Viking

-

Posts

4,702 -

Joined

-

Last visited

-

Days Won

35

Content Type

Profiles

Forums

Events

Posts posted by Viking

-

-

It will be interesting to see what Russia does on July 21. If they continue to ship gas they will allow Europe to better prepare for winter (build out storage). Russia may have maximum leverage now… cut off supplies today and Europe WILL be screwed when winter comes.

—————Exclusive-Russia's Gazprom declares force majeure on some gas supplies to Europe

- https://finance.yahoo.com/news/russias-gazprom-declares-force-majeure-121224916.html

LONDON (Reuters) -Russia's Gazprom has declared force majeure on gas supplies to Europe to at least one major customer, according to a letter from Gazprom that will add to European fears of fuel shortages.

Dated July 14 and seen by Reuters on Monday, the legal force of the letter is to shield Gazprom from compensation payments for disrupted supplies, but risks escalating tensions between Russia and the West over the invasion of Ukraine that Moscow calls a "special military operation".

The letter said Gazprom, which has a monopoly on Russian gas exports by pipeline, could not fulfil its supply obligations because of "extraordinary" circumstances…

The Nord Stream 1 pipeline is shut for annual maintenance, which is meant to be completed on July 21, but some of Gazprom's European customers are nervous supplies will not resume.

-

When valuing a company most investors focus on a company’s stock price. What has the trend been? What is expected in the future? EPS. PE. Market cap.

Most investors to not spend a lot of time looking at the debt side of things. Debt tends to be pretty stable for most companies… it's kind of just there. Now if a company is taking on a great deal of debt, yes, that can be a red flag. Because too much debt can get a company into trouble when the lean times arrive.

————-

Where am i going with this? What does any of this have to do with energy?

Energy companies (as a whole) are paying down their debt at what has to be an unprecedented pace for a sector in recent economic history. And its not like they were over leveraged when they started down this road about 6 quarters ago (some were; most were not). Lots of energy companies have plans to reduce total debt by as much as 60-70% - and most will have hit their targets by the end of 2022 or 1H 2023.

As a result, for lots of energy companies Enterprise Value is driving closer to Market Cap. Energy companies are making enormous amounts of money. It has been going to pay down which in turn has been actually driving down Enterprise Value (assuming constant Market Cap). Bizarre.

This is not a situation thar most investors are used to thinking about… i would appreciate hearing others thoughts on this topic.

—————Enterprise Value vs. Equity Value/Market Cap: What’s the Difference?

It's more than just the numbers. It's how they're used that counts.

- https://www.thebalance.com/enterprise-value-vs-equity-value-market-cap-5189488

The equity value, or market capitalization, of a company is one piece of the company’s enterprise value. Both measures are used to make investment decisions, but they provide different perspectives. Market cap estimates what a company’s outstanding common stock is worth. Enterprise value calculates all financial interests of the business, including those of debt holders and subsidiaries.

-

There was a lot of commentary in energy markets the last week or so that Biden’s trip to the Middle East would result in an increase in supply from Saudi Arabia. “Why else would he go if not to announce an increase in Middle East oil production?”

What did we actually learn? Oil supply from Saudi Arabia is indeed at/near capacity. Or Saudi Arabia is still pissed at Biden. Or some combination of the two. Pretty much nothing was said about oil during the trip (in public). Bottom line, no good news on the supply side of the equation for oil.

-

I think as winter approaches we are entering a phase of the Ukraine war i would describe as maximum uncertainty:

1.) how deep will the recession in Europe be if nat gas prices remain where they are today for the next 6-12 months? Can heavy industry in Europe survive? Can European governments afford the required energy bailouts, especially the southern countries?

2.) what will Europe do if Russia cuts back further on gas supplies (driving prices even higher)?

3.) the flip side of 2.) is can Russia even afford to cut off nat gas to Europe? Unlike oil, nat gas cannot be diverted to China and India (until new pipelines are built which will take years). Russia needs $ to keep its war machine going.

4.) where does Russia take the actual Ukraine war from here?

