy will continue. Greece is expected to have one of the better performing economies in Europe over the next couple of years. This is a very positive backdrop for Eurobank. How much of Eurobank does Fairfax own? Fairfax owns 32.2% of Eurobank (1.166 billion shares). A stake worth $2 billion today. Timeline of key events for Fairfax and Eurobank: Dec 2014: FFH investment #1 in Eurobank of $444 million for 12.5% position Nov 2015: FFH investment #2 in Eurobank (recapitalization) of $389 million for 17% position Dec 2015: FFH purchase of 80% of Eurolife from Eurobank for $360 million May 2019: Eurobank recapitalization / merger with Grivalia Properties - Fairfax owns 32.4% July 2022: Fairfax increases stake in Grivalia Hospitality from 33.5% to 78.4% (from Eurobank) for $195 million Importantly, Eurobank is Fairfax’s minority partner in Eurolife and Grivalia Hospitality. How important is Eurobank to Fairfax? Eurobank is tied with Poseidon/Atlas as Fairfax’s largest equity holding. With a market value of $2 billion, Eurobank represents about 12% of Fairfax’s total equity holdings of around $16.3 billion. For context, Fairfax has an investment portfolio of about $56 billion, with fixed income investments of $40 billion and equities of $16.3 billion. What is the trend for earnings at Eurobank? Earnings have been on a steady upwards trajectory in recent years. Management is guiding to earnings of €0.22/share in 2023. Management is conservative with their forecasts. Analysts are expecting earnings to come in around €0.24/share in 2023. How has the stock price of Eurobank performed? Eurobank’s stock price has been spiking higher - it is up 176% over the past 30 months. The market value of Fairfax’s position in Eurobank is up $1.3 billion over the past 30 months, or $56 per Fairfax share. Clearly, Mr. Market is recognizing and rewarding the improving fundamentals and results at Eurobank. How is Eurobank stock valued today? Despite the 176% increase over the past 30 months, Eurobank’s stock is still cheap (sound familiar?). The stock is trading at a forward price earnings of 6.65; price to tangible book value of 0.83; return on tangible equity of 12.5%. Note: I used the analysts guide for EPS for 2023 of €0.24/share because it is the likely number. Morgan Stanley currently has a price target for Eurobank of €2.10/share = $2.29/share. With shares trading at €1.595 today this suggests 32% upside. Currently 79% of analysts who follow Eurobank have the stock rated ‘Overweight’. Of interest, if Eurobank traded at €2.10/share, Fairfax's position would be worth $2.675 billion. How is Eurobank valued on Fairfax’s books? Eurobank is not a mark-to-market holding for Fairfax. Since Jan 1, 2020 it has been a consolidated holding (equity accounted). At March 31, 2023, Eurobank had a carrying value at Fairfax of $1.6 billion. So as of today there is an excess of $400 million of market value over carrying value ($17/share pre-tax). This excess is not captured in Fairfax’s reported financial results (although they do highlight it in their commentary). This is a good example of where Fairfax’s book value is understated. How do results at Eurobank flow though to Fairfax? Dividends. Eurobank currently does not pay a dividend. The plan is for Eurobank to start paying a dividend in 2024. In Q1 2023, Eurobank said they are targeting a minimum payout ratio of 25% - for both dividend and buybacks - in 2024. Let's assume Eurobank goes with a payout ratio of 20% for the dividend. This would likely mean an annual dividend of around €0.048/share. In this scenario, Fairfax would start receiving dividends of $61 million per year. For context, Fairfax currently receives about $135 million in dividends per year from all their various holdings. A dividend from Eurobank would increase this amount by 45%. This would be significant for Fairfax. Something to watch for in 2024. Share of profit of associates. Eurobank is a big reason we are seeing ‘share of profit of associates’ at Fairfax spike to over $1 billion per year in recent years. And as Eurobank grows earnings ‘share of profit of associates’ at Fairfax will only grow more. Investment Gains. Down the road, as Eurobank gets more fully valued, Fairfax could start to sell down its large position. That would crystallize any 'excess of fair value over carrying value'. Today the 'excess' is $400 million. How much has Fairfax earned from this holding since inception? Fairfax is up about $935 million or 85% over the 8.5 years it has owned Eurobank. Fairfax 2019AR Prem’s Letter: “The animal spirits are coming back to Greece and we think the Greek economy and Greek companies will thrive. Eurobank should benefit!! Our cost of 1.2 billion shares of Eurobank after the Grivalia transaction is now 94¢ versus a book value of approximately 135¢ per share post the transaction. At year end, Eurobank was selling at 68% of book value and 6.5x normalized earnings. We still believe it will be a good investment for us.” Conclusion Despite getting off to a terrible start in 2014, Eurobank has turned into a very good investment for Fairfax. This has only happened due to the hard work over many years from the Eurobank team in Greece, lead by CEO Fokion Karavias and Vice Chairman George Chryssikos. Having a long-term oriented, strong, supportive and patient partner in Fairfax also helped greatly. Most importantly, Eurobank is poised to perform even better in the coming years. Given it is such a large holding this should benefit Fairfax shareholders greatly. Making the initial investment in Eurobank also had important added benefits for Fairfax. It led Fairfax to buy 80% of Eurolife which has been an exceptional investment. It also led them to buy a 78.4% stake in Grivalia Hospitality (it is still early days on this investment). Importantly, Fairfax is viewed as being a trusted and strong foreign investor and partner in Greece.

