Dinar

-

Posts

1,840 -

Joined

-

Last visited

-

Days Won

1

Content Type

Profiles

Forums

Events

Posts posted by Dinar

-

-

15 minutes ago, Ross812 said:

In Georgia the average crew member at MCD makes $12.09 in New Jersey its $13.29. I'd say it not government programs. In NJ median income is 39k versus 30k in GA; it might just be typical economics. MCD charges what the market will bear.

Would you mind sharing the source of the data? The reason that I am surprised is that I was told by an ice cream shop operator in Bergen county (NJ) that he has to pay $20 per hour to attract teen-age staff to work.

-

6 minutes ago, Gregmal said:

I marvel at this even within the States. In NJ its $10 for a Big Mac meal and yea like $8 for breakfast. The dollar menu is now the $3 each menu. In Georgia or Tennessee? You can still get 2 1/4 pounders with fries and a drink for $5.

There is a simple explanation. In NJ, there is no incentive to work due to very generous welfare programs, and so labor costs and arm and a leg. In the South, you do not have generous welfare programs, so people actually work, labor supply is higher and hence cost of labor is lower. Real estate costs of course play a role as well, but they are dominated by labor costs.

-

Eniro is a melting ice cube, and has been that way since 2004

-

Value and opportunity blog did a project looking at firms in that part of the world, take a look.

-

18 minutes ago, changegonnacome said:

Is there a thread on this or write up you could point me too? Came across it mentioned enough times now to trigger my interest. Cheers

not my write-up, but see below

Tel Aviv Stock Exchange (TASE IT) Investment Overview

October 2021

A Brief History

▪Tel Aviv Stock Exchange (“TASE,” or “the company”) began operations in 1953 when a consortium of Israeli banks and investment houses joined together to establish the exchange.

▪Over the next ~50 years, TASE established a clearing house, enabled electronic trading, launched options trading, and created the first exchange traded note.

▪In 2000, the Knesset (the unicameral national legislature of Israel) approved an amendment to Israeli securities law enabling dual listing in Tel Aviv for shares that were listed in the United States.

▪Subsequently, the company expanded upon this arrangement, allowing dual listing of securities trading on the London Stock Exchange and Nasdaq.

▪In 2018, Hong Kong, Singapore, and Toronto were also added for dual-listing.

▪In 2017, the Knesset ratified an amendment enabling changes to TASE's ownership structure. Additionally, the Israeli District Courtratified the TASE demutualization arrangement.

▪The privatization paved the way for TASE’s for-profit evolution, reducing conflicts of interest and increasing TASE’s freedom to operate as an independent, standalone entity.

▪In August 2017, Itai Ben-Zeev was appointed as CEO.

▪In July 2019, TASE became a publicly traded company when it floated 31.7% of its shares to foreign and Israeli institutional investorsand to the public at large.

▪The shares trade under the Bloomberg ticker symbol “TASE IT”.2

Source: company filings and presentations.

Business Description ▪TASE is a monopoly financial infrastructure asset that plays a central role in Israel’s capital markets and overall economy.

▪The company is unique among global exchanges in that it spans the gamut of Israel’s entire capital markets infrastructure, offering products and services that include (a) listing, (b) trading in equities, fixed income, and derivatives, (c) clearing and settlement, (d) securities lending, (e) IT/co-location, (f) market data, and (g) indices.

▪To our knowledge, no other exchange has all these products and services under one roof.

▪TASE’s revenue streams are diverse, with non-transactional revenue (e.g., clearing, market data) growing as a percentage of the3

overall mix

1H21 Revenue by Source

1H21 Revenue by Type

16% 20%

21%

40%

40%

Trading and clearing commissions Clearing house services

OtherSecurities registration

Distribution of trading and other dataTransactional

Non-transactional

Source: company filings and presentations.

