SafetyinNumbers

-

Posts

2,822 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

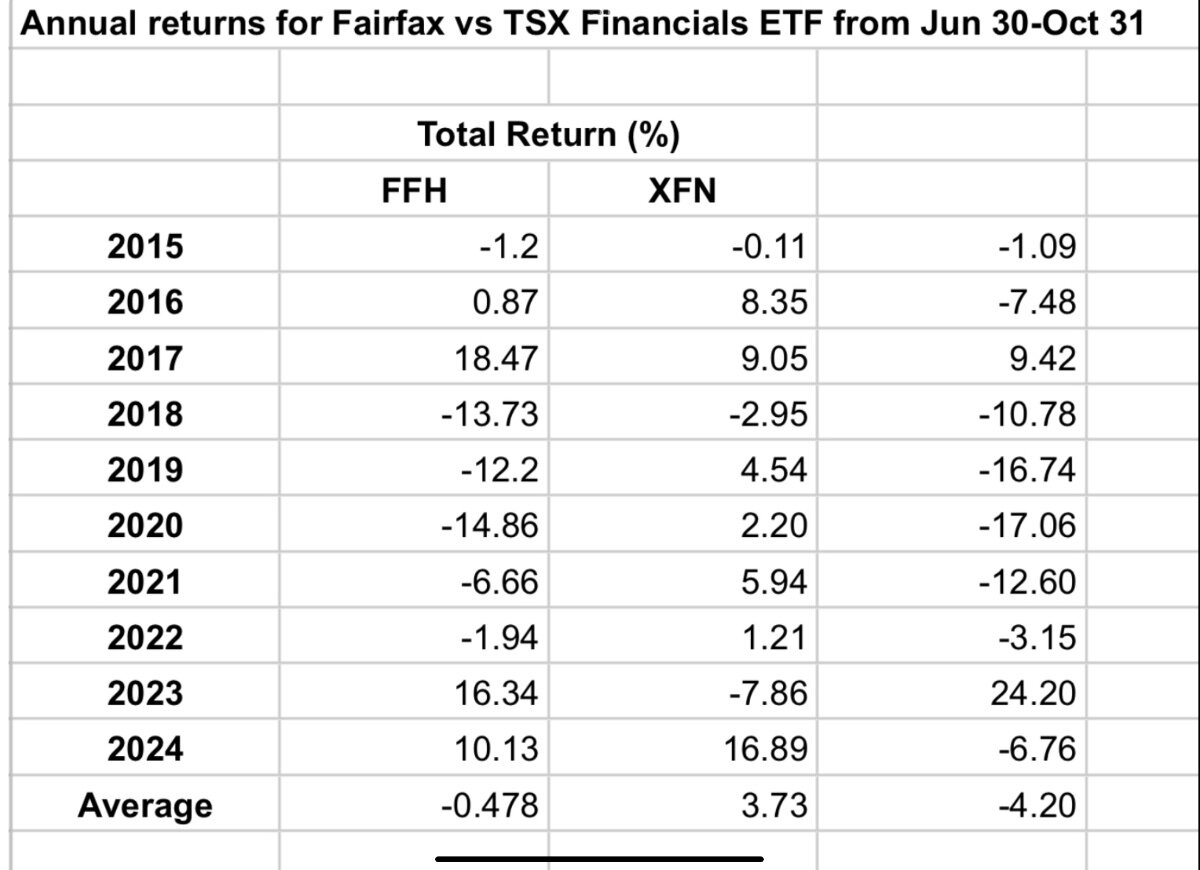

I was trained to always understand why my positions weren’t “working” because I usually had a someone at the bank looking over my shoulder asking me why I was losing money It makes sense when one considers how money is managed and who the marginal buyers and sellers are. No high turnover PM wants to look stupid owning a company that insures against hurricanes during hurricane season. If they lose money, they should have known better. From November through to Q1 earnings there is a lot of good news with three earnings reports, the shareholder letter and the AGM. I think @kodiak calling FFH a fat pitch on the Business Brew podcast helped defeat seasonality in 2023 or it was just that investment income and float were growing so fast that long term investors offset the marginal sellers.

