LearningMachine

-

Posts

1,829 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by LearningMachine

-

Got it. One company I've been watching in biotech space seems to be operating more as an investment fund. Similar to how Sequoia buys tech companies early and takes them through IPO, this company takes drug pipelines in early stages and takes them through approval, which looks like a high ROI activity to me. The company is Biogen. It is not super-great how they have been handling their aducanumab investment, and we also don't know how well their recent other investments will actually pan-out. Have you looked into it? XBI might be able to capture some of these early pipeline companies also, but then we have to study the success rate of these companies - because of the huge pricing power, getting approval is such a huge success that maybe a low success rate could be ok? My other worry with biotech companies is that it needs just a small tweak in the law for their pricing power to deteriorate, e.g. if Medicare is allowed to negotiate with drug companies. The other issue is constant expiry of monopoly on drugs. Medical device companies can get around that through other means, e.g. new patents for the same evolving devices, brand-name, insider-secrets, more complex/evolving interfaces/functionality that is harder to copy, etc. However, they are all trading with high valuations.

-

If biotech is going to be the next big waive, wouldn't S&P 100 based indexes, e.g. EQWL, be able to catch it also?

-

I think Nortel and Cisco were more like automakers, and QCOM was more like patent owner for some technology needed for autos. None of them owned a right to scare pathways, and thus weren't like highways. The analogy for the internet could have been fiber only if more fiber was not allowed to be laid. So, fiber is not a good analogy for spectrum either.

-

QQQ - I have the same concerns that it is Nasdaq-only, and the company that ends up leveraging AI most might not end up being on Nasdaq Regarding IWO/IWF, I think there is a good chance that any new companies that have potential to leverage AI might go IPO after they are already quiet big in valuation. So, going with broader index might dilute your bet too much unnecessarily. Given what you said about winners taking it all in the other equal-weighted etf thread, what about S&P 100? One risk there is you miss out on the growth of the company from S&P 500 to S&P100, but there might be a good chance that such companies with huge potential might not become public until they have already reached S&P 100 market cap, and that way you dilute less over the bottom 400 in S&P 500? One risk with this approach though is that Antitrust might get more active and might not let companies get too big. While at it, how about equal-weighting S&P 100 now? Given it is S&P 100 not S&P 500, it addresses your concern to some extent about winners taking it all?

-

It is possible that might work. That said, this expectation is somewhat already reflected in the P/E by the market. So, if prediction ends up wrong here by any chance, e.g. new companies come and do a better job at providing technology or provide amazing consumer experiences directly, those buying at today's prices might not do as well. One thing all these bots buzzing around and even stationary bots (IOTs) will need is ability to communicate with the mothership (i.e. companies owning them) and/or with each other. For bots running around at home, that communication can be over the unlicensed spectrum at home, that then connects them over fiber to the motherships. For bots running around or stationed outside home, the communication will likely need to be over spectrum that has some sort of guaranteed availability, i.e. licensed spectrum. Spectrum for AI bots is like highways for cars. Another way to look at it is that imagine if before humans arrived, you could have figured out that they will need a way to communicate with each other and with some central data repositories/services they create. Imagine you could somehow own some percentage of audio-frequencies that humans can hear & utter, and some percentage of electromagnetic-spectrum frequencies visible to humans (e.g. black, blue, green, white colors), and humans had to pay you with their fruits of labor for using those sound & light frequencies, you could make a lot of money. Currently, there is only one company that has the most amount of cash coming in to buy out spectrum frequencies as they become available, and Buffett is investing in it. Market is currently predicting not much from this company for AI. If market prediction ends up being incorrect here, it might work in the favor of those investing in it today.

-

Buffett/Berkshire - general news

LearningMachine replied to fareastwarriors's topic in Berkshire Hathaway

Continuing to add to Kroger - still a relatively small position. -

Buffett/Berkshire - general news

LearningMachine replied to fareastwarriors's topic in Berkshire Hathaway

Also, as expected, getting out of drug companies. Also, getting out of Chevron. -

