All Activity

- Past hour

-

Would everyone (including Parsad) be happy with an LLM scraping all the contributions/copyright from here, training on it, and potentially commercialising it in future? If it was an internal LLM just for the site that couldn't escape the garden, then much more interested.

-

I sleped on that one. After Keiko Fujimori won it was obvious .. But I stoped following. Aprox 13$ for what I understand and has to close before september. Quite good arbitrage.

I sleped on that one. After Keiko Fujimori won it was obvious .. But I stoped following. Aprox 13$ for what I understand and has to close before september. Quite good arbitrage. -

Not seeing a lot of matches here as the time difference makes it difficult. Watched my country play against Egypt though, we sucked balls. Coach needs to get his act together or we won't last long.

-

Here is an introduction to the chapter... Chapter 14: The Evolution of Fairfax's Investments Introduction Learning about a company's history can be a valuable exercise for investors. It provides context, helps explain management decisions, reveals how corporate cultures are shaped, and highlights lessons learned along the way. One of the defining characteristics of Fairfax over the past forty years has been its willingness to learn and adapt. The company has enjoyed remarkable successes. It has also made significant mistakes. What is most striking is not that both occurred—it is how Fairfax responded. Fairfax has one of the more colourful histories in modern investing. That history can be both a blessing and a curse. It offers important lessons, but it can also obscure the company that exists today. This chapter attempts to bridge that gap. The first article examines Fairfax's highly successful credit default swap strategy from 2005 to 2009—its version of The Big Short. The second reviews the costly equity hedge and short positions that followed, a decade-long mistake that weighed heavily on shareholder returns. The third analyzes Fairfax's equity investments from 2014 to 2017, a period marked by too many chronically leaking boats. The final article explores the emergence of New Fairfax beginning around 2018, as the company shifted toward higher-quality businesses, stronger management teams, and a more powerful compounding model. Together, these articles tell a story: Success → Mistake → Learning → Transformation More importantly, they explain how Fairfax became the company it is today. History is not the investment thesis. What matters most is where a company stands today—its management team, business fundamentals, capital allocation and future prospects. But understanding how Fairfax evolved provides important context for evaluating the business it has become and where it may be headed. In many ways, the transformation of Fairfax over the past decade is one of the most important parts of the Fairfax investment story.