-

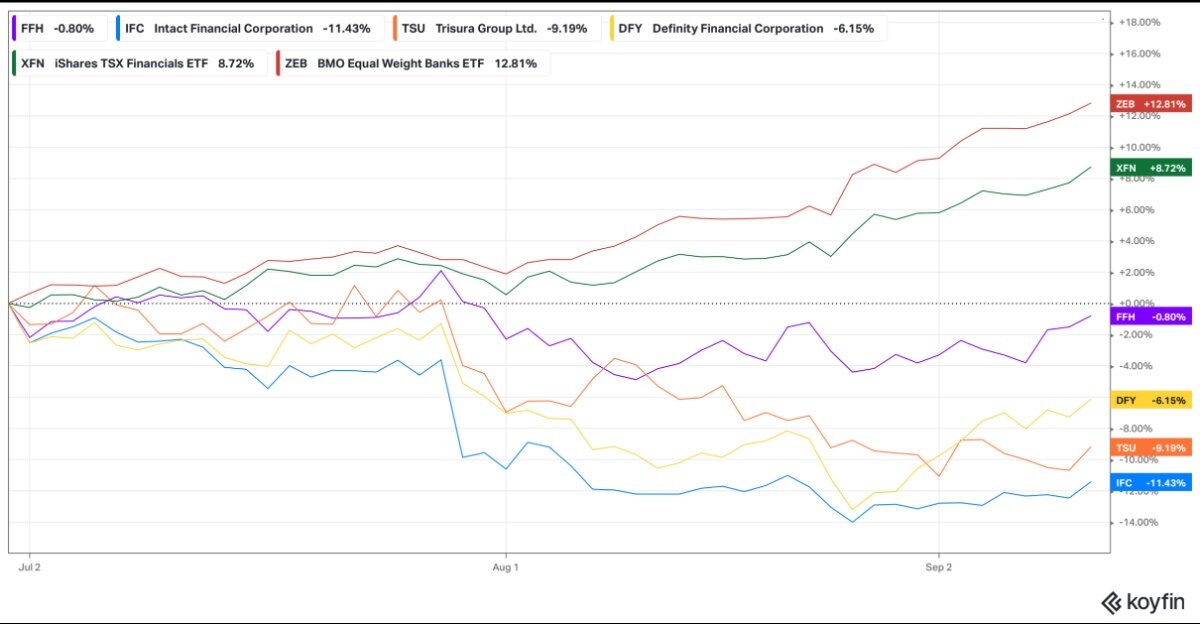

I still try to understand the flows. I think I have a good idea why we are going sideways recently including the historical underperformance during hurricane season and this year the rotation out of P&C insurers into more economically sensitive financials like banks. FFH has actually outperformed in a pretty big way vs the other P&C insurers.

-

I probably don’t have to use leverage too but I am.

-

I bought a few shares at $2340 a few weeks ago. It’s still over 50% as a percentage of net assets but I couldn’t help myself. It’s been a big mindset change for me to add at higher prices but the longer I own it, the better I understand the business and how cheap it is on an absolute and relative basis.

-

Correct. The value seems pretty clear. The surprise to me is that they bought so much during hurricane season although with slower premium growth there is more excess capital for buybacks. Hopefully we’ll also see them take in the Allied World minority in the next 3-6 months.

-

It seems to be regular buybacks and not an unwinding of the TRS. Last year when they unwound some of the TRS, it was done as a block trade which makes sense because price really doesn’t matter and the counterparty owns the shares. I suspect we’ll see another block trade at some point in December which will be TRS related.