Buffett/Berkshire - general news

LearningMachine replied to fareastwarriors's topic in Berkshire Hathaway

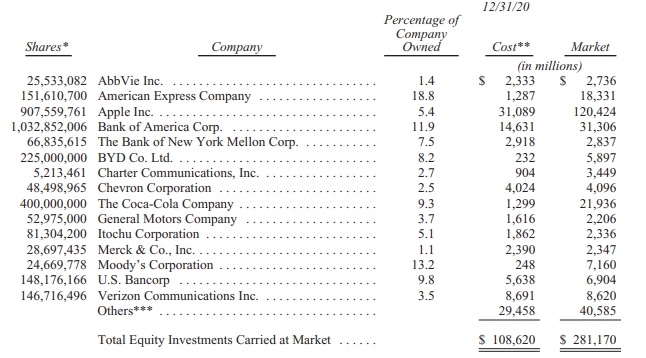

As expected, BRK added VZ shares, albeit not as much as I was expecting. Increased VZ stake by 8.2%, i.e. 12.1 million shares. I see VZ holding at 158,824,575 + 73,357 = 158,897,932 shares https://www.sec.gov/Archives/edgar/data/1067983/000095012321007024/xslForm13F_X01/0000950123-21-007024-4471.xml https://www.sec.gov/Archives/edgar/data/1004244/000108514621001803/xslForm13F_X01/infotable.xml' This is up from 146,716,496 + 71,907 = 146,788,403 shares. That is 12,109,529 shares added. That is $701,626,110.26 added at today's closing price of $57.94. -

... and more expensive each crypto transaction gets.

-

Stanley Druckenmiller interview (2018)

LearningMachine replied to Liberty's topic in General Discussion

Thanks @VersaillesinNY and @Spekulatius. I really like what he said about how hard it is to predict which company will be successful in some areas long term, e.g. Facebook was the 11th social network Before Google, there was a company called Yahoo, and If cryptocurrency ends up being used for exchanges, the winning cryptocurrency might not even be invented yet -

At the May 1st BRK AGM, Buffet's lesson from 1903 was inspiring for me: Imagine you see a quick glance from 2040-2050: AI can learn and do anything that 90-95% of humans do today for work. What's the best way to invest to benefit from that glance of AI future? Here is a list of what humans are doing today: https://www.bls.gov/oes/current/area_emp_chart/area_emp_chart.htm. Here is the list of U.S. companies by number of employees: https://en.wikipedia.org/wiki/List_of_largest_United_States–based_employers_globally. Imagine a lot of those things that humans do today could be done by AI. Which companies will capture the value creation from that AI future for their shareholders? Will it be some existing brands and companies whose customers continue to stay loyal to them or have no choice, where companies can use AI to reduce employment costs? Will it be some new companies that patent it well and license the technologies for other companies to use? Will it be some new companies that come up with amazingly new customer experiences at great price-points using these technologies? Are there highway-equivalents that you can buy now that will be needed with 100% certainty in that AI future by AI bots buzzing around? Back in 1999, imagine you had the glance from the future that Internet was going to change the world. How could you have invested so that you would have picked Amazon and Apple, as well as, Google and Facebook, when they went public, while avoiding investing in thousands of DotCom companies that went bankrupt? Imagine back in 1999, you also decided that you didn't want to have to sell anything to pay capital gains. Is the only way to pick Google and Facebook automatically as they went public would have been through picking an ETF or Index fund? Which ETF or Index fund would have picked them up automatically? Would that have picked Amazon and Apple as well? Would that be able to pick automatically any new companies that benefit from AI in the future? Is there a better answer than S&P 500?

-

Thanks, I'm thinking the same. I wouldn't be surprised if the upcoming 13F shows he is now out of BMY and ABBV.

-

Our memories are not as reliable as the transcripts are :-). Here is what Buffett said exactly: In other words, what he said was that he is not going to put $50 billion into something like that :-). I doubt it includes Verizon as he understands that business well as he had the confidence to tell the questioner who asked about Verizon that "he's analyzed the situation well ... he's very capable of thinking it through very well himself."

-

Thanks @Thelilyinvestor for sharing and thanks @Krapdivad for highlighting. I like how Buffett openly shared, "[W]e'd love to put that to work...we won't get a chance to do it under these conditions, but conditions change very, very, very rapidly sometimes in markets." Have we ever seen Buffett use three "very"s in a sequence to indicate how strongly he believes in being ready for that opportunity?

-

Greg Abel named successor

LearningMachine replied to CapriciousCapital's topic in Berkshire Hathaway

I wonder what the conversation between Munger and Buffett was like after that, and if Buffett is thinking he will need to be more cautious with Munger leaking things that they had presumably jointly agreed to not yet share publicly :-). -

@Xerxes, you are probably right. Do I remember correctly that Buffett publicly committed to the Japanese companies that he will be a long term shareholder? Which companies do you think he might have meant, given he started talking about them as "And they are as a group." Maybe some of the pharma companies, e.g. BMY and ABBV? I think figuring out the answer to this question will help us figure out what he sold in Q1.

