SafetyinNumbers

-

Posts

2,805 -

Joined

-

Last visited

-

Days Won

37

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

I think intrinsic value is between $35-45. I think returns are pretty reasonable from a starting point of $9.50, after the IPO fees. They could be more aggressive with their marks and holders could have paid more fees up to the parent. The move from a premium to book to a discount to book has a lot to do with change in market structure. Management has taken advantage of it by buying back stock and I’m sure they will again when they have more liquidity. It’s not clear IDBI will take a big cash investment from FIH. They may contribute CSB at a premium and be the GP earning fees from LPs that are brought into the deal.

-

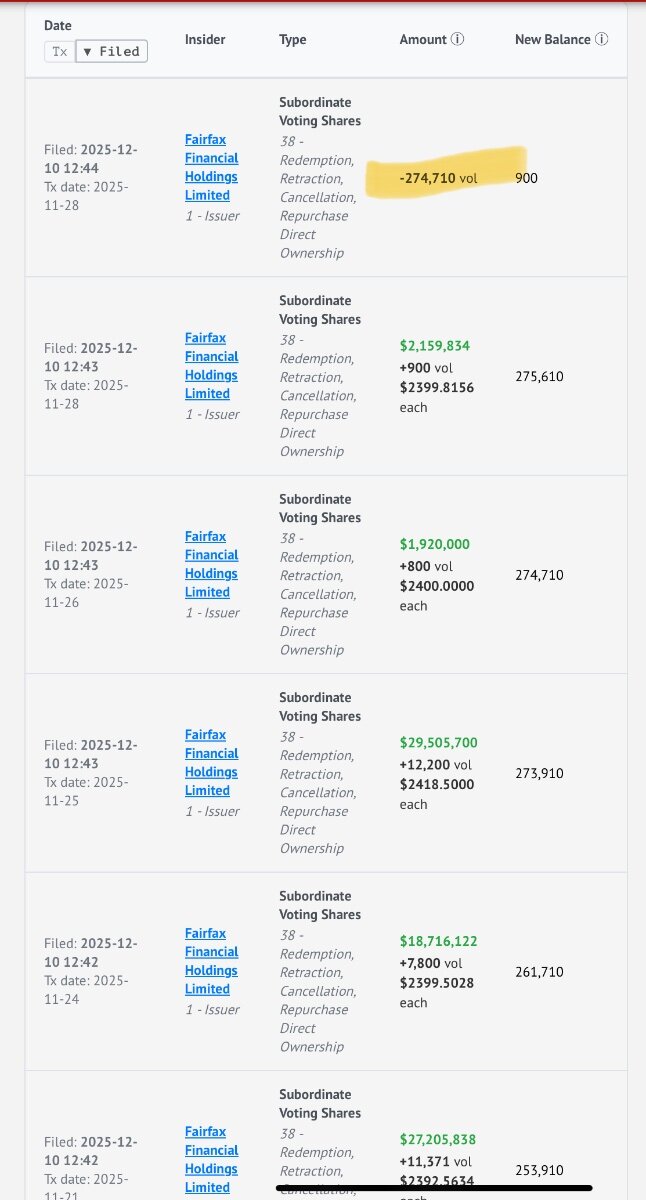

Fairfax canceled 274k shares last month.

-

This is an interesting discussion that I think applies tangentially to Fairfax too. To me it looks like Fairfax ramped technology spend a few years ago as premium growth accelerated. In theory, we should have seen more operating leverage but the expense ratio initially went down and then went back up again on more investment. This investment should have benefits so presumably at some point, the expense ratio will be lower and an improvement in the combined ratio could be more sustainable.

-

Farmers Edge launching a new division, Covian, to go after agtech. https://www.businesswire.com/news/home/20251210543212/en/Farmers-Edge-Announces-Corvian-A-New-Enterprise-Technology-Division-Built-to-Accelerate-Digital-Transformation-Across-Agriculture-and-Sustainable-Supply-Chains?utm_campaign=shareaholic&utm_medium=copy_link&utm_source=bookmark

