All Activity

- Past hour

-

Bond losses would be offset by the liability adjustment on the insurance if they ran equal duration. The bonds have typically been shy of duration of the insurance, so should actually be a sight net positive

-

Almost like when you ignore the shitty politicans and chronically online trolls, the US is a welcoming, friendly, accepting place for all people. At least much more so than many countries out there....

-

Basically the Berkshire problem, no? I know there are better ways to value it, but I have high confidence that when Berkshire trades at 1.3-1.4x book, it is trading below intrinsic value. Likewise, I have high confidence Fairfax trades at a discount when it trades at 1-1.2x book. And I think intrinisic value is growing quickly. Don't need to be exact to know when you got a deal. I also like the idea of valuing float. Smarter people than I can do SOTP for a better valuation..

-

What I found hilarious, is that for all the whining we ve heard about how horrible the US is and how hostile we are to foreigners….millions of them just had the time of their lives traveling here for the World Cup and seeing many different pieces of America. Somehow another dumb fuck liberal narrative gets exposed as a lie, go figure!

-

@73 Reds, great question: "Why use BV as a valuation metric?" The primary reason for me is habit - it is built into my models/mental framework. Another important reason is it also the key metric that the investment community focusses on for P/C insurers (rightly or wrongly). I do include "excess of FV over CV" in my models - that provides an important improvement to accounting BV - getting us closer to "economic BV." But that is incomplete. Is book value still relevant as a valuation measure for Fairfax? Great question. I need to think more about it. What do others think? PS: When I value Fairfax I like to use "normalized earnings" and PE. Much of their EPS is very stable. And for investment gains I use a three year average - which makes this part also very stable. As a result, PE works for me. Bottom line... stock is trading today at about 8 x "normalized earnings." Crazy cheap from my perspective.

-

@Viking I love your work but have a lingering question for you and others: Since most acknowledge the benefit of share buybacks even above BV which also go to reduce BV, why does everyone seem to focus on BV as a valuation metric? Can't we find a better valuation metric that doesn't overtly reduce the estimated value that we are trying to measure? Is it just because BV is so easy to measure or is there another reason why every time someone seeks to value Fairfax, book value is always considered?

-

Falkland War 2.0 My money is on General Belgrano going down … again

-

How do you gauge this?

-

It has been mentioned by the Indian press which is why I brought it up. It doesn’t make as much sense as IIFL Capital but we’ll see.

-

Buffett/Berkshire - general news

Spekulatius replied to fareastwarriors's topic in Berkshire Hathaway

I can’t help it:

-

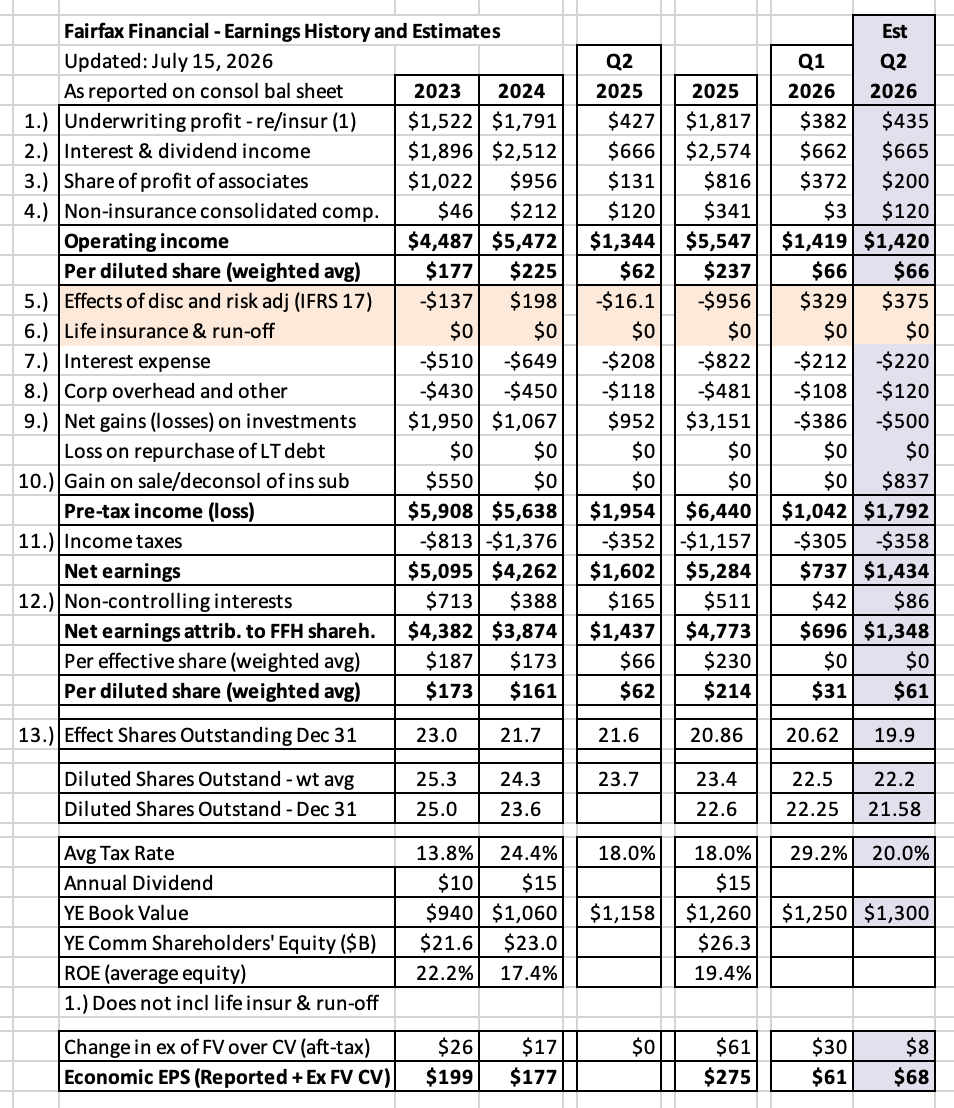

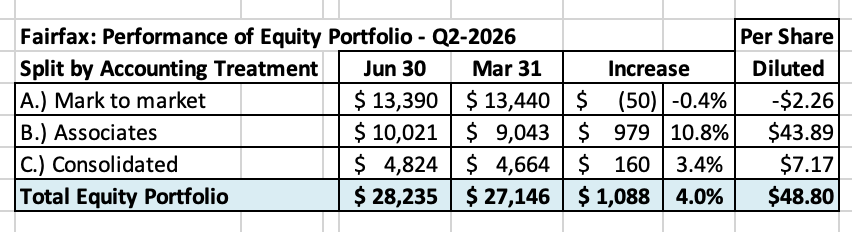

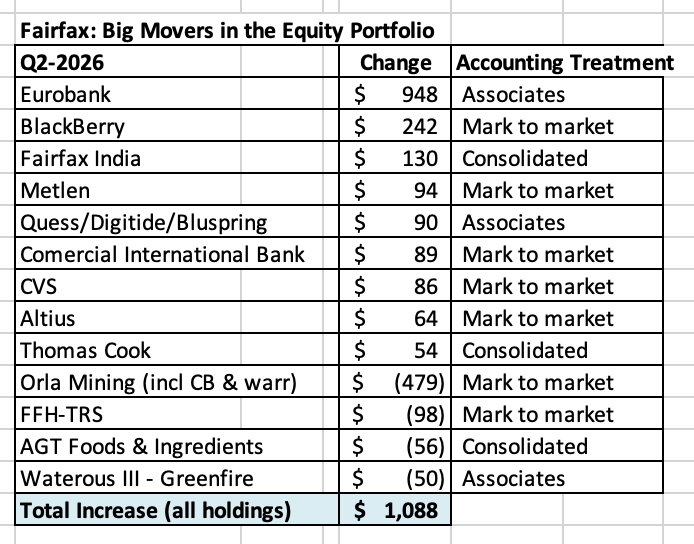

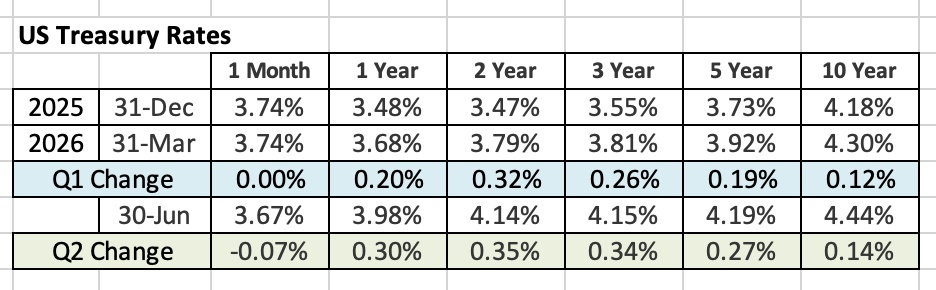

Fairfax Q2 2026 Earnings Preview My very rough guess is earnings will come in around $60/share when Fairfax reports Q2 results. Analyst consensus is about $80/share. I look forward to getting feedback from board members. This would put book value at June 30, 2026, at about $1,300/share. BVPS at March 31, 2026: $1,250 Earnings: +$60 Impact of buying back shares above BV: -$12 per share Accounting results for Fairfax are an incomplete measure of value creation. If we include excess of FV over CV for market traded non-insurance associate and consolidated holdings, '"economic earnings" increases to $68/share. 6-Month "economic earnings" are $129 per share. Outstanding. Note, I am not doing this exercise to come up with a high conviction specific number (I know it will be wrong) for EPS or BVPS. Rather, I do it for the build of the individual items - to help prepare me for Fairfax’s earnings release. Below is the logic I used to come up with my forecast. ————— Details Underwriting profit: Q2 2025 Net premiums written: $7.17B CR: 93.3% Underwriting profit: $426.9M Net favourable prior year reserve development: $163.2M Catastrophe losses: $140.1M Q2 2026 Estimate: similar to Q2 2025 Net premiums written: modest growth (low single digit) CR: 93.5% Underwriting profit: $435M ————— Interest income: Q4 2025: $646M Q1 2026: $662M At March 31, 2026: Duration: 2.2 years Average maturity: 3 years Yield: approximately 5%. Q2 2026 Estimate: similar to Q1 2026 $665M ————— Share of profit of associates Waterous Energy III (Greenfire). Q1: $117 million tailwind Q2: $50 million headwind (loss)? Poseidon sale closed May 29. Normal contribution: $75 million per quarter Adjusted for sale: $62 million ($13 million reduction) Sanmar??? (Sale in March) Q1 2026: $372M Q2 2026 Estimate $200M ————— Non-insurance consolidated companies Q2 2025: $120M Q1 2026: $3M (seasonality, AGT IPO costs) My annual estimate is $450M. Q2 2026 Estimate $120M —————— Investment gains (losses) Equities From an accounting perspective, it is only the market to market equity holdings that impact this bucket each quarter. Q2 2026 Estimate for equities loss of $50M Fairfax has been slowly selling down their position in BlackBerry over the past year. BlackBerry was one of the big gainers in the quarter. If Fairfax continued to sell BlackBerry shares in the quarter the gain may be much smaller than $242 million. As a result, the loss estimate for equities of $50 million would be larger. Big movers: Fixed Income Interest rates were higher in Q1. Impact on fixed income? Q1 2026: loss of $364 million