Viking

-

Posts

4,702 -

Joined

-

Last visited

-

Days Won

35

Content Type

Profiles

Forums

Events

Posts posted by Viking

-

-

1 hour ago, Dinar said:

There is a real cost to immigration that nobody talks about. Lower wages, higher traffic, higher stress on environment, higher rent and housing prices, higher economic inequality which leads to all sorts of social problems. Lower wages in our welfare state encourage people to stay on the dole with very negative consequence for the society as a whole. I am all for welcoming Einsteins/Fermi/, but not millions of unskilled people with two grades of education who will have ten children that taxpayers will have to educate. You want labor force growth? Reduce welfare benefits (welfare, food stamps, section 8, medicaid, free phones & internet and the list goes on). Fix public schools so that kids can get a good education rather than propaganda, so that middle class is comfortable having 2-3 kids rather than have one because they need to send him to public school.

It looks to me like both the US and Canada have built 2 very successful countries over the last +200 years. What was the secret sauce? A key ingredient was immigration. Immigration certainly was not a ‘cost’. Moving forward i can’t really talk to what is best for the US. For Canada i am all for immigration - too many positives to list. -

With the release of Q2 results we got additional information on the pet insurance sale to JAB. This has to be one of the best investments Fairfax has ever made. The after tax gain is $975 million ($41/share) and will be booked when the sales closes later this year. For a business with $350 million of revenue (if i understood the Q2 conference call correctly).

Fairfax made two purchases in 2013 and 2014. The pet insurance business was cultivated within Fairfax for 10 years. The pandemic likely accelerated the growth of the business. And now Fairfax is opportunistically exiting/selling at what looks to be a very good price. And selling this business looks like it will have little impact on Fairfax’s future insurance business (top or bottom line).

We like to obsess over Fairfax’s many investment failures over the years. Farmers Edge being the most recent example. The flip side of the coin is Fairfax has many examples of where they have hit the ball out of the park.

Most importantly, the gain from the sale of the pet insurance business will not be used to cover significant realized losses in the investment portfolio (like the recent $4.5 billion in losses from the disastrous shorting campaign that stretched over 7 years). Instead, the significant gains will be used to build future shareholder value. This is a significant NEW development for Fairfax. And that prospect should get all Fairfax shareholders very excited.

Fairfax is now, after 7 lean years, finally playing offence again. Strong underwriting + solid investment gains are now driving significant growth in BV per share. 2021 was the start. Much more is coming. Eventually investors will figure it out.

The trifecta is happening with Fairfax:

1.) growing earnings

2.) higher multiple

3.) lower share count

—————

Fairfax will receive approximately $1.4 billion in the form of approximately $1.15 billion in cash and $250 million in seller promissory notes, and the company will also invest $200 million in JCP V, a JAB consumer fund.

The transaction is expected to close in the second half of 2022. On closing of the transaction the company expects to record an after-tax gain of approximately $975, and deconsolidate assets and liabilities with carrying values at June 30, 2022 of approximately $150 and $32.

—————

Mark Dwelle RBC - Another quick numbers question. If I may, on the sale of the Pet Insurance business. Can you give us a sense of kind of a range of about how much revenue you'll be, I guess, selling when that happens? And again, it's just I'm trying to understand as we get into next year, that's revenue that will go away from Crum and to be able to keep track of the run rate there.

Prem Watsa: Sure, Tom. But forex must be $350 million, and it's a Pet Insurance and it's in the United States, mainly, but Canada and then the UK, some, and obviously, we like the price. But JAB is they get a lot of good things from Crum, including data on 30 million pets, and ASPCA support for 16 years. And so we think it's a win-win.

—————

TORONTO, ONTARIO--(Marketwired - May 15, 2013) - Fairfax Financial Holdings Limited (TSX:FFH)(TSX:FFH.U) announces the signing of a merger agreement with Hartville Group, Inc., of Canton, Ohio, pursuant to which Hartville will become wholly-owned by Crum & Forster's United States Fire Insurance Company. The transaction, which is subject to customary conditions including regulatory approval, is expected to close early in the third quarter of 2013.

Hartville, one of the oldest and largest pet insurance providers in the U.S., provides pet insurance plans under several brand names, including Hartville Pet Insurance and the Petshealth Care Plan. Hartville also is the exclusive strategic partner for pet insurance with The American Society for the Prevention of Cruelty to Animals®.

"We are very excited to have Hartville join the Fairfax group," said Prem Watsa, Chairman and CEO of Fairfax. "This acquisition represents a new phase in our existing relationship with Hartville through Fairmont Specialty. As a result of the vertical integration created by this merger, Hartville's pet insurance programs will be uniquely positioned in the industry to generate sustainable growth."

—————

TORONTO and OAKVILLE, ONTARIO, August 29, 2014 – Fairfax Financial Holdings Limited (TSX: FFH)(TSX: FFH.U) (“Fairfax”) and Pethealth Inc. (TSX: PTZ) (“Pethealth”) announced today that they have entered into an arrangement agreement (the “Arrangement Agreement”) under which Fairfax will acquire all of the outstanding common shares of Pethealth for $2.79 per share in cash. In addition, under the terms of the transaction, Fairfax will acquire all of the outstanding preferred shares of Pethealth for a purchase price of $2.79 per share in cash, plus any dividends accrued but unpaid up to, but excluding, the day of closing.

The purchase price represents a premium of approximately 26% to the closing price of Pethealth’s common shares on the TSX on August 29, 2014 and a premium of approximately 69% to the closing price of Pethealth’s common shares on the TSX on August 15, 2014 (Pethealth announced on August 19, 2014 that it was reviewing strategic alternatives). The purchase price also represents a premium of approximately 69% to Pethealth’s volume weighted average share price for the twenty trading days ending on August 15, 2014 and a premium of 36% to the all-time high price of Pethealth’s common shares prior to such date.