-

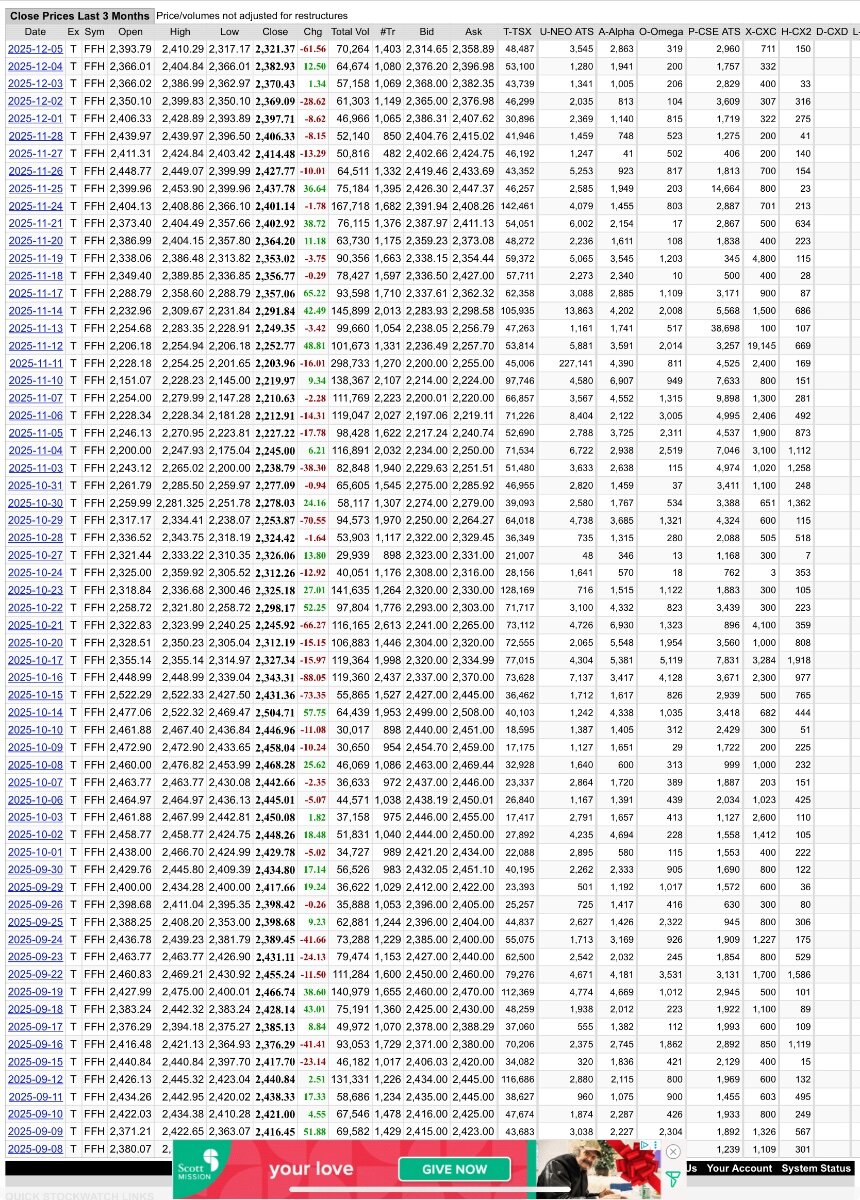

Should use stockwatch.com to see all of the ATS volume as well. TSX is only part of the picture.

-

I don’t understand the assumptions but it’s traded 220k shares so far this week. They will get done but the price depends on where extant shareholders want to sell. Ultimately, they try to hold back enough demand for the last day/hour to ensure the 19th’s close is above their average cost.

-

Brokers are saying 550-800k of demand. The brokers are motivated to get the closing price on Dec 19 above the VWAP for the two-week period so they hold back some buying until the last day.

-

Awesome, thanks!

-

Check out my most recent article for the Globe and Mail about Fairfax. This is a gift article. https://www.theglobeandmail.com/gift/b04eb1bcd666173196423362ad31a8785d529ba1ad1cee14b25891c6ca2ccfbf/AKS47ZLUWZFSXEKQVGUNGOWYCU/

-

Is Fairfax any different?

-

My guess is the banks are fully hedged on the TRS. The buying will start on Monday as the APs begin to accumulate to prepare to cross the shares into the ETFs. The wildcards are how much closet indexers buy and who is left to sell. Fairfax has bought 8m shares plus in the last 8 years if we include the TRS so the most valuation sensitive holders are already out. How do you guys make sell decisions? Is it based on valuation, weight in your portfolio or something else?

-

It’s a bit more liquid than it looks when all of the ATS are included. Maybe 0.35%. This is a real test for how strong the hands are in the retail shareholder base. As has been discussed often, investors like Parsad think the stock is fairly valued or maybe even expensive so they might sell into a big move wanting to avoid the next drawdown.

-

S&P/TSX 60 demand is estimated at 3% of the float and S&P 500 is closer to 10% plus CVNA has a high short interest so a bigger move also makes sense from that perspective. Any guesses on where it closes on Dec 19?

