SafetyinNumbers

-

Posts

2,805 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

This is the opposite of battening down the hatches. Perpetual preferred gives more flexibility not less. This was a decision based on maximizing returns as they replaced the preferred with long term debt which has tax advantages as you noted.

-

That plus these are rate reset preferred that were issued when interest rates were lower and when CAD was closer to par. Another example how Fairfax extracts returns from every part of the capital structure.

-

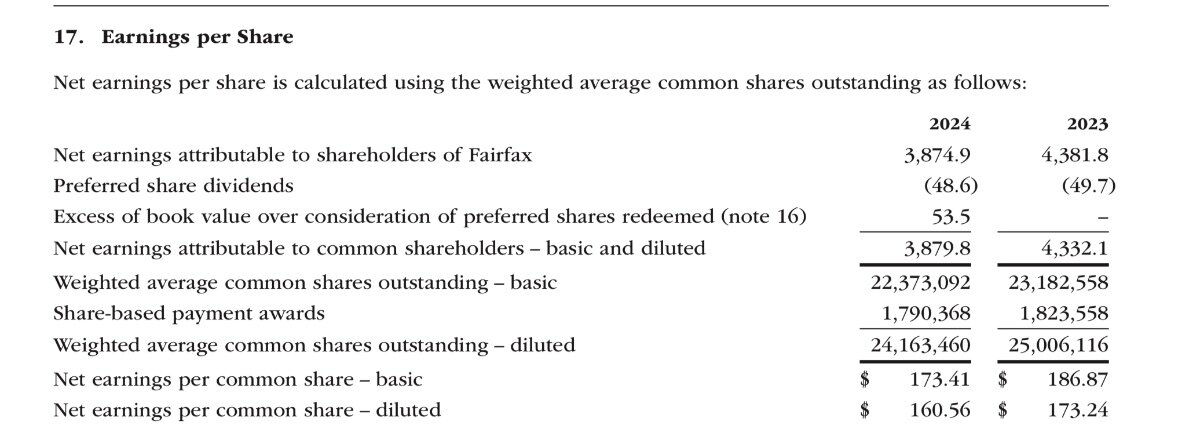

Fairfax preferred were not convertible like @Hoodlum ‘s example above so there is no impact on diluted share count but preferred dividends do reduce net income available to common shareholders. Further, to the extent the preferred are bought back below book value, they will boost net income by that amount.

-

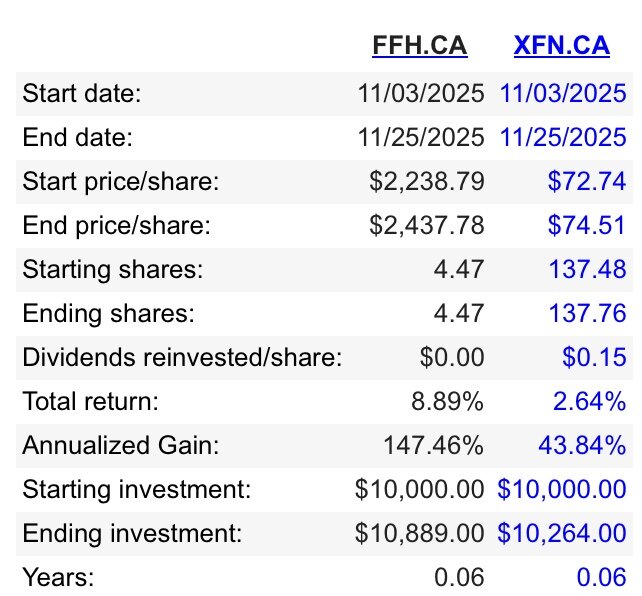

it’s a good day to buy it if the month end mark matters.

-

This is the track record to the end of Q325 and performance for the public stocks this quarter.

-

It’s the tiny chance of deal break vs the certainty of return above the cost of borrowing. That’s basically the strategy of risk arb funds. I used to manage the Canadian risk arb strategy for UBS prop so I have a different perspective. I think there are lots of interesting things to buy but hard to beat Fairfax or Fairfax India which are about 63% of my net assets.

-

Special committee first learns about it at the time of proposal. Usually insider bids get a bump like Atlas but always possible it doesn’t like Recipe. The closer it trades to the deal price the more sense it makes to sell. If I wasn’t using leverage to fund the purchase, I wouldn’t own it.