5.) does Western resolve hold? Do we reach a breaking point in the coming months in Europe where the economic pain starts to shift the political winds and support for the Ukraine war reverses?Currently my crystal ball is very, very murky. Normally, after analysis, i will develop a base case that i am fairly confident in. And then over time i try and figure out why i am wrong. Right now i really have no idea how the Ukraine war/ energy crisis in Europe is going to play out over the next 6-12 months. I see a lot of competing forces at work that are not sustainable (i think). The geopolitical risks are as unpredictable as i have seen them in a long time.

What is the investment angle?

1.) one obvious move is to carry a higher than normal cash balance. There is a very good chance that something breaks. Cash is king when that happens.

2.) oil: we are in the middle of an energy crisis that might be as bad as the 1970’s Arab oil embargo. So oil looks interesting should the war in Ukraine drag on or take a turn for the worse.

-

31 minutes ago, StevieV said:

WTI and the XOP ETF have correlated well over the last 1 and 2 year periods, but XOP has extremely underperformed the price of the commodity over the last 5. Over the last 5 years, WTI has advanced 109% versus a negative 9% for XOP. Can say a lot about that, but the briefest is - the E&Ps are being valued much less richly vis-a-vis oil prices than they used to be.

i think most analysts are saying where oil stocks are currently priced makes sense for oil priced at about $65-$70 or so. The fact oil is $98 is comical. This suggests to me there is NO DEMAND for oil shares currently. Big institutional investors (anyone who has to pay attention to ESG) cannot touch oil/energy stocks; they are probably still selling down positions.

So the price of oil stocks might not provide much information (on its own) to investors. The silver lining is oil companies are printing money. And most of them are buying back stock. Should share prices stay at these low levels AND oil prices stay north of $80 to $90, oil companies will be buying back a significant number of shares. Cheap share prices will just become another reason NOT TO GROW PRODUCTION (it will be more accretive to simply buy back shares on a risk adjusted basis). It will be super interesting to hear what management teams of oil companies have to say about capital allocation in the current environment when they report Q2 earnings in a couple of weeks. Specifically their low share price and stock buybacks.

-

Oil prices are back up to $98. Oil stocks have been crushed. Fears of recession appear to be trumping supply/demand fundamentals - for now.

It will be very interesting to see how Biden’s trip to the middle east goes this weekend. The following article sums up what a complete shit show the US relationship with Saudi Arabia has become. This just adds more complexity to the energy problems the world is facing.

—————Why Biden's Saudi trip has proved so thorny

- https://www.bbc.com/news/world-us-canada-62144217

Why is this so controversial?

America's decades-long dealings with Saudi Arabia have traditionally involved a trade-off between US values and strategic interests.

But President Biden explicitly emphasised human rights in the relationship, and now, as he bows to the political realities that shape it, he risks losing credibility on his values-driven approach to foreign policy.

The grisly murder of Khashoggi united both sides of Washington's partisan divide in fury. A journalist and prominent critic of the crown prince, Khashoggi was killed and dismembered in Saudi Arabia's Istanbul consulate.

As a presidential candidate, Mr Biden drew a categorical line in the sand, vowing to make the kingdom a "pariah" because of its grim human rights record. He used that sharp rhetoric to contrast himself with former President Donald Trump's unreserved embrace of Saudi Arabia. Mr Trump once boasted he had "saved [MBS'] ass" from the outcry over Khashoggi's death.

-

3 hours ago, lessthaniv said:

It's worthwhile to go back and re-read this thread from page 1 mining the content for investment lessons with the benefit of 10 years of hindsight.

Great comment. A few lessons for me:1.) the housing market cycle is nothing like the stock market cycle

2.) crazy low interest rates are rocket fuel to assets, especially highly leveraged assets like housing

3.) bubbles can blow for years and years (Canadian real estate and .com stocks being two good examples)

4.) information available to retail stock investors is much better than the information available to consumers on the housing market

One more lesson: all the money i have made on real estate the past 10 years is the result of dumb luck. Priceless

—————

I did sell my house in the spring of 2021 so i am once again a happy renter today.

-

Canadian oil juniors: MEG, WCP, ERF, TVE

Earlier today MEG was off 8%. Oil finished the day flat. Oil stocks are getting crushed and oil is… trading at $96. Oil companies are raking in the free cash flow. Moving forward more and more of the significant free cash flow will be going to share buybacks. And with the shares getting crushed that will be a very good use of cash. This is a very good set up for shareholders.

