TwoCitiesCapital

-

Posts

4,994 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by TwoCitiesCapital

-

Forgive me for being willing to admit that I was wrong and the investment was a mistake. I didn't buy it as a lottery ticket in 2012. I bought it because I believed in rule of law. 12 years later, multiple lost court cases, and administrations from both parties f*cking us over, I'm willing to call it what it is/was - a mistake. The reason I continued to hold it is because I recognized a very real possibility that Trump may win, that there are people out there who are willing to suspend reality to believe Trump isn't who he is/was, and the very small possibility that I am wrong about being wrong. Not many investments offer a 10-20x pay off and I recognized this is one of them. Trump has been elected - I knew that was a possibility. The prices popped - I knew that was a possibility. I have now locked in 300-400% gains on most of my shares acquired during COVID which is bout 1/3 of my position. I have other limit orders in to sell well below par for higher gains as the disillusionment knows no bounds. If we get to $20+ again on the $50 preferreds, I'll be out entirely. Feel free to hit my asks on FMCCJ if you're so confident.

-

Last time he was president, most of the people surrounding him were very decorated too. And a ton ended up in prison and very little was accomplished. Keep dreaming though.

-

Threats outside of Bitcoin. Threats to democratic institutions like independent media, independent courts, etc. Everyone likes to pretend that left leaning media is biased against the Trump and tells lies, but it was Fox news paying the largest settlement ever for peddling known lies in favor of clicks and eye balls. Everyone wants to talk about how the courts are biased against Trump while conveniently ignoring those same courts convicted Biden's son and Biden has this far not abused his power to prevent it. Today, we still have independent institutions that support and protect the democratic processes we have on both sides of the aisle. Trump made them enemy #1 the last time around. I don't expect it'll be different this time around and the effects of that will far outlive his presidency

-

All we've done is trade one "danger" for another. And the one danger that we're 'avoiding' was largely already solved via self custody. So we went from remote 'danger' that is already well managed to other dangers that are not.

-

You're not delusional. The people that expect this time will be different, but cannot say why, are.

-

Because, like most autocrats, Trump values loyalty. And Elon Musk spent $130 million to "buy" the appearance of his loyalty despite having been über critical of Trump in his first term. Trump is absolutely the type to throw friends a bone (most politicians are) and id expect he might allow for some regulatory wins that benefit Tesla over its peers - like going easier on self driving tech or something of the like.

-

I realize that everyone has been hopeful and wrong for the ~12 years I've been a holder. I realize that Trump's administration only made things worse, not better, the last time around. I realize that that some people seem to believe that he'll do something opposite this time around because he said so while ignoring all of the other unfulfilled promises he's made. And I realize last time the preferreds were at these prices we still had potential remedies through the courts that have largely resolved against us removing that avenue for payment. And I realize there are people willing to ignore all of this and bid the shares back up again on hopium - so am happy to let some of mine go for what has been a reasonable trade over the last 3-4 years.

-

Especially a president who is a debt guy responsible for many of his own personally bankruptcies who spent like a drunken sailor last time he was in office. But yes - a "Bitcoin" President indeed Exactly. Doesn't matter who is president and Trump is likely not any better, or worse, than Kamala in this regard.

-

Just thankful for an opportunity to exit a portion of the position at reasonable gains to get the capital deployed elsewhere. Someone else can be a sucker for the next 4 years. Making 300-400% on my COVID era adds has made up for the losses on my $7-14 lots ($50 par) that I'll continue to bag hold on just in case...

-

If I buy $500,000 home for 3% down, and it doubles in value next year to $1 million - is my ROIC 100% or is it 3300%?

-

The mechanics are slightly different than an option. With an option you can only lose the premium. With the TRS, you can lose 100% of the notional (or more with financing payments included). But they are similar in that both provide leveraged exposure to the underlying for a fraction of the cash for an implied, or explicit, financing rate. Very similar - yes. But instead of the bank lending you 100%, you're putting down 10-15% initial margin, any daily margin for moves against you (while also collecting it for moves in your favor), less any financing rate. So instead of being infinite with no money down, you're in the ballpark of 7-10x leverage. The actual ROIC will be determined mostly by where the stock ends, but also somewhat by the path of how it got there since you're daily on the hook for potential cash margin which each day adds to, or deducts from, the ROIC. We would basically need to recalculate daily to get an accurate ROIC figure, but taking 7-10x the underlying cash return should get us in the right ballpark. We may just be arguing semantics - the $ return will be very similar, but since ROIC is a ratio and the denominator of the ratio is changing dramatically, the ROIC between the is dramatically different.

-

This is akin to saying the ROIC of buying a call option is the same as buying the underlying stock/shares. It's not the same. The shares have a ton more invested capital than the option does. The $ return may be similar, but the Return on Invested Capital is different by nature of being a ratio and the denominator of "invested capital" being dramatically different.