-

The simplest answer is usually the best. It is obvious Putin is a mole for the West. He was likely recruited in St. Petersburg before his political career got going. He single-handedly has: revitalized NATO convinced Finland and Sweden to join NATO, when neither country wanted to before convinced all countries in Europe neighbouring Russia to quickly and heavily re-arm severed decades old economic linkages with Germany convinced Germany to re-arm set the Russian economy back a generation permanently lowered the living standards of current and future generations of Russian kids killed tens of thousands of young Russian men; turning what was already a demographic problem into a nightmare convinced tens of thousands of Russians to leave their country (lots of whom are educated) accelerated by decades the decline of the Russian state economically, made Russia a vassal state of China Simply amazing what he has accomplished in less than 18 months. And i don’t think he is close to being done.

-

@Madpawn my holding as of today is 100% Fairfax. I just added to Fairfax when it went under C$960. I prefer to primarily hold Fairfax today given how cheap i think it is (and i am way overweight). I have held Fairfax India in the past (i recently sold my small remaining position at just just under $14), and sometimes large stakes. But i use it more as a trading vehicle. That works when a stock moves in a sideways band (like Fairfax India has been the past couple of years). But if/when it pops higher then i am toast. I often get too cute with situations like Fairfax India. Fairfax India is unambiguously cheap. And the potential catalysts are there (big undervaluation, holdings are performing well, BIAL is a jewel/trophy asset, management buying back stock, Anchorage IPO, general interest in India). It has a very good management team. The stock is bumping up against $14, so someone is buying… If it sold off I likely would add back. But it would not surprise me to see the stock just keep powering higher.

-

@newtovalue i have not done a Q2 estimate yet. I will put something together before they report. The problem i am having is understanding the impact of much higher interest rates and IRFS 17. Any insight other posters have on interest rate changes and impact on IFRS 17 would be appreciated

-

@Munger_Disciple i agree. That is why i look at both BV and ROE together. IFRS popped BV for Fairfax but it also depressed ROE. Looking at the two together provides a more accurate picture. If we used old GAAP for Fairfax then P/BV would be a little higher for Fairfax’s (probably a little over 1 x BV) but ROE would be approaching 20% (much higher than peers). It would lead to the same conclusion - Fairfax’s stock is too cheap compared to peers. That is also why i like looking at PE. What other large stock is trading at a 5.4PE today? And the earning are real. And not abnormally high, driven by some one time event - my current mildly conservative estimate is Fairfax will earn an average of $135/year in 2023, 2024 and 2025. There are lots of catalysts am not including that could drive earnings higher (like a Digit IPO, more asset sales etc). And i am still learning about IFRS 17. It will take me 6-12 more months to get more comfortable with all the puts and takes (i am slow to grasp some stuff… but i do get it eventually). So my estimates could be off due to IFRS 17 impacts i do not yet understand.

-

Fairfax’s stock price has a history of selling off around 15% in June-Oct. This makes sense as this is hurricane season, and losses from catastrophes in recent years have been elevated. Last year the stock was trading around $550 in April and $450 in Oct; this decline happened AFTER announcing the pet insurance sale which delivered an after tax gain of $990 million. In 2021, the stock traded at $470 in May and bottomed around $410 in October. Where will the stock trade the rest of this year? No idea. Sometimes history repeats; sometimes it doesn’t. I like to look at it to understand potential outcomes… so i do not get caught by surprise when something happens. If we do get a sell off it makes sense to me that Fairfax would get more aggressive on the share buyback front, but perhaps not until we are on the other side of hurricane season.