Fixed income portfolio at end of Q1: Size: $49.8B Duration: 2.2 years Average maturity: 3 years Yield: approximately 5% “zero traditional private credit exposure” Interest rates continued their move higher in Q2. Q2 2026 Estimate for fixed income: Larger than loss in Q1 loss of $450 million Large one time investment gain Poseidon: $837 million I like to separate this number out in my model. Total investment gains (losses) Q2 2026 Estimate: Equities: -$50M Fixed income: -$450M Poseidon: $837M Total: $337M There are couple of other items that impact investment gains each quarter: Digit Insurance Fairfax India - change in value of the individual holdings Digits share price was flat on the quarter, so no impact of Fairfax. I do not track the holdings in Fairfax India from quarter to quarter, so not sure of the impact here to Fairfax. —————— IRFS 17 and Life Insurance and Runoff This is a catchall bucket for our model. IFRS 17 - Interest rate impact Rising interest rates are a tailwind for IFRS 17. This offsets some of the loss in the fixed income portfolio. Q1 2026: Gain of $180M (about half the loss in fixed income) Q2 2026 Estimate Gain of $225M Total IFRS + Life/Runoff Q1 2026: $329M Q2 2026 Estimate for this bucket $375M This number is low conviction. —————- Interest expense Q1 2026: $212M Q2 2026 estimate: $220M Corporate expense and other Q1 2026: $108M Q2 2026 estimate: $120M Tax rate Q1 2026: 29% Q2 2026 estimate: 20% Q1 was elevated. Not sure why. Q2: Significant gain ($837 million) from sale of Poseidon is likely taxed at lower capital gains rate. Minority interest Estimate is 6%? —————- Share count Shares outstanding Q1 2026; Effective: 20.62M Diluted: $22.25 It appears Fairfax was very aggressive buying back stock in Q2: 675,000? Total: $1.08 billion? Per share: $1,600 Estimate of shares outstanding at June 30, 2026: Effective: 19.95M Diluted: 21.58M —————— Impact on BVPS of share buybacks above book value Shares were purchased above book value: BVPS: $1,250 Difference: $350 per share or $236.25 million Reduction in BVPS due to buybacks above book value: $236.25 million / 19.95 million effective shares = $12/share —————- Excess of FV over CV for associate and non-insurance consolidated holdings March 31, 2026: $3.9B June 30, 2026 Estimate: $4.1B, or $206/share pre-tax or $175/share after-tax (15% tax rate) Quarter over quarter change: $200 million, or $8 per share after-tax Headwind: Sale of 50% of Poseidon was a reduction of $837M. Tailwind: Driven by Eurobank, remaining holdings had a strong Q2. Net result in the quarter: an estimated increase of $200M to $4.1B. Economic EPS estimate: $61 + $8 = $69 Economic BVPS Estimate: $1,300 + $175 = $1,475/share Fairfax share price (July 10): $1,660 P/BV: 1.13x

