gfp

-

Posts

8,121 -

Joined

-

Last visited

-

Days Won

20

Content Type

Profiles

Forums

Events

Everything posted by gfp

-

From the conference call they are predicting Milton losses "within the cat margin" and not having much of an affect on the expected combined ratio for Q4. They mentioned claims are coming in slow so it is still uncertain but obviously a much better outcome than the direct hit on Tampa they had modeled. For "cat margin" they mentioned they have been absorbing about $1 Billion of cat losses annually, maybe 5 combined ratio points Marval Guru fund 22% annualized over the last 5 years confirmed on the call

-

I mean, it's not every quarter that Prem offers you $300 million of his stock

-

-

-

Q3 results press release - https://www.globenewswire.com/news-release/2024/10/31/2973090/0/en/Fairfax-India-Holdings-Corporation-Third-Quarter-Financial-Results.html

-

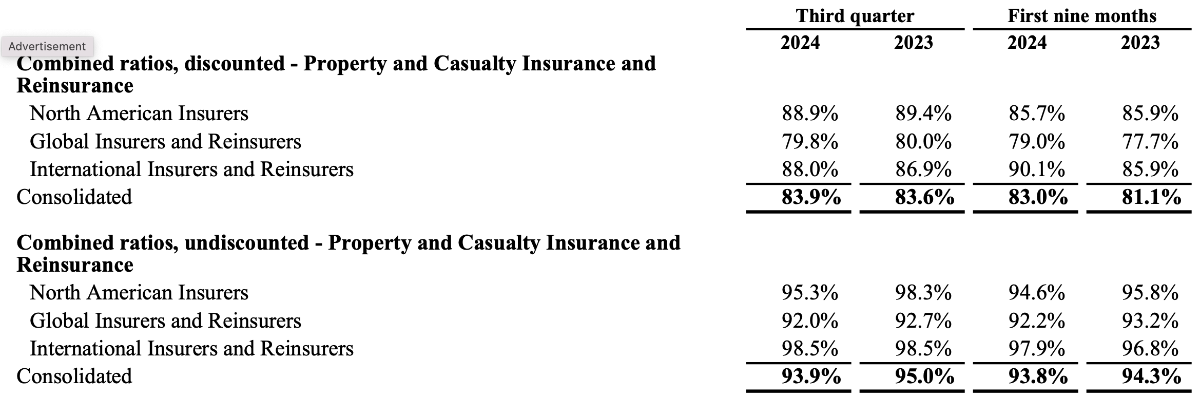

press release PDF here: https://www.fairfax.ca/wp-content/uploads/2024/10/2024_10_October_31-PRFFH-Q3-2024-Press-Release-Final.pdf Q3 report PDF here: https://www.fairfax.ca/wp-content/uploads/2024/10/2024_10_October_31-FFH-2024-Q3-Interim-Report-Final.pdf https://www.globenewswire.com/en/news-release/2024/10/31/2973087/0/en/Fairfax-Financial-Holdings-Limited-Financial-Results-for-the-Third-Quarter.html "Our underwriting performance in the third quarter of 2024 was outstanding, with our property and casualty insurance and reinsurance companies reporting a consolidated combined ratio of 93.9% and consolidated underwriting profit of $389.7 million, on an undiscounted basis, despite higher current period catastrophe losses of $434.5 million. " "At September 30, 2024 there were 21,990,603 common shares effectively outstanding." " The holding company expects to continue to receive dividends from its insurance and reinsurance subsidiaries, which totaled $728.1 for the nine months ended September 30, 2024, of a maximum $3,002.8 available in 2024." 1.2x unadjusted bvps ?? - do we really want the optics of the company investing $100m into Ben Watsa's fund? Seems unnecessary

-

My wife and I did that whole golden triangle area by motorcycle for several months in 2009-2010. It was so much fun up there. There is a road that goes right along the Myanmar border and it seemed pretty porous with people popping out from little holes in the bushes and disappearing into little holes. Several checkpoints along the way but that was a long time ago

