gfp

-

Posts

5,347 -

Joined

-

Last visited

-

Days Won

10

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

Here is another one that might be interesting - this is a company that has gone down a fair bit recently and has insider buying at the current price. Digital Turbine, ticker: APPS. So far, this is 3 directors buying shares in the open market in a cluster. Not huge numbers, between $72,750 and $152,730 in value - at prices ranging from 48.50-50.91 / share. I saw this company written up in a fund letter and had never heard of them. I still can't understand exactly what they do or how they make their money, but they are profitable and growing quickly. They just completed 2 large acquisitions that should increase revenue considerably while only diluting share count by 15% or so. Directors have bought in the past at much lower prices and done very well on those purchases. Maybe this company isn't on my AT&T iPhone and that's why I can't figure out what it does / how it makes money. Who knows... But it's a standard setup on a volatile tech stock with a small cluster of open market purchases with directors' own money: http://openinsider.com/search?q=APPS

-

Here is a recent example - just filed. It has a connection with Fairfax and it is an open market purchase by the CEO. Also it is rare and usually a good sign when a CEO buys shares at a 52 week high: https://www.sec.gov/Archives/edgar/data/901819/000140810021000125/xslF345X03/wf-form4_162864041464230.xml

-

Outside of PCP, Berkshire’s MSR companies are mostly in the sweet spot in this economy. Trains are slammed, car dealerships, furniture, home building, building products - hell, even NetJets had to suspend new sales because they couldn’t keep up. Obviously year over year comps make it look even better.

-

It doesn't seem like the most important item to put in the headline, but he did slow the rate of share repurchases. $9 Billion -> $9 Billion -> $6.6 Billion -> $6 Billion

-

GEICO is certainly under-earning but that should be temporary. Life/Health Reinsurance is also putting up bad numbers. Berkshire has primary insurance subs and property casualty reinsurance shooting the lights out (especially on premium growth out of BH Specialty and MedPro), but Berkshire's insurance mix is much different from other insurers. You should expect to continue to see underwriting losses out of Retroactive and maybe also the periodic payment business. The AIG transaction alone is responsible for a lot of the retro losses that get reported. The long duration of that float is key.