-

It isn't though. To buy the shares required a cash outlay of hundreds of millions of dollars. The TRS probably required outlays of 10-15% as initial margin meaning the trade was nearly 7-10x levered versus buying the shares outright. It's not exactly that though because there was a financing rate paid the whole time which would reduce the amount gained and then there were a handful of quarters with slightly negative performance requiring small additional cash outlays for that 3 month period that would have been return in the following quarter, but still impact the ROI calculation. Because they didn't have a full outlay upfront. They saved hundreds of millions which stayed invested in other parts of the company generating returns too. It's like buying a house with 100% cash or buying it with a 30-year mortgage. The return profiles and ROIC are different even if the $ gain on the home price is equivalent.

-

QED Slightly better than expected given another extension if duration, but basically all but totally offset. The duration on our bond liabilities are around 3.5 years, so it’s a little longer than it was last quarter, and if you look at our liabilities, it’s relatively close. We don’t match on purpose, but where we sit today, our liability duration is close to our asset duration. You can sort of see that in the IFRS 17 numbers, that we had a big loss on the discounting, about $750 million, $760 million that was offset almost--very closely with the $800 million-plus of gains on our bond portfolio, so we’re pretty much matched where we are today.” Peter Clarke

-

Yup. I did the analysis a week ago. I looked at the 3-year returns for top 100 stocks in the S&P 500 today (so should bias to the top performers because it was a different list 3-years). Even after this year's 20+% rally at the index level, 30+ had negative real returns and another ~7 or so we're basically at flat to sub-1% real returns from October 2021. I can't speak for the other 400, but I'd assume it's a similar story if this is the story of the companies that retained/obtained the top 100 spots over that time. Would have also been much worse at the beginning of the year. Having 30-40% of the index still having flat- to -negative real returns over 3-years is crazy to me - especially when looking at what the index as a whole has done. We really did have a bad inflationary shock that killed most equities - one that many still haven't recovered from - and it was all papered over by the performance of FAANGM and then MAG7. And not even all of them - AMZN and Tesla have sucked air over that period on an inflation adjusted basis as well. I think it may be the opposite. Similar to the tech bust - the MAG7 may struggle with regulatory scrutiny, higher embedded labor costs from inflation, and huge CapEx requirements for a later date pay off while the rest of the economy starts to gain momentum and recover from 2021/2022 inflation shock. I'm more comfortable buying stocks here, than I was in 2021, despite indices being far higher - and that's because many stocks are still quite a bit lower (some in nominal terms, most in real terms) despite 3 additional years of retained earnings and revenue growth.

-

-

How much do we think Muddy Waters is paying him to continue being negative?

-

I don't mind them assuming the insurance biz is commoditized. We know it isn't true and that good underwriting is what makes this business model work, but we could give him that since it is for many others. But not paying any attention to the historical track record of the investment portfolio? Of the earnings it's managed to spit off during the 2-3 years this guy has been critical of them? Fairfax's market cap at the end of 2021 was somewhere in the ballpark of $10-12B. They've earned nearly $12B in headline earnings (not including balance sheet items and gains) over the last 4 fiscal years and much of that wasn't the insurance biz.

-

I have had the CFA charter for nearly a decade at this point and nearly ~15 years involved with the program if you consider the studying and time up to the requisite work experience. Professionally, it was a no brainer. I went to school in Mississippi and then moved to NYC. I'm 100% certain the only reason anyone even looked at me was having passed the 1st level. As a matter of fact, I didn't get a single call back for interviews UNTIL a few days after adding it to my resume when I got the results. If you don't go to a target school, CFA is probably one of the few ways to get noticed and distinguish yourself. That being said, none of the roles I had in NYC required it and I was often the only one with it. Nobody really cares about it beyond it getting my foot in the door. It was just something to give me pedigree that was lacking in my school choice. The MBA from a top school was the be-all end-all when I was in NYC ~7-10 years ago. Where I'm at now in the Midwest, nobody really cares about MBAs. The CFA is everything and several roles require it or progress towards it. Outside of introductions to more esoteric products like derivatives/futures/interest rates theories and etc, I don't think it's helped a ton in my personal money management. But professionally it was worthwhile and has given me opportunities and wages I wouldn't have otherwise been eligible for. I also enjoy the events put on my by my local society, it's been great for networking, and my employer pays my dues. So its really great from my perspective.

-

What a joke - the mental acrobats to avoid admitting he was wrong is insane. Earnings will normalize. There will be lower rates in the future and more catastrophes. And FFH will have fewer shares, more retained earnings, and additional growth through its associates to make up for it. Not to mention today's value is still probably fair in that environment even if it doesn't happen like that. If this man actually put a pen to paper, he could work this out for himself.

-

Hard to measure an ROI on something that basically has no upfront cost, but ongoing cash draws. In Fairfax case, it's basically infinite because it's only been up since they opened it.