-

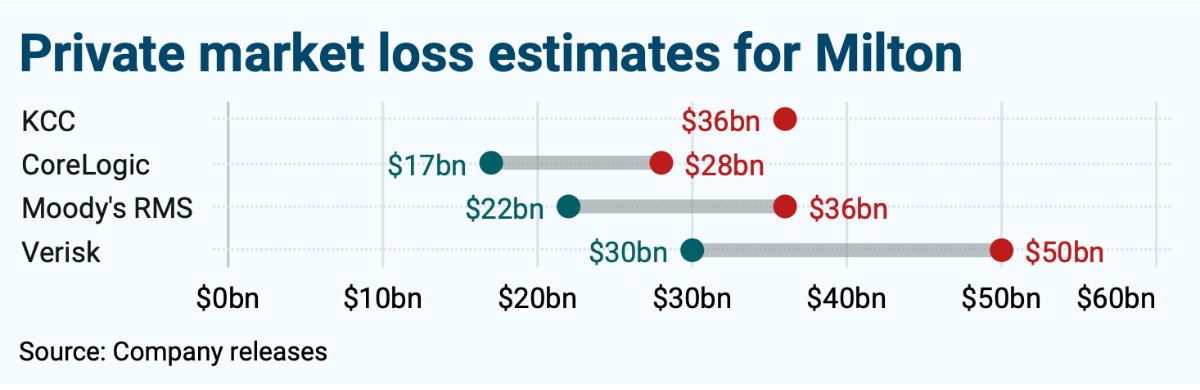

Here are some private insurance loss estimates from Milton - quite a range of outcomes. As always, keep in mind that a lot of the flood losses shown on television are not covered by private insurance. There will be substantial commercial insurance losses.

-

If a contractor is offering $4k discount for physical cash payment they are most likely defrauding their workers comp carrier as the primarily motivation. (I’m sure income tax avoidance is also a factor) Those carriers like to look at the bank statements.

-

I wouldn't read too much into a one month bond sell-off.

-

Here is today's newsletter out of the Baden-Baden conference of international reinsurers for those interested in more color (no paywall) https://pdf.static.prod.wbm.infomaker.io/c80c8f7a-cdbf-57a6-9364-adb3617297fc?utm_source=listrak&utm_medium=email&utm_term=Download+issue+three%3a+22+October&utm_campaign=Welcome+to+our+Baden-Baden+Day+Three+edition%3a+Tuesday+22+October