-

I bought a tiny amount post deal announcement. I think there is a decent chance of a bump and the dividend helps to carry the position. Really depends on what you plan to do with the proceeds and/or your cost of capital.

-

How do you decide when to sell?

-

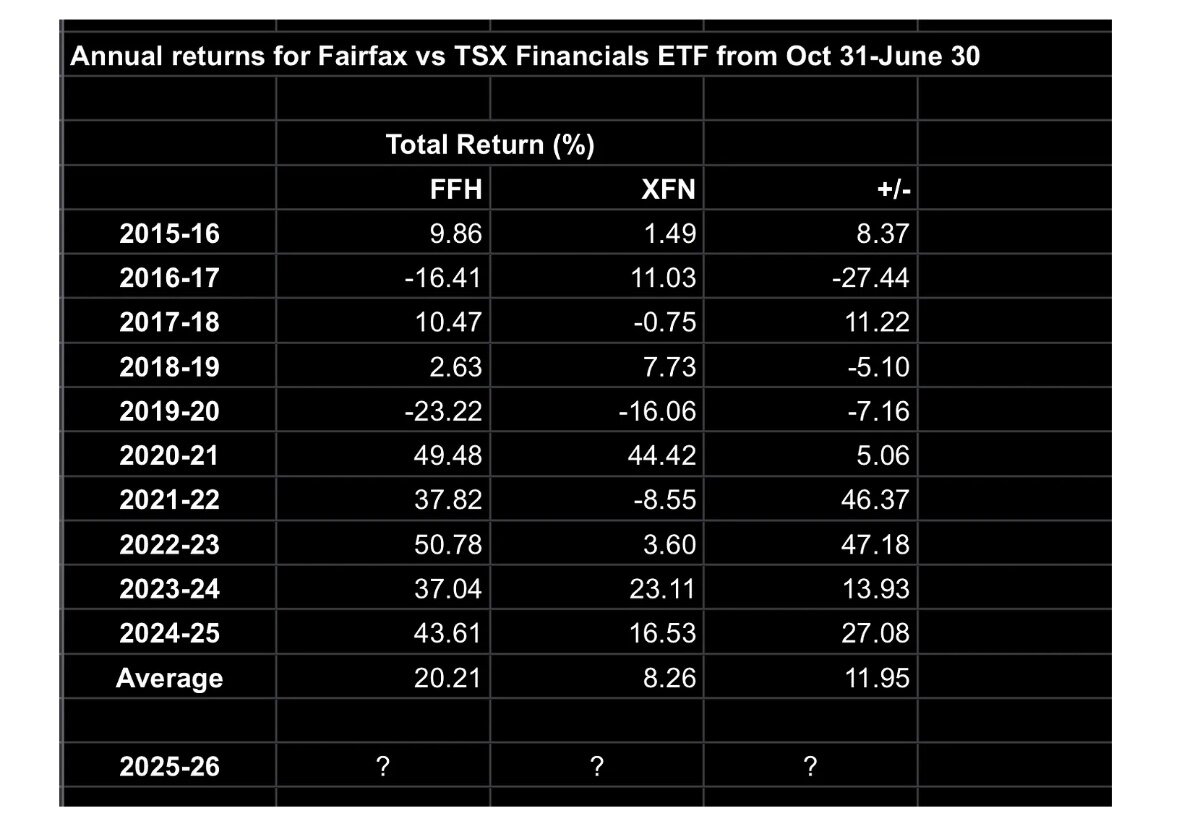

Also, clearly not believers in historical seasonality . The last 5 years in particular have been strong and this season has started well. I wrote about it a few weeks ago on substack. We could just be getting started. https://open.substack.com/pub/berczyparkcapital/p/fairfax-financial-seasonality-opportunity?r=ecc87&utm_campaign=post&utm_medium=web&showWelcomeOnShare=false

-

It doesn’t account for the range of possibilities including compounding.

-

You are annualizing quarterly earnings which is conservative and since you already own it, it doesn’t matter that the right tail might be a lot higher than you are willing to give credit for. On your own numbers < 10x earnings is cheap for most investors but not for you.

