LearningMachine

-

Posts

1,829 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by LearningMachine

-

Buffett/Berkshire - general news

LearningMachine replied to fareastwarriors's topic in Berkshire Hathaway

Thank you for sharing. Almost 30% annual return over 35 years without having to worry about taxes. -

@spartansaver, that is a good point. Turns out gold production has gone up lately, and there was also gold production boom in 1970s. Your point is taking me back to my earlier comment that there are really two different logical premises here: (a) Buy gold below or around marginal cost of production for all production at the time ---> You will not lose money (b) Buy gold below or around marginal cost of production for amount of supply needed by tech, jewelry & industry --> You will not lose money I think arrow (b) is much stronger and more likely to withstand test of time than (a). Looks like you might be implying that as well.

-

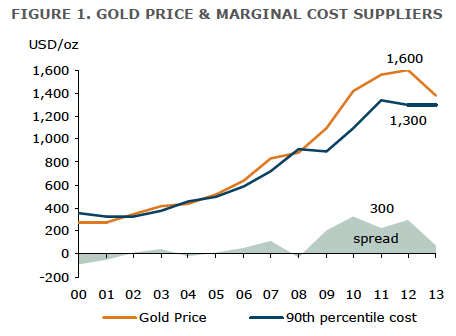

I wonder if gold price has even stronger correlation with the the answer to the question whether the price is below or about same as marginal cost of production? In other words, if you buy close to or below marginal cost of production, does it ever drop a lot from that? I thought data would be hard to get, but then I just did a Google search and found this article that I don't have full access to but was able to snap the picture and text before access went away. Normally, I wouldn't place any credibility on a SeekingAlpha article, but this article does have references to original sources of data. The article goes on to state, "The gold price has always followed the marginal cost of suppliers throughout history (figure 1). The correlation between gold prices and gold mining cash costs between 1980 and 2010 stood at 0.85, which means that the correlation is quite high (source: CPM Gold Yearbook 2011)." Source: https://seekingalpha.com/article/1472081-gold-prices-finally-hit-marginal-cost-of-production I'm wondering what would be that correlation between the answers to the two questions I posed at the beginning? Even higher than 0.85?

-

How long do you think it would take for profits to double? If 10% inflation and subsequently 10% risk-free rates really happen, discount rate will have to be more than 10%, i.e. P/E could go below 10 like it did in 1974. So, I should really be asking how long do you think it would take for profits to triple or quadruple given today's Shiller P/E is 37.47 and S&P 500 P/E is 44.88 at https://www.multpl.com/s-p-500-pe-ratio. Any chance we might get opportunities in the years it takes for profits to double, triple or quadruple to get to appropriate P/E for the new inflation rate/interest rate/discount rate?

-

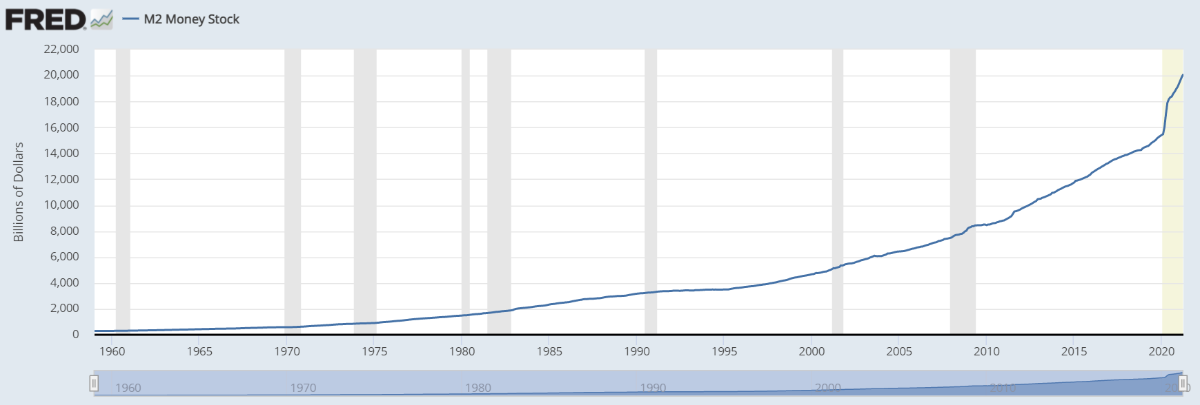

The article would have been more complete and accurate if it hadn't left M2 out of the picture:

-

@no_free_lunch, for probabilities, looks like you are saying: p1=50%: Mild inflation in 3-4% range for 5 years p2=20%: High inflation in 5-10% or higher range at some points in the next 5 years p3=30%: Inflation below 3% Let's go further and assume conservatively in the p2=0.2 scenario that gold will go to $3,528 (2x of $1,764), and that in p1+p3 scenario (0.5+0.3=0.8), gold will go down back to around $1200 (68% of $1764). Then, the expected value gold will get to is (0.2 * 2) + (0.8 * 0.68) = 0.4 + 0.544 = 0.944, i.e. 5.6% loss To get to break-even expected return on buying gold with these probabilities, you have to buy Gold at $1600 (so that downside $1200 is only 75% of paid price). If you wanted expected return to be positive on these probabilities, you have to buy Gold below $1600. $1200 purchase price would be ideal because that's the price it stablized before, likely because that's when it started approaching production cost for high-cost miners. I understand this might not be applicable to @wabuffo and @Spekulatius as they believe minimum gold price has nothing to do with marginal cost of production. I think marginal cost of production still matters for gold. I do think if gold production were to shut down completely, e.g. if gold price dropped to $800, jewelry, tech & industrial uses will start to drive price up to restart production unless central banks & investors were selling at that time for those uses.

-

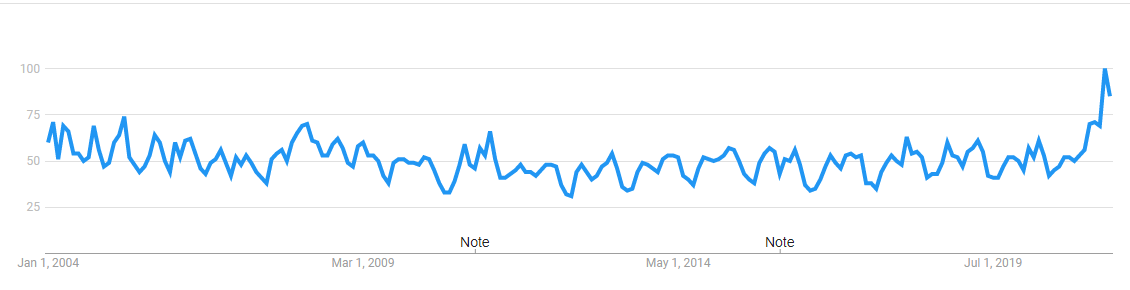

Inflation expectations are at highest they have been since 2004. So, both (1) monetary supply and (2) inflation expectations criteria are now being met to get inflation going... https://trends.google.com/trends/explore?date=all&geo=US&q=inflation

-

Here is how I worded my Scenario 2: "High inflation in 5-10% or higher range at some points in the next 5 years (p2= 65%?)" I'm not saying don't buy stocks at all. I'm saying Scenario 2 has a 65% probability of happening, and interest rates have a high likelihood of following at least at some points during five years if that scenario happens, and discount rates have a high likelihood of following if that scenario happens, and that we will likely get some opportunities if that scenario happens.

-

10% inflation --->10% interest rates ---> 10% cap rates I'm saying 10% inflation should lead to 10% interest rates, which should lead to 10% cap rates. I understand the first arrow hasn't been happening even for 5% inflation because of intervention from Fed, and Fed calling it intermittent. However, I think either Fed will lose credibility or Fed will have to start admitting that it is not intermittent, and interest rates will likely move up.

