LearningMachine

-

Posts

1,829 -

Joined

-

Last visited

-

Days Won

6

Content Type

Profiles

Forums

Events

Everything posted by LearningMachine

-

Thanks @Cigarbutt, is there a link to it? I was trying to poke around the treasury website to find the report, but would appreciate if you have already figured out exactly which report. Looks like this report only has the count: https://fiscaldata.treasury.gov/datasets/savings-bonds-issues-redemptions-maturities-by-series/paper-savings-bonds-issues-redemptions-and-maturities-by-series. I wonder if that $180M figure is moving up a lot in November and December of 2021? Regarding reduction in excess money supply, I'm wondering if you are going to tell me I got it wrong, and I am happy to learn from your perspective. I was just interpreting it from the perspective of M1 definition includes checking accounts but not I-Bonds. So, when someone moves funds from their checking account to purchase I-Bonds, that should result in reduction of M1, and reduction in them blowing up that money on competing with other folks to raise prices on things. I'm sure it is not that simple, and someone might come and educate me on the plumbing of it, e.g., no, no, no, that money now goes into the treasury's account with the Fed, and that should also be part of M1, or maybe that it ends up resulting in Fed, Treasury or banking system having to do something in the plumbing that results in not reducing M1 :-).

-

Now that the inflation probability has finally materialized as expected, looking further out, how much of the excess M1/M2 supply do we think I-Bonds will be able to soak up and how long would that take? Any readily available link out there on total amount of I-Bonds outstanding? If 100 million folks could max out their $10K limit each year, it could soak up a trillion dollars a year. But, we probably won't get that many folks buying it that fast. I-Bonds were not available in 1971, and people had to wait for interest rates to go up before high yielding treasuries could soak up extra supply at that time. Has anyone's barber started talking about I-Bonds yet?

-

We may not be in a different situation when it comes to how much cash is losing value. However, we will be in a different situation when it comes to valuing stocks because cost of rollover debt will change, alternative investments for people will change, and discount rate will change immediately while price increases will take time to come through.

-

@KJP, interesting example of how low interest rates can result in extra supply, and in turn, lower prices (not inflation) for consumers in some sectors.

-

@KJP, I really like what you're saying here. This is also a risk for those buying cable companies. Imagine buying an asset with 20% down and 80% funded with debt, but then the asset value drops by 28.6% from $7K per subscriber to $5K per subscriber. Ouch, suddenly equity is underwater.

-

@Spekulatius, very well put. Also, thanks for sharing $SHEN. Interesting to see their cost per passing comparison. @Spekulatius, I haven't looked at the transcripts yet, but do you know how come their cost per passing is lower for fiber than cable? Also, do you know if fixed wireless cost per passing includes cost of spectrum? I'm assuming it does. That low $250-$350/passing number explains well why VZ is going after fixed wireless business. Given that VZ is doing the same things as SHEN for future growth, can get longer-term bonds at lower interest rates, has better brand recognition, better opportunity to pair with mobile and streaming bundle, why not go with VZ over SHEN? Because you don't want exposure to their mobile side of the business, and you want pure-play broadband? However, longer term, wouldn't it be better to have broadband in the same company as mobile? The same fixed wireless spectrum can be shared between wireless subscription and fixed wireless subscription as they generally get used at different times of day.

-

I agree with you that people buy speed, reliability and brand. As @Gregmal would say, there are somethings that are etched into the psyche of society that you can count on. When talking with folks in general, including non-technical folks, I've found that "fiber" has become a brand in itself that has been etched into their psyche to be superior in terms of reliability, speed, etc. and there is a big enough percentage of non-technical folks who would pick fiber over cable for the same price in a heartbeat. Also, regarding brand recognition, cable brands are known for lower customer satisfaction compared to nationwide-telco brands VZ and T. That type of lower customer-satisfaction brand recognition actually is negative when compared to someone with a more positive brand. Comcast's NPS is actually negative, that is, on average, their customers will go out of their way to tell family and friends to not get Comcast. If Comcast was in an industry where it was not the only game in town, it would be gone in no time. The only thing that has been saving it with negative NPS is that it has been the only game in town for a lot of people, until now.

