UK

-

Posts

3,440 -

Joined

-

Days Won

16

Content Type

Profiles

Forums

Events

Everything posted by UK

-

Thank you! Yes, however this item will develope in the future, I doubt it could become 'thesis killer'. Underwriting, bond portfolio management and other/general execution continues to be excelent. I think this question 'Is Fairfax moving up the quality chain (of insurers) when it comes to underwriting' is much more important for the whole story. And the answer: it looks like so!

-

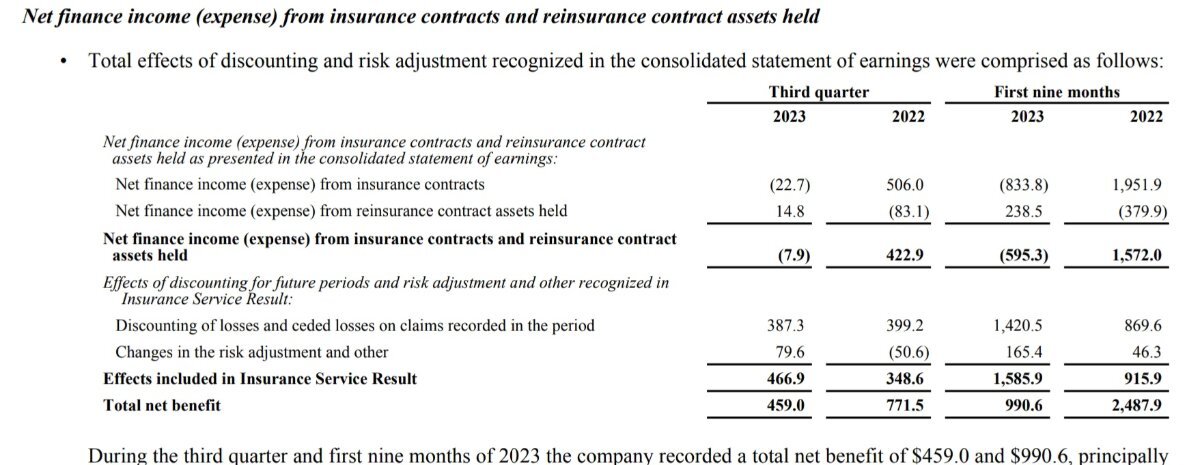

Yes, it is second thing I am not sure how awesome it is:). Seems this makes up some 31 per cent of total pretax earnings in Q3 (24 percent in 9M). Excluding this, EPS would be ~30 USD, much closer to analyst estimates for the quarter. Not sure how to think about this item, making up almost 1/3 of the earnings, but dynamics of which nobody seems fully understand:) Not sure how to estimate net insurance liabilities change in the Q3, but I suspect (or am afraid), this thing is much more change in discount (interest) rate, than change in reserves, driven. Somebody should just ask on the earnings call plain and simple, if this damned thing will reverse as quickly as it grew, if interest rates will go substantially lower in the future.

-

https://www.bloomberg.com/news/articles/2023-11-02/early-bets-on-nintendo-nidec-yield-big-gains-for-kyoto-bank?srnd=premium As a result of these early bets, the bank is now sitting on vast paper gains. As of March, the bank held shares in 137 companies worth about 920 billion yen ($6 billion). The stakes were originally worth about 150 billion yen, according to the company. The portfolio exceeds the bank’s market value of about 660 billion yen.

-

They also did bought a lot of shares and swaps when they where much cheaper. Also maybe they could delever more before buying shares aggressively?

-

No I didn't noticed. Why would they exclude this? On premiums growth, I think we should just wait for them to comment on it in tomorrow. Maybe not necessarily a big deal.

-

I wrote to him (cc morningstar) a while ago. Not sure he/they care. Not sure we should care about them either:)))

-

So highest EPS estimate was 26 USD vs actual 42 USD? Premiums growth is maybe the only thing which is not awesome?

-

Verdict?

-

https://www.economist.com/europe/2023/11/01/ukraines-top-general-on-the-breakthrough-he-needs-to-beat-russia The course of the counter-offensive has undermined Western hopes that Ukraine could use it to demonstrate that the war is unwinnable, forcing Russia’s president, Vladimir Putin, to negotiate. It has also undercut General Zaluzhny’s assumption that he could stop Russia by bleeding its troops. “That was my mistake. Russia has lost at least 150,000 dead. In any other country such casualties would have stopped the war.” But not in Russia, where life is cheap and where Mr Putin’s reference points are the first and second world wars, in which Russia lost tens of millions. ... “First I thought there was something wrong with our commanders, so I changed some of them. Then I thought maybe our soldiers are not fit for purpose, so I moved soldiers in some brigades,” says General Zaluzhny. When those changes failed to make a difference, the general told his staff to dig out a book he once saw as a student. Its title was “Breaching Fortified Defence Lines”. It was published in 1941 by a Soviet major-general, P.S. Smirnov, who analysed the battles of the first world war. “And before I got even halfway through it, I realised that is exactly where we are because just like then, the level of our technological development today has put both us and our enemies in a stupor.” ... Mr Putin is counting on a collapse in Ukrainian morale and Western support. There is no question in General Zaluzhny’s mind that a long war favours Russia, which has a population three times and an economy ten times the size of Ukraine. “Let’s be honest, it’s a feudal state where the cheapest resource is human life. And for us…the most expensive thing we have is our people,” he says. For now he has enough soldiers. But the longer the war goes on, the harder it will be to sustain. “We need to look for this solution, we need to find this gunpowder, quickly master it and use it for a speedy victory. Because sooner or later we are going to find that we simply don’t have enough people to fight.”

