All Activity

- Past hour

-

The existing title system is already quite efficient because with the passage of time and as property changes hands, there is less and less to research. The issue is, what are we insuring against today? My guess is, it is more and more scams, as opposed to legitimate title issues and questions, which are routinely picked up by title examiners. Tokenization probably would not make difference because unlike all other insurance, title insurance only provides coverage for prior events and is relatively cheap to begin with.

-

Buffett/Berkshire - general news

Intelligent_Investor replied to fareastwarriors's topic in Berkshire Hathaway

Surprised he sounded down on Apple. Maybe he was just a big Tim Apple fan -

Buffett/Berkshire - general news

Intelligent_Investor replied to fareastwarriors's topic in Berkshire Hathaway

Charlie didn't give a single f who he offended. Warren does care about PR -

But why do we need tokenization for this? The existing title system could probably be made more efficient but at least there is a public body there that people can trust.

-

Yeah I was saying this for a while, everyone was pretty exuberant about France but they never really faxed a strong team yet... and they choked. Shame cause the potential was there but always happy to see Mbappe lose.

-

That’s penalty decision against France was questionable, imo. The French looked soulless in this game and Mbappe was nowhere to be seen. I guess that’s how you win in against a team with a star player. Kudo’s to the Spanish defense and midfield. They destroyed the French game and while it wasn’t pretty , it surely worked. They clearly were the better team.

-

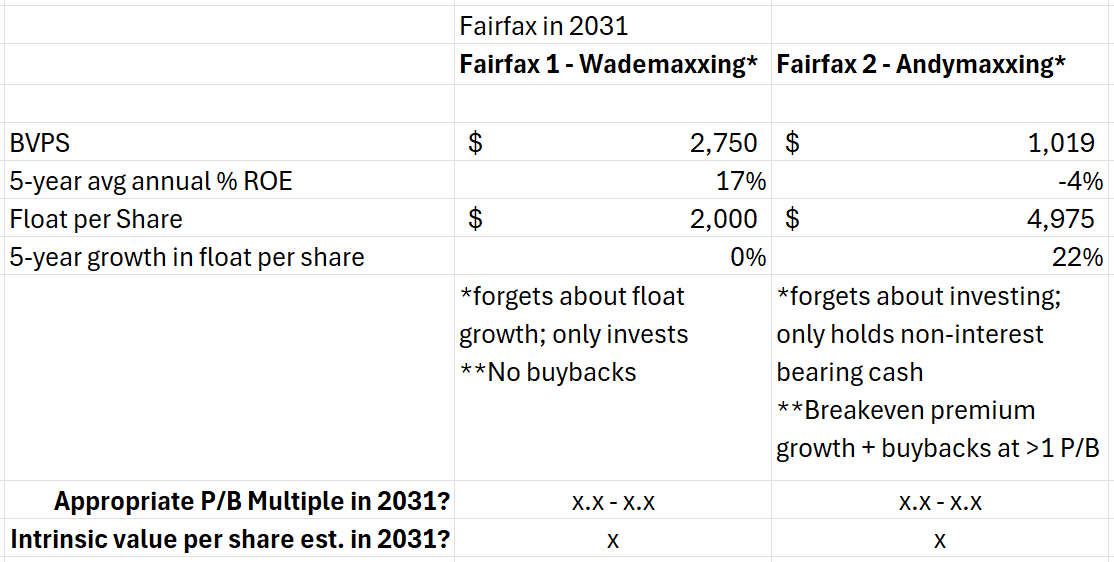

I hear you - these methods work, and ROE as a sanity check on economic book value makes sense. Also, hello...hope to catch up more at the next conference. Need as many smart and generous people in my life as possible! You'll have a perfectly decent day if you ignore the below. But if you get bored, humor this ridiculous & unrealistic thought experiment, if you will. How would you fill in the blanks? Is the premise too ridiculous to even consider?

