SafetyinNumbers

-

Posts

2,822 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

Fairfax didn’t increase their stake in Atlas. Their partners wanted to take it private.

-

How do you determine FFH is fairly priced?

-

The capital treatment for the insurance subsidiaries is the reason. You should ask the question on the conference call Friday.

-

NAV discount started in 2013 and efforts to close it started in 2020. Of course, the bigger the discount, the lower the historical return. It doesn’t mean the intrinsic value didn’t increase. Still a ~40%+ discount to liquidation value for very marketable assets including 1.48m shares of VOO!

-

Not going to happen with Fairfax India. Private Indian companies won’t get the same capital treatment as a TSX listed company.

-

I really like this deal. Diversified, asset backed, growing capital light management business and a good place to pick up returns above treasuries if the yield curve goes lower. The business benefits from lower interest rates so should help assuage concerns of those who think duration is too low and the whole yield curve is going lower.

-

This is pretty cool

-

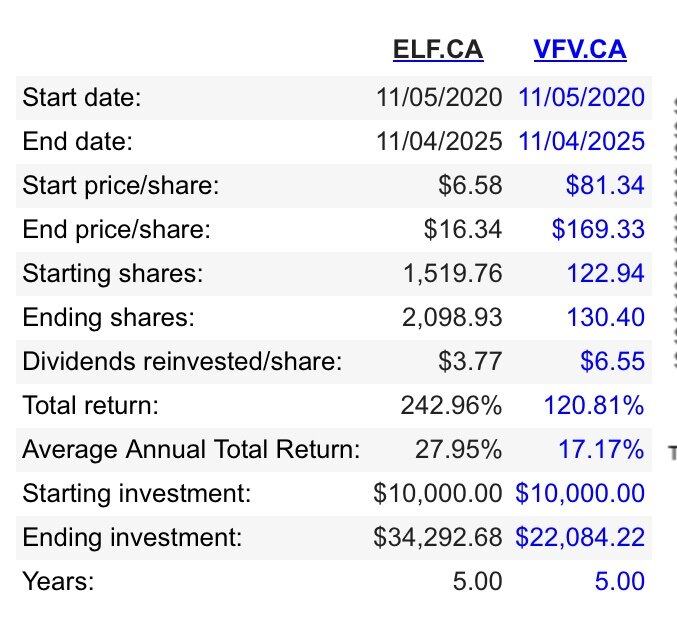

I still think it makes sense to buy ELF.TO instead of VOO. Give up some liquidity for margin of safety.

-

Yes, AI got it wrong. This disclosure is in the 2024 AR:

-

I think he made the purchase on margin too which likely influenced the decision.

-

The short answers are 1) The stock doesn’t pass their checklists (heuristics) and if it does 2) the portfolio doesn’t pass their checklists and if they get to 3) they use very conservative instead of realistic estimates and have such high hurdles that they still can’t get there. Mostly though the hurdle is finding room for a new investment as avoiding taxes on something already in the portfolio is paramount.

-

I was trying to determine if it was a concentration issue or a hurdle rate issue. Turns out it was the latter. I recently presented to a bunch of investors on the top 3 reasons why they didn’t own Fairfax and hurdle rate was #3. My own analysis suggests high teens+ ROE is more likely for the next 5 years so I’m happy to buy at this price. Fairfax has a hurdle rate of 15% themselves and they are buyers a hundred plus dollars higher which is nice confirmation.

-

Nice. Hoping it continues for the next 25!

-

That’s a pretty high hurdle. How have you done so far?