-

Each addition is idiosyncratic based on prepositioning. Expectations weren’t high this quarter for addition and many institutions were rotating out of FFH because of insurance and non-CAD exposure.

-

The analysts are a reflection of their clients.

-

S&P/TSX 60 is committee based. Any pre buying was from index arbs and they have been “burned” 5 quarters in a row so chances are this was the least gamed quarter in the past 6.

-

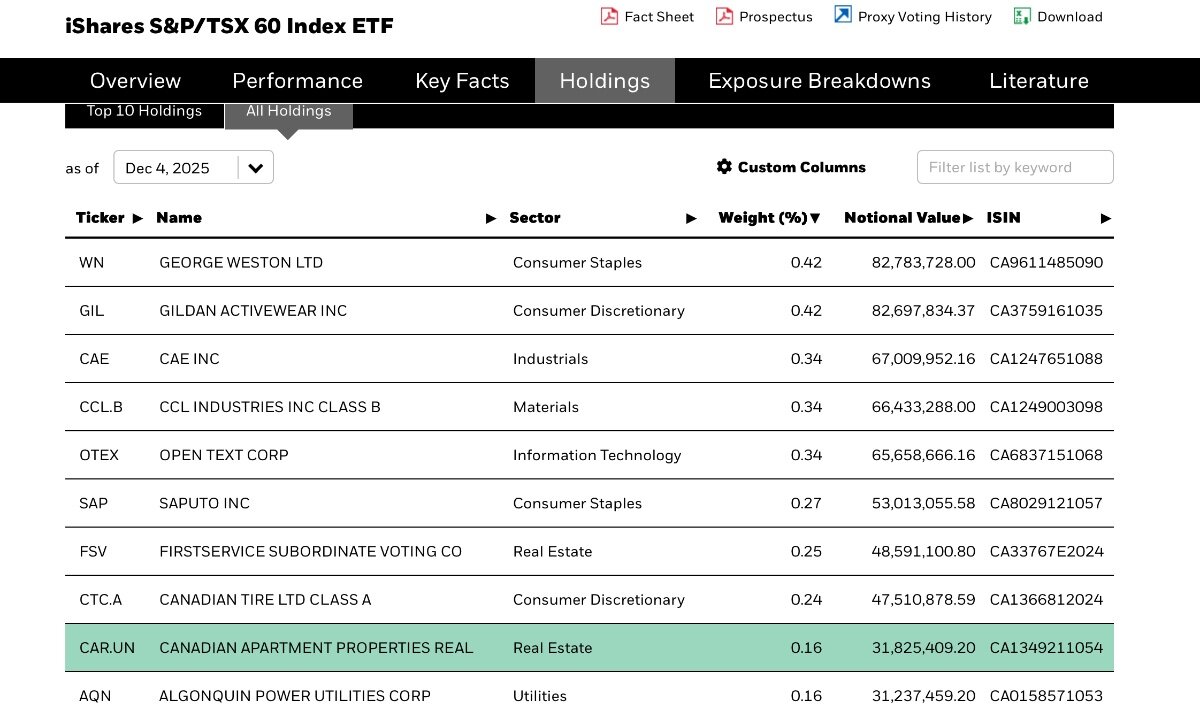

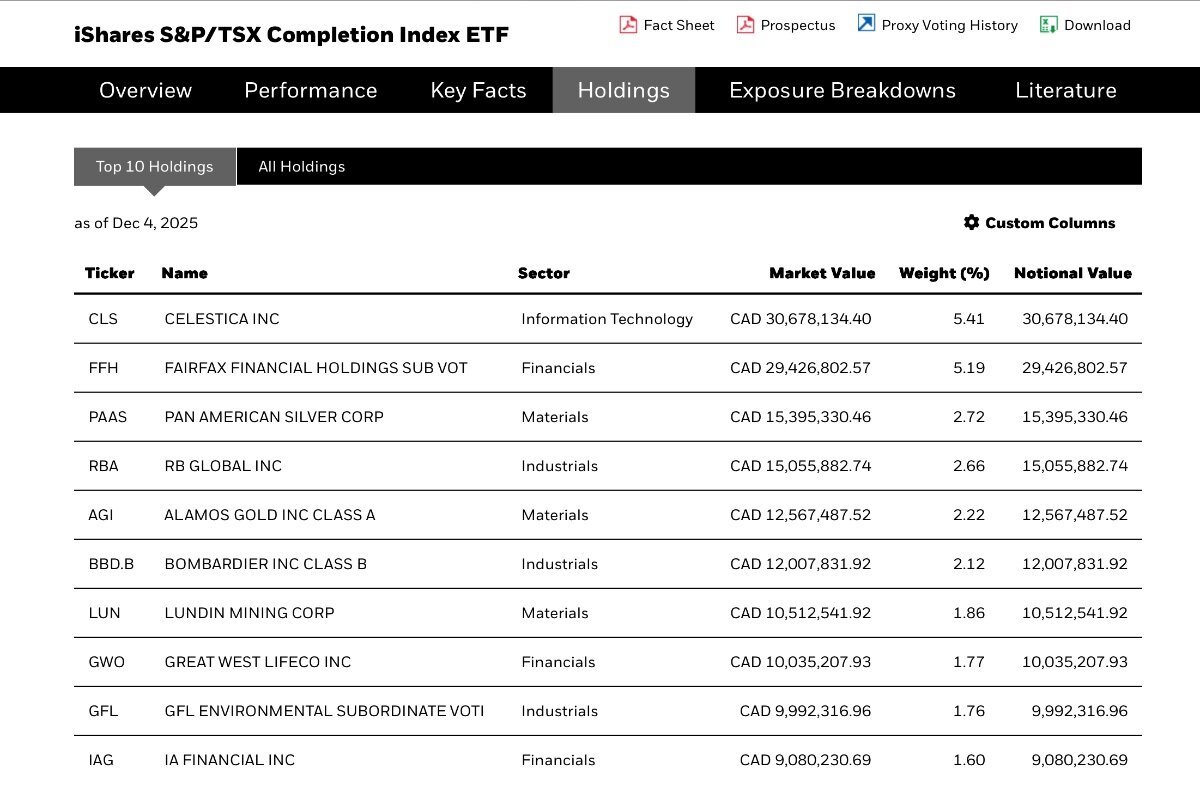

It’s based on the weighting not the performance. Algonquin is the smallest it’s been in 5 quarters by weight. Fairfax was still in the top 2 in the Completion index.

-

It’s important to understand that the investments are held mainly inside the insurance companies. To the extent capital is used by the holdco for buybacks and to redeem preferred, it’s from dividending up from the insurance subsidiaries which have a lot of excess capital and earn more every day.

-

My guess is that this a low risk / high reward set up. If it doesn’t work out it won’t cost too much.

-

I think it’s about 10k shares of buying for the low volatility index.

-

They issued 10 and 30 year CAD debt. Riskier than pref technically as it uses up debt capacity and has a maturity date but practically not really. Arguably lower risk when considering their expectations for long term interest rates given the pref were floating and rates are fixed for the debt up to 30 years.

-

Once there are other deals done sure but value can still be inferred.