- Today

-

Fairly good summation of the SOH tolling 'thing' ...... https://oilprice.com/Energy/Crude-Oil/Trumps-Hormuz-Toll-Could-Upend-Global-Energy-Trade.html 'Imposing a charge equivalent to one-fifth of the cargo’s value would achieve almost exactly the opposite. It would transform a temporary geopolitical disruption into a permanent structural cost, replacing the risk of an Iranian blockade with an American toll that could be just as damaging to energy markets. After spending enormous political, military and financial resources trying to preserve freedom of navigation, Washington would effectively begin charging the world for the freedom it claims to have restored.' 'The resulting levy on oil and gas could therefore approach $115 billion per year under fairly moderate assumptions, before including petrochemicals, fertilizers, containerized goods and other commercial cargo. This would not be a conventional shipping toll based on the cost of providing a service or maintaining infrastructure. It would be an ad valorem charge on some of the most important commodity flows in the global economy.' 'Washington would effectively be asserting that military protection of an international shipping route creates a right to collect a percentage of the goods passing through it. That principle would have implications far beyond the Gulf. If naval protection creates a right to tax commercial cargo, other military powers could make similar claims around contested maritime routes. The distinction between securing freedom of navigation and monetizing control over navigation would become dangerously blurred.' 'The direct 20% payment would therefore be only the beginning. War-risk insurance premiums would remain elevated, while shipowners could demand additional compensation for crews and vessels entering the region. Financing costs would increase because cargoes exposed to possible seizure, delayed payment or changing regulations would become riskier collateral. Traders would build larger margins into contracts, and buyers would seek supplies from routes not subject to arbitrary charges.' One has to be truly gifted to f*** ** this badly Gasoline prices have already begun to reflect the now higher crude prices; it is only a matter of time until US refineries start failing (running at capacity, no maintenance shutdowns), China has already further scaled back its refining, and the Saudi East West pipeline terminals at Yanbu are very vulnerable. Houthis don't have to destroy, continually damage enough to progressively reduce throughput .... is good enough. Of course ...... most would expect Orange Boy to do whatever he can to lower gasoline prices, and the speculative community to squeeze US inventories as much as possible. Rising volatility, rapid change, pending mid-terms, and an 80 year old dealing with the pressure ..... what could possibly go wrong SD

-

Insurance belongs to FFH - I don’t think they need to consolidate, perhaps similar structure to Anchorage but instead of Omers, have FFH

-

Call me skeptical. At age 95, Munger was much better at keeping his cards close to the vest.

-

Buffett on CNBC https://www.cnbc.com/video/2026/07/15/warren-buffett-ended-gates-donations-to-give-more-to-my-children-not-because-of-epstein-ties.html https://youtu.be/vaHbb3-tHQA

-

Buffett on Warsh - https://www.cnbc.com/2026/07/15/buffett-says-trumps-pick-of-kevin-warsh-for-fed-chair-was-good-choice.html

-

https://www.cnbc.com/2026/07/15/warren-buffett-calls-bill-gates-actions-with-epstein-distasteful-but-people-make-mistakes.html at the very end of the video - Buffett broke his leg a few weeks ago and had surgery and is recovering well. 96th b-day coming in a month or so

-

Thank you @gfp. From the interview: Becky: You did not buy when they were asset light, but are when they are spending big on assets. Why? Warren: I made a mistake. Any idea why he is willing to buy now but not back then? I am sure he is deflecting by the "I made a mistake" answer. Any thoughts on what he is not giving away?

-

Yeah, this issue isn't that difficult. We don't even need studies other than for those who can't understand that illegals absorb everything needed by those who are here legally.

-

Worth a watch - https://www.cnbc.com/2026/07/15/warren-buffett-tells-cnbc-he-initiated-berkshire-hathaways-investment-in-alphabet.html

-

Thank you very much @rajpgokul ! My *main* concern after looking at the raw numbers since 1999 is the quality of their current loan book. Good to hear that they cleaned it up. They are a bit overcapitalized now, debt level, deposit to loan ratio, current NPL trends and efficiency ratio all look well. So not much concerns here.

-

Now half time would be twice as long for the final because there needs to be a half-time show with Bieber & Shakira... Damnd American greed really does trump everything.

-

Actually this chart shows a weak correlation between rents and home in the short and medium term. Since 2020 (Biden’s term), home prices have increased much more than rents. However, since illegal immigrants (which allegedly surged during Biden’s term) rent rather than buy (because they can’t buy in 95% of the cases) how can this be - it should be the other way a round? The Fed study from the heavily politicized Dallas Fed is a draft paper. There are other studies that you can find showing a very weak correlation between immigration and home prices. In the US we have the situation that a lot of construction labor are immigrants and many of them illegals. What happens to the supply situation when they are gone and what is the net effect? It doesn’t seem that straightforward than you make it to be,

-

The pain for the IRGC is going up substantially next week. Bridges and power plants. https://www.iranintl.com/en/202607156387 "Next week it gets really bad for them because next week comes the power plants," he said. "Next week comes the bridges. We're gonna knock out all their power plants. We're going to knock out all their bridges unless they get to the table and negotiate."