Total cash consideration of approximately $100 million will be paid for Pethealth’s common and preferred shares and options. The transaction, which will be completed by way of a plan of arrangement (the “Arrangement”), is subject to certain customary closing conditions, and is expected to close in the fourth quarter of 2014.

-

32 minutes ago, Thrifty3000 said:

@Viking as always, THANKS for the fantastic analysis. One thing you may want to add into the spreadsheet is an assumption that the diluted share count will continue increasing by 200,000 to 250,000 shares annually (until prevailing trends change). 15%+ yoy growth of diluted share count is a bit disappointing, and certainly offsets a sizable portion of the benefits of the buybacks.

Diluted shares:

2016: 0

2017: 689,571 +689,571

2018: 890,985 +201,414

2019: 1,159,352 +268,367

2020: 1,273,250 +113,898

2021: 1,503,931 +230,681

@Thrifty3000 thanks for providing details on diluted shares. I do need to better understand this bucket. My assumption is these shares are part of employee compensation program. Do you know the details? Are they earned over many years? Are they performance based at all? -

How are Fairfax's various equity investments doing 1/3 of the way through Q3? My math says they are up about US$620 million = $26/share pre tax. Of the total about $170 million = $7/share is mark to market. Biggest movers:

1.) Resolute = +$230 million. This sale will close in 1H 2023.

2.) Atlas = +$127

3.) Blackberry = + $76

4.) Eurobank = + $48

4.) Stelco = + $35

-

2 hours ago, Viking said:

Fairfax Financial is an insurance company. However, the volatility of investment results usually overshadow the results of its insurance operations. The size of Fairfax's insurance businesses have increased dramatically. Over the past 8 years net written premiums have increased 228% from $5.98 billion in 2014 to $19.4 billion in 2022 (my estimate) for a compounded growth rate of 16% per year. On a per share basis Fairfax has compounded net premiums written by a little more than 14% per year over the past 8 years (the share count is up about 10%).

What has driven this significant growth? For the first 3 years acquisitions drove the growth: Brit (2015), International (2016) and Allied World (2017). For the past 5 years (2018-2022) the growth has been organic driven by the hard market of the past 3 years. Looking back, Fairfax timed their large insurance acquisitions perfectly.

2023 could see net premiums written grow another $3 billion. This would represent 50% growth over what was written in 2014. That is a big deal and possible a game changer for investors.

Why do we care what net written premiums are? Because this is a key input in determining underwriting profit. And underwriting profit is one of the critical inputs in determining what an insurance company is worth. Fairfax is on pace to earn an underwriting profit of $1.16 billion in 2022 ($50/share). A new record. My estimate is Fairfax could earn $1.3 billion in 2023 ($58/share). Another record. The previous record was $801 million in 2021 ($31/share). Bottom line, the significant growth in net written premiums the past 8 years is now resulting in Fairfax earning record underwriting profit. And the record underwriting profit party is just getting started.

Now we all know financial markets are extremely efficient when pricing equities. Everything that is know about a company is already priced into its equity price. So where was Fairfax stock trading at Dec 31 2014? About US$510. Where is Fairfax stock trading today? US$538. Wow! Really? So was Fairfax way overvalued in 2014? Or is Fairfax way undervalued July 28, 2022? Or is it some combination of the two?

Before we reach any final conclusion we need to look at the other engines that power earnings: interest and dividend income and the investment portfolio. We will do this in a future post

----------

Net Prem Earned CR Underwriting Profit

2023 Est $21.7 billion 94 $1.3 billion $58/share

2022 Est $19.4 billion 94 $1.16 billion $50

2021 $15.5 95 $801 million $31

2020 $13.86 97.8 $308 $12

2019 $12.54 96.9 $389 $15

2018 $11.91 97.3 $322 $12

2017 $9.71 106.6 -$642 -$25

2016 $7.86 92.5 $576 $22

2015 $7.37 89.9 $705 $27

2014 $5.98 90.8 $552 $21

----------

My numbers above do NOT include runoff. My guess is the cost of runoff will come in at about $150 to $200 million per year (about the average from the past couple of years).

With spiking bond yields in 2022, interest and dividend income at Fairfax has been increasing rapidly. With Q2 results Fairfax provided a forecast for interest and dividend income of about $950 million annually (current normalized run rate). This compares to a run rate of $530 million annually at the end of 2021. This is about an 80% increase in 7 short months.

By combining my last 2 posts we can now estimate Fairfax’s operating income = underwriting income + interest and dividend income.UI. I&DI

2022 est. $1.16 + $0.84 = $2 billion / 23.7 mill shares = $84/share2023 est. $1.3. + $1.0 = $2.3 billion / 22.7 mill shares = $101/share

Operating income is now large enough at Fairfax that it will serve as an important offset to the volatility of the company's deep value equity holdings - which can be very volatile from year to year (as we have just seen with results reported in Q2). Significant operating income will provide an important 'shock absorber' to reported Fairfax results and book value moving forward.

————-

The above does not include underwriting losses from runoff. It also does not include share of profit of associates (Eurobank, Altas and Resolute) which was $188 million in Q2 and $316 million in 1H.

—————Fairfax’s bond portfolio had an average duration of 1.2 years at June 30, 2022. Fairfax has been a significant beneficiary of rising interest rates. Given the comments from Prem on the Q2 call, Fairfax continues to believe interest rates are likely to increase over the next year. The average duration of Fairfax’s bond portfolio will be something to monitor in the coming quarters.

—————In my estimates for 2023 i think Fairfax’s share count will be at least 1 million lower (falling from 23.7 to 22.7). And i think there is a good chance the share count falls 2 million in 2023 to 21.7 million. How? After the pet insurance sale closes, and if we see a normal Q3 hurricane season, i think Fairfax will do another $1 to $1.2 billion buyback in Q4 perhaps with a price to US$600.