-

It impacts a subset, but a big part of the economy that is measured by CPI. It also has downstream effects. Long-long term, I understand it will be mitigated by productivity increases. I'm saying it increases the probability of us seeing high inflation figures within the next few years.

-

@no_free_lunch, I understood your question, but my point is that even a single-time doubling of minimum wage is drastic, and hence I switched to the comparison between U.S. and Luxembourg. I am not claiming that minimum wage will continue to double all the time. Single-time doubling of minimum wage over 5 years results in 15% sustained inflation over five years in some goods/services. My point is if that 15% figure shows up even once in a wide range of goods/services, it will be drastic.

-

By cap rate is a function of NOI, I understand you mean cap rate = NOI/Price of CRE. In other words, Price of CRE = NOI / cap rate Value of CRE with $100K NOI with cap rate of 3%= $100K/3% = $3.333 million Let's say inflation hits 10% and NOI goes up 10% to $110K, and interest rates follow, and cap rates follow Value of CRE with $110K NOI with cap rate of 10% = $110K/10% = $1.111 million. I understand things won't be this drastic, but even if they are half as drastic, not great. I understand if you're saying you don't need to refinance or sell during that time, and can ride the inflation and hold, you might do fine. For that, you need long term mortgage. To be balanced, better to have some cash ready to also buy.

-

Yes, if you go to McDonald's in Luxembourg with high minimum wages, McChicken is more than double compared to U.S. Imagine mass market goods & services doubling in price in the U.S.

-

Once you start doubling minimum wages, everything starts almost doubling. Goods & services with labor as a big component almost double, e.g. haircuts, nannies, maid service, restaurant meals, construction costs, etc. Mass Goods & services that are consumed by all, where minimum price is determined by what lower-income folks can afford go up, e.g. fast-food prices double over time. Those geographically-bound workers will compete for the same restricted housing supply with a third of their fruits of labor, causing rents for those workers to double over time, unless effective supply increases due to geographically-mobile higher-income folks spreading out to bigger estates, far out water-view, etc., which is a possibility. So, maybe high-density rent doesn't double. Doubling over 5 years is 15% per year inflation. Even it that inflation figure shows up once in five years, it will be deadly.

-

I think the other source of inflation is minimum wage inflation. Unlike lumber, where increased supply will bring prices back down, we can't decrease wages back down.

-

Of course, you want cash taken out at low long-term interest rates, and in the long run that should do fine. I'm talking about how you invest that cash, some of which is taken out at low long-term interest rates. You could either just put it all in long-term holdings that will do well over the long run, or save some for taking opportunities that might arrive.

-

@no_free_lunch, I agree imminent inflation is not a 100% certain scenario, and thus you shouldn't hold 100% cash. The amount of cash or gold you hold should be based on what probability you think will holding that result in a win (p), how much is the expected increase in your investment (b), probability of your loss (q), and how much is the expected decrease in your investment (a), i.e. the Kelly Criterion, i.e. p/a - q/b. In the simplest form for even bets where a=b=1, that percentage weight reduces to p-q. Overall, here are the possibilities we're discussing: Scenario 1. Mild inflation in 3-4% range for 5 years (p1 =35%?) Stocks with pricing power and long-term duration debt bought at a reasonable price do ok with high certainty (Probability p1s = high) Oil does ok in medium term with high certainty if bought at bottom last year (p1o = high) Cash loses 16% to 22% value with high certainty over 5 years (p1cashWin= low, p1CashLoss = high; Amount of loss = 16-22%) Gold: cannot say with certainty what happens - could go down as low as what makes miners unprofitable like the bottoms it has hit in the past and gold could lose money (p1gLoss = Medium). Low certainty that Gold does well (p1gWin = low). Scenario 2. High inflation in 5-10% or higher range at some points in the next 5 years (p2= 65%?) High quality stocks with pricing power and long-term duration low debt with stock price that assumes high discount rate do ok over 5 years (p2shqrp = high certainty) but may dip and provide buying opportunities (p2shqrpCashWin = medium certainty event) High quality stocks whose price assumes low discount rate or have earnings way in the future, low quality stocks with short-term debt or high debt or without pricing power suffer badly and indexes provide great buying opportunities to buy with CASH and hold (p2sCashWin = high certainty event) Oil does well in medium term (p2oWin = high certainty) Gold: Might spike if retail investors get on the bandwagon (p2gWin = 60-70% range but not high certainty; however, amount of win could be high) To summarize, Gold: In high-inflation scenario, gold does well, but only with medium certainty, albeit high amount win. In low inflation scenario, gold could possibly lose a lot. Cash: In high-inflation scenario, cash does well also, and that too with high certainty to give opportunity to buy indexes. In low inflation scenario, loss is bound with high certainty. Thoughts on probabilities above?