-

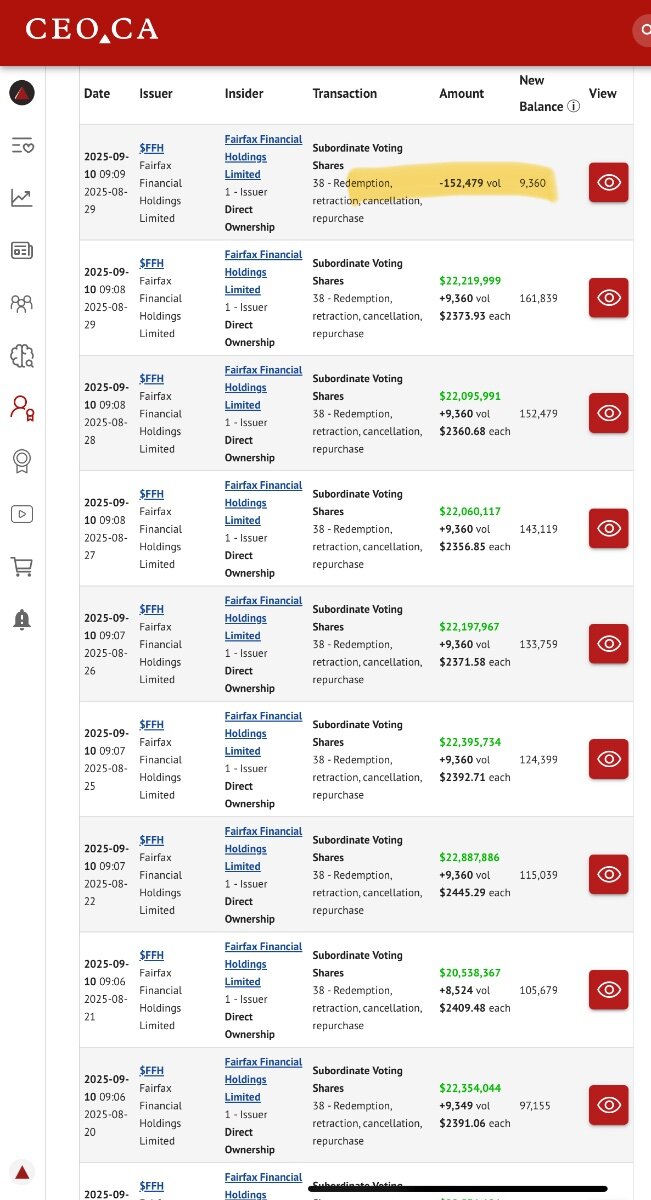

FFH cancelled 152k shares in August 2025 which is more in August than in the last three years combined.