-

I understand this group doesn't represent the general public, and has folks who are more sophisticated to understand the difference in reliability, upstream & downstream bandwidth, and latency between the different broadband options. That said, this group can also represent influencers who family and friends will look to for advice. So, it will be good to get opinion of this group to see if there is at least a small percentage who are willing to move away from their cable broadband when they have more options available for broadband.

-

You have to subtract liabilities (float, debt, etc.)

-

Interesting to see BRK trade in and out of CVX. I know Buffett has been looking at oil price for decades. I wonder if he keeps track of marginal production cost, and goes in when oil companies are priced assuming oil price below marginal production cost and gets out when oil companies are priced assuming oil price above that? Or, wonder if he is going in when he gets worried about inflation, and comes out when he is less worried? He has gone in and out of XOM multiple times before. If memory serves right, he also went into COP once, but then, had to sell at a loss because inflation didn't materialize and oil price fell a lot that time.

-

Thanks @KJP for sharing. Really appreciate it. The next paragraph after what you quoted from your source is also interesting :-):

-

How has the general market been doing in your area in terms of price/sqft, etc. for similar houses between Zillow's purchase date and now?

-

Buffett has not been a big fan of gold. That said, at any of the following moments in history, would it be have been easy to predict with certainty that if inflation were to happen, AISC of Gold was going to be eventually as high as $1000+ in 2021 at companies claiming to have the best gold mines (Barrick Gold, Newmont)?: August 1971: U.S. came off the Gold standard in August 1971, but Gold fell from $42.71 in August 1971 to $42.03 in September 1971. February 1974: U.S. inflation exceeds 10%. Gold price hits $151.22 January 1980: Gold hits peak of $677.97 Sep 1981: 10-year treasuries rate hits peak of 15.32%. June 1982:Gold drops to $314.79 Looking at it today, if inflation hits 10% per year for the next 10 years, i.e. costs multiply by 1.1^10=2.59, would AISC at miners also multiply by 2.59, and in turn, can we expect gold price to also go up at least that much? What is the probability that inflation could run that high for next 10 years, and that Fed will be slow in letting interest rates go up? If crypto crashes, what percentage of crypto investors run to gold? Some follow-up questions: What percentage of your portfolio are you putting in gold? How are you holding gold, e.g. GLD, GLDM, GOLD (Barrick Gold), or NEM (Newmont)? Gold price per oz: 10-year treasury rate:

-

@Spekulatius, @wabuffo, and anyone else putting more in Gold as the inflation prediction is starting to become a reality? What medium are folks using? Anyone consider GLDM now? Anyone considering GOLD (Barrick Gold)?

-

I think it is a matter of timing but eventually increase in size of desirable area to 60-90 minutes from city-center will show through. If interest rates are slow to move up, and builders are able to hit 2 million housing units per year sooner, that increased supply in increased size of desirable area will happen sooner. If interest rates move up faster, causing slowdown in demand, and in turn causing builders to not be able to hit 2 million housing units per year, it will slow down how fast the supply increases until builders can build profitably.

-

Foreign investors willing to buy U.S. dollar denominated long-duration treasuries and mortgage backed securities at low interest rates so far has been helping too, but agreed, even with that, it wouldn't be at current rates without Uncle Sam's purchases.

-

Thanks @ERICOPOLY. I found the following interesting at your link: The increases from 7.5% to 9.19% (22.5% increase) , and then to 11.20% (49% increase from 7.5% rate), are not as drastic as increases could be from 2.5% to 5.0% (double) or 7.5% (triple), or 10% (quadruple). I understand the mortgage payments don't go up exactly proportionally due to amortization component, but still the impact could be more devastating this time if interest rates were to follow inflation this time, both (1) because of the potentially bigger impact from interest rate increases from a much lower base, and (2) because of LTVs being possibly higher now making housing more of a financial asset dependent on interest rates similar to stocks. Now, add the (3) impact of increase in supply due to increase in size of desirable area to 60-90 minutes outside city centers as Zillow confirms at http://zillow.mediaroom.com/2021-09-14-Remote-Work-Will-Fuel-Housing-Demand-for-Years-to-Come. Supply increase in this bigger desirable area will take some time to materialize with inventory being listed as people come out of covid woodworks and new construction. Potentially, all three factors could come hit together.