-

I don’t but I assume 5% for fixed income given they tell us the average coupon and then play with different equity portfolio returns weighting fixed income at two thirds and non-fixed income at one third. As I discussed in this substack back in February, expectations for the equity portfolio look especially low after factoring in returns on the biggest positions which are equity accounted for a flow into EPS. https://open.substack.com/pub/berczyparkcapital/p/fairfax-financial-a-generational?r=ecc87&utm_campaign=post&utm_medium=web&showWelcomeOnShare=false

-

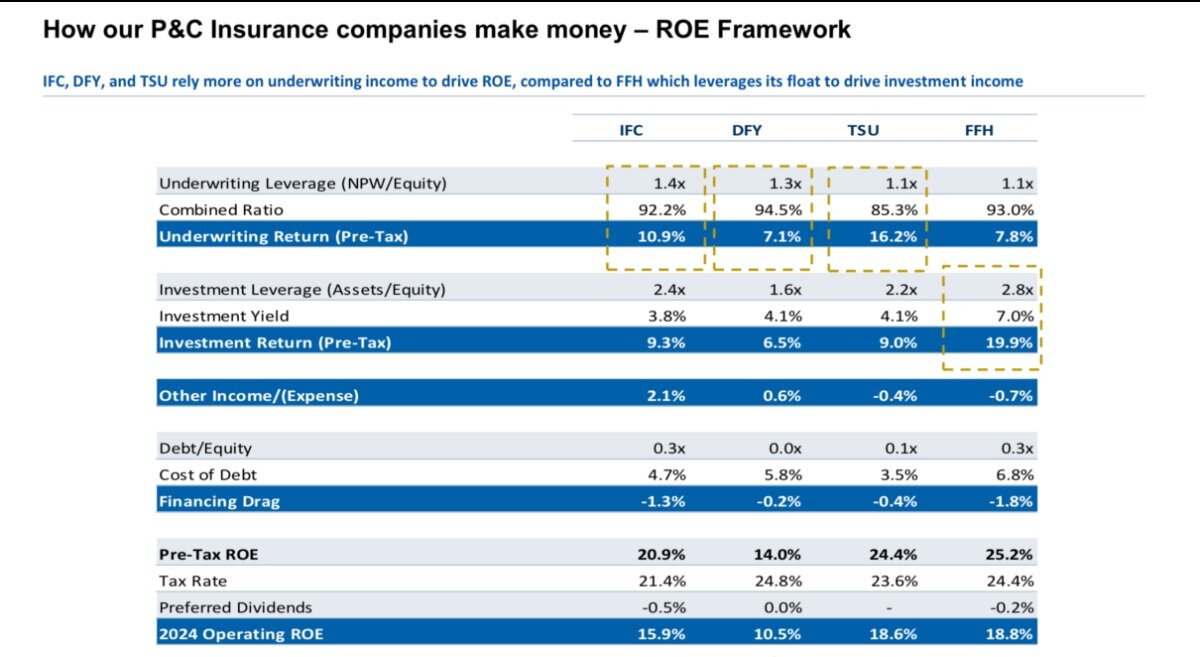

Thanks. I thought maybe you had a range of assumptions for premiums, combined ratio and investment returns. I like the below model for quick analysis to get to an expected ROE range. As @Vikinghas pointed out the economic returns have been higher than the accounting returns so that should give you more comfort in the assumption that gains can offset higher than expected cat losses as they come into earnings over time.

-

How do you get to $180-200 per share in earnings?

-

Can you tell us what you are forecasting for FFH over the next 3-5 years and what modelling assumptions are used to get there?

-

Certainly not but they had a serious flaw in their forecast assuming they weren’t just chasing momentum. Is it correct to say that you don’t make forecasts in your process?

