Dinar

-

Posts

1,840 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

Forums

Events

Posts posted by Dinar

-

-

@ValueArb, if you do not mind sharing, what is roughly the commission schedule for Robotti and Caldwell Sutter or whoever you use? Thank you

-

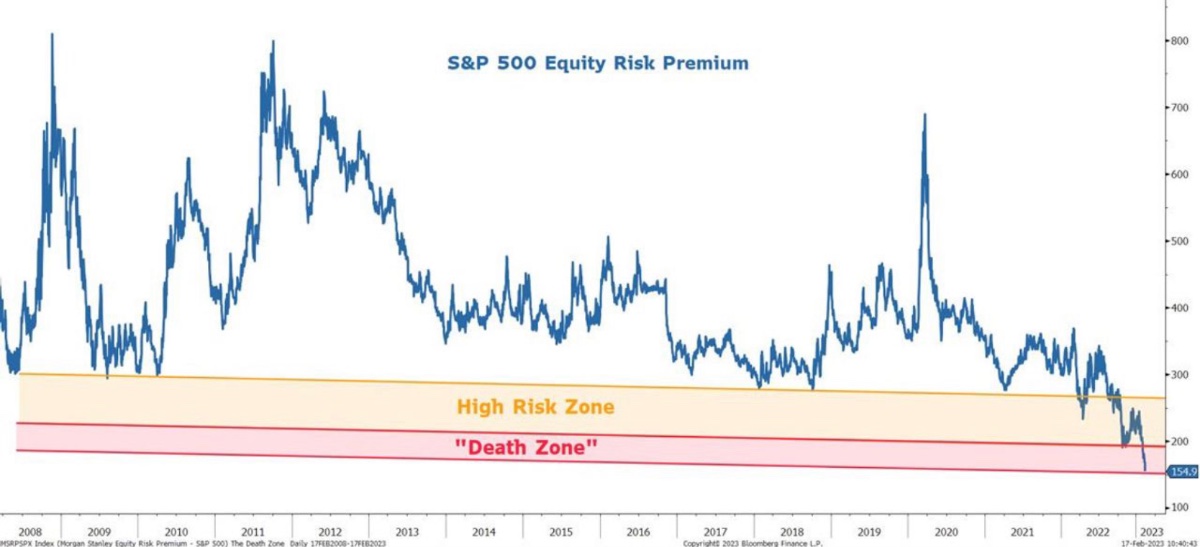

28 minutes ago, mattee2264 said:

To add another point to the equity risk premium discussion: the bond yield is the bird in the hand while the birds in the bush are uncertain. Even the current earnings may well disappoint. So if you think you are getting a 5% earnings yield and earnings fall as they are prone to do during a recession you may well be disappointed and part of the reason for demanding a risk premium is to insure against such possibilities.

That's why risk premium exists, the point is that it should be calculated properly rather than omitting most of the return that comes from owning equities - earnings growth over time.

-

48 minutes ago, changegonnacome said:

Pretty much my thoughts about where we are right now - when the pause/pivot delusion unwinds it’s gonna be interesting to watch.

If this guy computes equity risk premium as earnings yield - bond yield, he is incompetent and is not fit to come close to the stock market. Any equity risk premium that does not take into account future growth and capital that is required to provide is not worth the paper it is printed on.

-

Incredible. Instead of welcoming these educated, hard working people who greatly suffered, our government is keeping them in limbo, and potentially deporting them to their devastated country. Probably the only time in my life that I wished Carter was President. Although he did deregulate the airlines and railroads, so he certainly helped the country in that regard.

-

30 minutes ago, james22 said:

Seriously?

Yes, Russia has been a paper tiger for decades. By the way, how did you get your estimate of Pentagon spending $100-150bn per annum on the Russian threat?

I would frankly worry more about China, North Korea, and Islamic terrorists than Putin and his crew of incompetent buffoons

-

10 hours ago, james22 said:

US defense budget $715B.

Probably $100-150B is devoted to the Russian threat.

At a one-time cost of only $40B so far (another $38B planned 2023) aid to Ukraine is fantastically inexpensive to significantly degrade that threat for a meaningful time.

(The real cost is far less than $40B, most systems provided being older generations pulled from storage.)

For perspective, the US spent $115B/year for 20 years ($2.3T total) in Afghanistan (all for naught).

All without putting American lives at risk, there's no reason for the US to end this.Why would we devote anything to the Russian threat? They cannot defeat a country with 1/3 of the population and may be 1/5 the wealth, how could Russia be a threat to the US?

-

16 minutes ago, fareastwarriors said:

Why CNI or CP and not the others?

They have volume growth and will continue to have it, while others do not

-

36 minutes ago, RedLion said:

New position in UNP. Been wanting to invest in the railroads for several years and been waiting for a good entry point. I feel like $200 is an OK entry point, but I will look for opportunities to add.