-

6 minutes ago, glider3834 said:

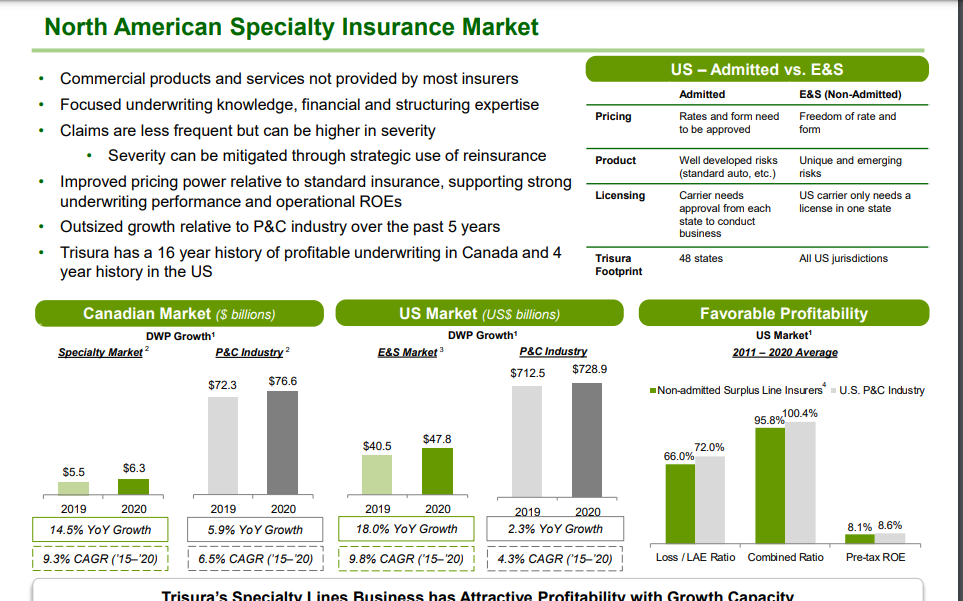

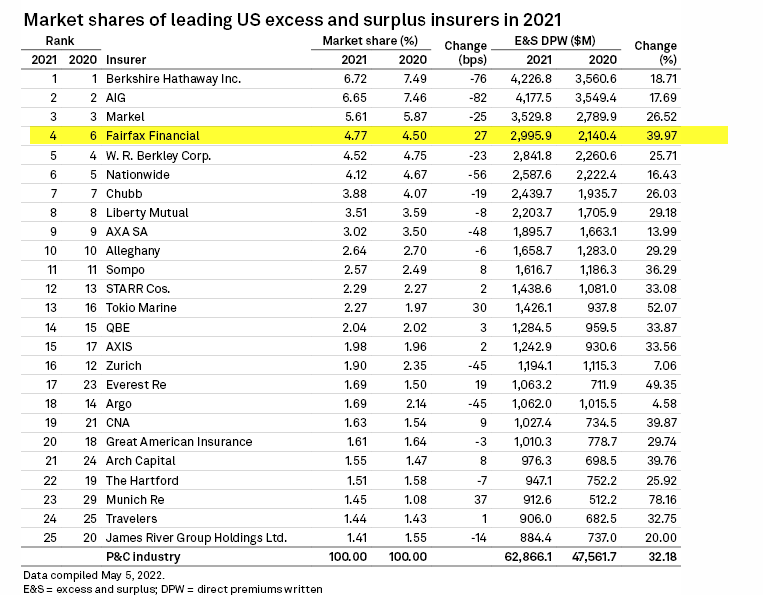

thanks viking - great summary - I also like how they are growing - one key area is specialty/E&S.

why? Its harder to do so more specialised, less competitive & more profitable (lower CR) than standard lines.

Trisura actually put up a nice summary comparing E&S(specialty market) to standard marketplace & why they are attracted to this space

Fairfax has grown to be the #4 E&S (Specialty marketplace) writer in US

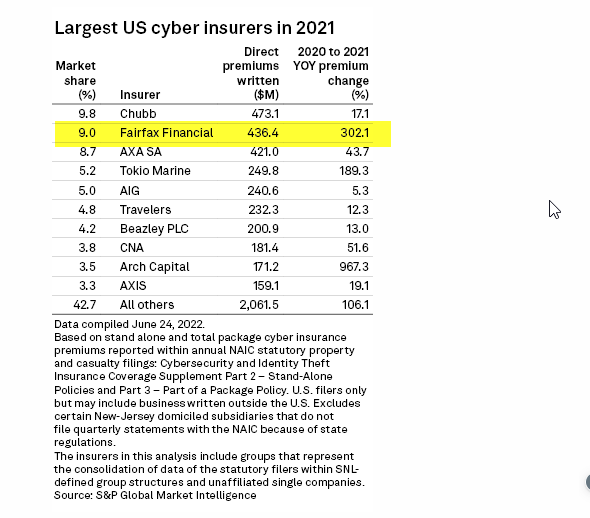

One of the fastest sub-sector areas in insurance is cyber insurance & with rates hardening here a lot in high double digits, Fairfax has been putting emphasis on growth here - #2 US writer

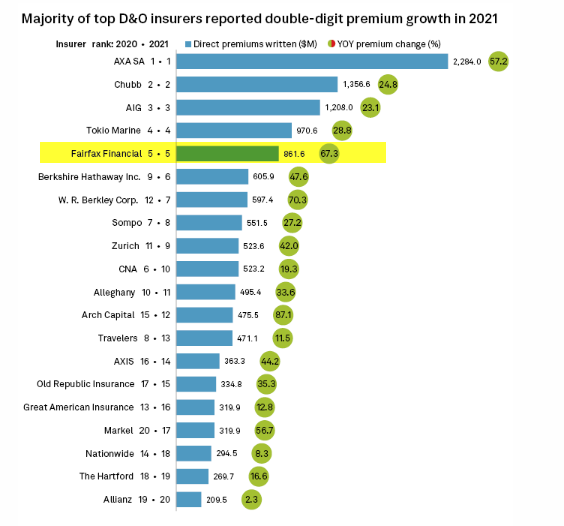

#5 US writer in Directors & Officers Liability - again this market was supported by significant rate growth https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/d-o-premiums-grow-38-5-in-2021-loss-ratio-falls-to-multiyear-low-70106981

Glider, thanks for the insight. Lots to like about what Fairfax is building… -

Fairfax Financial is an insurance company. However, the volatility of investment results usually overshadow the results of its insurance operations. The size of Fairfax's insurance businesses have increased dramatically. Over the past 8 years net written premiums have increased 228% from $5.98 billion in 2014 to $19.4 billion in 2022 (my estimate) for a compounded growth rate of 16% per year. On a per share basis Fairfax has compounded net premiums written by a little more than 14% per year over the past 8 years (the share count is up about 10%).