-

I think deficit is important, especially for the general economy. But in terms of functioning treasury market, it's hell/panics, as was the last time in 2020, QE perhaps is also or even more important? Also I am not sure QE is not working in setting rates in the longer term in Japan and they would be anywhere close were they are today in term of debt and rates without yield control via massive QE? Also, when bond market started to break in UK last year, because of too big/unsustainable budget, the central bank was forced to postpone QT and even made some QE very quicky. However, what I am more sure about, is I do not understand all these things at all:))

-

Interesting! Thanks for sharing.

-

Interesting interview, but, as always, perhaps not very actionable, at least for me. But I liked his position on USD (after being wrong several times recently) this time: would love to hate it, until I look at every alternative available:))

-

The Party explained that it was targeting inequality, monopoly, and excessive financial risks, but some of the arrests seemed personal. Ren Zhiqiang, a real-estate tycoon, received an unusually harsh sentence of eighteen years on corruption charges, after someone leaked an essay in which he mocked Xi as a “clown stripped naked who still insisted on being emperor.” None of the targets showed any organized political intentions. The only visible pattern is that Xi and his loyalists appeared intent on snuffing out rival sources of authority. One after another, he got rid of anyone with power, the entrepreneur said: “If you have influence, you have power. If you have capital, you have power.” Xi is said to have spoken bitterly of watching Boris Yeltsin contend with Russian tycoons in the nineteen-nineties. Joerg Wuttke told me, “When Putin entered the Kremlin in 2000, he assembled the oligarchs and said, basically, You can keep your money, but if you go into politics you’re done.” He went on, “In China, the big names should have learned from that meeting, because in this sense Putin and Xi Jinping are soul mates.” ... Local governments, short of cash, have adopted a subtle extortion method that lawyers call “taxation by investigation.” A factory owner in Shanghai told me that Party officials used bank records to identify residents with liquid assets of at least thirty million yuan—about four million dollars—and then offered them a choice: hand over twenty per cent or “risk a full tax audit.” Recently, the Party has signalled that the purge of the private sector is over, but many have grown wary. A former telecom executive cited an ancient expression—“shi, nong, gong, shang”—which describes a hierarchy of social classes: scholar-officials, farmers, craftsmen, and merchants. “For two thousand years, the merchants were the lowest,” he said. “What Xi is doing is just a reversion to the imperial Chinese mean.” The big winners, in the current era, are officials with deep personal ties to Xi; he has stocked the Politburo with trusted aides, and has cultivated the military by boosting investment and replacing top leaders with loyalists. ... In the Xi era, that principle has become, in effect: It doesn’t matter if the cat catches mice, as long as it’s red.

-

https://time.com/6329188/ukraine-volodymyr-zelensky-interview/ Amid all the pressure to root out corruption, I assumed, perhaps naively, that officials in Ukraine would think twice before taking a bribe or pocketing state funds. But when I made this point to a top presidential adviser in early October, he asked me to turn off my audio recorder so he could speak more freely. “Simon, you’re mistaken,” he says. “People are stealing like there’s no tomorrow.”

-

-

This was the line I wanted to doublecheck:) Also: "Well, I've never liked Jum Malone's extreme manipulations. I don't wanna be known as the great manipulator like Jum Malone is. He paid less income taxes than anybody. He just pushed everything to the dry extreme." Somebody should ask Charlie what he thinks about Brookfield, since it is in a competition with Berkshire and Fairfax in other thread of this forum.

-

https://www.bloomberg.com/news/articles/2023-10-31/uaw-strike-ups-drivers-writers-union-mark-record-wins-for-us-labor-movement?srnd=premium-europe&leadSource=uverify wall Workers in the US are getting record-breaking wage hikes this year thanks to strategic strikes and stunning contract wins. The result is a boost in middle-income wages and a shift in the balance of power between companies and their employees. Even before the United Auto Workers reached historic contract deals with carmakers, unions across the country had already won their members 6.6% raises on average in 2023 — the biggest bump in more than three decades, according to an analysis by Bloomberg Law.

-

I guess probability of all living hell in treasury market is still very low, but as soon as something happens (not necessarily something as serious as all living hell) I would expect abrupt end of QT and maybe start of QE4?

-

Thank you very much! I listened to it, very good interview with some really interesting tidbits, just wanted to check some places on transcript to be sure I understand them correctly:)

-

Does anybody know if there is transcript of this interview available? Tried to search and did not find find any, yet this is whar google shows on it's search page:

-

-

Thanks!

-

True:), but it is also good to know that the general market thinking is:)

-

https://www.wsj.com/world/europe/wars-push-up-demand-for-weapons-sparking-fears-of-shortages-57d664ad?mod=hp_lista_pos1 With demand increasing faster than production, prices of some supplies have soared. NATO-standard 155-millimeter artillery shells, one of the West’s most basic armaments, had cost governments about $2,100 apiece before Russia’s invasion of Ukraine last year, said Dutch Admiral Rob Bauer, Stoltenberg’s top military adviser, at the NATO forum. The price of those shells, which Bauer dubbed “one of the most coveted objects in the world right now,” has increased fourfold, to about $8,400, he said. ... General Dynamics said it has been able to boost production of artillery shells and other munitions faster than expected, boosted by Pentagon investment in new facilities. The company is targeting annual production of one million shells, a fivefold increase. Sales at its combat unit, which employs more than 2,000 staff in Europe, had been expected to be flat at best this year. They are up 15% so far this year, stoked by orders for shells, as well as for armored vehicles and military bridges. “Frankly, we don’t see that demand signal slowing down,” Aiken said.

-

https://www.bloomberg.com/news/articles/2023-10-27/bank-stocks-sink-past-svb-crisis-lows-as-rates-upend-business

https://www.bloomberg.com/news/articles/2023-10-27/bank-stocks-sink-past-svb-crisis-lows-as-rates-upend-business