-

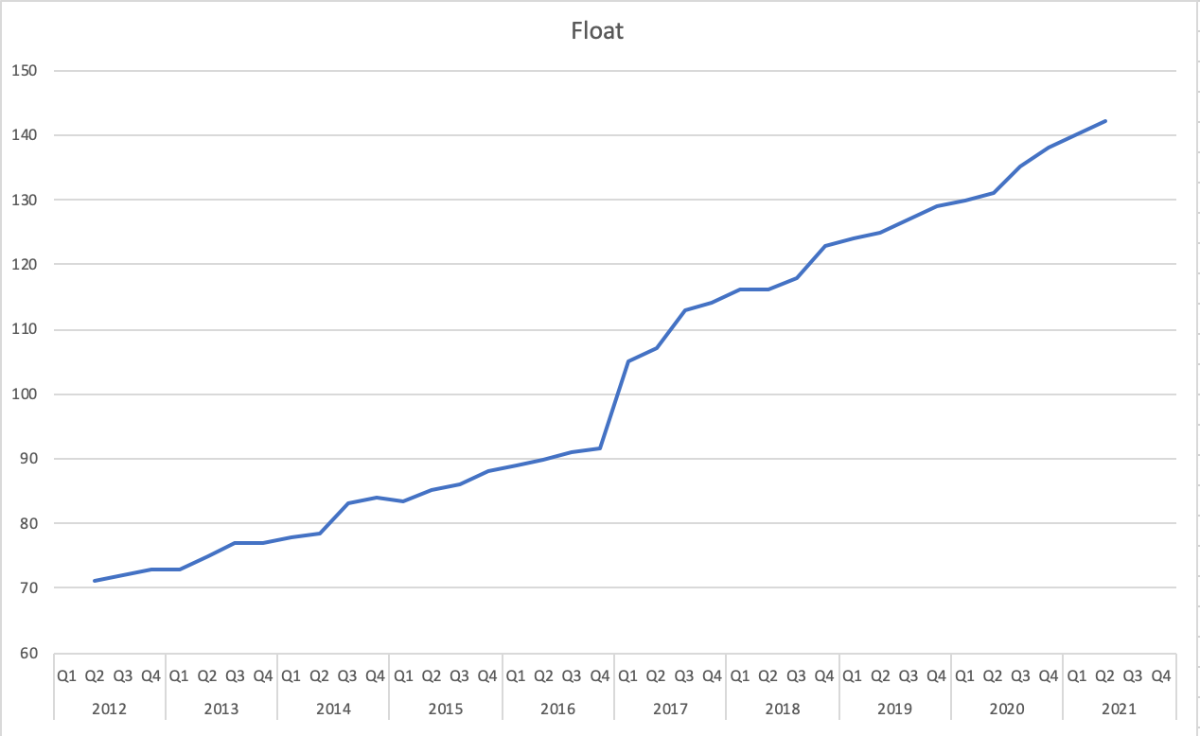

I wonder how Buffett thinks about the value of this $142 Billion balance sheet liability that is growing at a 4-8% annual clip... Surely he doesn't value it at negative $142B.

-

I agree on the gist of both of your comments (greg & wabuffo) but I wouldn't count on 5% being the number. The current run-rate is closer to 3.7% despite the trailing twelve month numbers looking like 5%. We haven't seen him repeat a $9 Billion repurchase quarter since Q3 and Q4 of 2020. I suppose he will increase the buying if the price declines and we don't really know what price he might decrease the repurchase rate.

-

The sooner you realize that you can't reliably predict the future of interest rates and stock indices the better off you will be. The S&P 500 hit an all time high today. It's a bull market until it isn't anymore. We could go parabolic on the upside or get a headline tomorrow about a new covid variant that kills people and evades vaccines. A cyber attack could shut down huge sections of the economy tomorrow. You can't predict the future so why try.

-

This one was a great heads up - Thanks Gregmal

-

They got the TGA balance down to $459 Billion - close enough and closer than I thought they would get https://fsapps.fiscal.treasury.gov/dts/files/21073000.pdf

-

Yes that is my understanding of it as well. No new cash invested at a higher valuation. It's a shadow way to subvert foreign ownership limits. Kind of like when Berkshire wasn't allowed to own more of MidAmerican Energy because of the Public Utility Holding Company rules. Berkshire owned some securities that could convert into very large ownership percentages only once it became legal. I think they were something like 10% income securities in the meantime. Would have to revisit. What is the point of limiting foreign ownership if government is going to allow deals like Fairfax's convertible preference shares? Seems like the violate the spirit of the rule, if not the letter.

-

Earnings announcement here: https://s1.q4cdn.com/579586326/files/doc_news/2021/July/FFH-2021-Q2-Press-Release-(Final).pdf

-

Hey ray, Insider purchases as a lead-generating tool for potential investments is something I have used for decades. If you look at insider purchases every day, over time you will quickly be able to see the meaningful ones. Sometimes there are clusters of someone buying every day for a while, filing every three days (like Dustin Moskovitz buying Asana. Or Chatham Asset management adding to FST after Tilman Fertitta sweetened the deal, etc.. - These are not recommendations, I don't own those stocks) I like setups like this recent bank de-mutualualization at William Penn Bankshares, WMPN. You get the de-mutual setup, which is very often combined with a discount to book value setup and the insider purchase setup. http://openinsider.com/search?q=wmpn Other stuff you will see every day and it won't mean much. Horizon Kinetics buys TPL every single day for instance. There are also fixed income traders that buy closed end fixed income funds regularly but you don't know the rest of their portfolio. Nick Swenson buys AIRT often, but he wants to maintain control so there might be more than just economic motives. Sometimes you get a nice fat pitch like Jamie Dimon buying a huge block of JPM and making it obvious for everyone. And Biglari. You will see Biglari using other people's money to buy BH and BH.A shares that he controls... Insider sales don't have the same utility. Unless its just egregious and obvious. At SAM, Jim Koch and his wife couldn't dump the shares fast enough. Also - there was one sale reported that did mark a bottom: Charlie Munger transferred a huge block of Berkshire shares to his children in exchange for a promissory note at basically the exact bottom of the '08 crash. Estate planning at its finest. Find a site you like the format of and start looking every day. You will soon see what stands out and what is just noise. edit: I forgot to mention, since you asked how to differentiate between option exercise, grants, etc, vs actual honest to goodness open market purchases - its helpful to look immediately at the price per share paid. If its a weird number like 13.47 and the filing shows that to be the average of a bunch of trades, you've probably got a real purchase. If it's 10 different insiders all buying exactly at $15.00, it probably isn't. And if the price is way different than the current market price it is either 1.) a typo, 2.) a delayed filing that is way overdue, or 3.) not a real open market purchase.