-

Well the Bank of Canada delivered a shocker today and raised their rate by 1% to 2.5%. The real estate market in Canada peaked in Feb/early March. Looks like a blow off top. Parts of the country that spiked the past 2 years (with 50% increases) are already seeing prices come down pretty hard from the highs (15% or so). Housing sales nationally have fallen off a cliff. What is interesting is inventory is building - but slowly. Canada is clearly in the early stages of a housing correction. And it will only get worse as long as the bank of Canada keeps increasing rates - which looks like the rest of this year at least. House prices are going lower. The only questions are how fast and how far they fall.

—————Lots of people are in shock right now. Most felt that with all the debt being carried by consumers in Canada there was no way the Bank of Canada would be able to increase interest rates like they have been doing. Next increase will be in Sept and it is expected right now to be another 50 basis points. More pain to come for Canadian housing.

—————

Canada Is 20% More Dependent On Housing Than The US In ‘06

Over the past year, GDP briefly began to outpace residential investment. It was a short-lived period, with the segment rising to 8.0% of GDP in Q1 2022. That’s a 0.3 point jump from the previous quarter and the highest share since Q2 2021. It’s down from the recent peak but way higher than pre-2020 — or any prior period that wasn’t a bubble, in hindsight.

-

If Kazakh production is cut off 1 million barrels per day will disappear from the market. Of course Mr. Market has fully priced this risk into an WTI oil price trading at $103. 12% of Chevron’s production would disappear. Exxon, Shell and Eni would also be significantly impacted.

Canadian oil producers are exceptionally well positioned these days.

—————

Analysis-Oil majors face output slump, deep losses if Russia stops Kazakh pipeline

https://finance.yahoo.com/news/analysis-oil-majors-face-output-133838289.html

LONDON (Reuters) - Western energy majors will cut output and lose billions of dollars if Russia, as is feared, suspends a pipeline that is almost the only export route for oil from land-locked Kazakhstan, company sources, traders and analysts say.

The closure of the CPC pipeline that carries oil from Kazakhstan to the Black Sea Russian export terminal in the port of Novorosiisk would shut in more than 1% of global oil supply, exacerbating what is already the most severe energy crunch since the Arab oil embargo in the 1970s.

The pipeline, which runs through Russian territory and is owned by a consortium of Western, Asian, Russian and Kazakh companies, has been in the spotlight since Russia on Feb. 24 invaded Ukraine in what Moscow calls a "special military operation".

Last Wednesday, a court in Novorossiisk ordered CPC to suspend operations for 30 days, citing concern about oil spill management.

A Russian court on Monday overturned the ruling against CPC and instead fined it 200,000 roubles ($3,300).

The sources, however, said they still thought major disruption likely. Pipeline co-owner Russia has said all stoppages are driven by technical issues.