60%

Investment Thesis

A recent demutualization and IPO, TASE is a monopoly financial infrastructure asset that we believe is capable of compounding intrinsic value at ~35%+ annually in the coming years. Historically, TASE operated as a member-owned, not-for-profit entity run primarily for the benefit of Israeli banks. Strategic and financial decisions were made on behalf of the company’s members. TASE’s recent demutualization reduces conflicts of interest and increases its freedom to operate as an independent, standalone entity.

We believe that TASE has significant opportunities to launch new products and services, optimize pricing, and drive efficiency gains. We expect significant value creation to result from accelerating revenue growth and margin expansion. In addition, there are several sources of value which we expect management to realize over time that, in aggregate, can be worth more than half of the company’s current market capitalization. We believe management is highly incentivized to create value and is taking appropriate steps in this direction. Finally, we believe that TASE could be an acquisition target for a larger global exchange.

We note the following:

-

▪ TASE’s revenue growth is accelerating and can grow sustainably in the high-single / low-double digits.

-

▪ The company’s margins can double or more as they approach peer levels over time.

-

▪ TASE owns its corporate headquarters building, which alone is worth ~30% of the current enterprise value and can be monetized.

-

▪ An unusual arrangement with pre-demutualization shareholders could result in cash proceeds to TASE equivalent to ~14% of the current enterprise value (without additional dilution).

-

▪ Net cash currently on the balance sheet (~7% of the market cap) and future free cash flow generation (we estimate ~30% of its current market cap over the next ~5 years) provide management with significant firepower for organic and inorganic investments.

-

▪ TASE’s CEO, Ittai Ben-Zeev owns options on 4.25 million shares, providing a strong incentive to create value.

-

▪ Given significant consolidation activity in the exchange space over the years, we think TASE could be acquired by a larger global exchange for a significant premium.

4

Thesis Point #3: Owned Real Estate a Sizable “Hidden Asset”

▪ TASE owns its corporate headquarters building at 2 Ahuzat Bayit Street in downtown Tel Aviv. ▪ The building is state of the art, less than ten years old, and in a prime location.

▪ We believe the company can crystallize the value of this asset over time.▪ Management believes it would cost ~2% of the building value annually to rent the space the company requires.

▪ A 6.0% cap rate (which we understand to be the approximate market level for premier Tel Aviv office properties), impliessignificant value creation in a sale or sale-leaseback transaction.

▪ Using conservative assumptions around rent / sqm and Tel Aviv office cap rates, we believe the building is worth ~500 million ILS,or ~30% of the current enterprise value:

7

Source: company presentations, CBRE Tel Aviv Market Survey (Q320).

Thesis Point #4: Unusual Pre-IPO Arrangement another “Hidden Asset”

▪ As part of the TASE privatization, pre-demutualization shareholders received shares in the new company that entitled them to a maximum of 508 ILs per share in value upon a sale, with the proceeds in excess of that cap going to TASE.

▪ In H2-19, the banks sold a bit over 10% of their shares at ~1,000 ILs on average.

▪ This resulted in proceeds to the banks of ~14.3 million ILS and proceeds to TASE of ~13.8 million ILS. ▪ Currently these shareholders own ~19.5 million shares (~19% of shares outstanding).

▪ If all these shares were sold at the current price, TASE would receive more than ILS 222 million of net proceeds.

▪ This value is equivalent to ~14% of the current enterprise value.

▪ On February 10, 2021, TASE announced that its board of directors is exploring a structure that enables the buyback and allotment of shares to pre-IPO shareholders with the goal of incentivizing them to sell their “Arrangement Shares.” While discussions have broken off for the time being, it is encouraging that management and the board are exploring ways to crystallize value and increase liquidity.

8

TASE IT - Pre-Restructuring IPO Proceeds

Shares Held by Pre-Restructuring Shareholders (at 12/31/2019) Maximum Value per Share to Pre-Restructuring Shareholders Total Proceeds to Pre-Restructuring Shareholders

Current TASE IT Share Price

Maximum Value per Share to Pre-Restructuring Shareholders Value per Share to TASE (at current share price)Shares Held by Pre-Restructuring Shareholders (at 12/31/2019)

19.5 5.1 ILS 99.1

16.8 5.1 11.7

19.5

Source: company filings and presentations.