Why UNP and not say CNI or CP? (I am long CNI & CP, but not other rails)

-

29 minutes ago, Viking said:

Here in Canada, a reasonably large subset of the population carries lots of debt (mortgages and LOC) thanks to our housing bubble. Lots of people own multiple properties with big mortgages (that were already cash flow negative at historically low interest rates). Most of this debt is variable, especially if interest rates stay high for years (even 20% of those 5 year fixed mortgages come due every year).

The real estate bubble has also created a mental rental market: here in Vancouver it is not uncommon to pay C$1,500-$1,700/month for a one bedroom and $2,800-$3,000 for a two bedroom - if you can find one (crazy low vacancy rate). Landlords with mortgages are going to need big increases in rental rates given their mortgage costs are going through the roof.

The learning is you do not want to blow a housing bubble because it usually causes big problems for years when it corrects. The US learned its lesson in 2008-2010. China is in even worse shape than Canada.

The Bank of Canada is really boxed in. Their answer is to stop rate hikes. Even in the face of high inflation (Canada has lots of very large public sector unions) and a very tight labour market. Government spending looks like it is accelerating.

No idea how it plays out here. Super happy i have no debt.

Man, that's low. How can I move to Vancouver? Nice two bedroom in NYC is at least USD 8K in Manhattan (10K+ CAD), and as much in nice neighborhoods in Brooklyn.

-

2 hours ago, changegonnacome said:

Yeah agree on the existential piece.....I'm just considering various levers they could pull.........pushing harder on the energy piece as a strategic tool to try to tip 'the west' back into an inflationary nightmare and/or recession......such that political support waivers is an interesting card Putin has left to play.......Europe got away with a warm winter/LNG purchases worked & US got to draw down SPR.......attention now turns to winter late-2023/24......and what tricks Vlad has up his sleeves & what the climate might serve up next winter

What makes you think that there is political support for Ukraine in France, Italy, UK, US, et all? Have the people been polled? Just because Biden was on Ukraine's payroll does not meant US public supports the war and the 50-100bn that was given to Ukraine. Do you really think that a typical family in the US would willingly give up a $1000 for Ukraine, let alone several thousand more that Ukraine is asking for? Similarly, I doubt that the public in Europe west of Poland/Czech Republic actually supports Ukraine despite what those leaders say/do.

Does the west actually have the ability to supply ammunition and the weapons that Ukraine needs/requests? When the entire Western Europe has 1000 battle ready tanks... When Ukraine fires more shells in a month than the US produces in a year?

Yes, the war clearly is very unpopular in Russia, but will that stop Putin & co?

In the long run, Russia has the advantage, and that's why once its nose was bloodied, the smart thing was to try to get a peace agreement or an armistice, instead we hear warmongers calling for Crimea returned to Kiev. The smart player knows when to hold and when to fold.

I disagree that the war or Ukraine are existential to Russia. I do not agree with Zeihan's point of view. Where are the new Panzer divisions going to come from? Germany? France? Give me a break! And the threat is far likelier to come from the East - China or South - Iran/Pakistan/ than from Germany or Poland.

-

@Gregmal, are you headed to the ST Joe area? Why do you prefer that to say Boca Raton? Thank you.

-

I got solicited by Fidelity the other day for a private real estate fund, the first time that this has happened in two decades even though I have had roughly the same amount of money there for a decade plus.

-

1 hour ago, thepupil said:

This discussion bring up the idea of time horizon. In truth, I don’t know my time horizon. 7-10 years ago, I’d have told you it was 5 decades, but then I plowed a large portion of my accessible net worth into a down payment on a house a few year a ago . So that money was thought of as 50 year money but was actually 5 year money. Maybe I should have invested more conservatively (though that would have been a worse result). Right now if I knew I wanted to work 3 more decades, I’d know my time horizon was super long. If I want to work 5 more years or 3 and start something entrepreneurial, my time horizon is not nearly as long. I think once one reaches a certain level of wealth / income from other sources, one doesn’t really care about drawdowns or volatility, but before then, volatility matters. Before you have “f you” money, before you know what path you’ll take, if there’s a chance you want to access your money for whatever reason before “many years from now”, you care about drawdowns and your time horizon is probably not as long as you think.

I don’t have super strong or well

formed views here but I don’t think it’s as simple as “young = long time horizon”

also when you’re young and have little money, new money is huge percentage of portfolio. Once you have a little scratch, you can’t as easily correct mistakes / invest into drawdowns with new money. $100k/year of savings is more meaningful to a $100k portfolio vs a $1mm or $2mm, so I think drawdown sensitivity increases as you get wealthier, then decreases again if you have so much that you can live well at very low withdrawal rate.

I thought I had F you money, but then I got married....