-

This is great colour. Thanks for sharing. How do you expect FIH to fund the deal? Would IDBI issue stock to consolidate IIFL Capital and Digit? Do they leave publicly traded stubs for those holdings?

-

A very valid question and you are right to be skeptical. Background: I live and invest in India - I would rate 'IDBI Bank' as an 'above-average' investment opportunity which doesn't clear my local hurdle rate, but I still believe this is a great deal for Fairfax Financial. To provide better background - Fairfax Financial is 17% of the global fund I manage, IIFL Finance is 10% of fund (we own 1.7% of the firm), Fairfax India is 2% and IIFL Capital is 2% of the fund. All these have been long term holdings for us 5+ years and IIFL group has been in my personal portfolio for 15 years now. Why winning IDBI is great for Fairfax: 1.) IDBI is not a standalone deal, but it would boost all Indian financial investments of Fairfax My guess is that - Fairfax will form a bank holding firm which will hold IDBI Bank, IIFL Finance, IIFL Capital and Go Digit as their subsidiaries in 1 integrated group framework. In Indian context, a bank is the central core around which the highly valued capital light businesses can be built and scaled. In most verticals like asset management, insurance, institutional brokerage etc - the banking subsidiaries own the largest market share as they have the brand, balance sheet, customer relationship and distribution network. IIFL Group and Go Digit have been able to build large scale businesses despite not having a core banking shareholder. WIth a bank backing them and providing them with all its advantages, they can move to the next level in terms of growth and profitability. For example, the cost of funding for a bank backed firm will be 100+ bps lower (higher credit ratings) and can directly mean a 5% ROE improvement. Similarly, valuation multiple can go up 50% by being aligned with a bank for all these entities. The group will have good cross-sell synergies across - banking, broking, wealth management, asset management, life insurance, general insurance, reinsurance, investment banking and asset financing. I would expect a 1 billion USD uplift in valuation across their Indian financial investments with IDBI in the loop. Fairfax increasing its position in IIFL Capital to 51%, IIFL Finance moving a shareholder resolution to raise 1.3 billion USD of equity (July 24th vote) and taking a direct stake in Digit ealier this year are points to be noted. Indian central bank (RBI) has also been pushing banks to move their insurance (regulated by IRDAI), NBFC or asset management (regulated by SEBI) arms into seperately listed firms. Hence, my guess. 2.) IDBI is an A+ asset that has been run badly IDBI like several other public sector banks is mismanaged and not run to its true potential. IDBI has a phenomenal deposit franchise that is very difficult to replicate. The issues that you mention are all due to their lending ability that used to be mired in corruption and bad culture that comes along with having Government as your ultimate owner. They asset side has been cleaned up over the last several years and Fairfax gets a clean slate on the asset side that they can build upon. IDBI's cost of funds is like 4.7% (250 bps below G-Secs) with a 45% CASA ratio. Almost a 18 billion USD CASA book that is sticky and hasn't left them even in tough situtations. This is very valuable. In CSB bank turnaround, Fairfax quickly fixed the lending side and has been able to grow their asset book at 25% type CAGR, but they haven't been able to build their deposit book. That experience should have reinforced into them as to how valuable this sticky deposit franchise is. I would say, with the current bank licensing conditions, it would take 15 years for any small bank and new licensee to build a CASA or deposit book of this size. IIFL Finance is a co-lending partner of IDBI even now. This along with running CSB for 5+ years should give Fairfax the necessary knowledge to build up the asset side without taking excessive credit risks. IDBI bank currently earns 13% ROE purely from the deposit side advantages. Fairfax should be able to build a good credit book and move it to 16-18% ROE along with all the low hanging fruits that comes with an ownership and culture change. The large CASA base will allow them to build prime retail and corporate loans that compound value with minimal volatility. 3.) Large ticket size compounding for the next 20 years At a 5.7 billion USD cheque size, there are few opportunities of this scale for Fairfax. I (similar to the folks at Fairfax) believe that India is a secular growth story for the next 20 years and has the potential to be a 20+ trillion USD economy in that time frame. India currently has 4 large private banks and 3 large public sector banks. I believe that 5 of these large banks will continue to be the Top-5 even then. Indian large private sector banks have a 10 year average valuation of 3X book value. Fairfax is buying IDBI at 1.15X closing book value. If the turnaround doesn't materialize, they will still be able to exit the business at 1X book value on a conservative basis. On the upside, they can compound earnings at 16-18% CAGR for the next 10+ years and the valuation can double in that time-frame. The INR has gone through a large depreciation cycle over the last 2 years and well placed for lower hit in the coming decade. The absolute dollar returns/ money multiple from this deal can be super attractive even with decent execution. The overall set-up looks asymmetric to me with a juicy Risk-Reward for that ticket size.