-

I’m not sure exactly what you mean. If Anchorage IPOs, they will use that valuation for the rest of the BIAL stake they own. They are also starting to mark up BIAL as the model price now exceeds what they paid Siemens. Generally for privates they use high discount rates and low terminal growth rates which is why valuations are low. It’s a good thing for long term holders as it defers fees but the returns don’t look as good.

-

If anyone buys this workbook, please provide a review here. It ships next week. https://www.amazon.ca/Most-Real-Knowledge-Fairfax-Workbook/dp/B0G2SYVT53/ref=sr_1_3?crid=2I4Q794Z1F3MF&dib=eyJ2IjoiMSJ9.96I3NJ95OtEEi_BeosN3o0KrTamTmjEWm4Xr8oC92RIFdEwrUATHZzqsI4dO1uXgPqDcvEqWx2-B0hXNWFamprcmZ1HRuQoPnkwS6dBXH2Icph9yo_Zmnuoi62DDQ7KmF8g-nV2R3-ckptQ-L0X9sNVwSjoITkQ8T-xj_0oVoy6KvZzAKcCWaAopk1WQwWVJ.-ZWfH-gsOvhEtf0RTr3Dwbu3tfDtOrcMFoGQLpSwms4&dib_tag=se&keywords=the+fairfax+way&qid=1764511462&sprefix=The+Fairfax+way%2Caps%2C101&sr=8-3

-

I agree lower fixed expenses is a good thing but it’s with the same leverage so it’s about maximizing returns not an attempt to reduce risk which is what I thought you were suggesting I’m not sure preferred have much impact on regulatory capital since they are issued at the holding company level and not in the regulated subsidiaries. The preferred probably help debt ratings i.e. lower cost for debt vs having more debt at the time they were issued. The excess capital that you note makes them unnecessary for that reason.