Total Proceeds to TASE IT (at current share price) ILS 228.2 % of Current Enterprise Value 14%

Extremely Attractive Pro Forma Valuation ▪ Multiple sources of current and future value have the impact of reducing our effective purchase price to a low single digit multiple of

estimated 2026 EBITDA. These include: ▪ Current cash on the balance sheet;

▪ Future free cash flow generation;

▪ Net proceeds from share sales by pre-restructuring shareholders; ▪ Monetization of headquarters building.▪ We believe that management could add further value through share buybacks or M&A, but we don’t give them explicit credit for that in this analysis.

TASE’s global exchange peers currently trade at mid-teens enterprise value / EBITDA multiples (see Appendix II) Source: company filings and presentations.

9

Extremely Attractive Long-Term Compounding Potential

-

▪ We believe the combination of accelerating revenue growth, margin expansion and several other levers for value creation can combine to drive intrinsic value growth of 35%+ annually.

-

▪ Should management allocate the ample firepower it will have at its disposal towards value-creating M&A or accelerated share repurchases, we believe upside can exceed 40% annually.

-

▪ While we’re not underwriting a takeout, we believe TASE is a logical acquisition candidate for a larger global exchange. Historically, such transactions have occurred at sizable premiums due to significant synergy potential.

Framing the Base Case Return Opportunity

(amounts in millions of ILS or ILs per share, unless otherwise specified)

Core Business: Estimated 2026 EPS Exit Multiple

Core Business Value per Share at Year-End 2025

Additional Sources of Estimated Value:

Net Cash per Share at Year-End 2025 Cumulative Dividends

Owned Real Estate Value (net of taxes) Pre-IPO Shareholder Sale Proceeds to TASETotal Additional Sources of Value

1.85 26.0x 4,814

Total Per Value Share 434 407 260 244 494 463 228 214 1,416 1,328

10

Total Value at Year-End 2025 Current Price

% IRR6,142 1,678 36%

Source: company filings and presentations.

Risk Factors

▪ Potentially adverse regulation.

-

▪ Given TASE’s relatively recent privatization, the regulatory environment in Israel is not yet well defined, which can create

scope for surprises.

-

▪ All indications thus far are that Anat Guetta, Chairwoman of the Israeli Securities Authority, is pro-market and has goals of increasing capital markets participation and opening the Israeli market to foreign investors and other market participants.

▪ Geopolitical risk.

▪ Particularly in the Middle East, this can be difficult to handicap.▪ Timeliness of management execution.

▪ The pace of revenue growth and margin expansion could take longer than anticipated.▪ Limited liquidity in TASE common stock.

-

▪ The company’s common stock has relatively low daily trading activity, which could limit our ability to purchase and sell

shares easily and may increase short-term volatility in the stock price.

-

▪ We believe that liquidity will likely improve over time as TASE moves past its demutualization and relatively recent IPO and develops a track record with investors, but this could take longer than anticipated or not materialize at all.

11

Appendix II – Comparable Company Analysis

13

Capitalization

Valuation

Profitability

TASE IT Comps Company

Tel Aviv Stock Exchange

Global Exchange Peers

B3 SA - Brasil Bolsa Balcao

ASX Ltd

Cboe Global Markets Inc

Bolsa Mexicana de Valores SAB de CV CME Group IncDeutsche Boerse AG TMX Group Ltd Euronext NV Nasdaq Inc