-

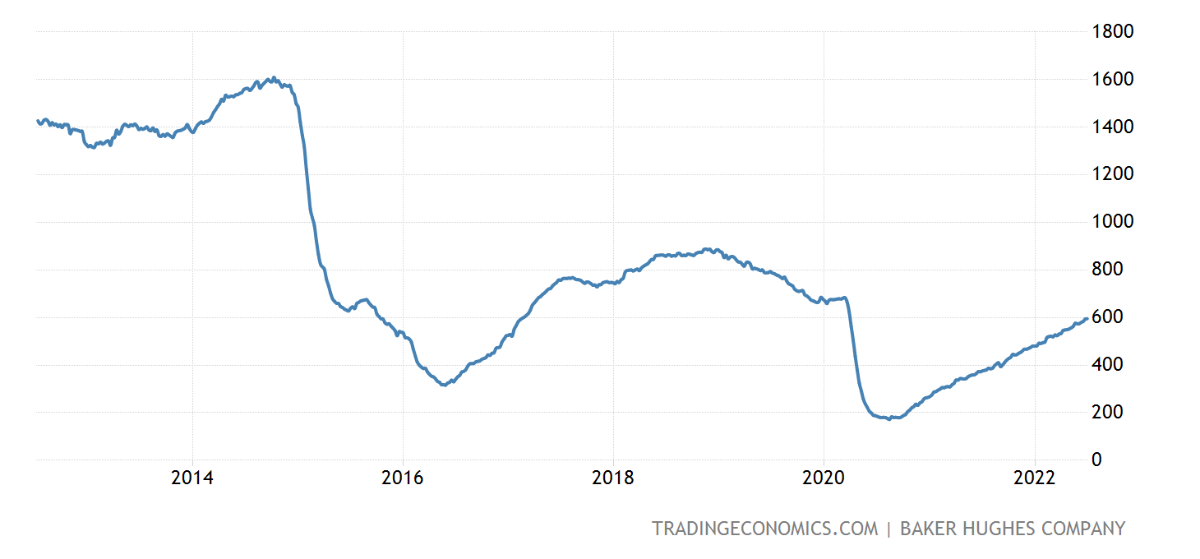

@Spekulatius If you remove the pandemic low, rig count today is near a HISTORIC low. And it is plagued by a severe labour shortage and extremely long wait times for equipment and steel. So yes, rig count will help grow NA production some; but likely not nearly enough to offset decline rates from existing wells and the demand growth we are seeing from the rest of the world.

-

1 hour ago, james22 said:

What can't go on forever (the Green delusion), wont.

ESG will matter less and less as it proves too costly.

@james22 i completely disagree. I think ESG is not only here to stay, but it is going to becomes even more important and bigger. ESG is now religion. It is STRONGLY believed by most of the population. And critically for investors, pretty much ALL governments, educators, institutional investors, pension funds, endowments, banks etc HAVE TO ACCEPT IT AND MINDLESSLY FOLLOW IT (and propagate it). To question ESG is heresy (you are labelled a climate denier). A strong belief in the strength and staying power of the ESG movement is one of the reasons why i am so bullish on oil stocks today.—————

Now to be clear… i do believe climate change is real. I also think we need to find a way to dramatically cut emissions. I also think the current set up is insanity:

1.) trying to throttle oil production for years in the West (which is what we have been doing… not approving new pipelines and demonizing oil producers and the entire industry are just two examples). And it has worked exceptionally well; supply growth WILL BE FAR LESS THAN IT NORMALLY WOULD HAVE BEEN (when compared to past cycles).

2.) oil demand growing like clock work by 1.5 million barrels a day for AT LEAST the next decade

3.) any meaningful transition to solar or wind is at least 5 or perhaps even 10 years away

4.) AND WE JUST DECIDED WE NEED TO KNEE CAP THE #3 OIL PRODUCER - RUSSIA

And this is all in an environment today where we already have a SHORTAGE of oil. That is why we are drawing down huge volumes from the SPR. Oh, and Buffett was buying more oil stocks today… (does anyone else hear that bell ringing?)

-

It is very interesting to watch the exit of global oil companies from the Canadian oil patch. Most global oil majors have stated they want to exit the country. And sooner rather than later. Forced sellers should result in reasonable prices for the acquirers.

Cenovus has already been able to purchase one joint venture oil sands asset from BP for $1.2 billion. At current oil prices it will be paid for in under 2 years (the clock started ticking May 1 so they are well on their way). After the asset is paid of it should be producing oil for another 3 decades or so… spitting out lots of cash flow. Buying out joint venture partners (especially when you are the partner operating the asset) is also ideal because it carries very little risk.

Canadian companies have been earning record free cash flow for the past 18 months:

- Stage 1 was focussed solely on paying down debt. Debt has been brought way down for most oil companies so this stage is done.

- Stage 2 is focussed on 50/50 split between paying down debt and shareholder returns (dividend/stock buybacks). This stage is ramping up is where most oil companies are today. Most oil companies will hit much lower net debt targets in 2H 2022 and this phase will come to an end.- Stage 3: as we enter 2023 most oil companies will shift to 25/75 split between paying down debt and shareholder returns. In 1H 2023 final debt targets will be achieved for most oil companies.

- Stage 4: as we enter 2023 we will start to get some Canadian oil companies shift to policies where 100% of free cash flow will be returned to shareholders (dividends and stock buybacks). As the year progresses more and more oil companies will get to this stage.

And we will enter a new age for Canadian oil companies: rock solid balance sheets (very little debt). And massive free cash flows. And what should be a golden age for investors.

