maplevalue

-

Posts

331 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Everything posted by maplevalue

-

NTDOY

-

Nobody really knows how much QT affects interest rates so the talking heads find it easier to just discuss the overnight rate.

-

The Economist had an article on Xi this week (sorry paywall https://www.economist.com/briefing/2022/09/28/an-investigation-into-what-has-shaped-xi-jinpings-thinking), and I found this part interesting Makes one wonder, particularly when viewing China news through a Western lens, how 'truly' Maoist Xi is. I remember when Trump talked about waging war in the Middle East and "taking the oil". Outsized rhetoric for political purposes (nobody could claim they would be tougher on the Middle East than someone who says that). Might Xi be employing the same hyperbole/sabre rattling, in order to defend himself from rivals in order to cement power here?

-

https://www.linkedin.com/pulse/starts-inflation-ray-dalio/ Dalio has been spot on since start of COVID in his evolution from 'cash is trash' -> 'cash is trash but equities are trashier'. Well worth a read. Particularly interesting is his view inflation stays elevated.

-

Where Does the Global Economy Go From Here?

maplevalue replied to Viking's topic in General Discussion

The estimates of the neutral rate are exceptionally uncertain, forecasts for inflation are exceptionally uncertain, and my feeling is that people have anchored themselves to what has transpired since 2008 as to what 'usual' interest rates are. In the 2010s many people spoke about how the Fed was 'pushing on a string' in that they struggled to increase inflation via more and more extreme monetary stimulation. Which makes sense, their policies mostly juiced up financial assets which are owned by the rich so their easing did not create that much inflation since the rich will not change their consumption patterns that much if assets appreciate. It is completely reasonable that we are in the reverse situation today, where in order to generate even a modest reduction in inflation the Fed needs to move interest rates an outsized amount. As of today, stocks, real estate, crypto, etc. are well above their pre-COVID highs. Therefore the vast majority of people are still feeling pretty rich. My sense is the Fed needs asset prices decently lower from here (via QT/interest rate increases) to generate a response from the real economy. -

It does seem like the tide has turned. I do wonder if there is an element similar to Afghanistan 2021 where the paltry will of the defenders leads to a swift recapture of territory.

-

https://www.gmo.com/americas/research-library/entering-the-superbubbles-final-act/

-

https://www.economist.com/business/2022/08/05/meet-chinas-new-tycoons - Some businesses suffering, but others thriving in Xi Jinping China - Record 58bn in IPOs in mainland China this year (19bn in America, 5bn in HK) - By 2020 privately controlled companies were half market capitalization of China’s 100 biggest firms, versus one tenth a decade earlier - Five years ago mood began to shift: first crackdown on conglomerates, then shadow banks shut down, then tech giants hit with regulator probes - Next generation of entrepreneurs, Mr Xi recently urged them to “dare to start a business” - Unwavering support for startups, as long as focused in priority areas: cloud computing, green energy, high-end manufacturing

-

Best thing they can do is continue to delay the new console. Recent PS/XBOX console releases were a bit of a gongshow with shortages. With the Switch performing as well as it is, seems to make sense to delay the new console until you are reasonably confident you can produce enough of them, and pair it with a blockbuster game release. Possibly a 2023 Holiday release alongside the new Zelda game. On another note NTDOY just previewed the new Pokemon game, which appears to be a shift towards the open-world format (which for that franchise appears to be a major change). Relatively positive reaction around it, with a Switch install base of 100mm and a Nov18 release date, could be 'the' holiday game.

-

The point of me posting the episode was more about hearing the couple's justification for buying a condo. With that said I would tend to agree with the host. You have two 25ish year olds who have been locked away for two years. They are unable to save money, and at the current rate will have to dip into investment savings soon. You could either advise the couple to a) cut back on the things the couple loves doing the most (advice unlikely to be followed, and based on their life stage probably does not make sense) b) rent instead of own a condo (a rip the bandaid type solution which would require some work up front, but after that nothing...i.e. not a hard financial plan to follow). Renting seems like a good solution for these individuals.

-

https://www.iwillteachyoutoberich.com/049-eric-elena-part-1/ Good podcast episode about a Toronto couple buying a condo and slowly going broke because of it. Good profile of the psychology behind Canadian real estate.