-

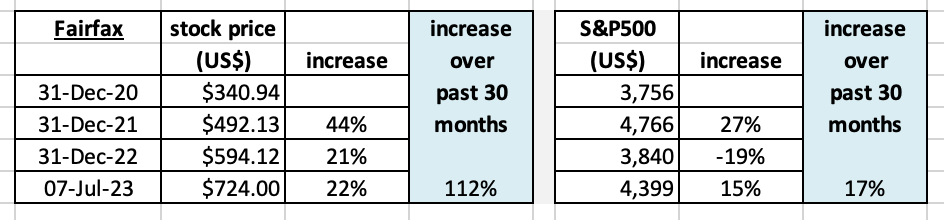

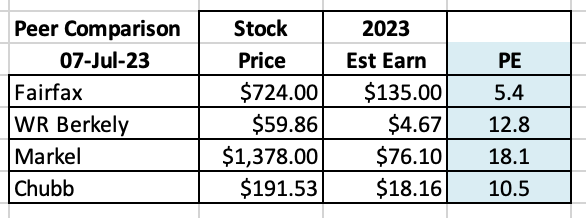

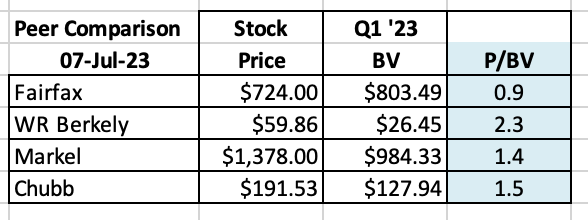

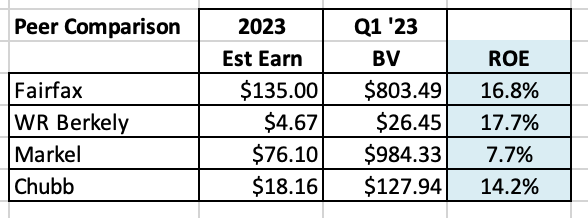

Is the stock priced properly? Efficient market hypothesis: “The efficient market hypothesis (EMH) is a hypothesis that states that share prices reflect all information and consistent alpha generation is impossible. According to the EMH, stocks always trade at their fair value on exchanges, making it impossible for investors to purchase undervalued stocks or sell stocks for inflated prices…” Investopedia A lot has happened at Fairfax over the past 30 months. Let’s do a quick review and see what we can learn. Most importantly, is the stock priced correctly, as the EMH would suggest? How has Fairfax’s stock performed over the past 30 months? First, let’s get some context. Fairfax has been one of the best performing stocks over the past 30 months both in absolute and relative terms. The outperformance has been remarkably consistent each year. Fairfax’s stock has outperformed the S&P500 by 95% over the past 30 months. That outperformance must make Fairfax one of the top performing large cap (in Canada) stocks over the past 30 months. Does this mean the stock is now expensive? The proverbial ‘big fish that got away’ from investors? Let’s find out. Let’s try and keep an open mind. What do the numbers tell us? And what about management? And future prospects? Let’s start by looking at the traditional valuation tools: Price to earnings ratio (PE) My current estimate has Fairfax earning about $145/share in 2023 and $135 in both 2024 and 2025. I view this as a mildly conservative estimate for the next three years. I’ll provide more details in my 3-year earnings forecast for Fairfax - coming in the next week or so. Importantly, the quality of the earnings being delivered by Fairfax are the highest in the company’s history; it is primarily being delivered by record operating earnings (underwriting profit + interest and dividend income + share of profit of associates). All three individually are at record levels. We learn in the chart above that Fairfax is trading today at a forward PE multiple of 5.4 times. That is crazy cheap, especially given the quality and durability of earnings. What is the PE multiple of the overall market? The forward PE multiple of the S&P500 is 20. Fairfax’s stock is trading at a SIGNIFICANT discount to the S&P500. Fairfax’s stock price could double from here and it would still be trading at a 50% discount to the S&P500 multiple. How about compared to some P&C insurance peers? Looking at PE, Fairfax is trading at 48% (Chubb) to 70% (Markel) below peers. Fairfax’s stock looks dirt cheap. But let’s keep digging. Price to book value multiple (P/BV) and return on equity (ROE) Let’s now look at the price-to-book value (P/BV) and return-on-equity (ROE). These two are the preferred metrics used to value insurance companies. Let’s start with P/BV. How does Fairfax stack up compared to peers? Looking at P/BV, Fairfax is trading 36% (Markel) to 61% (WR Berkley) below peers. How about ROE? Looking at ROE, Fairfax is poised to deliver an exceptional 16.8%, at the high end compared to peers. What can we conclude after looking at the valuation metrics? Looking at PE and P/BV, Fairfax’s stock is exceptionally cheap compared to the market and peers. At the same time Fairfax is delivering best-in-class ROE. This makes no sense. Let’s keep digging. What about management? I recently did a long-form post where I reviewed capital allocation at Fairfax over the past 5 years. Bottom line, it can be argued that Fairfax currently has a best-in-class management team (compared to peers). The mystery deepens. What about the future prospects of Fairfax? Fairfax has three engines driving its business: Insurance: Fairfax has grown net premiums written by 400% over the last 9 years. At a 95CR, underwriting profit is on track to be a record $1 billion in 2023. Investments - fixed income: Fairfax has navigated the spike in interest rates masterfully in their $40 billion fixed income portfolio, moving to 1.2 