-

Yeah - the linked report from Zoltan looked like he was using $450 Billion as his target as well. I've been assuming they only had to draw it down to $450 Billion or so.

-

Update on what the 3G principals are up to recently - They have seeded a new type of activist fund managed by Munib Islam, who ran activist campaigns at Third Point for quite a while. LTS One is the name of the new fund, no outside money so far. https://www.reuters.com/business/exclusive-3g-founders-launch-investment-partnership-with-former-third-point-co-2021-07-27/

-

I saw this Moody's report on Pilot Flying J's current planned $3.5 Billion bond offering and thought some here might find it interesting. Following this deal, Berkshire will own 80% of Pilot Flying J. Certainly, Berkshire will show a lot more revenue once it consolidates Pilot Flying J, since revenues were $27 Billion last year. The report also mentions that Pilot Flying J will spend around half a billion dollars this year on expansion and acquisitions. Report attached as a PDF Rating Action - Moodys-assigns-a-Ba1-to-Pilot-Travel-Centers-planned-term-loan-B-Ba1-CFR-uncha... - 19Jul21.pdf

-

Yes, Scott Fetzer owns a bunch of small to medium sized companies. Utility bodies for trucks, pumps, Ginsu, electric motors - it's interesting to peruse the current mini-conglomerate's holdings - https://scottfetzer.com/brand-portfolio/ Seems like most of those businesses would fit fine inside Marmon, but maybe you don't take a CEO's kingdom away from him until he retires on his own.

-

Untold Buffett/Munger/Berkshire Stories

gfp replied to longterminvestor's topic in Berkshire Hathaway

Thanks for that! The Nick Brady (treasury sec during Solomon scandal) story was one I hadn't heard before (15:45 mark, really 16:10 onwards) -

I mean I think we still have a couple at the family farm? No idea what they power but nothing important. Where I live it isn't windy but if I wanted to live somewhere completely off grid and it was often windy but not usually sunny, I would consider wind turbines to feed into the battery system (in addition to solar). If it was reliably sunny, it would probably make more sense to use only solar+battery storage. My personal residence has enough solar to power the entire house but we have a very favorable net-metering deal (we sell our excess power at the same retail rate they sell us power for) so we have never used battery storage.

-

Also, as a reminder, Pilot Flying J paid out a non-recurring $849 million distribution to Berkshire in Q1, with Berkshire owning 38.6% at that time. That indicates a $2.2 Billion total special dividend out of Pilot Flying J in Q1 of this year. Now they are refinancing some of that and accelerating the timetable of Berkshire going to 80%. The Haslams are going to be flush, having already received $1.1 Billion in the Q1 distribution. Sounds like the Call family will be selling out completely with this deal.

-

Thanks for posting. This was always the plan but it looks like they moved up the date by a couple years to take advantage of the current cost of money for corporate borrowers. The Haslams will definitely benefit from the Berkshire Halo on the cost of this debt.

-

Hey wabuffo - thanks for all your educational posts on this. It's been interesting to follow along. The TGA balance seems to be back on track, declining most days here in July. I noticed this CNBC article today, where only one of the 'experts' citied vague 'technical factors' as a contributor. Daily statement - https://fsapps.fiscal.treasury.gov/dts/issues Wednesday's balance down to $657.542 Billion https://fsapps.fiscal.treasury.gov/dts/files/21071400.pdf https://www.cnbc.com/2021/07/16/the-mystifying-bond-market-behavior-could-last-all-summer.html

-

FTC statement on the pipeline deal termination: https://www.ftc.gov/news-events/press-releases/2021/07/statement-regarding-berkshire-hathaway-energys-termination

-

It does make you wonder if merger approvals will be a lot more difficult for BRK Energy going forward.

-

https://news.dominionenergy.com/2021-07-12-Dominion-Energy-and-Berkshire-Hathaway-Energy-Agree-to-Terminate-Sale-of-Questar-Pipelines-Dominion-Energy-Commencing-Competitive-Sale-Process Berkshire - Dominion deal for Questar Pipelines has been called off. Uncertainty around FTC antitrust approval given as reason.