Short answer is that it is very cheap. Long answer: here is a VIC write-up (not mine) from last year that lays out the bull thesis pretty well. I would add that I am more bullish than the writer on the aggregates space, I think that the company will be able to generate a lot of value from bolt-on acquisitions in the aggregates space - the latest deal for Stavola seems very attractive and the company claimed that none of the three majors (MLM, VMC or CRH) bid, the last two for anti-trust reasons. In addition, when I see a CEO buying a million dollars worth of stock, I get interested, particularly since he already owns $30MM+.

Description

Arcosa (ACA) has everything we look for in an equity investment:

High quality core business benefitting from huge secular trends and government spending

Underappreciated secondary businesses inflecting rapidly

Giant catalyst in IRA tax credits that pushes numbers materially higher than expectations

Rock solid balance sheet

Great management and historical capital allocation

Zero hedge fund ownership despite ample liquidity and size

Cheap absolute and relative valuation

The short-term thesis is that, in 2024, every part of this business will inflect higher and truly underappreciated tax credits for their American made wind towers will drive EBITDA meaningfully above expectations. We can have high confidence in this as the law is written and the backlog is in place.

The long-term thesis is that at its core Arcosa is one of the highest quality aggregates businesses out there, and as they sell off non-core assets will be the most strategic asset in construction products – one day VMC and MLM will engage in a bidding war for it.

None of the above is in the valuation.

History

Arcosa was previously written up by AtlanticD in 2019. The bull case played out even better than expected despite COVID, although the stock has recently languished. There were zero comments on the post – generally a good sign for outperformance on VIC and a sign that despite the $3.5bn market cap, nobody cares. Well, maybe its time to start.

Arcosa spun from Trinity Industries at the behest of Valueact in 2017. ACA was TRN’s collection of infrastructure assets, which included aggregates, utility/wind towers, rail car components, storage tanks, and barges.

A few things have happened since the spin:

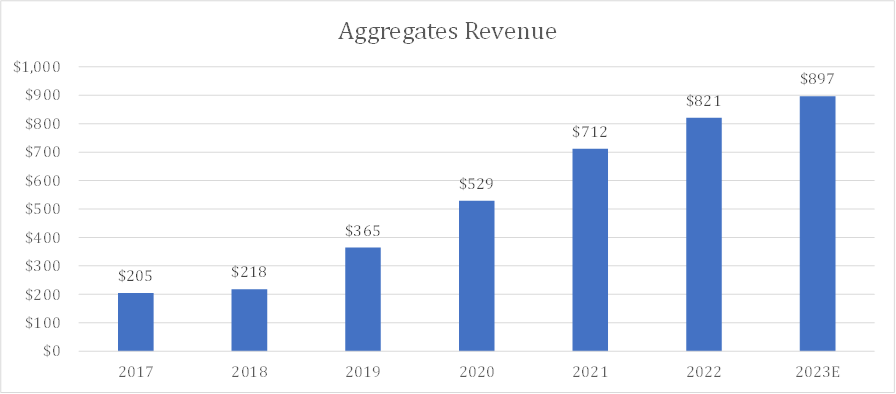

Construction products (mostly aggregates, more below) has gone from 33% of EBITDA to 60% - this is now mostly an aggregates business

A stellar acquisition program and core business performance has grown EBITDA by 60% despite a cyclical downturn in barges and wind towers (both swinging up right now)

They took storage tanks from zero EBITDA to $50m and sold it

Kept leverage low (1.0x EBITDA)

Generated 800m+ of FCF despite significant growth investments

In my view they have pitched a perfect game since the spin, its very hard to find fault in their execution and strategy, despite serious challenges to their cyclical businesses in the form of COVID, steel prices and delayed wind PTC. With renewed dollars for infrastructure at both a state and federal level and the IRA, my view is the time for ACA is now.

Businesses:

Construction Products – 60% of EBITDA

Arcosa operates a top tier aggregates business in terms of geographic location, growth, and margins. The business has some wonderful qualities:

Primarily located in TX (50%), OK, LA, and AZ, they participate in local oligopolies in high growth construction markets with growing populations and year-round construction

They have a solid mix of specialty materials and recycled aggregates which generate better returns both from pricing, but also are more ESG friendly to win environmentally conscious bidding processes

Through both acquisitions and organic growth, this business has grown 4.5x since 2017:

Margins are approaching best-in-class, with 23% EBITDA margins for the group (which includes lower margin trench shoring business). I estimate their aggregates margins to be around 25%. Given acquisition integration and smaller scale, this compares well with MLM and VMC, and given acquisition amort they are tax efficient.