Average Median

Market Cap

533

13,624 11,364 12,975

1,117 71,368 31,554

5,898 12,324 32,545

21,419 12,975

Enterprise Value

429

11,533 7,509 13,851 985 74,258 35,792 6,429 14,925 38,072

22,595 13,851

EV / Revenue

EV / EBITDA

P/E Ratio

Dividend Yield

1.08%

1 23% 3 97% 1 58% 5 19% 1 81% 2 09% 2 30% 1 48% 1 11%

2.31% 1.81%

EBITDA Margin

Growth

Proj'd Cur Yr+1 Growth Revenue EBITDA EPS

Ticker

TASE IT

B3SA3 BZ ASX AU CBOE BOLSAA MM CME DB1 GY

X CN ENX FP NDAQPrice

1,678.00

12 22

80 48 121 69 38 91 198 72 143 75 132 45 99 60 194 64

Cur Yr

4.2x

68x 10 4x 96x 51x 15 4x 89x 83x 10 1x 11 2x

9.5x 9.6x

Cur Yr+1

3.7x

64x 99x 93x 48x

14 4x 83x 79x 87x 10 7x

8.9x 8.7x

Cur Yr

13.4x

84x 14 2x 14 8x

85x 23 4x 15 5x 13 7x 17 0x 20 2x

15.1x 14.8x

Cur Yr+1

10.9x

83x 13 6x 14 6x

78x 21 3x 14 3x 13 3x 14 2x 19 6x

14.1x 14.2x

Cur Yr

39.6x

14 6x 31 4x 21 5x 15 3x 29 9x 22 0x 18 8x 19 4x 26 4x

22.1x 21.5x

Cur Yr+1

31.3x

13 8x 30 2x 20 8x 13 9x 27 2x 20 2x 18 5x 18 4x 25 3x

20.9x 20.2x

Cur Yr

31.6%

Cur Yr+1

33.6%

15.0%

22.3% 26.8%

80 7% 72 9% 64 7% 60 0% 66 0% 57 5% 60 7% 59 3% 55 4%

78 1% 72 9% 63 6% 61 0% 67 8% 58 2% 59 3% 61 2% 54 7%

54% 49% 30% 66% 69% 72% 48%

16 1% 4 3%

20% 50% 12% 85% 97% 85% 24%

19 8% 30%

57% 40% 30% 98%

10 2% 89% 15% 55% 41%

64.1% 60.7%

64.1% 61.2%

6.6% 5.4%

6.7% 5.8% 5.0% 5.5%

Despite faster revenue growth, significant margin upside, and substantial “hidden” assets, TASE trades in-line with its global exchange peers on an EV/EBITDA basis

Note: all market cap and enterprise values shown in U.S. dollars. Valuation metrics are based on consensus estimates from Bloomberg. Source: company filings and presentations.

-

-

37 minutes ago, crs223 said:

I think it would be easy to identify fraud in US stats relative to China given all the data available for research. My uninformed understanding is that people get black-bagged in China for speaking out against the party narrative.

Example: administration might say “no recession” but individuals can crunch the numbers themselves and come to a different conclusion.

Have you looked at the US CPI statistics? Take a look at food, healthcare, housing, education, services, et all over the past 50 years and see if you can reconcile with official inflation measures. I have lived in the US for 33 years, official inflation was 120% (CPI went from 134.2 on 12/31/90 to 298.349 on 12/30/2022). I say not true.

In terms of food, prices have more than tripled, and closer to 4x for fish. In terms of healthcare, going back to February of 2009, health insurance prices are up 5x for the same policy. And I would wager there was no deflation in healthcare between 1990 and 2009. Education - Yale tuition+room&board = $27K in 1995, and $80K+ this year. Services: haircut in Manhattan went from 12 in 2001 to $35 in 2023 for a male. Restaurants - Per Se in 2004 pre-fix = $125, today = $350 plus... (CPI = 185.5 on 12/31/2003 and 298.35 on 12/31/2022.)

Housing: harder to compare, but NYC rents increased three-four fold since 1990 based on anecdotal evidence/personal experience.