————-—- stage 5: massive consolidation in the Canadian oil patch as global oil companies exit Canada. Canadian producers will likely be able to use part of their free cash flow to pick up assets from forced sellers at very reasonable prices. This stage will drive top line growth. And pristine balance sheets will help. And shareholder returns will take their next leap upward.

The key point here is free cash flow will not move into finding new production. Rather, free cash flow will be primarily used to take out other players.

-

22 minutes ago, StubbleJumper said:

Agreed. Q2 numbers will be superficially bad. The realised gains will not appear until Q3 or maybe even q4 for RFP. But, will Mr. Market understand this, or will the stock price slide when the Q2 EPS number is released in 4 weeks? I sniff the possibility of an opportunity...

SJ

We can only hope. There have been many times in the past where Fairfax has been sitting on big gains and Mr Market has been completely asleep at the wheel… for a quarter or two. And then the shares pop

-

22 minutes ago, gfp said:

Doesn't seem like any of the positives would be recognized in the 2nd quarter so there would surely be a loss reported for Q2 - right?

Regardless, Fairfax will include details (and expected increase in BV) from pet insurance and Resolute sales in the opening lines of their Q2 press release. So investors and analysts will be able to easily include them in their models. I think they also have some further gains on Digit (pending government approval). Bottom line, this reinforces the likelihood that Fairfax will be able to grow BV in 2022 (absent a brutal hurricane season or another 20% sell off in equity markets). -

Solid transaction. Sale price is very good given the environment we are in (going into potential recession and housing market slowing). We all have been asking what Fairfax will do with the commodity type equity holdings and we now have our answer on one - they will be opportunistic. It would be painful to hold all of the commodity equities through the cycle. Nice to see them sell one at peak pricing. And this begs the question if more deals are to come (Stelco and EXCO?).

Psychologically, it is also nice to get closure on what had been a pretty terrible investment for many years (up until the pivot to lumber a couple of years ago). And at a much higher price than anyone could have dreamed possible not that long ago. Remember, this stock was trading under $1.50 in 2020. What a ride! As others have noted, let’s hope Fairfax is able to exit its Blackberry position also at a good price at some point.

Fairfax has +$1 billion rolling in in Q3. What to do in a bear market? Taking out another 2 million Fairfax shares sure would be sweet!

@Xerxes no i sold all my lumber stocks long ago. I am still a lumber bull over the medium term (i think the US housing building boom is just getting started and will last for years). But i am not brave enough to hold lumber stock as we get closer to a potential recession. But they are back on my watch list (as is Stelco) as they have come down a fair bit.

-

@Spekulatius i appreciate the back and forth… great way to test drive ideas and get other perspectives.

What i am also learning with commodity plays is the importance of management… and what they do with the buckets of cash when times are good. Especially to hold through the cycle. CNQ has increased the dividend for 22 consecutive years (which had many years of terrible oil markets). Pretty solid track record (balancing growth, dividends, share buybacks, debt).

Stelco is back on my watch list. Shares are down to C$32. Market cap is $2.3 billion and my guess is they will have about $1.3 billion in cash after they report Q2 earnings (assuming the land sale has closed). So company has an enterprise value today of about $1 billion (forgetting about the pension liability) which is getting pretty attractive. Especially if steel prices stay well above historical averages (which i think they likely will). BUT it all depends on ones confidence level in Mr Kestenbaum and his capital allocation skills.

-

1 hour ago, Spekulatius said:

Elevator up and down Syndrom:

If oil prices go from $60/brl to $100 brl, underlying oil stock trades at price A

Then oil goes to $120, and after that oil goes back to $100 and underlying oil stock trades at B

I can almost guarantee you that B < A, most likely significantly so.

The reason is simple - probably half the people who owns this don’t have a clue and just play the momentum or the story. They would actually pay more for a oil stock with crude at $80 on an uptrend than the same oil stock with crude $100 and trending down.

@Spekulatius so let’s test your theory with reality. Let’s look at CNQ the largest Canadian oil company (i focus on the Canadian producers). Looks like you are right! Investors ARE able to buy CNQ today at a much lower price (company also has much less total debt) than the last time oil crossed $100 (Feb 28).