-

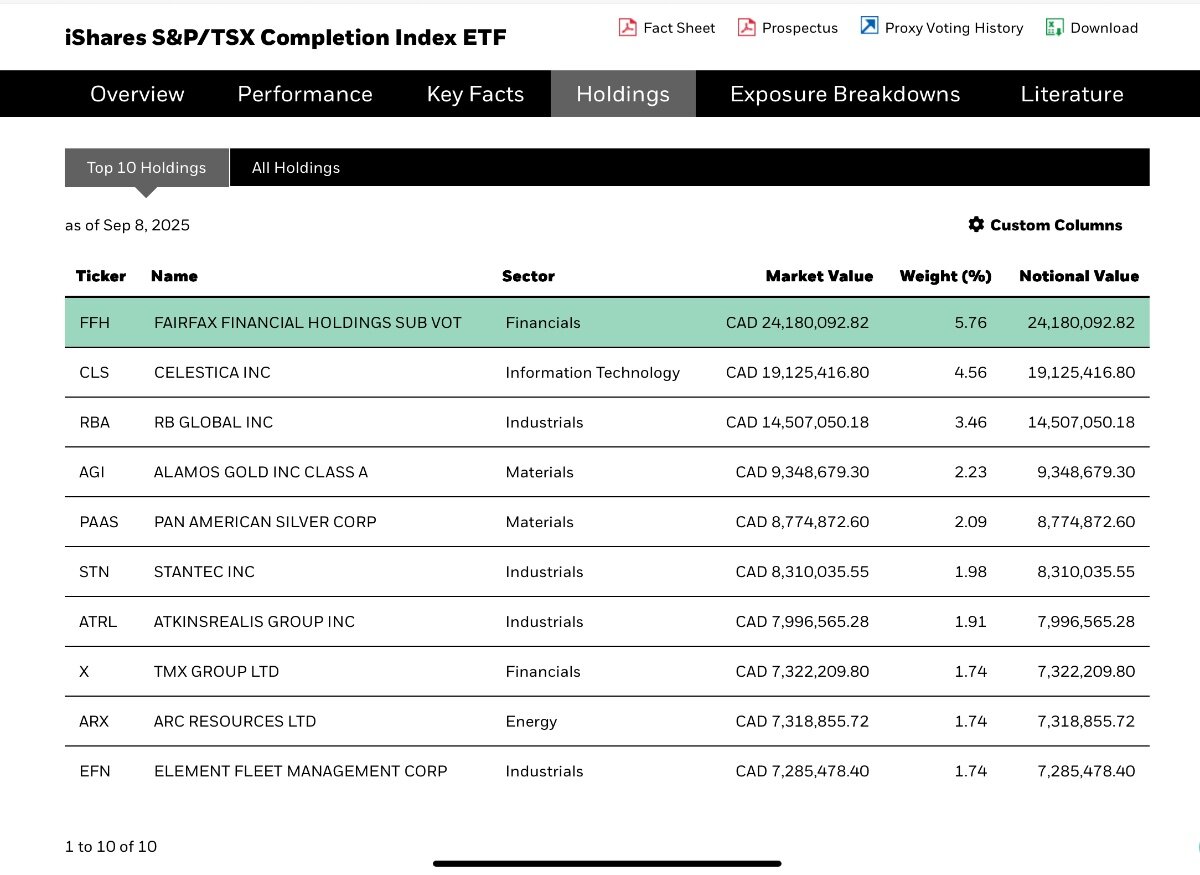

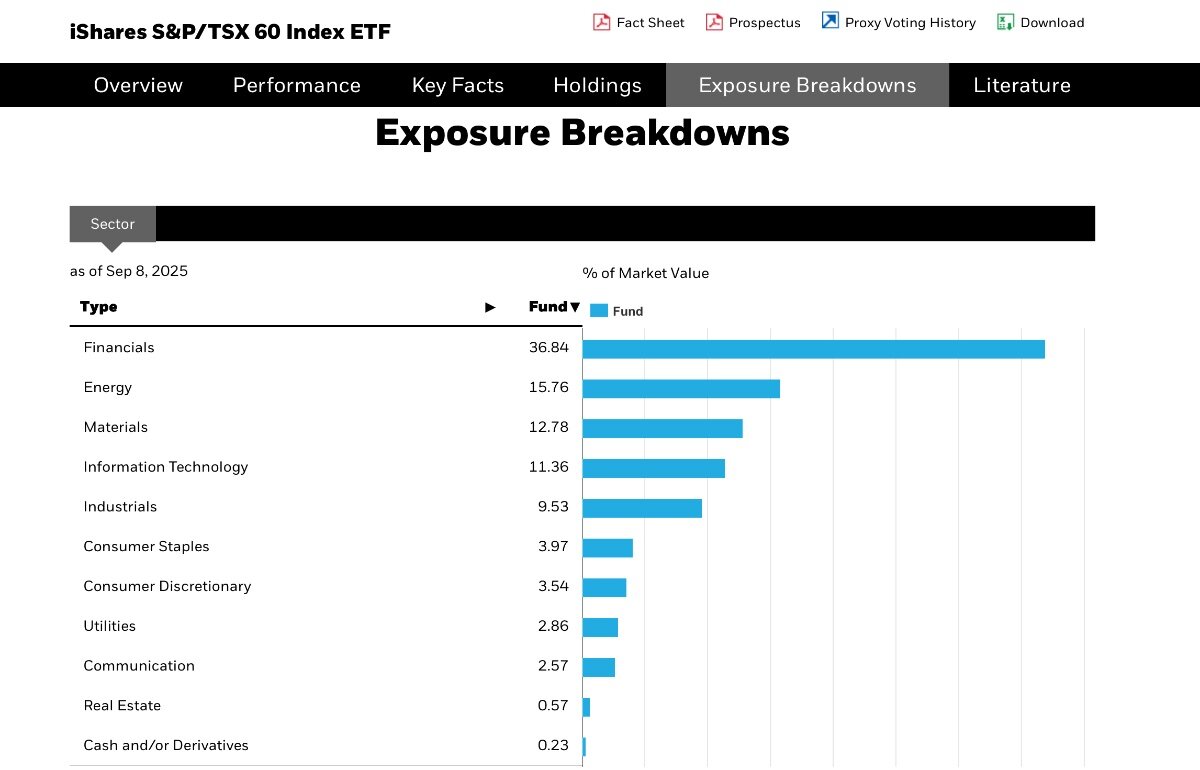

RBA is an Industrial as shown below but the same logic applies. Scotia is apparently out with a note today and have RBA as their top pick to replace. The committee apparently told brokers last year that size matters more than sector weighting but it probably matters what the relative size is when it happens. Last year FFH was much bigger than TFII the next biggest component, right now the spread is smaller.

-

For sure. The longer it takes the better but it happens when it happens.