-

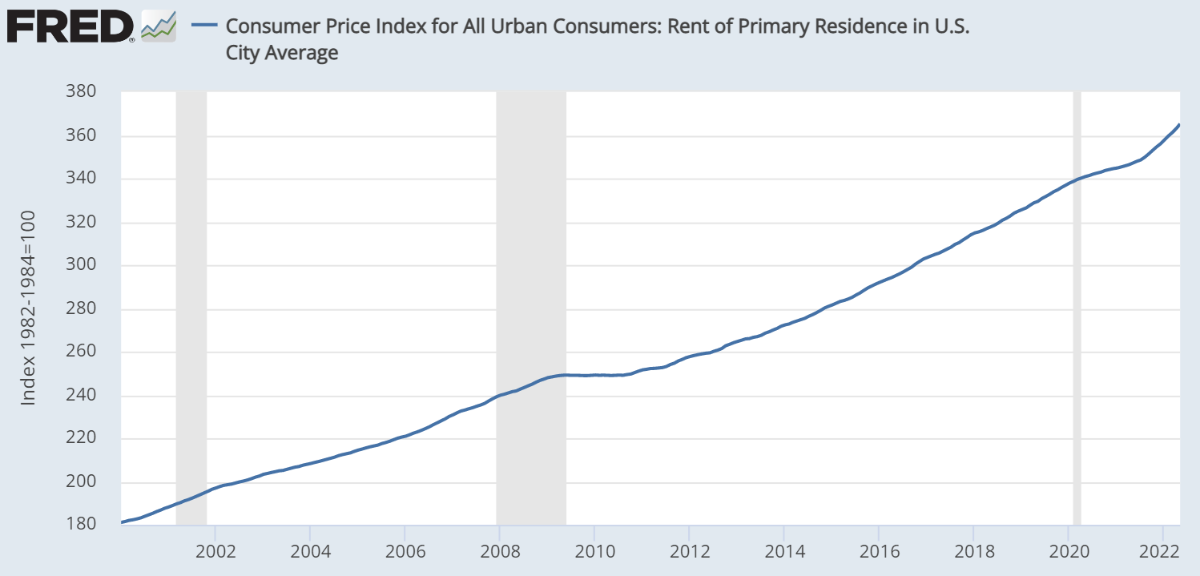

Just Ontario that has this https://toronto.citynews.ca/2022/06/29/ford-government-caps-rent-increases-2023/. Honestly I doubt there is much pushback since Ontario govt just won a majority and 2.5% is peanuts compared to what it 'should' have been (5.3%).

-

Does how much money a person has reflect their value to society?

maplevalue replied to Gregmal's topic in General Discussion

With Gates how much of his wealth is from making a great product as opposed to doing a bunch of anticompetitive stuff which the government should have regulated more aggressively but did not. -

Around 6 minutes Bridgewater's Karionol-Tambour discusses how commodities a tricky inflation hedge given idiosyncratic risk, but also their sensitivity to growth https://www.youtube.com/watch?v=UhM8ETH-H3c&list=WL&index=25. REITs an interesting asset as their cashflows are inflation protected, and in a growth slowdown scenario you still can probably get rent growth (especially if next slowdown we see more direct cash transfers to individuals). As @Gregmal has said they are like the new and improved treasury bond.

-

https://toronto.ctvnews.ca/office-workers-are-returning-to-toronto-but-foot-traffic-on-mondays-and-fridays-hasn-t-bounced-back-will-it-ever-1.5962940 Summary of the story is that TTC ridership in Toronto is about 50% of prepandemic levels. With each passing day it seems like hybrid/fully remote is here to stay, in Canada in particular which has less of a hard charging business culture than the US. Toronto housing will probably be fine given there are many reasons people want to live there. I would think Ottawa real estate might struggle given the public sector will likely keep WFH/hybrid more than private sector. Minto REIT (40% Ottawa) has struggled as of late

-

This is very interesting. Do you have a source for this?

-

Where Does the Global Economy Go From Here?

maplevalue replied to Viking's topic in General Discussion

To many people's careers in the finance industry a indexed 60/40 portfolio producing negative real returns is the 'end of the world' -

Where Does the Global Economy Go From Here?

maplevalue replied to Viking's topic in General Discussion

Well in fairness this is the 2nd year of 'transitory supply chain related inflation' one can forgive investors for thinking this might be persistent (especially if there is no quick solution in Ukraine). You are correct investors are not entitled to real bond yields. With that said real yields serve as inputs into the save vs. spend decision, and the more deeply negative real yields are, the more economic actors are incentivized to pull forward consumption. So if the Fed wants to slow economic activity, it's not enough to just have a higher nominal yield, but real yields matter as well. -

Where Does the Global Economy Go From Here?

maplevalue replied to Viking's topic in General Discussion

Since long rates are what most influences asset prices, and since asset prices are essentially what the Fed is using to affect inflation, if inflation is persistent this will force the all-powerful Fed to make long rates go higher too (faster QT + more hikes). Today's bond market reminds me of what it was like in the mid 2010s. Market kept saying "yields are so ridiculously low, they cannot possibly go any lower". Rates kept grinding lower (including the epic 2014 treasury market flash crash). Believe similar situation at play today where market convinced yields cannot go that much higher, and we will continue to grind higher in yield. -