-

New Fairfax: Moving Up the Quality Ladder (2018–Present) Here is the final article (#4) in my short history on some of Fairfax's investments. "Time is the friend of the wonderful company." — Warren Buffett Something changed at Fairfax around 2018. Trying to identify an exact date is a fool's errand. The transformation was gradual and remains ongoing today. But looking back, it is clear that Fairfax began refining its investment approach and upgrading the quality of the businesses it owned. The company did not abandon value investing. It evolved. What Changed? Three themes increasingly shaped Fairfax's investment decisions: Strong management teams. Strong balance sheets. Profitable businesses. Rather than trying to fix troubled companies, Fairfax increasingly partnered with capable operators who could create value on their own. The goal was no longer simply to buy cheap assets. The goal was to buy better businesses. This shift can be seen in many of Fairfax's major investments since 2018, including Stelco, Seaspan, Bangalore International Airport, Metlen and Orla Mining. At the same time, Fairfax began addressing mistakes from the previous decade. Underperforming investments were sold, restructured, recapitalized or merged with stronger partners. Capital was increasingly recycled from weaker opportunities into stronger ones. The quality of the portfolio steadily improved. Repairing the Past, Building the Future The benefits did not appear overnight. For several years, Fairfax was doing two jobs simultaneously. First, it was repairing the past. Weak investments needed to be sold, restructured or repositioned. These actions often produced short-term losses and disappointing reported results. Second, it was building the future. Successful investments rarely create immediate value. Management must execute. Earnings must grow. Intrinsic value must compound. In many cases, the largest gains emerge years after the original investment is made. As a result, the costs of repairing the portfolio partially obscured the value being created by newer investments. Today, that dynamic has largely reversed. Many of the major portfolio repairs have been completed. At the same time, a number of investments made since 2018 have matured and become meaningful contributors to value creation. Early Results The results can be seen across both new investments and legacy holdings. Stelco Fairfax invested approximately $193 million in Stelco in 2018. When the investment was sold in 2024, total value creation was approximately $544 million, including dividends, share-price appreciation and the value of shares received from Cleveland-Cliffs. The compound annual return was approximately 25%. Seaspan / Atlas / Poseidon Seaspan has become one of Fairfax's most successful investments. In 2026, Fairfax sold approximately half of its position in Poseidon at a substantial premium to carrying value, generating proceeds of roughly $1.9 billion and a pre-tax gain of $837 million. Even after the sale, Fairfax continues to own a significant interest in the business. The Hidden Gems Not all of Fairfax's success came from new investments. The company already owned several hidden gems within its portfolio. In some cases, Fairfax increased its ownership, strengthened the business and simply gave management time to execute. The best example is Eurobank. At the end of 2020, Fairfax's stake had a market value of approximately $900 million. By mid-2026, the investment had created roughly $6 billion of value through share-price appreciation, dividends and shares sold. The compound annual return has been 45%. This is an important distinction. Fairfax did not simply build a better portfolio. It also unlocked value from businesses it already owned. A More Powerful Business Model There is another important development that receives less attention. Fairfax has always centralized capital allocation while decentralizing operations. Since 2018, the company appears to have renewed its focus on improving the performance of the businesses it owns. The objective is not to run subsidiaries from head office. It is to partner with capable management teams, strengthen operations and increase earnings and cash generation. This creates a powerful feedback loop. Better businesses generate more cash. Fairfax can then redeploy that capital into the most attractive opportunities across the organization. Those investments generate additional earnings and cash flow, which can then be reinvested again. The company's earlier investments often consumed capital. Increasingly, its newer investments generate capital. That is a profound difference. In many respects, Fairfax today resembles a younger Berkshire Hathaway. Operations are decentralized. Capital allocation is centralized. Cash generated by one business can be redeployed into opportunities offering the highest returns elsewhere in the organization. The result is a stronger and more durable compounding engine. Why It Matters Understanding this history provides important context for evaluating Fairfax today. For much of the past decade, management's attention was divided between repairing weaker investments and building a stronger portfolio. Today, many of those legacy issues have been addressed. At the same time, the collection of businesses assembled and strengthened since 2018 is beginning to demonstrate its earning power through higher dividends, stronger operating results, increased earnings from associates and investment gains. Fairfax spent much of the past seven years moving up the quality ladder. What has emerged is a stronger collection of businesses, a more disciplined investment approach and a more powerful capital allocation engine. The portfolio repair phase is largely behind it. The compounding phase is increasingly in front of it.

-

Read the 14-point draft agreement between the US and Iran - https://www.cnn.com/2026/06/17/middleeast/us-iran-war-mou-text-intl The simple question remains for those ascribed to the Fox News/Iran totally defeated and on its knees narrative.......if thats the case why did the United States just give away all its leverage here and kick every single major nuclear issues down the road here (& if you think Phase 2 is going to wrap up in 60 days I've got a nuclear bomb in my basement to sell you!)?

-

@Marco Van BastenIt looks like Holcim announced their intent to make a tender offer for CPAC. Any idea what price they will offer?

@Marco Van BastenIt looks like Holcim announced their intent to make a tender offer for CPAC. Any idea what price they will offer? -

If the business is overcapitalized between inventory and real estate, it would not be a one time lift. It would be structural. Again, holdco decisions are not generally related to equity investments unless they are in insurance companies which include the minority interests and buybacks.

-

I don’t think they are borrowing to make this investment. The borrowing happens at the holdco. I assume Peller will end up in the insurance subsidiaries. I think the borrowing is to replace the class K preferred in March.

- Today

-

Not "many people", just the Trumpers.

