maplevalue

-

Posts

331 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Everything posted by maplevalue

-

Thank you for this comment and it led me to look more into the mechanics of how BoC QE is operating. One question I had, which you may know the answer to. So the BoC currently remits its earnings to the Federal Treasury. I am just thinking about a situation where if interest rates rose, the value of the bonds fell and interest expense on reserves increases, the BoC could run at a loss one year. Does the govt need to write a cheque to the BoC in this scenario? Or could the BoC just run a negative equity position (it's all funny money anyways).

-

With respect to government spending I think the comparison to the World Wars is weak at best (in terms of the necessity of the spending). One of the things that will be interesting is the future political will across the country to impose higher taxes to pay for the COVID response. Income taxes were introduced around WWI and made permanent after WWII. For me I can see how Canadians would have come to accept income taxes as an acceptable price to pay to put an end to Nazism. But with COVID related government spending there has been such incredible waste and misallocation of resources (e.g. self-employed people getting CRB who claimed negligible net income in 2019, Chinese state-owned companies accessing the wage subsidy, Leon's Furniture getting the wage subsidy and then paying out special dividends, WE Charity fiasco) that I believe a large part of the electorate will be unwilling to accept higher taxes. All of this probably points to a continued period of endless QE/zero interest rates forever.

-

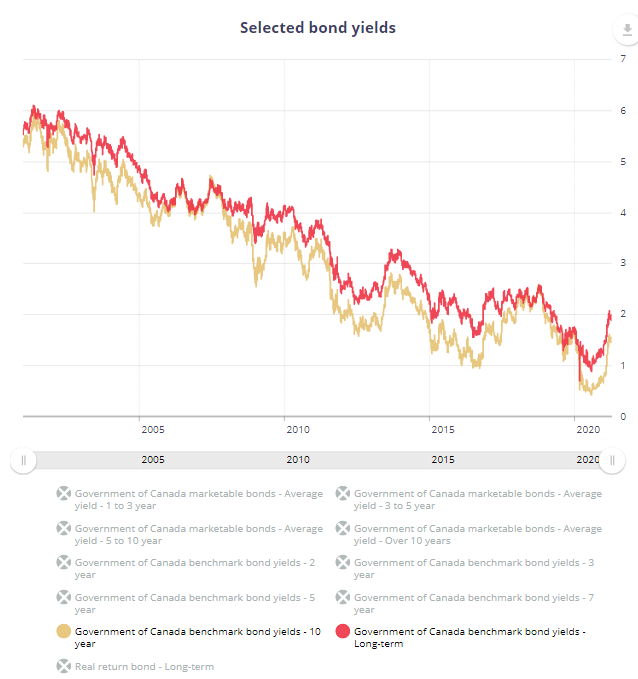

Also to put into context what is happening, in 2020-2021 GoC issued 267bn short-term bonds (2yr/3yr/5yr) 107bn long-term (10yr/30yr), 2021-2022 they will issue 160bn short-term 121bn long-term (and keep TBills about the same). Relative to keeping proportions the same it means they are issuing an 'extra' 38bn long-term debt. Now one can compare this 38bn to the total size of the debt outstanding (par value) right now: TBills: 218bn Under 1yr (excluding TBills): 104bn 1yr-5yr: 442bn 5yr-10yr: 120bn 10yr+: 166bn So while they are extending the term of the debt, it really pales in comparison to what is currently outstanding, particularly the 764bn maturing in under 5yrs. Better hope rates are low forever! Source on GoC's Bonds outstanding.

-

Two comments on this. First on the debt maturity profile. 10yr/30yr yields are already back towards pre-COVID levels so while it is nice to see the extended issuance, the attractiveness is not what it once was. Also, the long end of the curve is less influenced by central bank policy so issuing more can 'move the market'. I believe last year Canada was thinking of having more long-end issuance but did not because of possible market impact. Canada is a small open economy and investors do not view CAD debt in the same way as UST's so this shift to long term issuance could push rates higher (who really wants to buy 30yr debt at 2% in the midst of a massive economic rebound?), and is hence not the 'free lunch' it is being marketed as. Second, I view the green bond as a waste of everyone's time. It's not clear to me that that this will trade at a lower yield (i.e. savings for government) than standard issue Government of Canada bonds, and there are also likely to be a bunch of costs related to setting up the program.

-

TVO Interview with Federal MP Adam Vaughn - What Should the Government Do About Housing? Absolutely terrific interview to understand the mindset of politicians in Ottawa about house prices, and the lack of political will to do anything about it. Basically says we cannot have a 10% correction in house prices, even after a 20%-30% runup, because we need to "protect the investments Canadians have made in their homes".