-

Thanks @wabuffo. After BRK bought GOLD, I've been slowly warming up to the idea that having small amount of gold exposure might not be bad insurance to have as long as it is bought at a low enough price. I think one other factor we need to add above in determining price of a commodity is the speculation factor. Beyond price, I think we also need to look at what is the lowest price this commodity will trade at given its real needs, to figure out how much downside risk we are taking by buying it at a given price. Regarding stability, if products/services in the world were priced in gold, like oil was effectively priced in gold before 1970s inflation, we could have relied on gold's stability more. In today's world, if one wants to be prepared for S&P 500 bottom with very high certainty, wonder if cash might be more stable than gold.

-

I agree Crude is not a perfect inflation hedge also. That said if someone bought oil stocks at the bottom, those stocks could benefit from positive surprises from unexpected "bottlenecks". Also, on average, the price for crude will be determined by marginal cost of production of crude needed. So, if you could buy a producer that can produce below that cost, and buy at a time when crude was trading below that cost, it should work out ok during inflation as inflation should cause that marginal cost of production in general to go up and thus price of crude to go up. That said, I agree with you that unlike 1970s, oil and those oil stocks might not necessarily hit peak with high certainty this time when S&P 500 is hitting bottom due to inflation/interest rates.

-

I agree if interest rates hit 10%, REITS without 30-year mortgages will go down, and also CAP rates will track interest rates, lowering valuation of CRE.

-

Thanks @no_free_lunch, I couldn't find any REIT that could satisfy my criteria either. The best is probably to have 30-year mortgages on directly owned real estate. I agree it doesn't have be just REITs. Any entity with assets that don't need to be replaced at higher cost, i.e. "rights", that are cash-flowing well that can track at least inflation, trading at a reasonable EV/EBITDA ratio, and has long duration debt that is not too high relative to EBITDA, should do fine over the long run. I include spectrum as such a right as well. The best I could find here was VZ. However, 10% inflation per year will still take 7 years for prices to double, while 10% interest rates will increase cost of loans & discount rate immediately, potentially creating buying opportunity. So, I think it has to be balanced approach, where if the inflation/interest rates don't go too high, you do fine, and where if inflation/interest rates go high, you do well there too. For the scenario of inflation/interest rights going high, and being ready for a buying opportunity, I've also been trying to figure out what could hit high peak in that scenario when S&P 500 is hitting bottom. So far, I think the most certain way to take advantage of that bottom would be to have extra cash ready like BRK is holding. With alternatives, I like oil stocks the most for having some probability of hitting peak during S&P 500 bottom and doing ok also for low-inflation scenario. Gold is another possibility but I don't have conviction on that to do well also in the medium term possibility of us not hitting ultra-high inflation as currently it is trading at a price that doesn't have much downturn protection - best time to buy Gold protection to hold might have been to buy GLDM/GLD/IAU when gold was hitting bottom, or buy gold producers with lowest cost (sub-1000 cost/oz) when gold was trading below $1200. TLT put options would have to be timed perfectly to work well also - not high certainty scenario to get that timing prediction perfect. Any other ideas that will be high when S&P500 will bottom in event of high inflation, but will also not go down in case of low inflation? Looks like the only way to be certain to be ready for that bottom is to have some dry powder ready like BRK?