What has driven this significant growth? For the first 3 years acquisitions drove the growth: Brit (2015), International (2016) and Allied World (2017). For the past 5 years (2018-2022) the growth has been organic driven by the hard market of the past 3 years. Looking back, Fairfax timed their large insurance acquisitions perfectly.

2023 could see net premiums written grow another $3 billion. This would represent 50% growth over what was written in 2014. That is a big deal and possible a game changer for investors.

Why do we care what net written premiums are? Because this is a key input in determining underwriting profit. And underwriting profit is one of the critical inputs in determining what an insurance company is worth. Fairfax is on pace to earn an underwriting profit of $1.16 billion in 2022 ($50/share). A new record. My estimate is Fairfax could earn $1.3 billion in 2023 ($58/share). Another record. The previous record was $801 million in 2021 ($31/share). Bottom line, the significant growth in net written premiums the past 8 years is now resulting in Fairfax earning record underwriting profit. And the record underwriting profit party is just getting started.

Now we all know financial markets are extremely efficient when pricing equities. Everything that is know about a company is already priced into its equity price. So where was Fairfax stock trading at Dec 31 2014? About US$510. Where is Fairfax stock trading today? US$538. Wow! Really? So was Fairfax way overvalued in 2014? Or is Fairfax way undervalued July 28, 2022? Or is it some combination of the two?

Before we reach any final conclusion we need to look at the other engines that power earnings: interest and dividend income and the investment portfolio. We will do this in a future post

----------

Net Prem Earned CR Underwriting Profit

2023 Est $21.7 billion 94 $1.3 billion $58/share

2022 Est $19.4 billion 94 $1.16 billion $50

2021 $15.5 95 $801 million $31

2020 $13.86 97.8 $308 $12

2019 $12.54 96.9 $389 $15

2018 $11.91 97.3 $322 $12

2017 $9.71 106.6 -$642 -$25

2016 $7.86 92.5 $576 $22

2015 $7.37 89.9 $705 $27

2014 $5.98 90.8 $552 $21

----------

My numbers above do NOT include runoff. My guess is the cost of runoff will come in at about $150 to $200 million per year (about the average from the past couple of years).

-

My key takeaway after listening to the Q2 conference call:

Question: What are plans for proceeds from pet insurance sale?

Prem’s answer: buying back stock #1 priority—————

Music to my ears.

-

I like listening to different conference calls for oil and gas companies to broaden out my perspective. Just listened to the Shell Q2 Q&A. What really jumps out in the call is Europe is screwed. And the situation is likely to get much worse. 80% of the questions on the call were from media/newspapers. Record profit levels for companies. And historic pain for consumers. ‘War profiteering’ is the new description and this is not a good development for European energy producers.

The Shell CEO had an interesting come back: Europe wants to consume oil and gas… but it doesn’t want to produce it. You can’t cut off supply and use that as the lever to curtail demand. The result of this policy is the current catastrophe (oil and gas prices for consumers at record levels).

The more i learn the more i come to understand how absolutely messed the government energy policy is in the West. A building block of this mess is a public that has completely unrealistic expectations of the energy transition. So we are living a fantasy.

The problem has been percolating for years. And there is no easy short term fix. Much higher prices (oil +$150) leading to demand destruction is the only short term solution i can see.

-

Surprisingly in-line quarter. Crazy volatility with investments (expected given we are in the middle of a bear market). Tailwinds just keep getting better…

Insurance:

1.) does top line growth remain close to 20%? Yes +24.9% (net premiums written)

2.) is CR below 95? Below 94? Solid 94.1%

3.) is hard market still alive and kicking? Outlook for remainder of 2022? TBD

Bond portfolio4.) what kind of increase do we see in interest income? Solid increase in Q2 from $161 to $$203 million

5.) what changes do we see in bond portfolio? Bought a little more 1-2 yr bonds

6.) what is average duration? (1.4 years at March 31) At 1.2 years7.) what is amount of mark to market loss? US$400-500 million? $413 million

Equity Portfolio

8.) what is amount of mark to market loss? (My estimate is around $1 billion) Equity/Other = $1.135 billion

Other

9.) share of profits of associates? $200 million? $257 million

10.) Book value? (Was US$626/share March 31) $588

11.) share buybacks during quarter? (At March 31, 2022 there were 23,810,965 common shares effectively outstanding.) June 30 there were 23,654,827 shares outstanding. Suggests 156 million shares were repurchased during the quarter = 0.66%

12.) capital allocation priority moving forward? TBD

- level of debt is ok

- continue to fund growth at subs in hard market?

- buy back stock?

- buy out minority shareholders in Allied World?

Updates/Commentary:

13.) pet insurance sale: on track? To close when? Proceeds to be used for?

- expected to close in 2H. On closing after tax gain = $975 million.

14.) Resolute Forest Products sale: to close when?

- expected to close 1H 2023. Est pre-tax gain = $180 million + value of CVR (max $180 million)

15.) Stelco dutch auction: will Fairfax be tendering shares? TBD16.) was regulatory approval received to take control of Digit? Not yet.

—————

Looking ahead, is Fairfax on glide path to earn $2 billion from underwriting income + interest and dividend income in 2023? Yes. $2 billion might be low—————

Other notes from Q2 release:

- Farmers Edge impairment charge = $109 million

- Grivalia Hospitality stake increased from 33.5% to 78.4% for $195 million

-

With the Fairfax Q2 report set to be released after markets close on Thursday here are a few of the things i will be watching. What am i missing that others are looking out for?