-

2 hours ago, KJP said:

Some things don't change much. That data series appears to go back almost 50 years to January 1976. Here are the bottom 10 states in labor force participation then and now:

Jan 1976 [For context, national was 61.3%]

West Virginia - 51.7%

Florida - 54.6% [Dec. 2022: 59.6% -- surprising to me given the number of retirees]

Louisiana - 55.7%

Alabama - 55.9%

Arkansas - 56.3%

Mississippi - 57.5%

New York - 57.6% [60.1%]

Pennsylvania - 57.6% [61.6%]

Tennessee - 58%

Arizona - 58.5% [61.4%]

Dec 2022 [National was 62.3%]

Mississippi - 54.1%

West Virginia - 54.2%

New Mexico - 55.8% [Jan 1976: 59.3%]

South Carolina - 55.9% [64.3% -- huge decline. Loss of textile manufacturing with insufficient new industry or increase in retirees?]

Arkansas - 56.2%

Alabama - 56.8%

Kentucky - 57.2% [59.5%]

Maine - 57.5% [60.6%]

Tennessee - 58.5%

Louisiana - 58.5%

West Virginia, Mississippi, Alabama, Louisiana, Arkansas, and Tennessee make both lists, and New Mexico and Kentucky nearly did. So whatever the underlying causes are for relatively low labor force participation in those states, they appear to go back a long time.

Yeah, and it is cultural! There is a reason why Chinese thrive in every country they are in! Culture matters and trumps almost everything!

-

4 hours ago, Spekulatius said:

The real problem with labor force participation is in the south:

https://fred.stlouisfed.org/release/tables?rid=446&eid=784070

Alabama, Arkansas, Kentucky, South Carolina, West Virginia, Mississippi .

All MAGA land.

The only Blue state coming close is Maine

Spek, I am not sure about the accuracy of the statistics that you cited. In NY, around 40% of the population if I am not mistaken is on Medicaid. Seems to me NY has a problem with labor force participation, no? In California, 33% are on Medicaid, and 55% of births are to women on Medicaid. Given that someone who works 40 hours per week, will enjoy income north of $40K a year in NY or California, something tells me that quite a few people are not working.

Also, if my wife is not working and is at home raising our three children, she is not participating in the labor force. If my wife works and we hire a nanny, then she is participating. That could easily account for the difference in labor force participation.

-

28 minutes ago, SHDL said:

Yes, I always feel a bit nervous about them. Hopefully the Fed's stress tests are reliable enough and they won't do anything so reckless as to topple the money center banks but you never know for sure. SCHW is technically a bank with a somewhat different risk/return profile - I have some just as a diversifier.

Well, there is an accounting concept held to maturity (Spek & others discussed it before.) Basically, it means that if bank plans to hold security to maturity, it does not have to mark it to market. So when bonds go down 40%, the balance sheet does not reflect this. While the Fed may not shut the bank down, the loss will manifest itself through the income statement overtime due to much lower net interest margins.

-

15 minutes ago, SHDL said:

I'm overweight some banks/insurers for this reason. But it's not like I'm looking to 2x in 12 months or anything.

If I had stronger conviction and was a professinoal macro trader I would consider trading US treasury futures or similar.

Be careful with banks, some may be insolvent due to collapse in bond prices

-

1 hour ago, Jaygo said:

Guys if you want to lower inflation go produce something that your neighbor needs. We have higher inflation now because people are lazy as hell and just sit around with their phones or push paper around. The government condones this shit for some reason. The last decade we had low inflation because poor nations were working their asses off for us. That stopped during CoVid. It is starting back up and inflation will drop.

there is a video of a shirtless roughneck covered in drill mud working an oil rig. That bad ass hombre is the solution to inflation not typing on a forum or trading stocks back and forth with each other.

sorry guys but if you are not part of the solution your part of the problem. Myself included. Look around society. Most people do not produce shit.

also low interest rates should reduce inflation in a healthy free economy by allowing for increased production of goods. I’m hungover and am really part of the problem today. Sorry for the cussing .

The best way to lower inflation is to increase labor supply. To do that, you need to create incentives to work. So, a) gut welfare and social programs; b) cut marginal tax rates - in NYC they approach 60%

-

Bought Diageo today.

-

@thepupil, what's the best way to play CLO AAA? Thank you.

-

@Castanza, do not debate. Anyone who says anything rational here is immediately called a Putin apologist, and a pro-Russian jerk. One can be sympathetic to the Ukrainian cause and abhor Putin & Russian invasion, while being realistic about vulnerabilities of both sides, however too many people here cannot think rationally about this war.

-

-

solution seems to be to gut welfare, then people have to work

-

Spek, anecdotal evidence points to recession. Car repossessions increasing sharply, Diageo reporting volume declines in North America, massive lay-offs across the board, real estate is down - so massive layoffs or declines in employment/income (mortgage brokers, construction workers, real estate agents.) Crypto wealth destruction is insane, and a lot of people also worked in that field.

Railroads

in General Discussion

Posted

@Spekulatius, when you look at CP, you need to adjust for what will be close to two billion in synergies with KSU once the deal closes, and the fact that KSU has been growing volumes in low single digit per year. Canadian railroads - both CP & CNI can probably grow volumes at 1% per annum, layer in price = inflation + 0.5-1% per annum, possibilities of additional costs cuts thanks to technology, and then they do not look expensive anymore, at least to me.