-

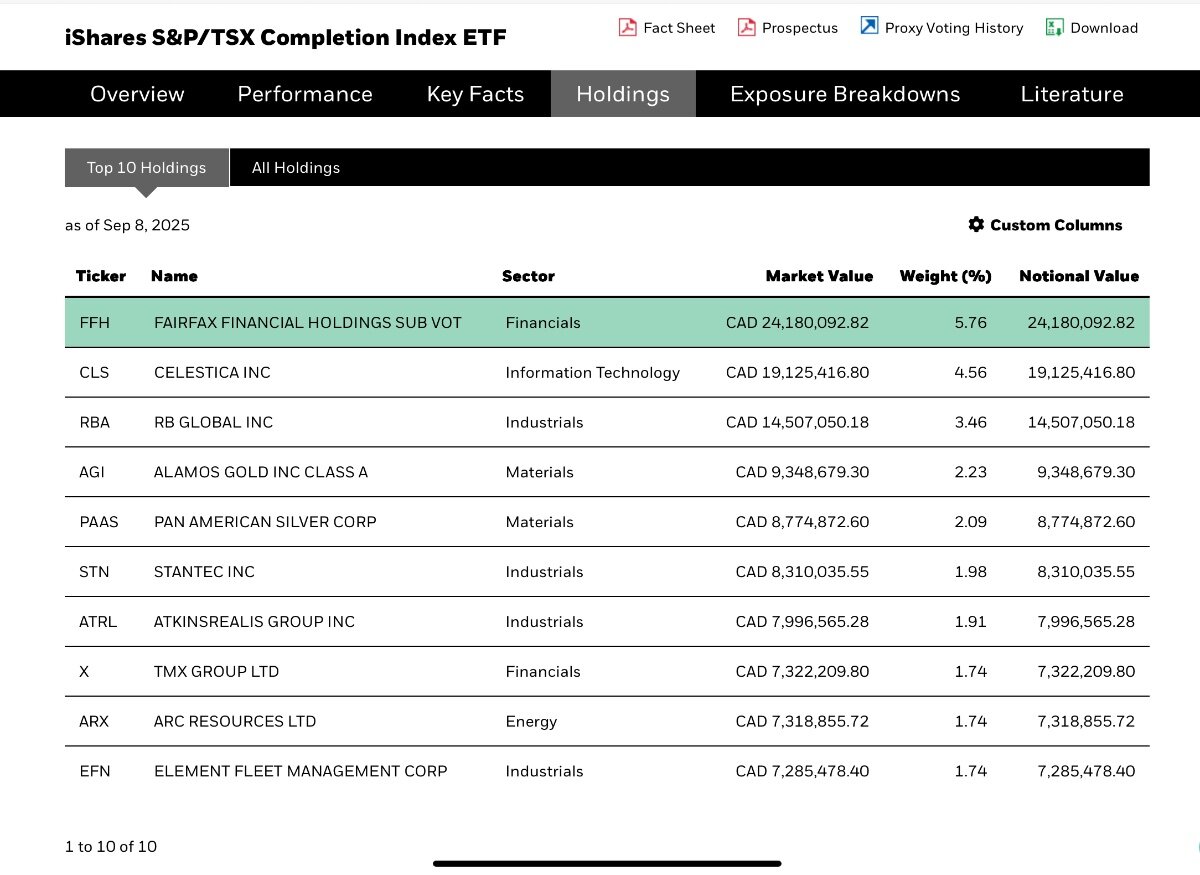

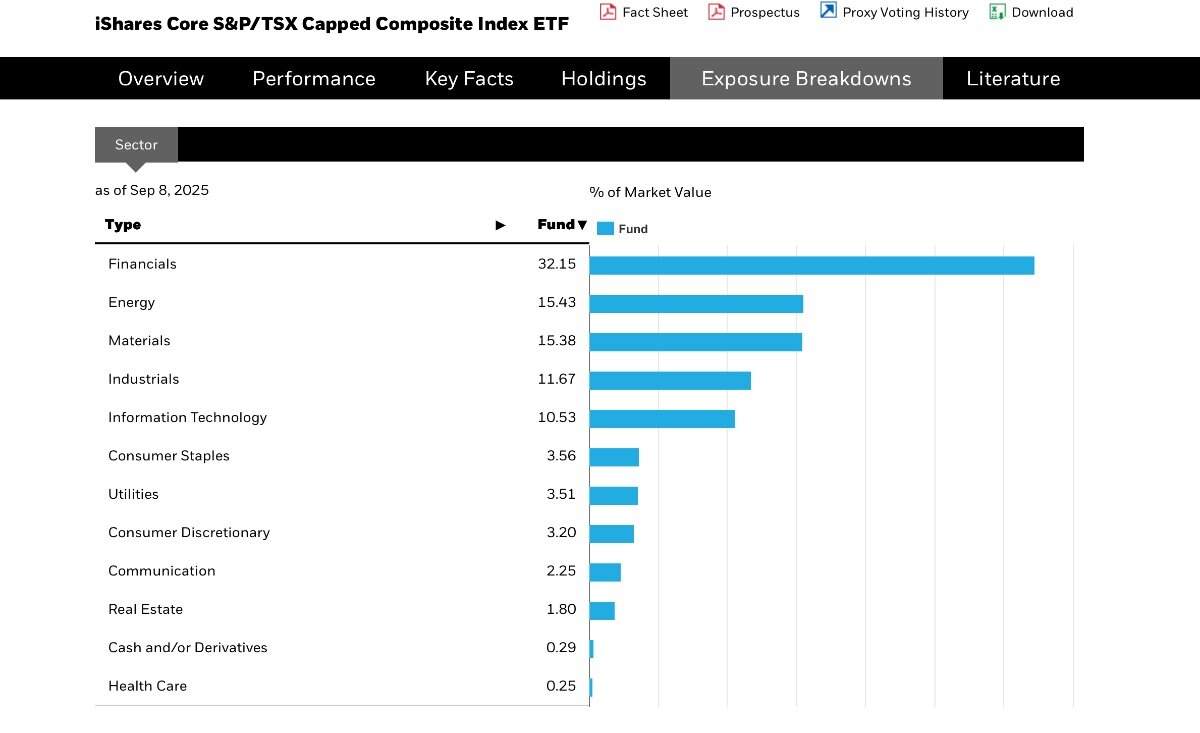

I posted about this on Twitter last night (@brownmarubozu if anyone is interested). It does look highly probable that an opening is coming in the next 12-18 months. The other two alternatives are CLS and RBA which are smaller but not financials so it’s possible they will skip FFH in their favour. Here is what the weightings look like now. I also included the exposure breakdowns. They could jump to RBA and justify it based on the industrial weighting.