Insurance:

1.) does top line growth remain close to 20%?

2.) is CR below 95? Below 94?

3.) is hard market still alive and kicking? Outlook for remainder of 2022?

Bond portfolio4.) what kind of increase do we see in interest income?

5.) what changes do we see in bond portfolio?

6.) what is average duration? (1.4 years at March 31)7.) what is amount of mark to market loss? US$400-500 million?

Equity Portfolio

8.) what is amount of mark to market loss? (My estimate is around $1 billion)

Other

9.) share of profits of associates? $200 million?

10.) Book value? Was US$626/share March 31

11.) share buybacks during quarter? (At March 31, 2022 there were 23,810,965 common shares effectively outstanding.)

12.) capital allocation priority moving forward?

- level of debt is ok

- continue to fund growth at subs in hard market?

- buy back stock?

- buy out minority shareholders in Allied World?

Updates/Commentary:

13.) pet insurance sale: on track? To close when? Proceeds to be used for?

14.) Resolute Forest Products sale: to close when? (I think i read Q1 2023 due to needed regulatory approvals)

15.) Stelco dutch auction: will Fairfax be tendering shares?16.) was regulatory approval received to take control of Digit?

—————

Looking ahead, is Fairfax on glide path to earn $2 billion from underwriting income + interest and dividend income in 2023? -

I think we just got another Powell pivot. The hawk has been put back in the cage. The beginning of the next pop in stocks?

-

2 hours ago, StubbleJumper said:

If FFH tenders the whole thing at $35/sh, we might do well to ask Prem what he was doing last summer when the prevailing market price was dependably higher. FFH could have trickled out their shares over 8 or 9 months and done better than $35.

SJ

The world was very different 8 or 9 months ago. Looking though the rear view mirror Fairfax should have sold pretty much every equity holding 8 or 9 months ago. They would be in a much better position financially today. Of course that is not realistic.Rather, you make decisions based on the facts as they exist today. Fairfax has an opportunity to get taken out of its Stelco stake at $35/share. Simple, clean and timely. If Fairfax tenders shares i think it will be to re-deploy the proceeds into something else that is a much opportunity.

It would also be very rational for Fairfax to sit tight. If 30 million shares get tendered (doubtful if Fairfax does not tender theirs) then total share count would fall to 42 million. Fairfax owns 13 million = 31% ownership. In a few short years Fairfax would have doubled its ownership of a business with a very bright future. Steel is trading at US$850 which is still a very high price historically. So maybe with the tender Kestenbaum is trying to bottom fish Fairfax’s shares… and perhaps Fairfax does not bite. I will not be disappointed in Fairfax does not tender all (or a portion) of their shares.

-

Stelco has just announced a massive SIB (see below). What Fairfax does will be super interesting. My guess is they tender. The reason? The 30 million share number from Stelco (+40% of shares outstanding) is too convenient: it allows Stelco to take out both large shareholders. At a low price. But we are in a bear market… Fairfax likely has lots of other great opportunities they can flip the proceeds into.

My guess is Fairfax will be happy to take a low price for Stelco because they can flip the proceeds into another investment they have more control over, better understand, that carries less risk and that is much cheaper than Stelco at C$35.- buy another $1 billion Fairfax stock back at wicked low valuation

- buy out minority partners in Allied World

- buy outstanding stake of Fairfax India back at wicked low price

IF Fairfax tenders they could have +$2 billion in proceeds coming in from recent sales: pet insurance, Resolute Forest Products and Stelco.

EXCO is another resource position to watch. Is Fairfax unloading most of its resource holdings?

—————As a reminder, Fairfax is the largest holder of Stelco with 13 million shares = 17% of shares outstanding. Proceeds would be C$455 million.

—————HAMILTON, Ontario--(BUSINESS WIRE)-- Stelco Holdings Inc. (TSX: STLC) (“Stelco” or the “Company”) announced today its intention to commence a substantial issuer bid (the “Offer”) pursuant to which the Company will offer to purchase up to30,000,000 of its outstanding common shares (the “Shares”) from holders of Shares (the “Shareholders”) for cash at a price of $35.00 per Share (the “Purchase Price”) for an aggregate maximum purchase amount of $1,050,000,000.

—————

TORONTO, Nov. 19, 2018 (GLOBE NEWSWIRE) -- Fairfax Financial Holdings Limited (“Fairfax”) (TSX: FFH and FFH.U) announces that it has acquired, through its subsidiaries and by way of a private share purchase agreement, a total of 12,200,000 common shares (“Common Shares”) of Stelco Holdings Inc. (“Stelco”), representing approximately 13.7% of the issued and outstanding Common Shares, at a price of C$20.50 per Common Share. The acquisition represents Fairfax’s entire interest in Stelco. (Total cost was C$250 million.)

-

Good summary of current state of oil market. Bottom line, expectation prices will remain in $95-$105 range into 2023. Oil companies will print money.

————-Morgan Stanley oil analyst Martijn Rats has cut his oil price forecasts

-

“Over the last year we have argued that oil supply would be tight-enough-for-long-enough that some demand erosion needed to take place. In June, prices reached levels that achieved just that, and demand appears to be softening in response. As a result, we lower our near-term price forecasts … Prices reached levels that are hard to absorb: Add to this tightness in the refining system and this explains why diesel and gasoline prices reached ~$187 and ~$180/bbl respectively in June. In response to the commodity-induced inflation surge, central banks are now hiking rates in-sync. Of the 38 central banks globally, 29 (or 77%) have hiked rates in the last 6 months. That percentage is at a 40-year high, making this the most-synchronized cycle of rate hikes since the early 1980s … This combination of factors continues to drive rapid downgrades to GDP expectations in all main regions. Our oil demand forecasts were not stretched, but equally, they were not designed for the breadth of rate hikes and magnitude of GDP slowdown that now appears to be unfolding. With actual oil demand data also starting to come in softer than expected, we lower our 2022e growth estimate from 2.2 to 2.0 mb/d, and our 2023e estimate from 2.7 to 1.8 mb/d”

Mr. Rats has reduced his fourth quarter WTI forecast by US$20 to US$107.50 and his second quarter of 2023 estimate from US$107.50 to US$97.50.