- Today

-

Agreed, that kind of behavior made me quit football and switch to Futsal.

-

I think we Buffett nerds need the full interview: https://www.cnbc.com/video/2026/07/15/watch-cnbcs-full-interview-with-berkshire-hathaway-chairman-warren-buffett.html or excerpts as a transcript: https://www.cnbc.com/2026/07/15/cnbc-exclusive-excerpts-berkshire-hathaway-chairman-warren-buffett-speaks-with-cnbcs-becky-quick-on-cnbcs-squawk-box-today.html Cheers!

-

You forgot the punchline SD. After terrible bombing campaigns, the Nazis and Japan lost the war. Trump has given the IRGC every opportunity to submit. Like Japan and Hitler - they refuse to.. The battle for control of the SOH is now on. That's pretty much all that matters now.

-

Great post @rajpgokul, highly appreciated insights! many thanks

-

Quite agree .... as it's not collectable Thing is .... every time a balloon is floated, it's a few more days of diminished traffic through the SOH before it is resolved, and a further draw on global SPR inventory. Jawbone all you want, but you fight against a price rise as that inventory depletes ... and have to fight harder the less inventory you have left. Knocking out the bridges and power stations, just means the Iranians knocking out the same in US friendly states, not Iran magically coming to the table. It just evidences a trapped, drowning man, punching at every/anything, desperately searching for a way out of the tarpit. Let the man tire, and drown. One of the WWII takeaways was that bombing civilian infrastructure to diminish ability to produce more war material, just made the population more resistant ... even when their leadership were Nazi. Arguably, the same thing happening here. SD

-

Right. Getting rid of the capital gains tax altogether would be a fine solution.

-

Great post, thanks for sharing. And now I'm curious what clears your local hurdle rate...

-

My god, Buffett looks so older

-

The man loves to float trial balloons, as many politicians do. He got his immediate feedback and changed course/strategy. Some would say that this is "pragmatic" behavior.

-

I did not realize that getting to the truth is now by majority rule. Indeed at one time, the earth was deemed flat and heretics were executed. Rather than put up a coherent argument to me - I suggest you write your detailed thesis and send it off to the Federal Reserve telling them why they are wholly incorrect and that their data is incorrect.

-

The 20% toll is not "real"... ...it is just his style to negotiate and make people talk about himself...probably in his mind it is smart anchoring to a bad outcome to more easily achieve a "middle" ground (that is not middle but in his favor)...some people do it in negotiations...

-

I actually agree, it is getting ridiculous. They need to get stricter about all the acting, and about tactical fouls. Players don't give a shit about yellow cards. There should be more time penalties, that put your team at a serious disadvantage, being down to 10 or even 9 players. A tactical foul preventing the opponent from launching a quick counterattack should lead to a 15-minute penalty. Acting seriously hurt, slowing down the game for more than a few seconds, should automatically put the player on the sidelines for 5 minutes, so he can recover from his pain.

-

Buffett/Berkshire - general news

John Hjorth replied to fareastwarriors's topic in Berkshire Hathaway

@Milu, you're such a troublemaker! , It's sacrilege to post something like that here! [j/k naturally!] -

These rules are a huge incentive to build new rental housing (or rehab housing that will otherwise eventually get torn down), and they also encourage more inventory of existing housing stock available for sale. For 1031, if an individual investor can't 1031 they're just going to hold the house until death when the basis steps up. For an institutional investor, they're going to hold the property until they can sell it for 25% higher to meet the same IRR after tax. For bonus depreciation, an investor will need to rent a house for much more in order to meet their IRR hurdle. Maybe there's a better system without 1031/bonus depreciation, but if you just end those two provisions in the tax code the housing crisis will be exacerbated if anything.