-

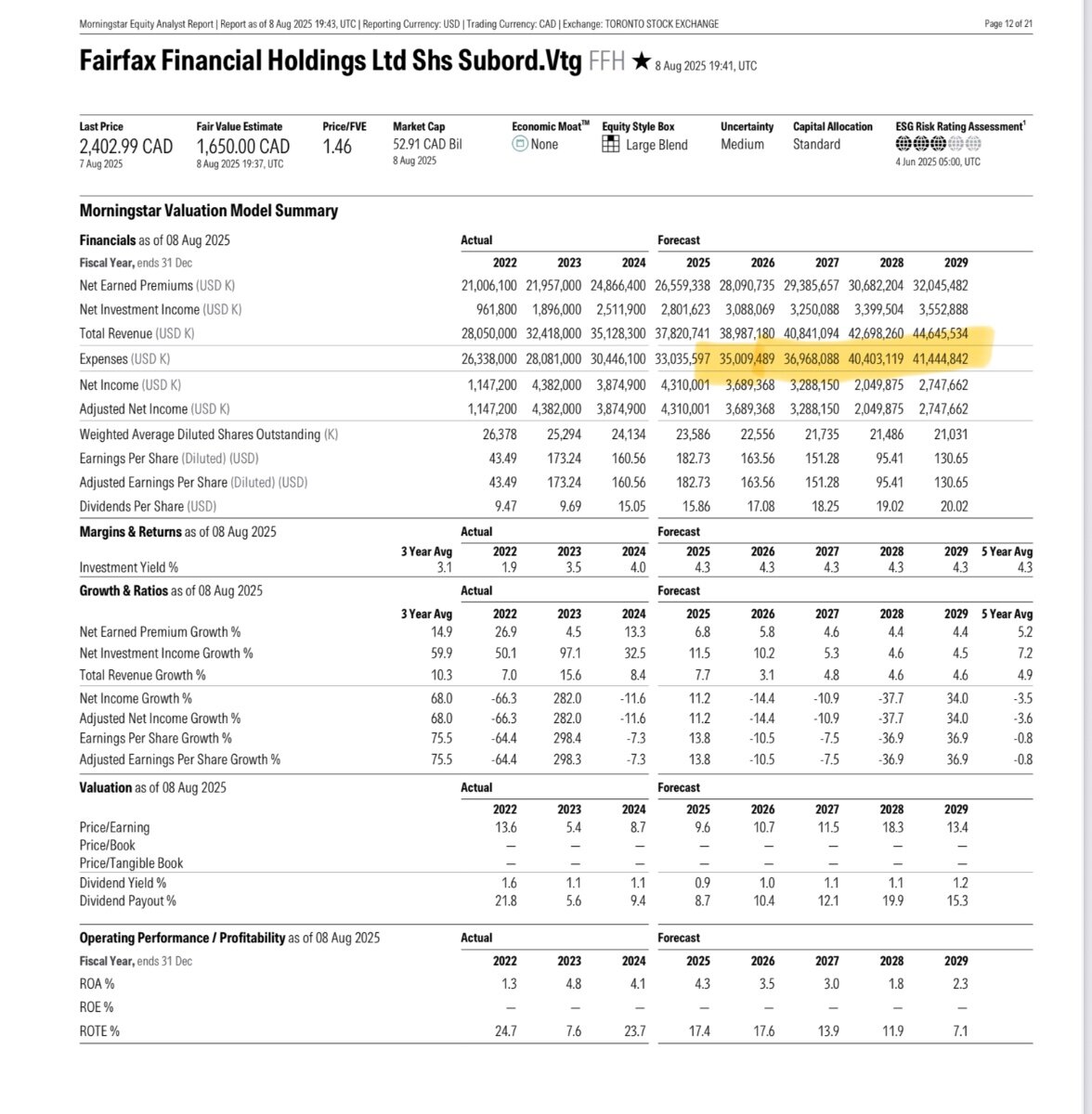

There is only 1 analyst with estimates in 2028-29 and that’s Morningstar. He forecasts unusually high cat losses in the out years. Generally, quants don’t like P&C insurance because it’s lumpy and the float looks like debt but this guy is also not a good analyst.

-

Substack post on why this time of year is usually a good time to add to Fairfax. https://open.substack.com/pub/berczyparkcapital/p/fairfax-financial-seasonality-opportunity?r=ecc87&utm_campaign=post&utm_medium=web&showWelcomeOnShare=false

-

I appreciate you think it’s too expensive to add to your already large position but to be clear hypothetically if you didn’t own any, you would not start a new position unless it traded below book value. Is that correct?