-

http://zillow.mediaroom.com/2021-09-14-Remote-Work-Will-Fuel-Housing-Demand-for-Years-to-Come

-

Thanks KJP. Yes, we discussed it last year. Looks like you're offering chart of San Francisco housing prices as proof that remote work didn't have a substantial effect on demand for urban housing. Housing actually went up everywhere. Some would argue it went up more as a percentage in exurbs than in city centers. I think we are not fully done with impact of remote work yet. So far, we have been caught with emotional pent-up demand for more space, lowest inventories, construction rate not hitting 2 million housing units per year yet, remote-work policies slowly being put into place, people looking to their companies and colleagues' behavior for confirmation that remote work is here to stay, etc. https://fred.stlouisfed.org/series/MSACSR https://fred.stlouisfed.org/series/HOUST I'm not arguing that people won't have any desire for being close to cities. I'm saying some people will be willing to go farther out from their employers than they used to be. Before covid, in tech hubs, most desirable real estate was next to big tech employers. Now, I see people with families willing to drive much farther out from their employers for new construction, bigger lots, water, etc. Search radius for most desirable real estate for families has gone up from pi* 1^2 miles = pi square miles to something like pi * 30^2 miles = 900 pi square miles, or even pi * 50^2 miles = 2500 pi square miles. There are multiple good school districts in bigger areas, and I see people realizing schools get better in general where they move in big numbers for new construction. However, this huge increase in size of desirable area didn't have much impact on housing so far due to several reasons. As those reasons get addressed, I think this increase in size of desirable area will have an impact. The biggest thing we need to wait for is for new construction and inventories to come up in the bigger area.