-

The # of ADRs are fixed and the # of shares backing them are fixed so the ratio remains constant, but ADRs CAN trade at wide premiums or discounts to the underlying security of the issuing bank isn't engaging in the creation/redemption of the ADRs units so that the different can be arbitraged. I'm not 100% sure what drives whether the banks are engaged in issuing/destroying ADR units, but there are ADRs that do trade at premiums/discounts in periods where the sponsoring bank closes that ability to arbitrage. Please don't make me hate FFH with this thesis. Right? It finally seems like the stock is actually responsive to earnings announcements now! A few hundred million tacked onto Q4 earnings as a result a la the TRS. Brilliant! He might have been the one pushing it up today trying to exit? Though he should've exited as soon as it was clear his thesis on the aggressive accounting was bunk when Digit IPOd...

-

I feel similar watching Elon Musk over the last 18 months...definitely seems to be taking after his father. I suppose you have to have some eccentricities and a willingness/ability to be different to achieve the level of success these guys have...but when that starts bleeding out of business success and into personal turmoil it really is sad.

-

I didn't sell in the past few quarters, but sold a small portion of my position in 2023 to keep it below the position limits of 10% of networth that I set for myself. Now that Bitcoin, and other, names have performed fairly well in late-2023/2024, I have been able to hold onto shares this year and may actually be able to add in the next pullback. Isn't necessarily optimal - but the rules were set for a reason and am being diligent about following them.

-

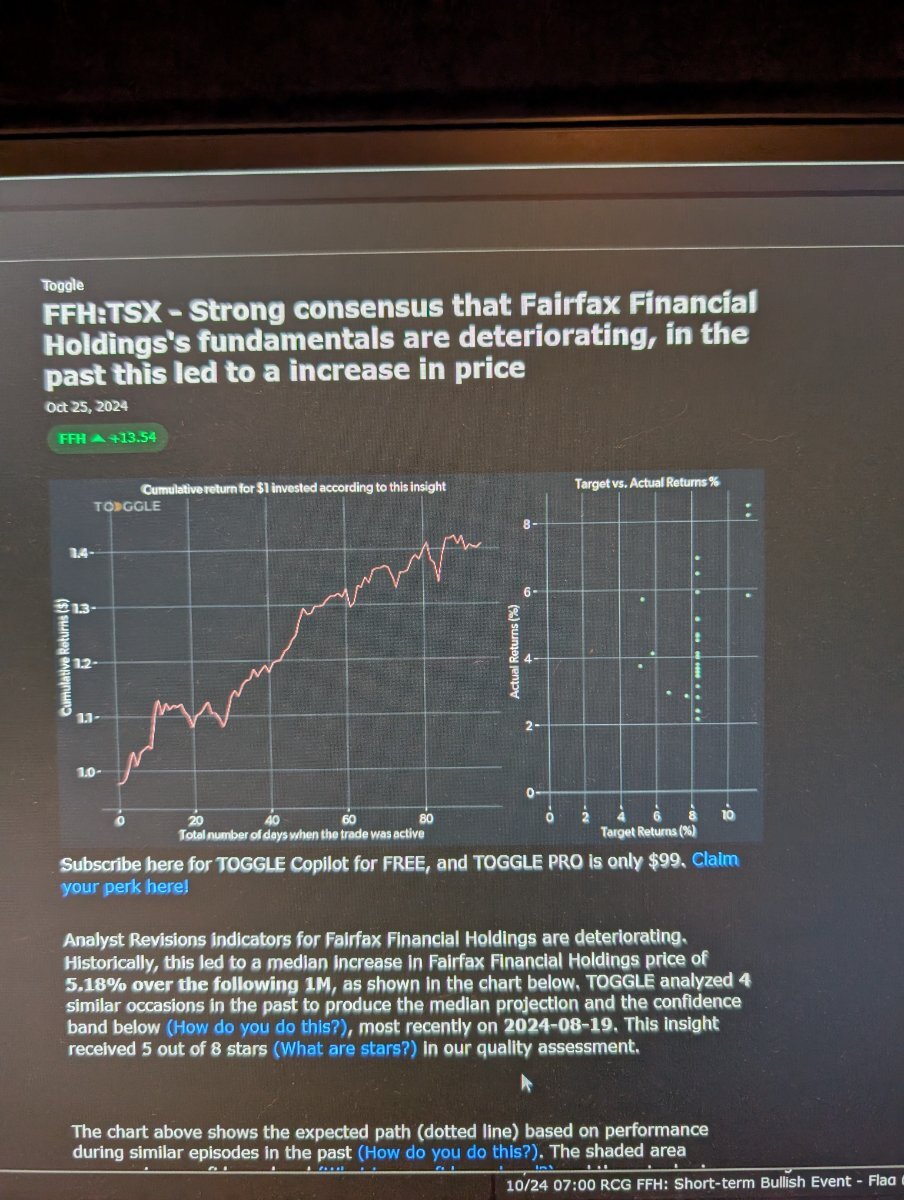

Lol Is it the deteriorating fundamentals OR Q3 earnings that is gonna propel this higher?