-

I spent nearly my entire childhood growing up with older people. My parents ran into their own set of problems very early in my life, and I subsequently moved in with and became adopted by my grandparents. I lived with them until I was about 16 years old, experienced some events that made me want to live somewhere else, moved in with my dad for about a year or so, and then actually came back to live with my great-grandma. Now that was an interesting experience. Under the age of 20, I probably spent 18 to 19 of those years living with grandparents. Where am I going with this? If there is one thing that I've learned having spent so much time living with older people, it's that change does not come easily to them, and oftentimes it's goddamn near impossible. For better or for worse, the vast majority of older adults are largely stuck in their ways. The same of course applies to our now 80-year-old president. I see him as the worst combination of Buffett's trifecta that you mentioned: he is one of the most incompetent people I have ever seen, he is corrupt to the core, and though it seems he's falling asleep quite a bit here lately, I would say he is boundless with energy. Now that is a man who is dangerous, especially so as the president of the United States of America. I was reading a book late last night that talked about the events that took place during the Pandemic and shortly thereafter. It was still somehow shocking to me how Trump acted during that period, and just how erratic his actions were given the circumstances. It dawned on me that this is a man who has decided his character. He is who he is. There is not a scenario where Trump is going to have some epiphany where he suddenly wants to do good by the American people. Trump will engineer chaos; you can count on it. He will not change.

-

They quite literally have so many capital allocation options right now that lowering the bar makes no sense. Not the least of which is just buying back their own shares. Or clearing out the remaining outstanding ownership interests in their insurance subs. Yet they are borrowing $ to make this investment. So they likely have some plan. Both with this as well as Sleep Country, my concern is retail has never been an easy business. And neither is Food and Beverage. Recipe/Keg for example over the long term has not really generated any sort of impressive returns. As for the real estate angle, even if there was a ROI lift it would be a one time benefit, and not a recurrent scenario. It would be interesting to see how it plays out over the course of time. It's why I said every such decision should be benchmarked against a share buyback.

-

@villainx More like retailer

-

Is this why you repeatedly make a point of claiming so many people are stupid?

-

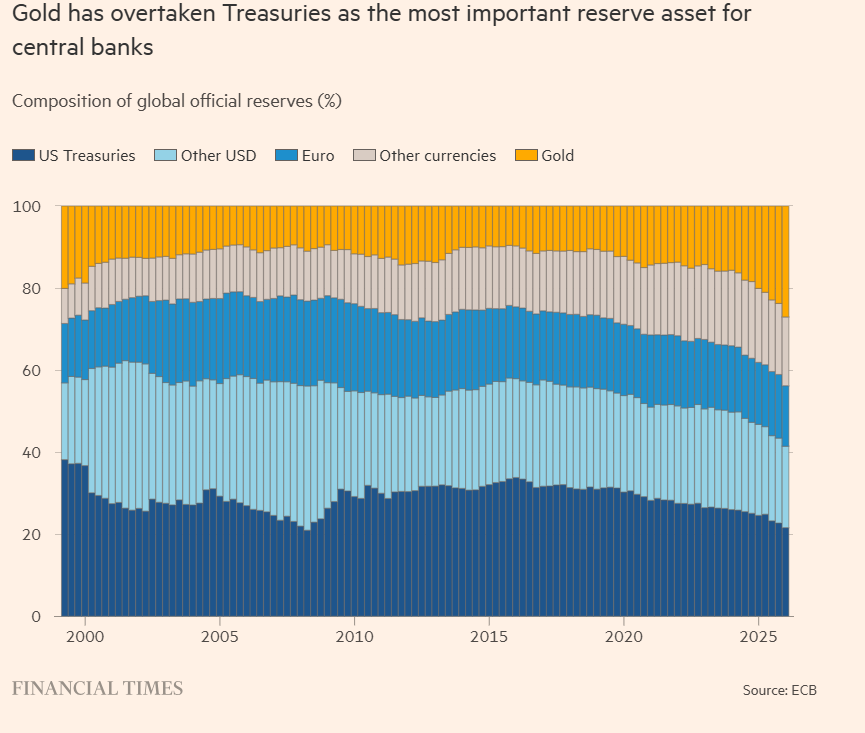

This was dated June 2 so maybe Treasuries have recaptured the lead. Two trends - gold as a diversification for CBs from USTs and physical holdings of gold moving from NY and London to CB vaults in the country that owns the gold. What does this reflect? Multi-polar world? The return of history?

-

I've tried the same - doesn't work. It would be a useful add on, to quickly get up to speed. It would be great to even isolate certain themes (e.g., the evolution of Viking's thesis on fairfax in a thousand page thread).