-

A clause in Rogers’ 128-page takeover offer has hedge funds eyeing big gains from Shaw’s preferred shares - Globe and Mail

-

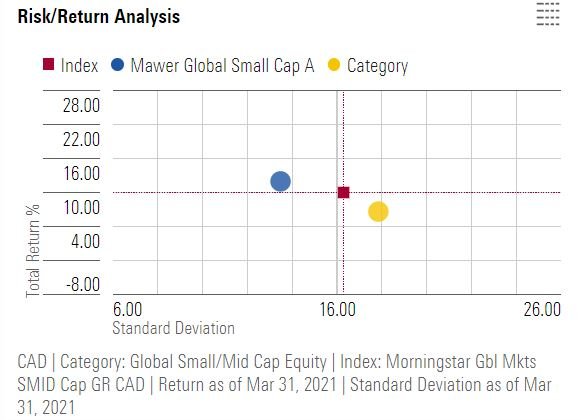

No thoughts on that particular fund, but worth looking at some of the Mawer funds. Risk-adjusted returns fairly strong (Global Small Cap fund risk/return analysis from Morningstar below). Can invest as a Canadian, and can invest direct with them for lower MERs (fund I mentioned is 1.76% MER). Does not resemble the index very much.

-

Some similar comments from Prem Watsa in Fairfax Financials most recent annual report https://s1.q4cdn.com/579586326/files/doc_financials/2020/q4/WEBSITE-Fairfax-Financial's-2020-Annual-Report.pdf

-

FFH, have been growing more comfortable with the name and prefer it over the indices in what is today a very uncertain investing environment.

-

Message on TD Online Broker Today "We are currently experiencing issues with order entry. You will not be able to edit or cancel orders submitted. You may also experience delays receiving fill reports in your Order Status. Please use caution when placing your orders; they may have been filled. We are investigating the issue and working to restore service as soon as possible." !

-

I agree with this wholeheartedly. It is amazing how frequently one reads about new labour saving technology (take a look at this video on autonomous fruit picking which looks like it is out of The Jetsons ). I think we have almost become numb to how fast technology is advancing.

I agree with this wholeheartedly. It is amazing how frequently one reads about new labour saving technology (take a look at this video on autonomous fruit picking which looks like it is out of The Jetsons ). I think we have almost become numb to how fast technology is advancing. -

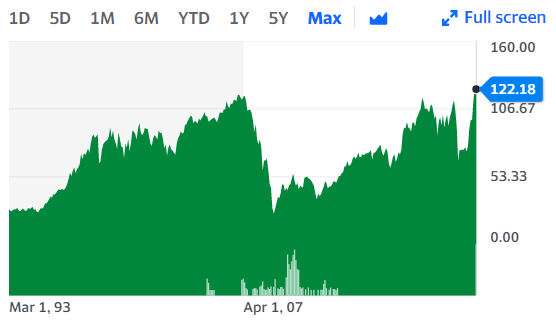

One obvious one is banks/insurers. The KBW Bank Index only recently exceeded its pre-GFC high (chart below https://finance.yahoo.com/quote/%5Ebkx/)

-

Why do people accept it? Because of the money illusion (https://en.wikipedia.org/wiki/Money_illusion) where most people think in nominal, rather than real terms. Inflation of 2% is small enough that most people barely notice it, and do not adjust their behavior much (i.e. still treat cash as a fine asset to hold). Why do governments accept it? Because the government can use it as a hidden tax on individuals. It's no surprise that when government deficits are large the same governments manipulate interest rates so that the real interest rate is negative (right now in the US the short term real rate is deeply negative, 10yr real interest rate is -0.60%). From a fairness standpoint it is very unfair to individuals who are not financially sophisticated, since these individuals would tend to have large amounts of cash or GICs. The rich largely avoid the negative effects of inflation as they tend to own things like equities which fare relatively better during inflations.

-

Agree with you here. One interesting thing to think about is that in response to a rapidly changing economic situation in 2020, the Fed conducted monetary policy in an 'emergency' fashion (i.e. inter-meeting cuts, cuts larger than 25bps). Given the nature of the COVID shock, and the potential for inflation dynamics to rapidly change in 2021/2022, it is not too crazy to think about the possibility they need to react in an emergency fashion to raise rates. Probably a low-probability event, but given it is not priced in at all it's interesting to think about.