-

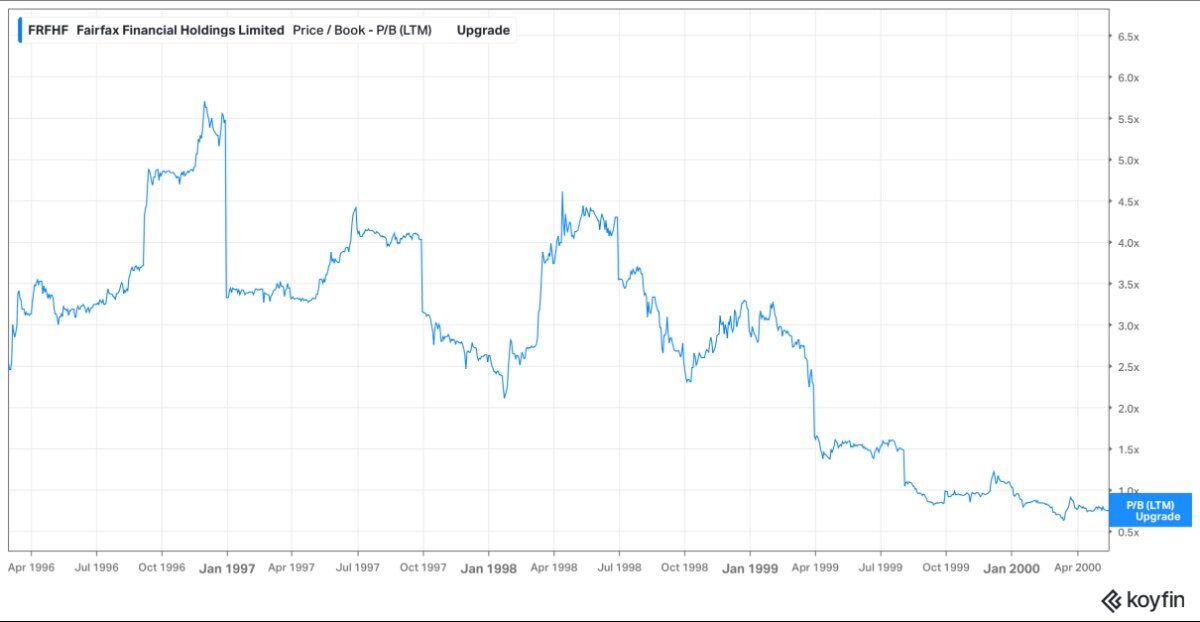

I kid not. Issuing equity well above book value increased equity first. The losses from underwriting then hit the equity. The earnings from the float initially covered it but ultimately the reason they were able to buy float so cheap was because there was a lot of bad policies on the books. When they bought float they got the investments and the future claims.

-

The P/B wasn’t that crazy when the investment:equity leverage was factored in. With 6:1 leverage if the portfolio could earn 7% and the combined ratio was at 100% or better, it made sense to buy. The assumption about the combined ratio was clearly wrong and could have been forecasted to be wrong. What assumptions are the bulls (like me) making now that are clearly wrong?

-

This is really profound. A lot of investors like to invest based on analogs and so they look at charts to get comfort on what might come next even if all of the facts have changed.

-

P/B matters for balance sheet businesses but it should be looked at in conjunction with ROE. Assets that are marked below FV but are earning an appropriate return will increase ROE all else being equal. The relationship between the BV and ROE should be exponential. At a 10% ROE a P/B of 1x makes sense for a 10% required return. At a 20% ROE P/B should be much higher than 2x because the compounding effect over time of the return on incremental capital. For Fairfax, I use BVPS + float, 15x earnings and 2.5x BVPS to triangulate intrinsic value.

-

A multiple between 1.3-1.5 suggests a very high return expectation vs long term equity index expectations of 10%. I think there are a few ways to triangulate intrinsic value and all get me well above 1.5x BV. I also don’t think Fairfax would be buying stock back at fair value. They would want a discount.

-

Great point. The buybacks above book value also reduce equity. Both actions are boosting forward ROE which in theory should boost the forward multiple. The conservative valuation of the equity portfolio and the high reserves also both act to boost current ROE but over time they make their way into earnings.

-

I don’t think the insurance acquisitions were mistakes. They were risk adjusted bets that worked out on an economic basis but didn’t look great on an accounting basis after the initial acquisition. As for the investing side, we should expect them to be wrong a third of the time. We just don’t which ahead of time or the sequence of the mistakes. Otherwise, I fully agree!

-

They had very high ROE in those early years but I think the multiple really exploded because investment to equity leverage increased significantly. They were buying float so cheap and analysts couldn’t fathom how much of that float would get paid out over the years so forward ROE was likely overestimated. Still great deals but not as good as they looked. Now underwriting and investments are contributing to returns. If ROE were based on economic returns, it’s much higher than the accounting returns the last 4 years as Viking”s work highlights and a big part of the reason I have such high confidence in accounting ROE for the next 4 years.