Where Does the Global Economy Go From Here?

maplevalue replied to Viking's topic in General Discussion

Forget about recession or no recession. The most important consensus in the market right now is that rates can't go up that much. Market thinks Fed can get to neutral at ~2.5%-3% (which at current inflation rates is still one of the most stimulative monetary policies the US has had), real 10y yield at 40bps well below historical norms. All retail investors and real estate investors conditioned on BTFD of the past decade because you get rewarded by ever lower discount rates. Very big pain will occur if consensus shifts to higher rates than what is currently discounted. Not saying it will happen, but macroeconomic uncertainty is super high right now so its a very real possibility. -

Demography - declining birth rates / falling population

maplevalue replied to Sweet's topic in General Discussion

Great trend to consider long term. In the declining population scenario housing is particularly at risk outside of urban centres. Just look at Japan https://www.vice.com/en/article/88nxkx/japan-abandoned-homes-akiya. On the other hand, there is good reason to believe life expectancy could dramatically increase in the years ahead which would soften the effect of declining birthrates (https://www.youtube.com/watch?v=nnnXVUWlTkI). -

There is probably something to be said for the fact that there has been no post in the BABA thread today, on one of its biggest moves in awhile (+15%). Maybe sentiment is just really bad?

-

@Spekulatius I am sympathetic to your view about Xi's vulnerability, but the more I read on it the more I am convinced he is not very vulnerable (many China experts believe his next 5 years a done deal). Xi has essentially purged most of his opposition via anti-corruption campaigns. Plus we are at the beginning of China opening up and he will be able to say "yes it was hard, but I saved millions of lives at the expense of a few percentage points of GDP growth". Good article below (paywall) Rumours that Xi Jinping is losing his grip on power are greatly exaggerated https://www.ft.com/content/5e14bfb2-f0a9-4259-9d4c-a1b0ff607560

-

A House in Canada Now Costs Almost 2X A House in the US

maplevalue replied to Viking's topic in General Discussion

Blackstone targets Canadian real estate, opens office in Toronto Blackstone Inc. is ramping up its Canadian real estate business and opening an office in Toronto as it expands from significant investments in warehouses into new sectors such as commercial and residential properties. https://www.theglobeandmail.com/business/article-blackstone-targets-canadian-real-estate-opens-office-in-toronto/ -

China - Economic Consequences of Zero Covid Policy

maplevalue replied to Viking's topic in General Discussion

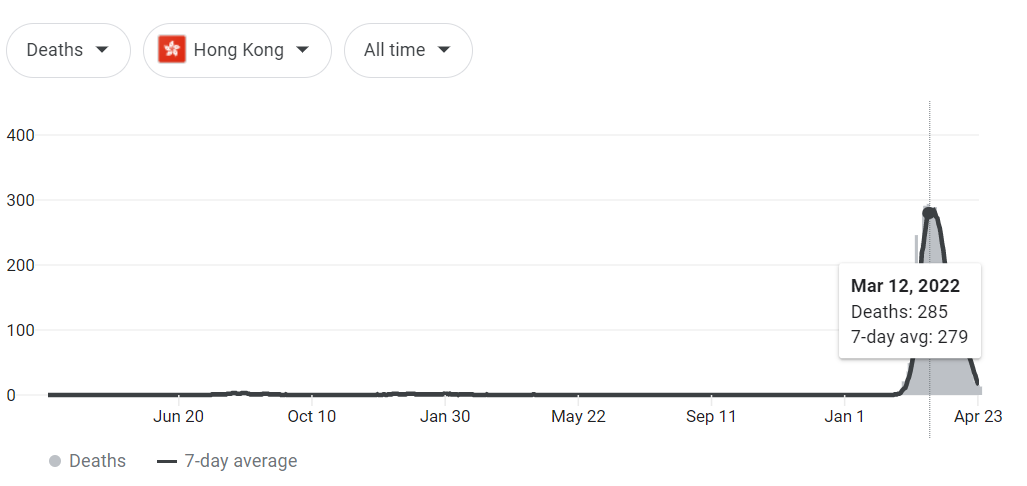

Year of Xi's re-election -> desire for 'stability' in China. Chinese hospital system is not great -> keep COVID 0 even in face of Omicron to at least slow spread of COVID amongst population without natural immunity, bad vaccines, and a elderly population that is relatively unvaccinated. This will likely follow the path of Hong Kong where there is a sharp peak, and then it declines. Overall, after this latest amount of lockdowns China probably will have been less locked down on average since 2020 than many Western countries. COVID 0 gets relaxed going forward.