-

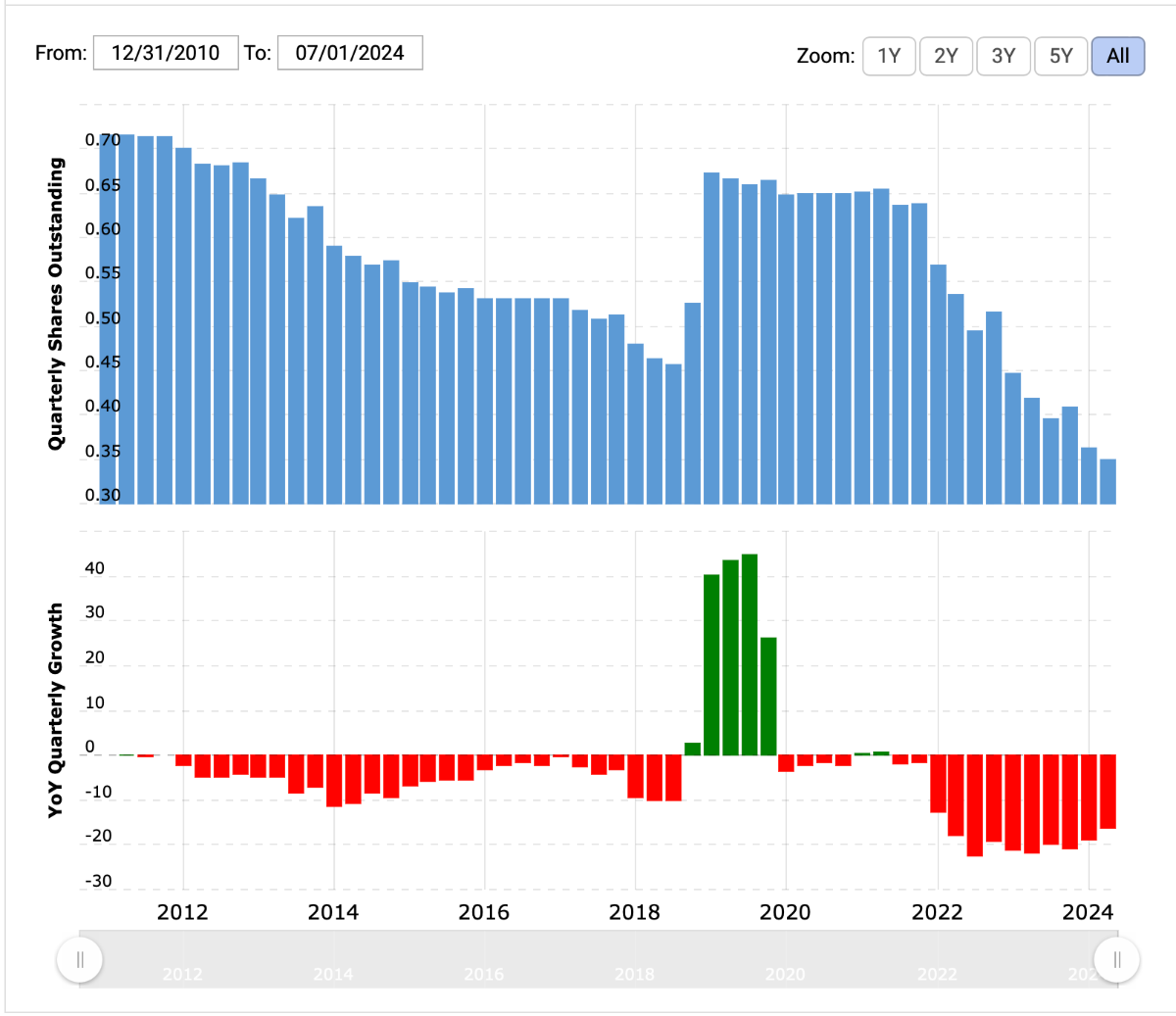

This chart does an even better job of showing the history of repurchase activity including the share issuance from the large Andeavor acquisition/merger in 2018

-

Back from Japan finally and going to close out this TLT short since it was always just a seasonal pattern trade. I suppose Trump win odds going up could push long yields up some more but I'm out. The trade worked out as expected

-

Interesting news! I'm in Japan so just seeing this now as I wake up. I think Abel was paid a premium price for his shares in order to take cash instead of the BRK.A stock he could have exchanged for under his shareholders agreement - so I think the story isn't really that BHE declined in value by 45% on the wildfire liabilities. RationalWalk makes a good point that there was a deal with Scott family interests at around $50 billion in 2020. Berkshire didn't use any of its own cash to do this deal! BYD sales proceeds, cash on hand at BHE and a debt swap covered most of the deal in the form of a repurchase at the BHE level. The remaining minority shares (which benefitted form the repurchase and became more potent) were a straight tax-deferred equity swap.

