John Hjorth

-

Posts

8,662 -

Joined

-

Last visited

-

Days Won

18

Content Type

Profiles

Forums

Events

Everything posted by John Hjorth

-

HaHa, it reads totally crazy, brainwashed @gfp!

-

Added a bit again today to : MC.PA - LVMH-Moët Hennesy Louis Vuitton SE, & BAIN.PA - Société Anonyme des Bains de Mer et du Cercle des Étrangers à Monaco SA.

-

HAHA! - ! - Great humor on a Monday ..., ehh Tuesday! ... - Just so awesome!

-

James [ @james22 ], I call you, either you provide links to posts about your yearly returns at least for the last 5 years, better more, or I have hereby called your *BS*. You've been around about a half year less than me here on CofB&F.

-

Great topic, thank you for starting it, @schin!, So, we have a really pro book worm among us, @Santayana ! - That's just great! -Do you have links to the above?

-

Added a bit to : MC.PA - LVMH-Moët Hennesy Louis Vuitton SE, CDI.PA - Christian Dior SE and BAIN.PA - Société Anonyme des Bains de Mer et du Cercle des Étrangers à Monaco SA, but some of my orders for BAIN.PA diden't fill today, so hopefully better luck tomorrow with that.

-

This, and worth repeating. His world is just so different from ours.

-

@LC, I still remember you telling about the start of this business venture of yours a few years ago here on CofB&F. If you now walk away from the business venture having earned at least some money, all while your role has been to be a successful catalyst for a back then potential business owner, who now becomes exactly that, and you also leave the business venture with some practical, on-the-rim basic business experience, that nobody can take away from you, that's not shabby at all; -it's actually awesome!

-

-

Started yet another small position today in a tiny Danish bank : DAB.CPH [Danske Andelskassers Bank A/S], trades at P/E 12.1 and P/B 1.1. CofB&F topic. Potential for a good puff in a few years, I think.

-

Reminds me of a scene in 'The Mechanic' [2011], where Arthur Bishops apprentice Steve doesen't follow instructions to use Rohypnol to take out the meat mountain Burke, who has a soft spot for young males, after which things get totally out hand. And after that, Steve visits a bar for a drink, totally beat up. After which a chick adresses Steve in the bar, looks him in the eyes, saying : 'I wish somebody would hurt me like that'. So, I guess, the morale is, that if you're kinky, you'll enjoy your friends hurting you. Not one word from me here about Mr. Arnault in that respect. - - - o 0 o - - - I'm likely going to buy more LVMH next week.

-

lol! at around 13:40 : Compare to the time stamp on this :

-

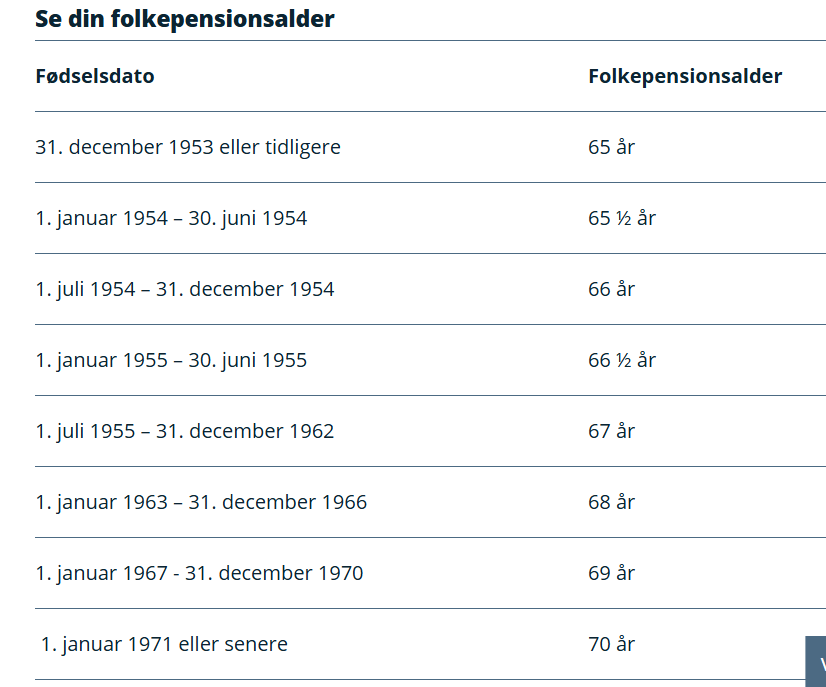

@WFF, It's a gradually increasing retirement age mechnism here in Denmark, that is taken politically up for discussion every fifth year in the Danish parlament, and a further step was added from 69 years to now 70 years in 2030 : 'Folkepensionsalder' -> Retirement age, & 'Fødselsdato' -> Date of birth It's all based on population statistics for the Danish population over time, and concerns for not getting in trouble over time in the future with the state budget running out of control by deficits because of increasing retirement obligations for an aging population, that on average over time gets older and older due to improved living conditions in general. So, political management of a continued balanced social contract between generations.

-

Reuters - Asia-Pacific [May 22th 2025] : North Korean leader Kim Jong Un condemns warship accident as 'criminal'. Little Rocket Man in grief, almost declares national day of mourning. Now somebody is in June going to be euthanized by the use of a howitzer.

-

Please stay stingy while bottom-fishing, @Milu

-

Added a bit more today in the morning hours to MC.PA at EUR ~483. Should likely have been more stingy with the orders.

-

Greg [ @Gregmal ], No doubt this a good, really good idea by POTUS and / or his administration. Here in Denmark, we have had such similar things for several decades now.

-

Marco [ @Marco Van Basten ], Do you see, 'Wednesday' in my post above yours? It's a clickable link! -Please just click on it!

-

Huh? - Isen't Dinar a live and kicking account? [but it seems @-ing him suddenly doesen't work?] - He visited CofB&F as late as Wednesday.

-

Thank you very much, @KJP, It's much appreciated. Yeah, the art here is 'not to drown' in technical stuff and all kinds of details. . Also, I'll try to take a look at the PwC US website tomorrow.

-

Marco [ @Marco Van Basten ], A basket of trophy assets, that I think likely never really will go out of favor, to own for the long term. [When I'm personally motivated for it, I may perhaps and eventually open and start a separate topic about it in the Investment Ideas forum]. - - - o 0 o - - - Thank you for asking.

-

Bottom-fished a bit more JOE during the day at a bit above USD 43. - - - o 0 o - - - Also got filled today on the first few shares ever in BAIN.PA [Bain de Mer Monaco, on the company website called Monte Carlo Societé des Bains de Mer, full formal company name : In French : ''Société Anonyme des Bains de Mer et du Cercle des Étrangers à Monaco', translates to English by : 'Anonymous Society of Sea Baths and the Circle of Foreigners in Monaco', -no secret why no one wants to own it [ ]] at EUR ~102 as a starter position.

-

Isen't there a a non-secondary 'executive summary' like elaboration on a government or administration webpage somewhere? I personally consider both WSJ and NYT secondary and biased as well on exactly this stuff, although and while I visit them both every morning.

-

Blake [ @Blake Hampton ] and other US CofB&F members, Where to read about the factual content of this proposal and the expected consequences of it? Thank you in advance.

-

Added a bit to MC.PA [LVMH - Moët Hennesy Louis Vuitton SE] today, at EUR ~485. - - - o 0 o - - - Edit : Also got filled today on the first few shares ever in CDI.PA [Christian Dior SE] at EUR ~453 as a starter position.