-

Thanks @Xerxes for sharing. On Alibaba, when Buffett put up the top 20 list of companies, which contained Alibaba, and helped attendees realize that the list won't be the same 30 years from now, to me it felt like an internal conversation that Buffett might have had with Munger as well to not get too excited as we cannot even say with certainty that Alibaba will stay on the top 20 list. I had a similar feeling when he made the audience realize that even if "you had seen a quick glance back in 1903 of all the interstate highways, 290 million vehicles on the road in the United States, everything about it and had realized 'Well, this is pretty easy. It's going to be cars. It can be autos.", investors would have still failed by trying to pick one of the auto-manufacturers or even all of the auto manufacturers in all the excitement. Felt like he must have had a conversation with Munger that even we can see the vision that Chinese economy is going to be much bigger than the U.S. economy, you can still fail by trying to pick one of the Chinese companies at a high multiple based on the assumption that it will stay on the list for a while. It was also interesting to see Buffett talk about Google, Microsoft and Facebook: "So those are the kind of businesses -- they're the best businesses, but they command the best prices too. And there aren't that many of them, and they don't always stay that way." I think Buffett is still opposed to paying best prices for businesses because the high multiple assumes the businesses will stay that way for a while, but "they don't always stay that way."

-

It came up at the Berkshire AGM yesterday that the number of Chinese companies in the top 20 list will probably be higher than 3 thirty years from now. Their valuation will likely be also order(s) of magnitude higher than today's valuations. What do folks think would be the best ETF to take a cut of Chinese economic transactions, and grow along with the Chinese economy?

-

Thanks @Spekulatius for sharing. Really helpful in understanding deeper what was said yesterday :-).

-

Compared to Dec 31, 2020 Cost basis for Commercial, industrial & other went down from $47.561B to $44.934B, which means that in net, he sold something(s) that he had bought for at least $2.627B in total. Fair value went down from $68.361B to $67.054B, that is, $1.307B - there is probably noise in this from various stock movements but some noise could be removed. Net unrealized gains went up from $20.8B to $22.120B, that is $1.32B - same for noise here. Cost basis for Banks went up a little from $26.312B to $26.730B, which means BRK probably bought at least $418M of some bank stocks Cost basis for Consumer products went up a little from $34.747B to $34.787B, which means BRK probably bought about at least $40M of some consumer products stocks What do folks think he sold that he had bought for at least $2.627B? Looks like it will probably be something in this list with a cost total above $2.627B? Looks like it wasn't AXP, AAPL, BAC or KO.

-

Buffett/Berkshire - general news

LearningMachine replied to fareastwarriors's topic in Berkshire Hathaway

Thanks for sharing. It was a good reminder how he realized at such an early age that he had a unique market power to be able to successfully sell more (magazine subscriptions) to his existing well-off customers (who were on Washington Post subscription), compared to others who didn't have that existing positive & direct subscription relationship with well-off customers. -

Buffett/Berkshire - general news

LearningMachine replied to fareastwarriors's topic in Berkshire Hathaway

This is so true! Also true for Apple! Also becoming true for Bank of America! Will probably also become true for Verizon! Of course, Buffett's got a knack for buying good businesses when they are cheap. Then, after Buffett is done building his position, and starts talking about the "why", Mr. Market starts to realize as well how good of a business it is :-). Buffett could literally take a business that is consistently growing cashflow at single digits annual rate, and turn it into a stock that is consistently growing at double digits annual rate, up to some point! Sometimes he screws up like he did with Kraft, where he gets it wrong whether the business will be able to grow cashflow at low-single digits because he missed the loss of pricing power to grocers, but mostly he knocks it out of the park by being able to identify whether the business has economic power to be able to extract single digit growth each year! He has gotten better with age! -

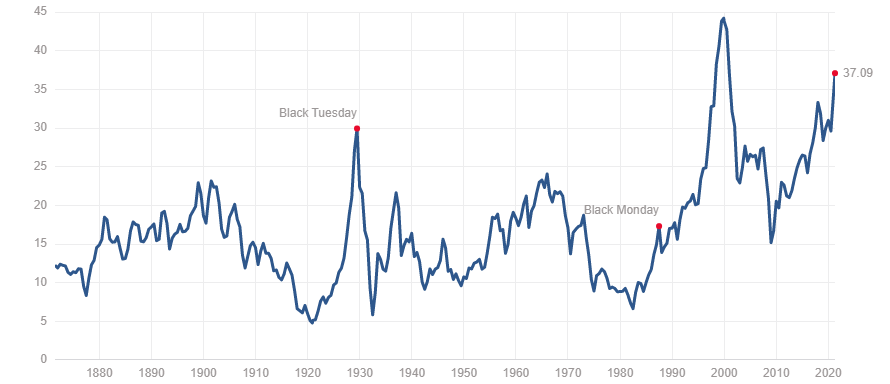

It is hard to predict when the market will crash next. I wonder if it will be easier to predict the range for peak Shiller PE this time? I think we can probably all agree with almost 100% probability that we won't hit Shiller PE of 100. We can probably also agree that probability is high that we won't hit Shiller PE of 50. What about 40 and 45? Above what number will folks start getting some more dry powder ready? Having a range in mind for max Shiller PE might help us be prepared. So far we have went above Shiller PE of 40 less than 2 years in 150 years, i.e. less than 1.3%. Only the 2000 crash started at Shiller PE above 40. All other crashes were at Shiller PE of 30 or below, except the 2020 flash crash. I understand we are in different times with respect to interest rates - if you think these times are different because interest rates are low, it will be great if you could consider that over the past 150 years, we haven't had interest rates low for too long either (https://www.multpl.com/10-year-treasury-rate). Source: https://www.multpl.com/shiller-pe