Unlike larger peers, they can still do modestly sized and priced acquisitions (they have acquired at about 8x EBITDA historically) and move the needle

As may be obvious, the current environment for this business could not be better. Just taking lettings data for September for example, bidding activity was up over 20% in ACA’s markets on average, with their core TX and OK markets up 28% and 45% respectively. It’s a great time to be in the aggregates business in the Southwest US. Over the last few years this has mainly been a stagnant volume/positive price market – but we are about to inflect to a growing volumes/positive price market so I expect growth to accelerate from here.

Engineered Structures – 30% of EBITDA

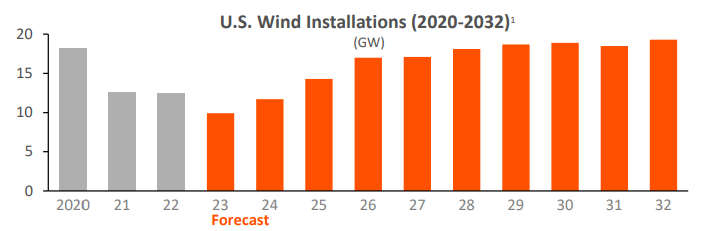

Arcosa is the leading manufacturer of wind towers and utility towers in the US. This segment is where our key, underappreciated catalyst lies – but more on that below. They operate in oligopoly markets for these products in the US – giant specialized steel structures used to secure the electric grid and hold up wind turbines.

These are not easy to make. You need very specialized manufacturing that has to be built from the ground up to be efficient manufacturing structures of this size (wind towers can go up to 50m), and then you need rail connects and specialized transportation to move these things where they need to go. As a result, there are few players domestically that can handle these jobs, and ACA has a history of high quality products.

While they don’t disclose specifically, some sleuthing has helped me discover a few things:

The utility towers segment makes up about 70% of revenue and ~100% of non-tax-credit profit in this segment in 2023.

Utility towers is a great, growing business operating near capacity – grid modernization plans across the US require a robust tower build program. If you like PWR or HUBB, these guys should be on your list. You have a 10 year secular growth path here, with no cyclical risk

Steady state margins for utility towers is likely in the ~20% range (once again, they don’t disclose). But you can back into this number given we know wind towers are zero profit in ’23.

Wind towers is at the lowest of low ebb right now. Because of the delays in renewing the renewable Production Tax Credit, wind orders fell off a cliff and in 2023 ACA will be operating at only about 40% capacity – barely keeping the lights on.

The wind forecast dramatically changed with the passage of the IRA.

Arcosa has gotten $1.1bn in orders just since passage, just for wind (!) this is over 5 years of backlog at the current rate, and still 3 years if at 100% capacity

This bill goes 10 years, and expectations are for a meaningful uptick in wind deployments:

We haven’t even gotten to the best part – the IRA carves out billions for the manufacturing of things like wind towers – that goes straight into ACA’s pocket. This is our catalyst. See below.

Transportation Products – 10% of Revenue

A coiled spring in the process of unspringing - transportation products is ACA’s inland barge manufacturing business and its railcar components business. Both cyclical, both finally inflecting from the depths of the cyclical trough – with years of upside runway. A few facts:

Steel components is mostly railcar components, a cyclical business that has been in trough for years. This was a $200m revenue business at spin, did $90m in 2021, and is now run-rating at $160m.

One of the key aspects of steel components is railcar coppers, a market that has suffered due to imports of late – this summer a 400% duty was put on imported coppers from China and final determinations are coming for Mexico shortly

The capacity utilization in steel components remains low, but railcar scrappage really picked up with steel prices in 2022 and we should see continued growth in new cars this year and next

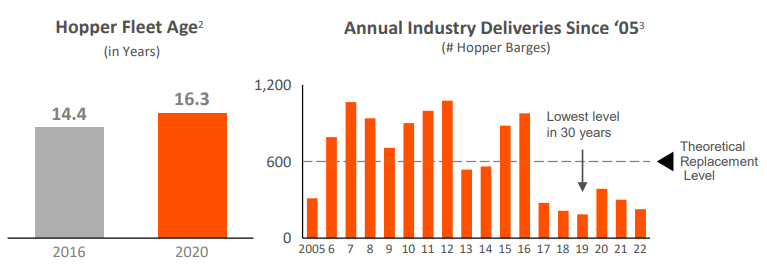

The barge business is one that a lot of investors really turn their nose up at, although in reality it has some very interesting dynamics, and recent results are very promising:

At peak this business did $150m of EBITDA. Today it does maybe $30.