-

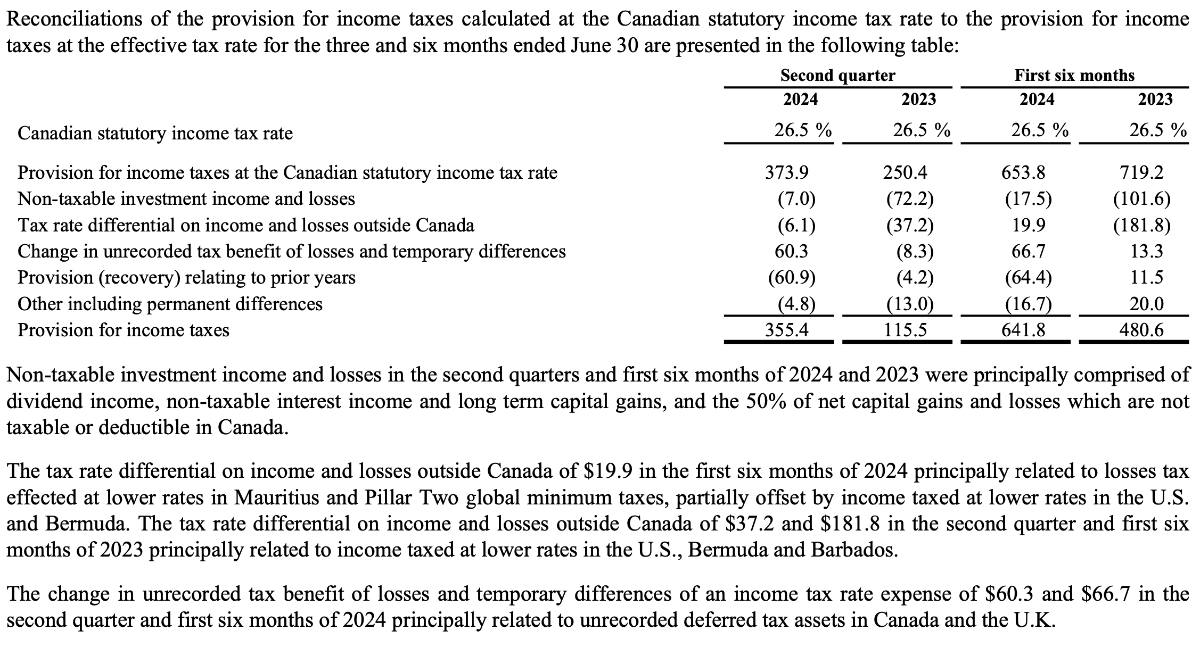

Just remember that what someone running for president puts on their website has little connection to 1) the actual powers of the presidency and 2) what will happen if they are elected. If Joe and Kamala wanted 28% corporate taxes and a 4% buyback tax why aren't they doing that now? Because they can't. POTUS doesn't get to make these types of decisions so it doesn't matter what you put out there. If you have a view on the composition of each house of congress then maybe you can game out something that could actually pass that she would sign (if she is elected, still an open question). Also, since this was a Fairfax specific question originally, remember that Fairfax is a Canadian company, with subsidiaries in multiple tax jurisdictions from Bermuda, Mauritius, the UK, and the United States (and many many others). Fairfax's actual cash tax rate is complicated and different forms of income in different jurisdictions are taxed differently. Fairfax Financial is not like Berkshire with a large deferred capital gain tax liability and a fairly pure USA tax jurisdiction. I still hope somebody asks on one of the conference calls if gains from the total return swaps Fairfax holds on their own shares are tax-free. In the United States, transactions in an issuers own stock are not taxable but this is Canada and these are derivatives so I have no idea what the treatment is. I guess I should just email them and ask. Below is one quarter of FFH tax complications - and cash taxes paid will differ from this substantially

-

We are all in different countries with different rules. But generally in practice, undeclared precious metals, art, jewelry and furniture / antiques is a way that wealth is passed confidentially to the next generation. Art is particularly subjective to value. What the rules say and what is generally done in practice are different things and I have no idea what the official rules or tax rates are outside the USA. I assume Jaygo is in Canada. In the United States we currently have a decently high lifetime exemption to gift taxes (which may expire / be reduced) so there are a lot of ways to get assets legally out of your estate - confidentially or on the books - and there has always been a lot of subjective valuation of private assets - illiquidity discounts, absence of an observable market, etc. In my experience the problem with physical gold is that true gold bugs tend to be conspiracy minded old men buying it and hiding it on their property and if they don't map it out properly and then they lose their marbles, they lose the gold, and the next generation has no idea where it might be or how much should be out there. Some gold is fine if it makes you feel better or safer. It's never going to be a good investment. It certainly has new-fangled competition. I prefer a valuable artwork passed down that I can enjoy every day but not everybody has the same taste and a small fraction of the art market is actually investment caliber.

-

I don’t think the Trump corporate tax rate cuts expire. Congress would have to do something

-

You could invest in the fuel itself through a physical uranium vehicle like Sprott's U.U in Canada or Yellow Cake. (sometimes the Sprott ticker is listed as U.UT). There is also an ETF with the symbol URA that owns some Uranium related things.

-

My understanding is if Fairfax entities "win" the deal for IDBI, CSB will have to be merged into IDBI with the IDBI "identity" being preserved.

-

they call it sulfuryl fluoride I think.

-

Anecdotally, it would seem to me like the Terminix business would benefit from the US market for existing home re-sales becoming less frozen, more active. Home inspections are a big driver of Terminix sales where I live. In my market there are only two companies with the tents to fumigate for dry wood termites. Terminix and House Call. Everyone else subcontracts to one of those two.

-

yes, after decades without a single claim we were sued by a former tenant for a slip and fall and had a Hurricane peel our solar panel covered asphalt shingle roof off. USAA was great through both experiences.

-

Welcome! Long-time happy USAA customer here. Not only can you pay monthly for no extra cost, but you can pay with a rewards credit card for no extra cost! Free flights for all

-

Have Federal Reserve rate cutting campaigns resulted in higher multiples in the past? I haven't had that experience in my (admittedly short) 24-year career. I'm fine with being surprised to the upside.

-

I don’t think the potential IDBI bank deal is for $10 billion USD. It is not the entire company that is being offered. good to have some friends with capital when a deal comes along. Hey prem, who ya got?