-

Ultimately, it’s the leverage that is important for FFH going forward but I don’t think it’s so high that we have sweat at night. Historically, FFH did have some moments where shareholders were sweating at night but I think it’s in a much better position now. @Haryana if you are doing the analysis on leverage, I would look at the insurance float to equity ratio and debt to equity ratio. For the latter, I think the holdco debt matters more as some businesses like a utility might run with high leverage given the nature of the industry. Another way to do it would be to analyze investments to equity annually which in effect captures both the insurance float and any other debt. 3:1 investments to equity ratio can yield really amazing returns in a high nominal yield world. Seems like very good protection against inflation. Twenty years ago the street would have figured it out already but the market structure now makes money management a very different game.

-

Poseidon and Ki (which is not in the investment portfolio) are two others that really stack the deck for ROE to exceed 15% over the next 5 years. For BIAL probably need to add in the 20% performance fee which they get on 69% of the gain (5% is held by OMERS via Anchorage).

-

Looks like Fairfax sold some Metlen https://www.athexgroup.gr/sites/default/files/hermes_3/2025-09/el/c8d604f8-a1f1-4fe5-9604-f8a1f1cfe5be/1528_6356_2025_Greek_English_1.pdf

-

Class A fee structure: management fee 1.5% performance fee 20% hurdle rate 6% with a high-water mark Class I fee structure: management fee 0% performance fee 25% hurdle rate 6% with a high-water mark

-

I agree other insurance companies don’t do it because their incentives are short term and also because with equities there are going to be mistakes. Look at how many people still avoid Fairfax because of its mistakes over the years. It follows that it is still impacting the multiple. Most management teams want to give the market what they want (steady predictable growth on an adjusted earnings basis) which leads to a high multiple. It is ideal for raising capital to do accretive deals. Fairfax is the opposite. They don’t do anything to get a higher multiple but the quality of the shareholder base is improving over time which might lead to an appropriate multiple at some point.

-

I like this table to show the ROE decomposition. I think a 96 combined is way too conservative. More likely to be under 94 than 96 over the next 5 years, in my opinion as reserve releases ramp and they benefit from scale. Also, net premiums are closer to $28b and growing.

-

The Hamblin Watsa investment style is expected value and most investors are quality investors. On this board quality with a value screen. Quality investors don’t accept that a third of the investments will likely be duds and that we don’t know which investments will be duds ahead of time. I think @73 Reds is correct, that the focus should be on the results. I’m not sure we’ve ever had more visibility on future results so it’s easy to own at such a cheap valuation. If it starts getting cloudy at a high valuation it will be more difficult to own.

-

I really like this chart as I think it demonstrates that cat loss risk is about the same as it was a decade ago but net premiums written and shareholder’s equity are a lot bigger.

-

The message I keep hearing is a focus on quality. What is the last distressed asset they bought?

-

I think all of the gains that are being recognized annually as the portfolio turns over gives some clues as to how value surfaces over time.

-

I’m not sure it’s a coincidence

-

Allied and Odyssey had a lot of CAT losses

-

I don’t think they have a lot of distressed assets left. It’s just how accounting works that delays the recognition in the accounting statements for the increase in the multiple which comes when they liquidate the position. I’m not sure why that changes under Wade and Lawrence.