-

Which REIT is shareholder oriented enough to have (1) 30-year long mortgages and (2) doesn't have the culture to print shares to buy expensive real estate? If you don't have examples of REITs that satisfy both #1 and #2, how about examples of REITs that satisfy #1? If you don't have examples of #1, what's the REIT with longest average-weighted mortgage duration you've found?

-

I agree oil is a much better inflation hedge. That said the only thing we can predict with above 99% certainty with these commodities is that the price in the long run will be above the marginal production cost for the amount of supply needed to meet real needs. There are still times when the commodity price falls below that price during which the producers of commodity go on sale, and that is a good time to buy. With oil, that marginal production cost ranges anywhere from $30 to $60, or maybe higher at some time, and then longer term, when consumption goes down, marginal product cost could possibly go down eventually. We had some opportunities last year when it was trading below that medium term marginal production cost price of at least $30-60. Even today, it is not too far off from that. With oil, because some ownership is consolidated, there is possibility of positive surprises. With gold, the consumption needs for jewelry, tech, and industry are so small, that they could likely easily be met with marginal production cost of below $1000. It is currently trading far higher than that. So, there is little downside protection. There is a possibility of positive surprise here if many neural nets end up getting influenced by historical gold prices and end up pushing them up during high inflation or any other surprises. The probability of such a speculation is higher than probability I'd try to give to any meme stock speculation, but it is still similar-type speculation, except that the influence on human mind is much stronger from much more historical data. That said, that influence on human mind has gone down a lot since 1970s when we had just come off the gold standard, and there were fewer options for folks to speculate on during 1970s inflation. To diversify beyond oil, anything else folks have considered other than gold, TLT put options, banks, and to some extent, companies with pricing power, to protect against high inflation/interest-rates? Ideally something that would immediately go up if inflation/interest rates spike just when S&P 500 is bottoming so that one could then sell at peak to get into S&P 500 bottom. Something that will also not go down if inflation/interest rates don't spike.

-

Thanks wabuffo clarifying. I see where the disconnect is. GLDM sounds like it is an ETF composed of gold miners :-). However, it is not :-). Both GLD and GLDM are backed by physical gold itself. Both are created by State Street. The difference is that GLD has been around for a long time and provides liquidity for large institutional investors. For that, State Street continues to make them pay 0.4%. Because there was demand for lower expense ratio, State Street created another physical-gold-backed ETF with 0.18% expense ratio, especially to serve the needs of smaller investors that don't need to make huge purchases/sales that need higher liquidity. There are some other differences as well. Please see: https://www.ssga.com/us/en/institutional/etfs/funds/spdr-gold-shares-gld https://www.ssga.com/us/en/institutional/etfs/funds/spdr-gold-minisharessm-trust-gldm

-

Thanks @wabuffo, are you saying GLDM doesn't maintain a peg? Does that make a huge difference? For long term gold exposure, GLDM seems to have lower expenses at 0.18% vs. GLD's 0.40%. Any issues you see with GLDM? Looks like with miners you get amplification of changes in gold price, i.e. (price of gold - $1000 all-in production cost/oz) * Multiple. Have you looked into marginal production cost curve of gold? I think the ideal entry point would have been when gold price was close to marginal cost of production needed to supply jewelry/industrial/tech needs. Now, it is way higher than that, and somewhat speculative, no? Yes, marginal production cost curve should move as labor prices move up, but looks like marginal cost needed to supply those needs will still be much much lower than today's prices.