1.) when did oil hit $60? Feb 20, 2021. CNQ share price was US$27.292.) when did oil hit $100? Feb 28, 2022. CNQ share price was US$$55.83

3.) when did oil fall back to $100? July 5, 2022. CNQ share price was US$51.33

And over the past 4 months CNQ has earned about US$3.50/share in free cash flow that was used to pay down debt, buy back stock, pay dividend and grow future production (management has been exceptionally rational and shareholder friendly).

—————

As an investor what i care about is earnings. CNQ is projected to earn about US$10/share in free cash flow in 2022. 1/2 of the year is in the bag. Do i think they will hit the annual number? Yes. Forecasts for 2023 are for slightly higher free cash flow. This is based on oil of $96/share (i use RBC). My guess is there is at least an equal chance oil trades over $96 the next 18 months as below it. So buying CNQ today at $50 (which is what i did) there is a reasonable chance i will see $15 in free cash flow over the next 18 months. To me that looks like a reasonable risk/return (on an extremely simple back of the napkin analysis).

And i am learning to love the volatility. I think of Graham’s Mr Market coming to my door each day with a price… sometimes wicked high and other times wicked low…

-

12 minutes ago, Spekulatius said:

You can buy similar FCF yields with companies that have very little commodity risk, Examples : GEF-B, WRK and to a lesser extend CE.

In my opinion, these may turn out to be better investments in the long run. They have much less ESG headwinds and I would argue secular tailwinds from industry consolidation and substitution (WRK) and electrification (in the case of CE)

Or if you like real cash returns ( not promises of cash returns ) look at the miners BHP or RIO. They are currently distributing double digit dividend yields. Those dividends are variable , but they own world class resources (iron ore for BHP etc) that place them as the best quality and lowest cost on global scale. BHP builds a potash mine that is going to be a 100 year life - think about an inflation protected asset here (it will require continued reinvestment but the initial outlay is one time >$7B). It could become a tremendous asset if it operates well (which is TBD).

All the above are a much less crowded trade than energy and they have come down a lot from the peak, as have some commodity prices. However I can see that one can get high single digit returns from cash distributions alone without any multiple expansion or price change with inflation at all.

Even with modest increases in equity value the returns through the cycle should be double digits.

People go gung ho on energy because makes a lot of headlines sind performed well, but there is a lot of stuff out there that seems to scream value and nobody seems to care much.

( I own GEFB right now, but looking at WRK and CE as well). The miners are for later…

Yes, there are lots of opportunities out there for investors. The narrative for oil has shifted… the new narrative is oil is going to $60. Even though it is $100.

I think it is pretty clear demand for oil will grow minimum about 5 million barrels over the next 5 years. Where will that incremental supply come from? What countries? In a world that has been under investing for 8 years. I cannot find any plausible answer to this question. If anyone has read anything that lays out where all this oil is going to come from please share it. (And ‘the cure for high oil prices is high oil prices’ is not a very sophisticated answer). -

1 hour ago, Spekulatius said:

I mentioned this before, I think crude goes back to $80-90/ brl which is where it was before the Ukraine invasion. Russian oil has not disappeared from the oil market, they export about the same quantities than before, just to different destinations A lot bulls are getting high on their own supply here.

The money here is likely made on the short term we see the same nonsense playing out again and again (looks at semis ) and it’s not better than betting on COVID-19 winners.

That said, I do think energy prices will end up higher than before the epidemic , but not as much than bulls think.

@Spekulatius my read is today we have a demand / supply imbalance (requiring US to draw down SPR). Demand continues to increase, driven by India, China, indonesia etc. I see little new supply coming on line (unlike the past). I think people underestimate how broken the supply side of oil is today.

Oil trading at $90-$100 is the best outcome for oil companies over the medium term. At that price demand will continue to grow. And little new supply will be coming on stream. And oil companies will continue to print money. Low debt targets will be hit in next 6 months. What to do with all that cash? When stock price is low? Not rocket science… share count will be the next big use of free cash flow.

The more the politicians demonize the industry and enact stupid short term policy they will simply ensure the supply response is less than it otherwise would be.

And oil equities will be SUPER VOLATILE. investors have to be able to handle this.