Since the prior peak, a competitor JeffBoat – with 30% market share in inland barges – liquidated, selling all of its assets….to Arcosa for pennies

Now Arcosa has 70% of inland barge market share, vs 40% at the prior peak

Inland barges are protected by the Jones Act – they must be built in America to use American waterways

Barges are *the* most efficient way to transport anything in the US, in terms of cost of fuel, labor, etc – obviously, you still just have the waterways that we have

Deliveries are really at low ebb, well below replacement – this market needs to inflect:

Backlog in this segment has doubled in the last 12 months, so we are seeing signs of this inflection.

Finally – and importantly – the key issue here has been the cost of plate steel, which has remained high. Arcosa restructured their operations to be able to use hot rolled coiled – and lowered the cost of barges to the customer. Our checks indicate this has unlocked many more orders and inquiries – and with HRC prices cut in half since April, the barge momentum should continue

On its own, all of the above would constitute a great investment in my mind. A solid core business, positively inflecting cyclical businesses near trough earnings and huge long-term tailwinds underpinned by government funding.

But here is where this gets very interesting.

The Catalyst

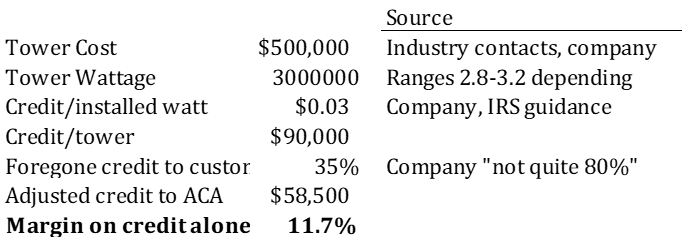

The IRA includes a provision (45X) that includes the Advanced Manufacturing Production (AMP) tax credits for manufacturers of wind energy components in the US. This is a game changer for the wind towers business. Let’s do some analysis:

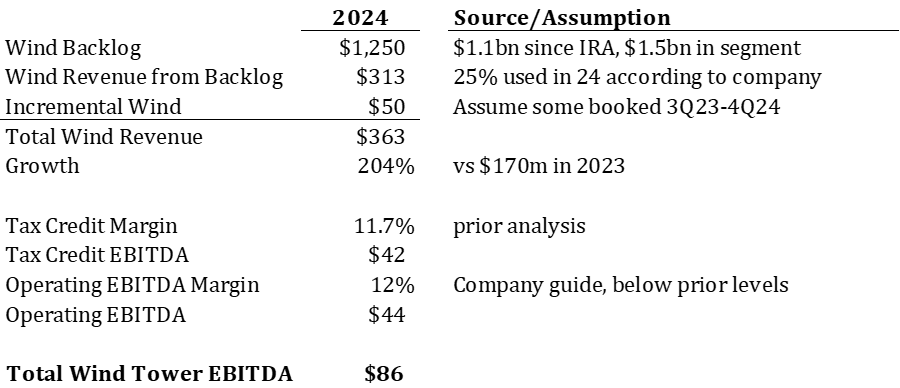

First – how much do they make per tower?

We have high confidence they will make $58k or better per tower they build.

Second – how big IS wind towers?

Pretty small in 2023 – makes sense they are earning zero EBITDA.

Finally – how much will they earn in 2024?

Whoa! And, at least I think this is conservative. We assume only $50m in new orders come in between June 30 2023 and Dec 2024 – it will likely be a lot more ($1,1bn came in in last 12 months). Plus, they have the capacity to produce well north of this number. Finally, they have earned as high as 17% EBITDA margins here in higher utilization environments, so the 12% assumption is also likely conservative. So – we can have confidence in somewhere around $80m of EBITDA in wind towers next year, growing from $20m this year.

Now, let’s bridge ’23 to ’24 – consensus has EBITDA growing from $364 in 2023 to $396 in 2024 – growth of $32m. So, already wind alone puts us well ahead of this. Let’s take a look at some reasonable forecasts:

Look, maybe I’m really missing something here – maybe I’m too optimistic about the barge/rail business, or am overestimating the share of the tax credit ACA keeps, etc. I could also be underestimating these things and more – the above seems very reasonable to me. But, one has to be very, very wrong just to get back to where consensus is for 2024 – I just don’t see it.