-

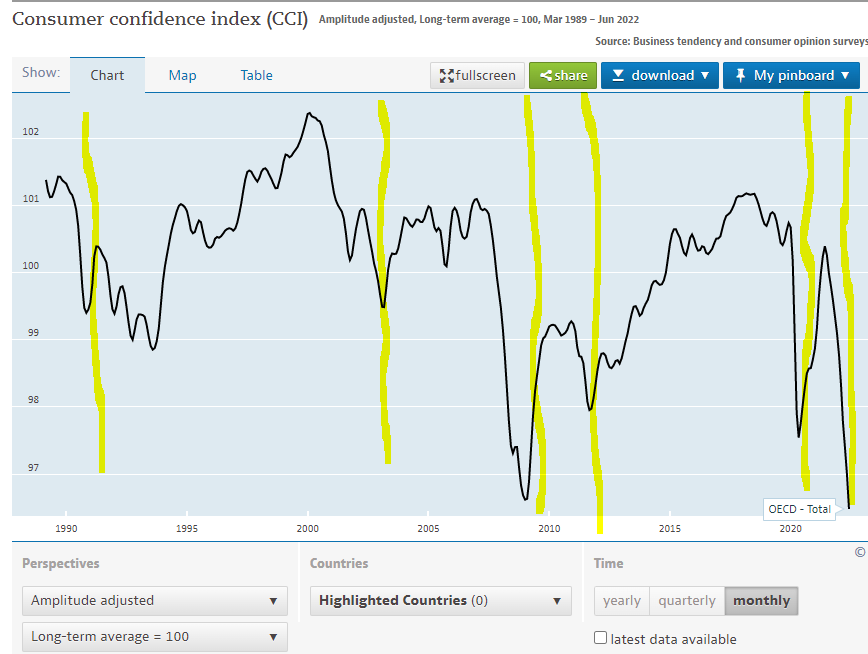

23 minutes ago, Spekulatius said:

@Viking - low consumer confidence has been an extremely reliable contrarian indicator (my guess is it seeps into investment decisions) and when you bought stocks when consumer confidence was at low levels, it has worked very well every single time.

Looks at the lows in 1990 (gulf war) 2002 (9/11, recession) 2008 (GFC), 2010 (Europe). 2020 (epidemic) 2022 (inflation).

@Spekulatius any of the 8 points i made above on their own are not a big deal for the overall economy and stock market. What i found interesting is these are all the headlines on just one day. And they are pretty broad based covering large parts of US and global economy. Bear markets can take years to play out. We will see.i am looking forward to seeing earnings from Microsoft, Alphabet and Apple. They have a habit of outperforming expectations.

-

Below are a few of the news headlines from today. Looks to me like the Fed is getting what it wants = slower economic growth. This is also a global phenomenon - not only happening in the US. Europe and China are also slowing. What does it mean for investors? Slower economic growth is now slowing revenue growth. Inflation is increasing expense growth. Slowing revenues + rising expenses = lower profitability. This dynamic is just getting started. Not a great set up for the stock market.

1.) “Walmart slashes profit outlook as food inflation wallops consumers”

2.) “GM cusbs discretionary spending and hiring; earnings miss estimates”

3.) “3M cuts sales and profit forecast”

4.) “UPS sees decline in package deliveries for second quarter”

5.) “McDonalds Q2 sales drop after Russia and Ukraine locations closed”

6.) “Shopify cutting 10% of workforce as e-commerce growth slows”

7.) “IMF cuts global economic forecasts for 2022 and 2023”

8.) “US consumer confidence drops to lowest since Feb 2021”

-

One of the unanswered questions is when will US end SPR oil release? I think the current release is set to end Sept 30. Sounds like that may be the end of it. 1 million barrels per day will come off the market.

—————'We can't be an oil supplier': Biden's adviser says oil reserve releases must end

One of Biden’s top energy aides confirmed Friday the administration won't extend the oil releases from the Strategic Petroleum Reserve that are scheduled to end this fall.

The Strategic Petroleum Release “was really a stop-gap measure,” says Amos Hochstein, Biden’s Special Presidential Coordinator for International Energy Affairs. “We can't be an oil supplier. It's a reserve and so we have to keep that.”

…Hochstein says he has secured promises from CEOs that investments being made now in improvements like drilling profiles and platforms will pay off with an increase of about 800,000 to a 1 million barrels a day towards the end of the year. This would replace, his argument goes, the 1 million additional barrels a day on the market right now because of Biden’s April move to release the oil reserves.

-

3 hours ago, Ulti said:

V,

your welcome…… I think the only solution is that the US , Canadian governments and energy producers get together and figure out how to increase production and exports while being environmentally aware… This also should include energy conservation and helping renewable energy along… As one gal said on the podcast… we are at war with Russia ( and maybe other autocratic states) and need to approach this crisis with that in mind… As an aside I like the Columbia podcasts/ always thoughtful

i think the ‘war footing’ analogy fits the current situation well. The logical thing to do is get all the players together and build out a 3-5-10 year step plan. Part of the plan would include the necessary investments to accelerate the transition to EV/renewables (power grid, materials etc). A kind of Marshall plan for energy. But herding cats is next to impossible in a democracy. So we try all the dumb things first and then, when catastrophe hits, finally do the right thing. I guess what is going on in Europe has not reached ‘catastrophe’ yet because Europe certainly doesn’t look interested in actually moving in a pragmatic direction. So the beatings will continue… -

1 hour ago, mcliu said:

I think many US/EU companies & funds have divested their oil sands investments.