-

Yes, and closely connected to the big risk that exists in the market. 10yr risk free rate of ~1% vs. a pre-GFC 10yr risk free rate at 4%+ has wildly different implications for where the broad indices trade. Ultimately it will be driven by the inflation outlook, and with the financial markets increasingly divorced from the real economy the assumption of a continued Fed put is a dangerous one. With this risk out there makes sense to stay defensive a be less sensitive to what the performance of the index is.

-

Right. I don't get it. We didn't have 6% inflation before covid, so what has changed? What has clearly changed is the attitude of governments, and the general population, towards running large budget deficits. To take the example of Canada, the Federal Government ran a $400bn deficit in 2020 (16% of GDP vs. 4% in 2009), and has not produced a budget in two years. This government now has a ~50% of winning a majority this spring (if an election is called), and there is very little appetite for austerity. One of the 'classic' causes of inflation is the government printing money since desired spending > taxes. The political dynamics around deficit spending ('build back better') are likely to be very different post-lockdown vs. post GFC so the low inflation experience of the 2010's is unlikely to be repeated. Deficit source: https://tradingeconomics.com/canada/government-budget

-

In 2017 1 of every 50 dollars of Canadian GDP came from real estate transaction fees! Source: https://www.cbc.ca/news/business/real-estate-fees-home-sales-1.4226630

-

If inflation is at 6% for a sustained amount of time central banks will have to decide between 1. Keep low rates while letting inflation run at 5-10% for a few years to decrease the real value of debts while the general populace grumbles (much like Canadians have grumbled about higher real estate) but asset owners do well. 2. Raising rates in a meaningful fashion, leading to the collapse of the entire financial system and bankruptcy of the governments that appoint central bank chiefs. My money would be on 1 being the more likely outcome.

-

Hence why I prefaced it by "on a much more speculative note" :D

-

I think when looking at a broader range of stores of value it is easier to see the currency debasement. Stocks/real estate being prime examples, trading cards (https://www.pwccmarketplace.com/market-indices) and fine wine (https://www.liv-ex.com/news-insights/indices/) being more esoteric examples. On a much more speculative note I increasingly am of the mind that gold is becoming a relatively poor store of value. It is not too big of a stretch of the imagination to think asteroid mining, while somewhat fanciful at this very moment, has the potential to impact precious metals' values in a big way over the next 50 years.

-

What would be so bad about that? I rather Central Bank's focus on the real economy and less on boosting financial assets. If main street is doing well with higher wages, better quality of life, and less inequity while stock markets are going down, I'm perfectly okay with that. But we don't really see that anymore. We can't withstand prolonged pain in the financial markets anymore. After some signs of distress, CB's come in with their massive rate cuts and QE infinity. I overall agree with you, one of the reasons the CBs/governments would not agree with you is because the 'common man'/'average voter' has become levered up ever since QE got going (see Canadian debt levels and real estate). Governments/central banks will do whatever it takes to try and keep these people out of a negative equity position, and will likely tolerate higher inflation.

-

This is the million dollar question for asset markets. Current prices for stocks/bonds/housing are all dramatically 'wrong' in a higher rate world, particularly one where higher rates are driven not by productive economic activity but by high government spending.

-

I am currently reading the book Studies in Hyperinflation and Stabilization http://www.centerforfinancialstability.org/hyperinflation.php which is a collection of oldish papers examining different hyperinflations which have happened through time. The first lesson they state (page xxii) is that "We, like others, have identified the cause of hyperinflation as the substitution of [money creation] for the tax financing of government expenditures" (i.e. when instead of raising taxes to finance government spending the central bank just prints). Now not wanting to dive into politics too much, but I think its safe to say in the US/Canada at this point there is very little appetite for the type of tax increases that would be necessary to fund the type of deficits of the past year, and are expected for the coming years. As well, the politically easy type of taxes that may be implemented (i.e. wealth taxes, tax on high income earners) will not end up generating that much revenue. With this in mind it is very easy to imagine a high inflation scenario (maybe not hyperinflation, but higher than most of us would have experienced in our lifetimes) over the next decade or so, the government keeps printing because it is the easy thing to do.

-

Worth remembering that the constraint on Fed's ability to control rates is inflation. All the jawboning in the world will not be able to prevent the market radically repricing the Fed's path if inflation starts showing up. M4 up ~30% YoY + economy is just about to open up + have some more stimulus coming down the pipe; a scenario that looks pretty inflationary to me. Buckle up. Source on M4: http://www.centerforfinancialstability.org/amfm_data.php

-

This whole episode makes me thankful for the existence of a professionally managed CPP in Canada. Sure, people may have their gripes about CPP (and them running ads), but at the end of the day having CPP as a backstop protects investors against themselves doing stupid stuff like investing in meme stocks.