years average duration in Dec 2021 and then pivoting and moving to 2.5 years average duration in Q1 2023, locking in higher yields. As a result interest and dividend income is expected to be a record +$1.5 billion for each of 2023, 2024 and 2025. Investments - equities: Fairfax’s $16 billion equity holdings have been performing very well, lead by Eurobank and total return swaps on 1.96 million FFH shares. Most importantly, all engines are performing very well at the same time, perhaps for the first time in the company’s history. Significant asset sales over the past 12 months have been icing on the cake: pet insurance ($1.4 billion), Resolute ($626 million+$183 million CVR), Ambridge Partners ($400 million). In short, Fairfax’s prospects have never looked better. What are external groups saying? AM Best, the credit ratings agency who specializes in insurance companies, just upgraded Fairfax’s ratings (including those of its two largest subs - Odyssey and Allied) because of its much improved financial profile. Most sell-side analysts have been warming to Fairfax over the past year, repeatedly increasing their estimates and target prices. Most have Fairfax as ‘outperform’ and a few have it as a ‘top pick’. Conclusion What did we learn about Fairfax? The stock price is unambiguously cheap in absolute terms and when compared to peers. The quality of the earnings are high and durable. The management team is best-in-class. Future prospects have never been better. Ratings agencies are drinking the Kool-Aid, with upgrades. Sell side analysts are drinking the Kool-Aid, with upgrades. The cheap stock price stands out like a sore thumb. How do we explain it? The answer is simple: Mr. Market is wrong. Now I know, according to EMT, this is not supposed to happen. What we have today is a real life example of where the efficient market hypothesis is bullshit. At least in the short run. We have situation where Mr. Market is grossly mis-pricing a stock. Now I do think the EMT is generally accurate over the medium to long term… the mis-pricing usually does not last for long. The disconnect with Mr. Market is fundamentals. The fundamentals have been improving at Fairfax for the past couple of years but are just now showing up in earnings. It’s like Mr. Market has been standing on the beach the last couple of years wondering why the water is running out to sea. The answer is we have a tsunami of earnings coming from Fairfax in the coming quarters and years. Mr. Market will figure it out. But in usual fashion, only when the wall of water comes crashing in (wiping out all the wrong-headed thinking on the company in the process). "What a shocker!" everyone will say. "Who could have known?" A similar thing happened to Fairfax in the 2006-2009 period. The coming spike in earnings is not a surprise to those who follow the company closely. So we are in this surreal environment where the future is kind of knowable (a spike in earnings leading to a spike in the share price). What to do? Trust the analysis (be right). Get the correct position size. Have patience (sit tight). ————— “And right here let me say one thing: after spending many years in Wall Street and after making and losing millions of dollars I want to tell you this: it never was my thinking that made the big money for me. It always was my sitting. Got that? My sitting tight! It is no trick at all to be right on the market. You always find lots of early bulls in bull markets and early bears in bear markets . I’ve known many men who were right at exactly the right time, and began buying and selling stocks when prices were at the very level which should show the greatest profit. And their experience invariably matched mine - that is, they made no real money out of it. Men who can both be right and sit tight are uncommon. I found it one of the hardest things to learn. But it is only after a stock operator has firmly grasped this that he can make big money. It is literally true that millions come easier to a trader after he knows how to trade than hundreds did in the days of his ignorance.” Reminiscences of a Stock Operator