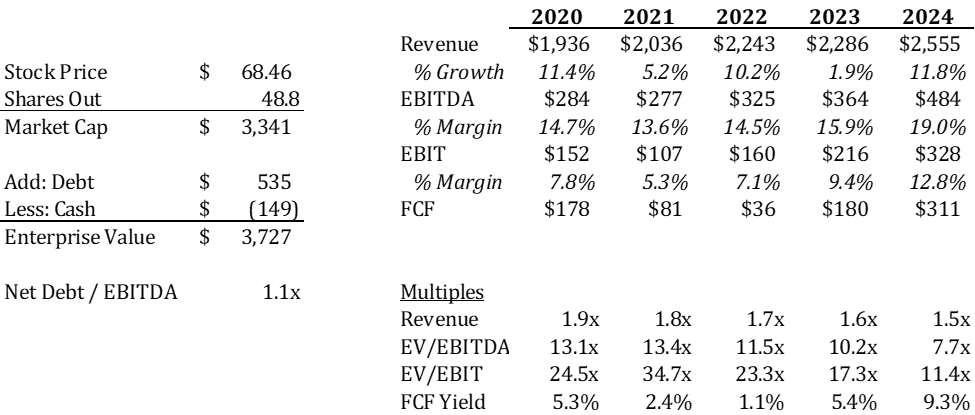

Moreover, growth capex is falling – this $480m of EBITDA likely converts into ~$300m of free cash flow given lack of interest expense, tax efficiency and the working capital efficiency of this business historically. That’s a 9%+ FCF yield on today’s relatively unlevered market cap.

Valuation

On my numbers ACA trades at a 7.7x EBITDA margin and over 9% FCF yield. Just for fun, lets say you took their aggregates business and burdened it with its share of corp costs, and value it near aggregate peers – that’s $2.7bn of value. Then add in the fact that the cyclical businesses are earning a fraction of what they could in a more robust market, the 10 year runway in IRA funding, etc – I think this is a very compelling, near-dated opportunity that you can then hold for years.

Arcosa remains an off-the-run idea, despite its size and scope. I had a conversation with the infrastructure analyst at Goldman just a few months ago and he had never heard the word Arcosa before. They do not market often and are unknown in platform world. Hedge funds own less than 4% of the shares. I believe a lot of incremental buyers wait in the wings as numbers begin to inflect higher.

Risks and Pushback:

The primary pushback I hear is – this is a jumble of assets and hard to understand. And while I agree – it takes some work – that is also part of the appeal. I think people quickly write the business off as “not a pure play” without understanding the dynamics of each piece – and when they all come together at the same time, the upside to numbers is obviously very substantial. Finally, they are in the process of simplifying this business, and as cyclical elements cycle back up, they will sell them (like they did with storage tanks). In 3 years I’d expect this really does look like a pure play aggregates business.

Wind tower orders and renewables implosion – after the NEP debacle, there is some skepticism about the future of wind. This is warranted, although our checks indicate that traditional onshore projects, mainly in the middle of the country, are still very compelling because of the host of tax credits that are locked into the IRA bill. Moreover, you don’t really even need ACA to book a single new wind tower for them to still crush 2024 expectations here on current backlog alone.

Cyclical businesses worth very low multiples: I agree – anytime near peak! Putting a low multiple on a business doing $30m of EBITDA that can do $200m in an upcycle seems strange to me – I’d rather just watch it inflect. Plus, even if this is true, the stock is probably still too cheap

Disclaimer

This document is for informational purposes only. All content in this report represents the author's opinion. The author obtained all information herein from sources believed to be accurate and reliable. However, such information is presented “as is,” without warranty of any kind — whether express or implied. All expressions of opinion are subject to change without notice, and the author does not undertake to update or supplement this report or any information contained herein. This report is not a recommendation to purchase the shares of any company. The information included in this document reflects prevailing conditions and the author’s views as of the date submitted, all of which are accordingly subject to change. This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity. Any or all forward-looking statements, assumptions, expectations, projections, intentions or beliefs about future events included in this document may turn out to be incorrect. Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the potential complete loss of principal. Investors should conduct independent due diligence, with assistance from professional financial, legal and tax experts, on all securities, companies, and commodities discussed in this document and develop a stand-alone judgment prior to making any investment decision.

I do not hold a position with the issuer such as employment, directorship, or consultancy.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

IRA tax credit drives huge outperformance in wind EBITDA vs consensus for 2024