-

All investments, including assets & businesses, involve purchasing "rights" protected by law: Real estate in law is defined as the "right" to legally exclude others from a well-defined boundary, and certain other rights, e.g. right to build a certain amount, right to use for something specific, etc. Sports team investment is the "right" to legally prevent others from having another team for a defined area and certain other rights. Railroad is the "right" to use a physical pathway and exclude others from using it. Spectrum is the "right" to use a frequency band and exclude others from using it. Pipeline owns the "right" to easement Trademark is the "right" to exclude others from using your name that stands for something. For some of the "rights" above, there is an alternative option, e.g. for Trademark or "sports team" or even real estate or pipeline. For some rights, there is no alternative or alternative is very suboptimal. If a "right" has no alternative, you can make it cashflow higher and higher. How much you can make a right cashflow depends on the alternatives. Ideal investment would be directly owning a "right" that has no alternative and that can cashflow unleveraged at 20+% per year, where there is no other alternative to that "right" for those that need to use it, and where you can take the cash and buy more such "rights" at a price that cashflows unleveraged at 20+% per year. Such an investment is really hard to find. Usually, buying "rights" directly is expensive because other neural nets can easily comprehend what they are buying and are willing to pay a high price for it. So, you cannot buy it at 20% unleveraged cashflow. The next best alternative is buying shares of an entity that owns such "rights". Now, as soon as you put an entity between yourself and the "rights", you take several risks, e.g. agency risk from those employed by the entity taking a big chunk of the cashflows before they let it pass it on to you, leverage risk created by those employed by the entity while not caring about taking the risk for the shareholders, etc. Another option is directly buying rights that might have an alternative also. However, if you are paying a high price for those rights (because other neural nets comprehend the right as an investment also) and those rights have an alternative also, it might not be as good an investment.

-

This is a really hard question to get right. If memory serves right, Snowball mentions Buffett playing this game as well. If we compare his record between his 2000 and 2020 letters, looks like he didn't do too well on this game either: American Express: $8.329B to $18.331B, for annualized return of ~4%, excluding dividends Coca Cola: $12.188B to $21.936B, for annualized return of ~3%, excluding dividends Wells Fargo: $27.844/sh to $30.18/sh, for annualized return of ~0.4%, excluding dividends I'm thinking he probably didn't too well on these because he didn't want to sell as he had to pay 35% tax on capital gains, which would have left only 65% of the capital gains to invest in something else. Selling and reinvesting would have required a higher return to get to the same amount in 2020. Another reason I'm thinking is that looks like he has been investing while worrying about 1970s style inflation kicking in any time and thus has been focusing on Pricing Power and Return on tangible assets/Return on Equity, and so far, high inflation just hasn't kicked in. Also, he probably wasn't able to foresee the impact of GFC and reputation-hit on Wells Fargo. Also, Coca Cola lost some of the pricing power to oligopoly of retailers, which he probably couldn't foresee in 2000. On the other hand, he nailed it with BNSF, where he was able to see it owns rights to scarce physical pathways that are cashflowing well, and that he'll be able to monetize higher not only because of inflation but also because of more and more goods needing to be transferred through those scarce pathways, causing access to be given to highest bidding customers. Looking 15 years from now, I think probability is higher than last 20 years that inflation will finally kick in with minimum wages going up. With high inflation, high probability that interest rates will probably go back up to historical norms. You all know which stock I'm talking about here. We'll see in the May 13F, but I wonder if he is thinking rights to cash-flowing scarce licensed spectrum can also be monetized higher not only due to inflation but also as our economy becomes more and more digital & mobile, with more and more end-points needing access to scarce wireless pathways, which will cashflow best in the right entity's hands, which can give access to highest bidding customers. It is similar to if you could buy a big percentage of the road network before cars became ubiquitous. You all know which stock I'm talking about here. Even though Buffett wasn't super-successful at this game over the last 20 years, I still think he is probably better than any of us at this game as he has been playing it for decades. So, nothing big to share here as you could all see this already in Buffett's annual letters and BRK filings.