This is why I do not trust US government statistics. Do not start me on quality adjustments and other tricks. Somehow if I ate lobster and it doubled in price, I automatically switch to chicken, so there is no inflation. My first laptop lasted 8 years - IBM thinkpad, top of the line Dell's break within two years (happened to five Dells that I owned, before I stopped buying from Dell.) We inherited a baby carriage from sister-in-law, the carriage lasted 4 kids and 15 years, my wife decided to buy new, top-of-the line from the same brand since she was ashamed of the looks she was getting at our private day-care in Manhattan. New top-of-the line Uppa Baby broke within twelve months. Same story with jackets - zippers no longer last more than 24 months, Mephisto shoes used to last a decade, now break within 24 months and the list goes on.

-

It is very area and product specific. For instance, NYC real estate prices seem to be unchanged vs 2019, yet in the suburbs real estate prices rose 20-40%? In Florida probably 50%+? Although property taxes and maintenance at co-ops and condos up 30%+ in NYC. Private school and nursery school tuition in NYC is probably up 5-15% vs 2019 for 2023-2024 season. Healthcare probably up 20%+ since 2019. Haircuts are up 50% in Manhattan since 2019 and the same on Staten Island. Food is probably up 30-50% vs 2019, restaurants up 20-50%, the more expensive ones - Michelin up closer to 20%, the Chipotle up 50%.

So what is the inflation rate?

-

Added to my position in Tel Aviv stock exchange. Now a 10% position.

-

Left unsaid is that we can't handle another 12 months of the war in Ukraine.

-

2 hours ago, cubsfan said:

^^ Well, ok - how about excess spending on defense did the trick?

If your enemies can outspend you by orders of magnitude - it's just a matter of time until you're done. You can't be running a sustained campaign when you're solely dependent on a commodity price like oil.

No. Look at US or USSR in Afghanistan or US in Vietnam, or China in Vietnam. Or go back to in time and look at Mongols, Arabs in 7th century AD, Ottoman Turks, and the list goes on.

-

18 minutes ago, cubsfan said:

^^^ Excellent post. And likely the reason Ukraine has such a strong chance against Russia. Much as I hate to see USA dedicate $100B a year to this war, then along with Europe adding billions for weapons - tough to see how Russia can not get buried, like Reagan buried them in the 80's. Russia has manpower, but with a defense budget of $80B - they are in real trouble.

The wild card, of course, is nuclear weapons, which, in the hands of Putin - who the hell knows.

And my other fear - is just how much of that arms aid gets stolen by the Ukrainian corruption.

Reagan did not bury the USSR in 1980s. The Afghan war and the collapse in petroleum prices did the trick.

-

It is not just China. Do you trust US governmental statistics? I for sure cannot reconcile CPI over the past three decades that I have lived here with how costs have changed. Not for housing, healthcare, food, education, haircuts, newspapers, restaurants, take-out, and the list goes on.

-

3 minutes ago, vinod1 said:

I am talking about estimate for transaction/expenses/etc prior to the 1950s for holding diversified portfolio of stocks.

I follow Damodaran's work and learned more from his "Investment Valuation" book than from CFA exams.

You may want to ask him whether he has the data. Somebody else who may is professor Robert Shiller at Yale. If I recall correctly, before 1975, retail investors paid 1% commission to buy or sell stocks. Institutions I believe paid 5 cents per share, but I may be wrong. The Coles foundation at Yale has a lot of old stock market data, so it may have the data that you are looking for. Also, there is a guy named Martin Sosnoff - he has a blog, used to be a money manager, he may be in his late 80s. Email him, may be he will be able to give you answers off the cuff.

-

2 hours ago, vinod1 said:

I was an indexer from 2001 to 2005 and thinking/researching ERP one of my favorite hobbies (isn't it sad?) and I picked this up somewhere in that timeframe. It might be something I read somewhere or it might be my own thinking but hardly any of my thoughts on investing are original.

One of the reasons I got interested in stock picking is because of the low ERP.

Anyway the argument has definitely been made by Siegal and Philosophical Economics which reinforced my own conviction (no confirmation bias, of course

). But I did not see anyone make estimates of this.

). But I did not see anyone make estimates of this.