-

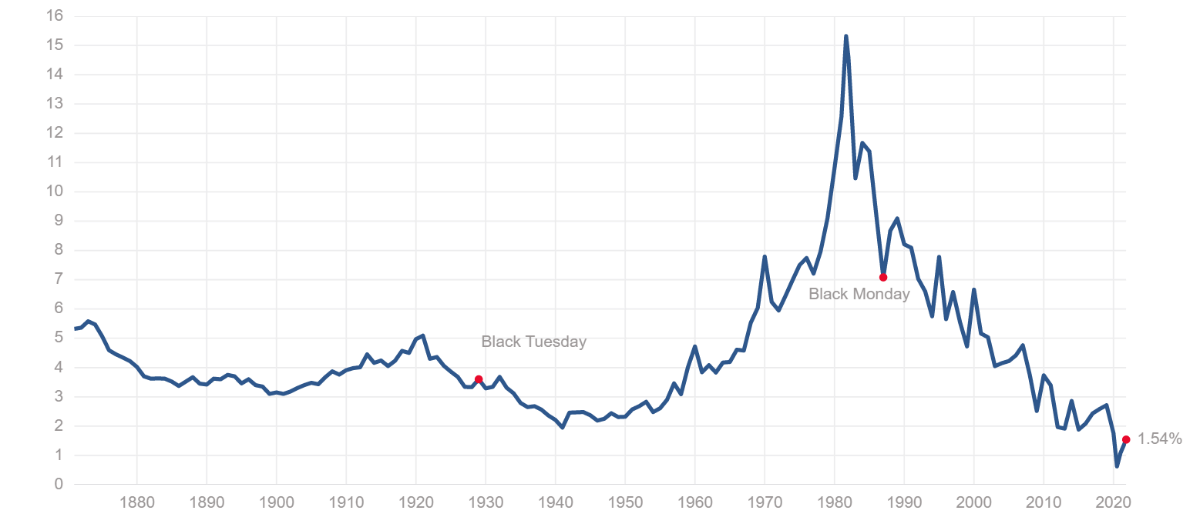

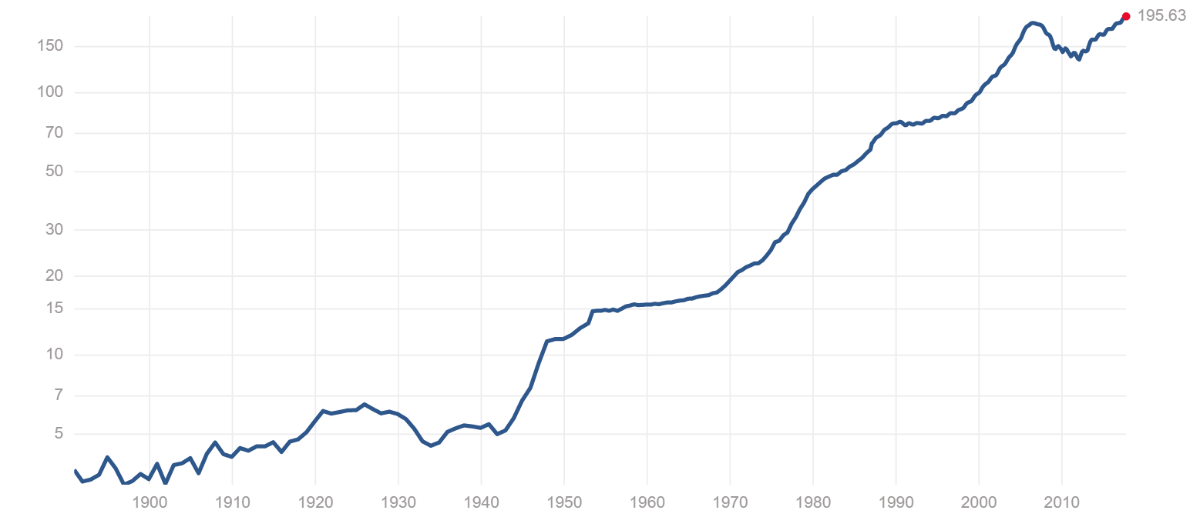

Thank you KJP for sharing. Very interesting to see that Average LTV ratio of mortgaged homeowners was much lower those days. That can partially explain that at that time, housing was not as much of a financial asset dependent on interest rates as it is today, and thus increase in interest rates didn't impact nominal price of housing as much those days as it impacted other financial assets, e.g. stocks, those days. However, it doesn't explain fully why nominal house prices didn't drop when interest rates went up in 1970s. For example, you see a spike in interest rates after 1974 and then again in early 1980s. However, there is no drop in nominal home prices at those times. https://www.multpl.com/10-year-treasury-rate: https://www.multpl.com/case-shiller-home-price-index (Nominal home prices): Wage growth doesn't explain it either as wages didn't double within a year of interest rate spikes.

-

Now, what if $2108 per month was max buyers could afford to pay before 10% inflation and 10% interest rates hit. After 10% inflation, say they could afford $2318. So, with 10% interest rate price would have to adjust for mortgage payment to be $2318. Why didn't the nominal price adjustment happen in 1970s when interest rates shot up?

-

Another way to show status for geographically freed folks could be that $500K waterfront lot instead. It is starting to happen. You will have to give it some time for supply to catch up and for people to hear others flaunting new construction, water views, etc. for others to follow to move out.

-

For some knowledge workers freed from geographical constraints, $500K waterfront is still cheaper and more desirable than $3-10M shack with no water views and issues created by density in some tech hubs.

-

Thanks, the reason I asked was to confirm that there is a limit to what percentage of their yearly income year-after-year people are willing to pay for something in restricted supply they want or need badly. The uppermost limit is 100% of income. Practically, it would have to be somewhat less. If mortgage payments double or triple, people can still only pay a certain percent of income. 10% increase in income due to inflation in first year wouldn't be able to afford doubling or tripling of mortgage payment for any buyers out there in such an environment, without a price drop. I understand folks holding with 30-year mortgages don't have to sell, but some have to always sell for reasons beyond their control. One thing I haven't been able to fully explain is why did the nominal home prices didn't fall even though inflation-adjusted prices fell, when interest rates shot up in 1970s and early 80s. Could it be that LTVs were low in general and housing wasn't really a financial asset equivalent dependent on interest rates like it is now? If LTV was equally high then, and percentage of income people were already paying was very high also, how did buyers find the money to be able to pay mortgage payments above a certain percent of their income when interest rates shot up? Maybe lenders didn't restrict that debt service payments had to be below certain percent of income? https://www.multpl.com/case-shiller-home-price-index https://www.multpl.com/case-shiller-home-price-index-inflation-adjusted https://www.multpl.com/10-year-treasury-rate

-

Well said. Now, software engineering can pay better not only in certain areas with restricted supply, but anywhere with plenty of desirable land with water views, acreage, etc.