-

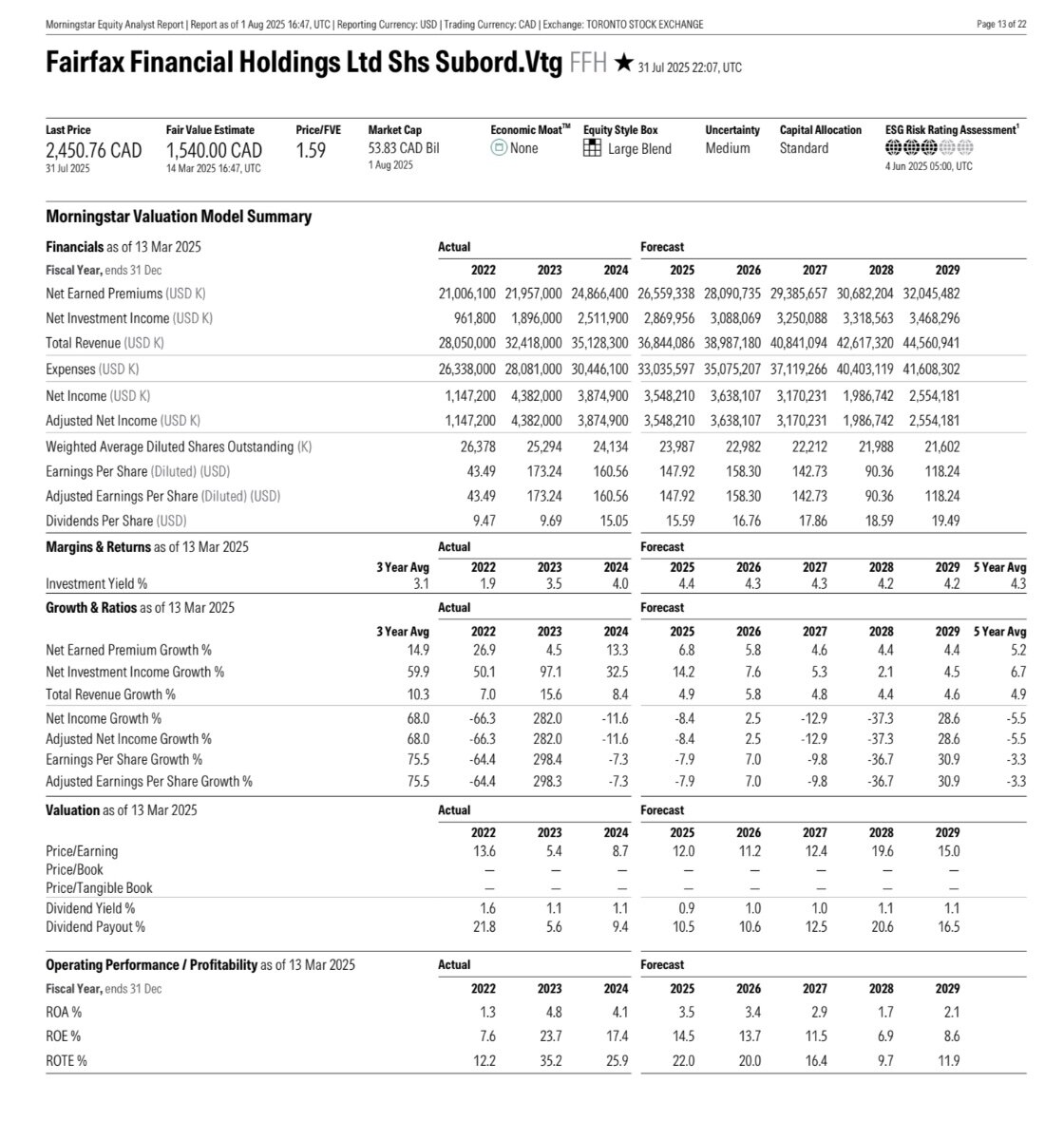

Actually he’s got pretty healthy growth in investment income.From my quick review, he doesn’t have anything for gains and expects underwriting to get much worse.

-

A Morningstar computer sets the target. He sets the moat rating and the financial estimates. It’s not surprising the algorithm doesn’t like the no moat rated stock where earnings are ultimately collapsing.