Vinod

Go to professor Aswan Damodaran at NYU. He did and still does a lot of work on equity risk premia at various times.

-

Sold Feb 17 2023 MANU 23 strike puts for $1.25 each.

-

The mercenaries you need to fear are from North Korea. If, and that's a big if, North Korea has 500K well trained troops, then they can and most likely will be leased to Russia for a king's ransom.

-

53 minutes ago, lnofeisone said:

There is a large contingent of west-trained Afghan army that fled to Iran when taliban took over. They are generally pissed at the US. I can see russia tapping into that reservoir and Iran not objecting.

Can they actually fight? Did not put up much of a fight against the Taliban

-

27 minutes ago, changegonnacome said:

Part of the style drift I spoke about…..I remember seeing the portfolio years ago……and it was predominantly EMEA……and sector weighting was to financial services, if anything, back then.Everybody started to hear Cathie Wood in their head it seems towards the end of the great bull market

Interesting on return fact sheet……if anyone cared too they should email him and ask…..I myself couldn’t be bothered.

He will tell you that it is in USD excluding dividends. So all he is doing is comparing apples in dollars to oranges in Euros. Honest mistake that happens to be in his favor! What's 500 basis points per annum between friends?

-

1 minute ago, ratiman said:

Thanks. I thought that was the answer but I've run into some companies with such slow turns that I thought it might be that the company was valuing inventory at retail price. Another quick question: if a company ships off the inventory to a retailer, does the inventory shift to the retailer or is it still considered in inventory until the retailer pays?

If I remember correctly, once you ship the inventory, you take it off your books and put accounts receivable on. There may be nuances, you may need to put allowance for bad debt expense. You do not wait until you get the cash. The exception would be retail trade - I walk into a super market, buy an apple, cash changes hands and inventory falls. If the company has slow turns, you need to compare it with others in the industry (and its own history) to make sure that there is no fraud (inventory on the books that does not exist in reality.)

-

Lower of cost or market. Now there are different inventory costing methods - FIFO, LIFO, average costs, and some companies capitalize expenses such as overhead into inventories.