-

More Terravest and new (well I had before but I reopened) Nintendo and Copart positions. First one 1% of NW, others 0.3-0.4% so obv looking to increase. All with CPNG profits, selling some short term calls into this strength.

-

Sounds good. It's a wonderful company (at a price). Hard to find much higher quality, so worth a place in a portfolio. Good luck to us all!

-

more Karelia Tobacco.

-

While I do subscribe to Claude and Perplexity, they can not access the website - guess I tried using simple prompting as opposed to coding...hmmm...

-

Sounds like you are saying data centers?

-

Spot on from the MD&A: “On June 15, 2026, the Company entered into a definitive arrangement agreement with 18013632 Canada Inc., a newly- formed and wholly-owned subsidiary of Fairfax Financial Holdings Limited, and Fairfax Financial Holdings Limited, in respect of a transaction whereby all of the issued and outstanding Class A Non-Voting shares and Class B Voting shares of the Company will be acquired by 18013632 Canada Inc. pursuant to a plan of arrangement under the Canada Business Corporations Act (the “Arrangement”). Completion of the Arrangement is subject to customary conditions, including, among others, court approval, regulatory approvals, and the requisite shareholder approvals.” A first pass I had a brief look at this and I am still not sure how this deal clears a 15% IRR hurdle on the stand-alone numbers. At roughly 8x FY2026 EBITA and a mid-single-digit earnings yield on the equity value, it does not scream “fat pitch”. The base case still feels more like a mature Canadian consumer business than a “classic” Fairfax opportunity. But the deal starts to look more interesting if Port Moody is monetized well ($20-$30m?), margins continue to rebase higher, and Peller becomes a platform for smaller wine, craft beverage, import-agency and succession-driven family assets. I was bracketing around the following crude return estimates and the benefits of Fairfax Ownership Case Return feel before credit benefit Credit-rating benefit/Balance Sheet No real estate monetization 9-10% Minor Port Moody monetized well 10-12% Helpful but secondary Port Moody + margin expansion 13-14% Adds some bridge Port Moody + platform roll-up 15% possible Most valuable here Arguably the more important signal is that John Peller is rolling over rather than just selling out. He knows the assets better than anyone, has already stepped back from operating leadership, and could presumably have taken cash. Instead, he appears to be choosing Fairfax as a long-term home for the family legacy and a partner with patient capital, better credit support, and a willingness to let the business compound outside the public market. That says something. In fact it made me think about Buffett’s old pitch to appeal to family businesses: Berkshire as a permanent gallery rather than a trader of assets. Fairfax may be offering a Canadian version of that bargain, liquidity for public shareholders, continuity for the family name, and a permanent-capital owner that can back the next phase. I would not call it obviously great yet, but I think I can see how it moves from “single-digit winery deal” toward “asset-backed platform with a credible path to low-teens, maybe 15% if execution is good.” My concern is always “are they lowering the bar”? So hopefully there is more to it than a superficial first pass reveals. In this regard I would definitely give Fairfax the benefit of the doubt.

-

You mean to suggest this activism for our favorite India fund, or adopt similar tactics?

-

We do a bit of pair trading as well, with each 'pair' being a different asset class (BTC/Oil), (CPG/Oil), etc. Sell the expensive and buy the cheap. Some of it is relative near term prospects, but it adds time frame to the risk; the expected 3-4 months often doubling to 8-9 months. Two sets of stars need to align .... if/when they do, you do very well. Key, is comfort with open exposure .... not for everyone. Some of it is seasonal. Sell the CAD drillers in May to buy CAD beer; reverse around Thanksgiving. Capture the busiest times of the year for each industry. Key is honest and accurate forecasting ... not the what you hope might happen. Not for everyone. Used to do pair trades within the different sectors of o/g itself, but it just wasn't worth tying up the portfolio. Were we to accept the restriction, we could do a lot better on the risk/return. Differeng strokes. SD

-

Buffett/Berkshire - general news

ValueMaven replied to fareastwarriors's topic in Berkshire Hathaway

So sad - this is a huge negative for Netjets! Even still they have world-class safety