-

"Greedy bastard day"... (Russell Crowe quote from A Good Year). Backed up the truck on CNQ. Stock is down almost 9% today ($CAN) and trading back where it was trading in mid January. Before $100 oil. And before Russian invasion was on anyones radar. Best managed/performing large cap oil stock in Canada the past 5 years. Always wanted to own... never traded a a price i was comfortable with (trades at a large premium to peers). Except today it is trading like a junior. Dividend yield is 4.6% and it paid its dividend throughout the covid lock down (rock solid).

-

Yes, happy belated birthday to Canadian and American board members… not many other places in the world i would rather live and raise a family. Yes, not perfect. But much to be thankful for.

-

2 hours ago, glider3834 said:

viking I think they will separate out the pet insurance business as asset held for sale at its carrying amount in Q2 results. And the gain on sale would be reported when transaction is closed.

Once we have the carrying amount, we can work out what the gain should look like.

Cheers

@glider3834 thanks for the clarity. Pretty crazy how much they are earning on the pet insurance transaction. An under-appreciated part of Fairfax are these very large one time gains they are able to surface… -

1 hour ago, StubbleJumper said:

Thanks, Viking.

This could very well become a table-pounding opportunity as we enter the most intense portion of the annual hurricane season! In early August, Mr. Market probably will not like the headline EPS number resulting from those M2M losses, and Mr. Market never seems to like the uncertainty during hurricane season which really gets into full swing in mid-August. If you've still got dry powder, you might get a good opportunity...and if you don't have dry powder, it might be worthwhile reflecting on what you might choose to sell if FFH shares take a serious dive.

SJ

@StubbleJumper I have been thinking about the same things you discuss above. The challenge (to Fairfax shares selling off) is Fairfax shares have been trading pretty well all year (compared to the overall market). So it looks to me like someone is buying and I wonder if it is not Fairfax. So the stock could hold up better than expected even after earnings. And once the pet insurance deal closes Fairfax will have significant cash to buy back stock. But if we get a bad hurricane season, yes, Fairfax could get hit. And if we see top line slow (signs the hard market is ending) we could see all insurance stocks sell off. Having said all that I have been reducing my position (taking advantage of the recent run up) and shifting most of the proceeds into a basket of oil stocks - people are probably getting sick of all my oil posts in recent days. My cash balance is back up to 60% (I want to keep a high cash balance until i we are closer to a Fed pivot). Fairfax continues to be my third largest holding (after oil and BAC). I would likely be a buyer of Fairfax below US$500 and would likely get aggressive if it hit US$450.

Energy Sector

in General Discussion

Posted

We KNOW world oil demand is going to grow by 1 to 1.5 million barrels per day over the next 5 years (probably 10). Where is the increase in supply going to come from. Only a MODEST amount will come from Saudi Arabia…

—————

Saudi Arabia Reveals Oil Production Capacity Limits

- https://oilprice.com/Energy/Crude-Oil/Saudi-Arabia-Reveals-Oil-Production-Capacity-Limits.html

Saudi Arabia, the world’s top crude oil exporter, will not have additional capacity to increase production above the 13 million barrels per day (bpd) it has pledged to have by 2027, Saudi Crown Prince Mohammed bin Salman told the leaders of the United States, the Gulf Cooperation Council (GCC) states, Jordan, Egypt, and Iraq at a summit this weekend.

“We also stress the importance of continuing to inject and encourage investments in fossil energy and its clean technologies over the next two decades to meet the growing global demand, with the importance of assuring investors that the policies adopted do not pose a threat to their investments to avoid their reluctance to invest and to ensure that no shortage of energy supply would affect the international economy,” Crown Prince Mohammed bin Salman said in his address.

“The Kingdom will do its part in this regard, as it announced an increase in its production capacity to 13 million barrels per day, after which the Kingdom will not have any additional capacity to increase production,” he added, as carried by the Saudi Press Agency.

Last year, Saudi Arabia said it expects to have boosted its oil production capacity to 13 million bpd by 2027 from 12 million bpd now…

At the Jeddah summit, the Saudi crown prince also criticized the growing backlash against fossil fuels, saying that “The adoption of unrealistic policies to reduce emissions by excluding major sources of energy without taking into account the resulting impact of these policies on the social and economic pillars of sustainable development and global supply chains will lead in the coming years to unprecedented inflation, rise in energy prices, increase unemployment and exacerbate serious social and security problems, including an increase in poverty and famine and crime rates, extremism and terrorism.”