-

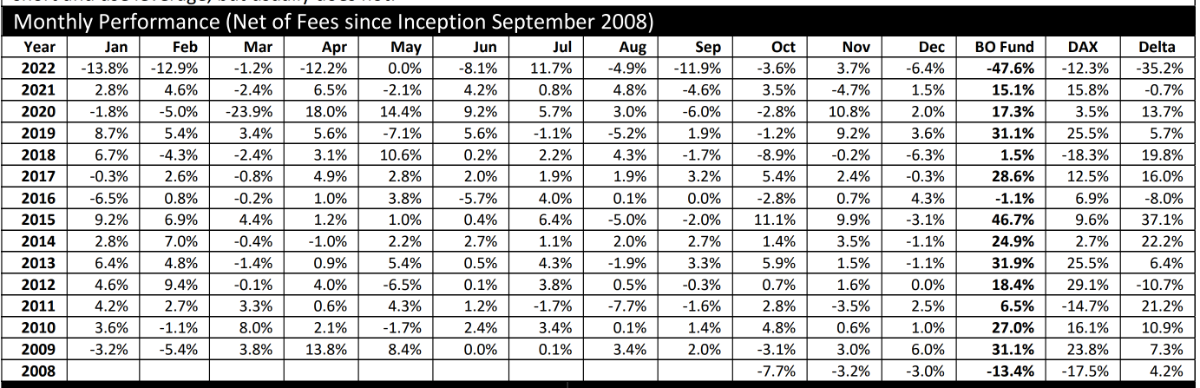

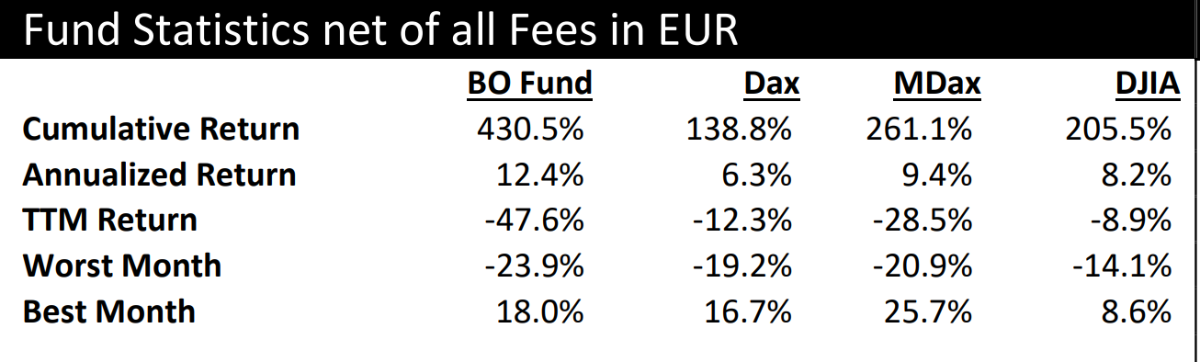

49 minutes ago, changegonnacome said:

See below - European manager so EUR investor base........as European manager then your benchmark isn't really SPY.....however....returns net of fees annualized & including the 2022 drawdown for fund come out at a 12.4% CAGR

Thank you. These statistics are clearly inaccurate or misleading, whether by accident or design I do not know. DJIN total return from 09/30/2008 through 12/31/2022 = 352% in USD or 11.97% annualized. In Euro, it is 466.84% or 13.88% annualized. If he cannot get this right....

-

How do his returns in USD compare to the S&P 500 since inception?

-

https://www.jpost.com/international/article-728770

Apparently Russia is recruiting mercenaries in Serbia

-

2 hours ago, Warner said:

Russia has more resources that most will admit to. Not high tech of course but they will go low tech. They have the collective thought to sacrifice for their country. This is not over and done. Russia will fight back again and a lot more people will die. We tend to look through at Russia like a western country and that they are not. For better or worse that is for them to decide. Who will be victorious, how that looks, and the costs of it no one can know yet. But, I promise the costs for both sides will be extreme and this will not likely end in an amicable long term agreement.

Everyone looks at Putin like a villain in this. And, he is.

But, very few people are looking back at the main missile and arms treaties the USA have unilaterally backed out of. And no one is also looking back in the recent history and noting that the West have perpetually lied to Russia at every opportunity in the past 30 year.

Russians look upon Putin favourably as he has actually improved Russia a lot since the 90's. He has their goodwill in general and he can't loose this war entirely.

I agree with everything that you say except for your claim that Russians look upon Putin favorably. I know many people who either came from Russia recently or know people who have. None of them know anyone who looks upon the guy favorably. Millions of people fled Russia. Last week I took a gypsy cap in Brooklyn, the driver was from Yakutia. He and his two sons made it via Kazakhstan to Mexico and walked across the border. According to him, it is not an isolated case. Had Putin been so popular, would he really need to rig every election?

As for backing out of treaties, I recall Kaiser Wilhelm saying that treaties were just scraps of paper. I personally do not support this view, but this has been the way of the world for millenia. As for Russia being aggrieved here, spare me. Invasion of Poland in 1919 when Pilsudski stopped them, invasion of Poland in 1939, winter war with Finland. The bully gets punched in the face, cry me a river!

I do find it hypocritical when Boris Johnson is incensed about Russian war atrocities, and yet is silent on even bigger atrocities committed by the British in the Boer War.If the West was not run by hypocritical morons - Biden, Macron, et all, they would instead of sending tanks to Ukraine do the following:

a) Open borders to Russians fleeing Putin

b) Given citizenship to deserters from Putin's army

c) Publicize the above in Russia

Putin would not have an army in three months.

Hindenburg Short Adani Group of Companies

in General Discussion

Posted

Let's just say I do not understand how Mr Adani made his $100bn+