Would US/EU take it further and pressure Canada to reduce or even stop production?

The big problem for Canada is the EU/US will look the other way for now and take all the oil/nat gas Canada can produce because the world is in an energy crisis. But as soon as the EU solves their current problem (it will take a couple of years) of course the knives will come out and Canada will be ostracized even more for its ‘dirty’ oil. This is likely one of the many reasons why oil producers in both Canada and the US are being so disciplined with new investment… they KNOW as soon as we get through this crisis Western governments will be coming to take them out behind the woodshed. The end result is supply will increase much more slowly than past cycles.

The supply issues will not get solved until the demonization of the industry by Western governments stops. And of course that is not going to happen. Just one of the many reasons why i find the current set-up for oil and gas so interesting.

—————Now in all fairness to Europe and the US most of Canada does not want oil or gas produced in Canada either. I live in BC - our current government tried to shut down the TMX pipeline. I don’t think it is too strong to say they loathe the oil and gas industry. Quebec is the same. Completely bizarre situation given how important the products are to maintaining and improving our standard of living.

RBC just did an analysis of the tax revenue the various levels of government actually will receive in 2022 from oil and gas… it is something like $64 billion. This pays for lots of hospitals, schools etc.

-

On 7/19/2022 at 5:15 PM, Ulti said:

@Ulti thank you for posting the podcast by Columbia Energy Exchange. It was excellent and a must listen for anyone who wants to better understand what is really going on right now in oil and gas. It is increasingly looking to me like we are in the beginning stages of a complete re-set in global energy markets. Putin has decided it is time to make Russia Great Again. And he is going to do it via oil and gas, the most important products on the planet. People who try and understand what Putin is doing right now through the lens of Ukraine are completely missing the forest for the trees.

Russia is firmly in control of global energy markets. Why is Russia in control? Because we are under supplied. And we will be undersupplied for years. At the same time demand continues to grow. Hydrocarbons are the core building block for our quality of life. Life/society as we know it is built on cheap energy. Leaders in the West have completely lost their minds demonizing the industry for years. Putin understands this stupidity and will leverage it to his advantage. The crazy thing is leaders in the West are doubling down on their hatred of oil and gas. Michael Lewis… you need to write a book on the complete catastrophe energy policy has become in the West (the stupidity he wrote about in Liars Poker or the Big Short pales in comparison).

The world is in the process of creating a Russia energy block and a West energy block (including Japan/Australia). And we will see in the coming years which block other countries in the globe decide to join. What about the Middle East? My guess is they will try and straddle the two blocks; their relationship with the US has been going downhill since Obama. If you are a poor country you will be joining the block that has the cheapest price; in fact you will resent Western countries for driving up the price as they are forced to replace Russian energy at any price. Putin will be happy to sell them cheap energy (hello India).

What does all this insanity mean for investors? It is a wickedly bullish set up for energy. The most important resource on the planet (oil and gas) has been completely turned on its head. And Putin has the ambition and the means to finish the job. Most investors do not yet grasp what is going on. The first inning has not even ended (baseball games are 9 innings for our non-North American readers).

————-

PS: what about the environment, you ask? Do you think Russia gives a shit about the environment? Are the citizens in Sri Lanka thinking about the environment right now? Priorities change when you can’t feed your kids or heat your home. What is the priority? Access to cheap oil and gas… the basic building block of life. Today. And for at least the next 10 years IF we make smart decisions. Much longer if we stay stupid.

-

Well the first half of 2022 has been pretty crazy. Simply following the Fed has been a very profitable strategy. The interesting thing is the US and Canadian economies are NOT rolling over. Most importantly, the labour market continues to be very strong - we still have a big shortage of workers in US and Canada. And Mr Market expects inflation to be transitory.

The second half of the year could be equally as interesting as the first half. The Fed appears intent on hiking until inflation shows signs of coming down materially. Yes, we likely have hit peak inflation at 8% but what if it is still running at 7% in early 2023?.

1.) What if oil goes to $150 this fall? Don’t think this is possible? Might want to read up on the energy crisis unfolding in Europe (that will be getting much, much worse with each passing month).2.) Buy anything made in Europe? Imagine the price increases COMING over the next 12-24 months just due to the spike in energy prices alone. Europe is also heavily unionized. Super inflationary.

3.) Who thinks rents are coming down any time soon with the cost of capital (interest rates) skyrocketing?

4.) Labour has to make up for lost ground the past 18 months - inflation has been ripping and wage increases have been too low.5.) China’s continuing zero covid policy/lock downs? Inflationary.

6.) Who thinks companies are done dramatically increasing prices (that is called inflation…)?

7.) We need to build chip plants in the US… bringing manufacturing back to the US in scale will be… yes, inflationary.

8.) The globe desperately needs to transition to clean energy (wind and solar)… yes, that will also be… inflationary. (get the raw materials, manufacture the panels, build transmission lines etc).

9.) Electric vehicles? Massively inflationary. Everyone needs to spend a shitload of money to make it possible (get the raw materials, electric grid, car manufacturing etc).

10.) Russia’s war on the West (Ukraine being a small part)… wars on this scale are… yes, inflationary. And this war is just 5 months old and will NOT be ending any time soon.

Do i need to continue? And people think inflation will be back down to 3 or even 4% in 2023? Dream on.

Bottom line, i am now seeing forecasts for Fed Funds Rate to exceed 4% with some calling for 4.5 to 5%. I know, I know… it will NEVER HAPPEN. Just like a year ago EVERYONE said higher rates (like we have now) were impossible due to high debt levels.

What to do? Continue to follow the Fed. They are not done. (QT just started 5 weeks ago!) And buckle up (expect more volatility).

—————

Please note, i am not saying people should build a bunker and buy ammunition and Spam. What i am saying is i think as long as the Fed continues to aggressively raise interest rates and engage in QT then assets/financial markets will struggle. We will get big rallies (like we are seeing now… yay!). And we likely will get another big sell off (perhaps multiple). What investors do will depend on their age, financial situation, risk tolerances, financial objectives, investing style etc. Good luck and may we all prosper

-

A couple of good overviews of the nat gas situation in Europe.