-

Crore is confusing the hell out of me, I'm probably not the only one. So I just looked it up (again): 1 Crore is 10 million. 1 USD is currently 96 INR. So 50,000 crore is: 50,000 x 10 million. Then divided by 96 = $ 5.2B. Fairly soon 1 USD will probably be 100 Rupees. Then 10,000 crore will be $ 1B.

-

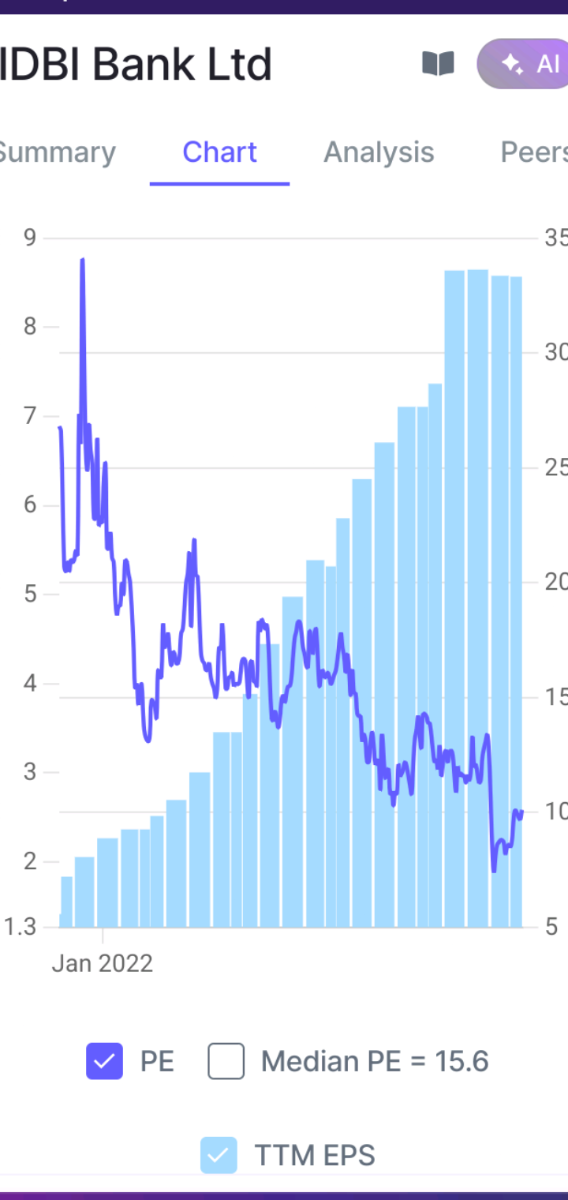

https://www.screener.in/company/IDBI/consolidated/ Click on PE Ratio on their chart, it shows that PE has fallen from 25 to 10 while EPS has grown from 2 to 8.5 over last 5 years.

-

I also think it’s a national banking platform that’s ready to go. CSB was always a good plan, but it remains predominantly a southern/regional franchise. IDBI potentially gives Fairfax a national platform overnight. At ₹81 it looks like a reasonable deal rather than the deal of the century, but with a meaningful right tail if they can leverage it across their broader Indian financial ecosystem. To your point, I suspect they’ve learnt a tremendous amount from both Eurobank and, importantly, the Bank of Cyprus. Those weren’t just banking investments, they were lessons in what a well-capitalised, well-managed banking platform can become. Bringing Hafize Gaye Erkan into the group also makes me wonder whether Fairfax’s ambitions extend well beyond simply lifting IDBI’s ROE. I’m not suggesting this automatically signals a banking roll-up, but it does feel like they’re assembling the people and platforms for something larger over the long term. Finally, if this gets over the line, it says a lot about Fairfax’s reputation and credibility in India that they were trusted with such a strategically important asset. No doubt the market will but it’s a sensible move (at the right price) and arguably a move that only Fairfax can make at this point in time.