-

I think in the last year at some point you said you wouldn’t start a new position in FFH if you didn’t own one already. Is that still the case?

-

MKL reacted pretty well to its beat.

-

So pessimistic! I think closer to 90 vs 95 but I am an optimist.

-

I think that’s just called analysis. The BMO analyst on the other hand expects higher cat losses than last year and a combined ratio of 97.9.

-

The first book on Buffett/BRK came out in 1992. At the end of 1991, BRK traded around 1.4x BV and the multiple proceeded to double over the next 5 years. It makes sense as book readers might be the type to buy (demand) and hold (reduce future supply). It took until BRK issued stock (increased supply) for the Gen Re deal for the multiple to come down.

-

I don’t think of it as trying to time the market but taking an expected value approach to fixed income investing much as they do with equity investing. I’m not expecting them to trade every move correctly, that would be impossible. If you ever do the study, please share.

-

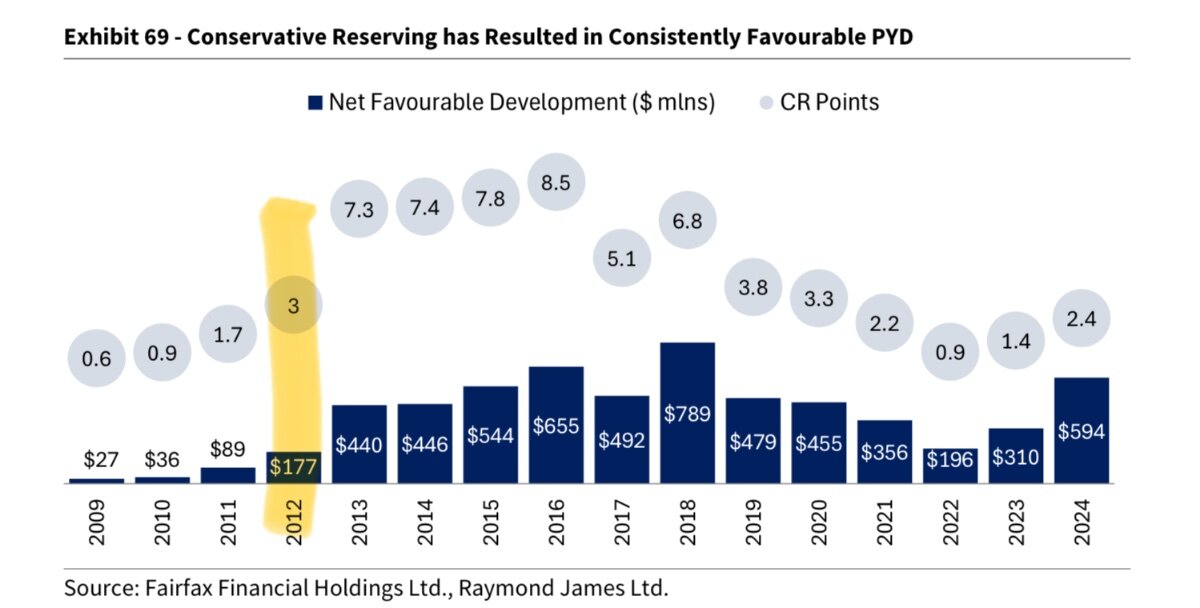

I think this chart shows how reserve releases are cyclical. It makes sense as high reserves are booked in a hard market and if there are no unfavourable developments have to be released in line with average claim duration (4 years). Premiums were growing fast 4 years ago and with slower premium growth since 2024, the reserve releases should have growing impact.

-

Very much disagree with the conclusion that underwriting income is going to be reduced. Premium and float growth will be reduced as we will write less business. I expect combined ratios to actually go lower over the next 4 years as reserves are released from the hard market over the past 4 years.