—————

Looming Natural Gas Shortages Has the EU Scrambling for Solutions

With the threat of recession and further inflation, Vladimir Putin could deal a devastating blow to the European Union if he cuts gas supplies this winter. Should that happen, it would be a major test of solidarity for the block.

—————

The Anatomy of Germany's Reliance on Russian Natural Gas

The Americans warned Germany, as did the Eastern Europeans. But Germany just continued buying more and more natural gas from Russia. The addiction stretches back several decades, and it is full of misjudgments and errors.

…Anyone could have recognized that energy shortfalls were a distinct possibility. Instead, though, Germany's political parties forged ahead and set about abandoning technologies to save the climate. The nuclear phase-out was accelerated in 2011, followed by decision to phase-out of coal in 2018. And along the way, Germany decided not to access its own natural gas, since it involved fracking, and shunned natural gas from the United States for the same reason.

But the great energy transition failed to materialize, or at least it hasn't taken shape quickly enough. "We elevated our climate goals, but even today, we still don't know how we are going to achieve them," says a leading economic policymaker from the center-left Social Democrats, the party of Chancellor Olaf Sholz. Altmaier also speaks of how surprised he was when he became environment minister in 2012 and found no master plan waiting for him for how the country planned to secure its energy supply while also phasing out all fossil fuels by 2050.

Time Has Run Out: As a result, desires have transformed into a reality in which the approval process for a wind turbine can sometimes take as long as six years. And in the meantime, political and business leaders elected to rely on what was left, and which was the most profitable for companies anyway: cheap Russian natural gas. -

4 hours ago, Kupotea said:

Agreed but supply is only so elastic. With a current deficit and spare capacity almost fully tapped you get demand destruction as the balancing factor.

You need a way to encourage supply growth in what many see as a sunset industry. If we do get a recession and oil prices collapse do we not just end up with a bigger gap coming out of the other side? If the economy muddles along how long does it take to fill the current deficit?

I think we continue to grind higher until the economy breaks or the investment community changes their minds on the need for higher capex.

The comment was made somewhere before: oil is effectively in runoff.

Politically speaking we are currently in the BEST OF TIMES for oil companies. Political risk from governments in the West will only get worse from here. Higher, and possibly much higher costs are coming in the future. Higher taxes likely coming too. Profit tax. Carbon tax. Oil companies will be a piggy bank for Western governments (someone has to pay for climate change/ESG/energy transition).

What is a rational oil company to do? Sweat the assets for as much cash as possible as fast as possible. Cherry pick your best assets. Acquisitions only make sense if they are strategic and/or have an exceptionally quick payback. How do you even value a long life assets like the oil sands?

What all this means is perhaps oil companies remain permanently on sale. Suggests to me that dividends are a much better ‘shareholder return’ option that stock buybacks. Long term? Who cares!

Perhaps the biggest takeaway is supply is likely permanently screwed moving forward. Who in their right mind is going to sink billions in large projects that will only start producing in 6 or 7 years? (I was thinking of the recent announcements for Newfoundland.) And the case to invest in new production will only get worse with each passing year.

—————What an absolutely crazy incentive system. Because oil is actually essential to life as we know it today.

—————Where this really gets interesting is… what if we do not transition to alternatives as fast as people assume? What if it takes 10 more years before we are ready to start the transition to alternatives for real? We will have a scenario where demand for oil keeps growing and supply remains increasingly constrained. Oil prices will remain high (and will likely go much higher). And the “high oil prices solves the problem of high oil prices” moment actually never comes…

Where Does the Global Economy Go From Here?

in General Discussion

Posted · Edited by Viking

immigration policy is just like any other government policy. It should be well thought out and rational. What little i know of Canada’s immigration policy sounds ok to me. Like i said before, i do not follow the US.

My views of immigration have been shaped by personal experience. My wife’s family came to Canada in the 1950’s from Italy. Talking to my mother in law - pretty much all the negatives about immigration you posted earlier were strongly felt by lots of Canadians in the 1950’s. My mother in law hated living in Canada for the first 5 years or so… why did she do it? She wanted a better life for her kids (than what was then available in Italy). So she and her husband worked their asses off to build a life for their 3 kids (2 were born in Canada). They succeeded in building a very good life. How? Work ethic. Thrift. Love of family. Value of education. Love of community and country (this last one took some time). Kids? One’s a nurse, another was a professional hockey player and the third (my wife) graduated from university and worked in HR. My mother in law laughs at the idea of moving back to Italy.

A second story: one of my best friend’s (who i have known since high school) family came to Canada in the 1970’s from India. Same story as my wife’s parents. Parents worked their ass off. Pretty much all the negatives about immigration you posted earlier were strongly felt by lots of Canadians in the 1970’s (especially in my rural home town) so my friends family had to deal with all of that. The parents passed on great set of values to kids: value of education, work ethic, thrift, importance of family etc. Kids all went to university and have built great lives for themselves and their families (two are senior administrators in education system).

I have been telling my kids for years that i am going to screw their lives up. Because i am going to do what many non-immigrant Canadian families do: they want to give their kids a better life. Free of hardship. So they spoil their kids. Who then grow up with an entitled attitude… they DESERVE a great live. Shitty work ethic. Shitty attitude. Scoff at education. Money morons.

i tell my kids to talk to their grandmother. To hear the stories of growing up in Italy during the second world war. Coming to a country where you could barely speak the language and everyone hated you for ‘stealing’ jobs etc. Working in the mines in BC in the 1950’s. Working 2 full time jobs for close to 10 years to get a leg up. I want my kids to hear first hand what life is really like for most of the worlds population. I also tell my kids that living in Canada is a gift - one that they need to be thankful for and take full advantage of. I think immigration is important in part because it provides the next wave of parents who want to make a better life for their kids. Yes, just like parents of every generation going back hundreds of years.