maplevalue

-

Posts

331 -

Joined

-

Last visited

-

Days Won

2

Content Type

Profiles

Forums

Events

Everything posted by maplevalue

-

Where Does the Global Economy Go From Here?

maplevalue replied to Viking's topic in General Discussion

I guess what I am wondering is how much first time homebuyers having a hard time buying their first house is really going to drag on the economy. Inflation is an economy wide phenomenon, and I feel the factors driving inflation (supply chain, govt spending, etc.) are going to far overwhelm the economic impact of some millennials having to continue renting instead of buying a house. -

Where Does the Global Economy Go From Here?

maplevalue replied to Viking's topic in General Discussion

For variable rate mortgages my understanding (see here https://www.canadalife.com/investing-saving/mortgages/fixed-vs-variable-mortgages.html#variable-rate) is that if rates go up your payment stays the same its just the interest vs. principal ratio changes over the course the 5 year term. At the end of the 5yr term that is when you could face higher monthly payments. My original point being higher rates are not immediately leading to higher payments for those with variable rate mortgages. -

Where Does the Global Economy Go From Here?

maplevalue replied to Viking's topic in General Discussion

One thing I think about, and can't wrap my head around, is the economic sensitivity to higher rates in Canada. Canada has 5yr mortgages so payments more closely track where short-term rates go than US. However I suspect when all is said and done, and you account for the fact many mortgages are partially paid off, or based on mortgages taken out many years ago (i.e. lower prices), or that mortgages over last two years will not reset for another ~3 years (either because they are fixed, or the fact variable payments remain the same until end of term just the amount interest vs principal changes) the dollar amount that mortgage payments change with higher rates is not very high. Also for credit card debt nobody notices a difference between 20% rates and 22% rates, and for HELOC debt people are sitting on massive MTM gains on their houses so a small change in rates doesn't matter. So do we get a situation where the Canadian economy is on fire (reopening from crazy stringent lockdowns + commodity sector + Libs/NDP spending like crazy until 2024), rates are going up, but the economy doesn't respond? That is a really scary situation for asset prices if the BoC is 'pushing on a string' with its rate increases necessitating they raise rates even higher. -

Where Does the Global Economy Go From Here?

maplevalue replied to Viking's topic in General Discussion

It's true, the proportion of the population that doesn't like inflation represent a huge percentage of the electorate (particularly older people on fixed incomes). This is why today there is a heightened risk that central bank inflation targets get lowered (I think there is a non-negligible chance they get changed to ~0% CPI/PCE inflation). Just think about how popular a "no more inflation" policy would be from one of the candidates in the 2024 election. -

NTDOY

-

Where Does the Global Economy Go From Here?

maplevalue replied to Viking's topic in General Discussion

Hat tip to @crs223 for posting the Dalio video, I think it is worth a watch. @Viking I think you are correct in saying your macro ball is pretty cloudy. We are in a very uncertain environment with respect to the future path of interest rates (another way to look at it is the future path of where the Fed wants asset prices). Fed clearly behind the curve, economy at full employment, inflation at 8%, and likely Republican sweep of government coming by 2024 (remember what happened with long rates in 2016...they skyrocketed after Trump's victory). It is hard to say exactly where the market will go. However given market direction is a combination of fundamentals + positioning, I will offer the following two thoughts. i) The entire financial system is positioned for rates to go up but stay at historically low levels (market pricing overnight rate to go up to just north of 2%). A particularly egregious example of this positioning is in Canadian real estate where prices have become mind boggling on the back of variable rate mortgage rates of ~1%. I saw a tweet the other day of mortgage rates in 2006, where TD's 5yr fixed was ~7%. As a long-term investor, given the current macro environment you cannot rule out the possibility the regime has shifted and we are go back to more 'normal' levels of rates (fun fact if they made the overnight rate 7% today real rates would still be negative), and I think one's portfolio should be insulated against this possibility. ii) Many individuals such as Russell Napier have argued that because government debt loads are so high we are about to enter into an era of financial repression where rates are kept below inflation. While this is completely possible, what is different today is central banks are far more independent from governments than they were in past eras of financial repression, and hence more likely to push back against high inflation. -

I thought I would revive this thread to post some interesting commentary on EM I read recently. Obviously there is lots of discussion in the Russia/Ukraine war thread, and in individual investment threads (e.g. BABA), but I thought there would be value in having a place for a slightly more general discussion with respect to EM. This is especially relevant now given the large underperformance of EM over the past year (EEM -21% vs. SPY +7%). FT: Emerging markets: all risk and few rewards? https://on.ft.com/36dg3Gm Larger emerging economies appear to be in less immediate danger. But Ed Parker, head of global sovereign research at Fitch Ratings, a credit-rating agency, talks of “a long tail of weak, fragile frontier markets” that look to be at risk. Investors are particularly concerned about countries such as Ghana, El Salvador and Tunisia — not to mention Ukraine, should Russia invade. “This is not an abstract concept,” warns Parker. “Given the pandemic, many of them are much less able to withstand the shocks that could hit them this year.” Six countries have already defaulted during the pandemic: Argentina, Belize, Ecuador, Lebanon, Suriname (twice) and Zambia. ... The outlook is not wholly bleak, say analysts. Many emerging economies are much better placed today to withstand such difficulties than they were in the past. Previously, persistent and deep current account deficits made countries vulnerable to external shocks and dependent on foreign finance. Now, in aggregate, emerging markets are running a current account surplus. Many, including Brazil, South Africa and India, have substantial reserves of foreign exchange and deep local capital markets, which offer protection from swings in exchange rates and in foreign investors’ appetite for risk. FT: Letter: South and east Asian countries offer the best places to invest https://on.ft.com/3J75un9 It is time the Financial Times grew out of using the generalisation “emerging markets”, a lazy way of covering the majority of the world (Big Read, February 16). Whatever the problems of a few middle-size economies like Turkey and Argentina and a myriad little ones such as Belize and Suriname, just a brief glance at currency rates alone would show continuing sustained levels of confidence in the large majority of south and East Asian countries. Currencies of these mostly externally-oriented economies have been stronger than the euro and the yen over of the past year. The Vietnam and Taiwan currencies have risen against a strong US dollar and the Indian, Indonesian, Thai, Malaysian, Korean and Philippine ones have been roughly stable on trade-weighted terms. Sri Lanka may be in crisis but the vastly bigger Bangladesh economy has been growing, albeit slowly, all through the pandemic. ... Although some economies, notably India and the Philippines, were especially hard hit in 2020, India has led the world with 12 per cent bounceback growth in 2021 and Indonesia’s gross domestic product is back above its 2019 level. Growth is back in Kazakhstan — and never stopped in Uzbekistan, the most populous state in central Asia. The inflationary impact of supply chain problems so far seems greater in rich countries, meanwhile most commodity prices have been buoyant. Future growth will be slowed by demographics everywhere, especially Europe and China, but there is nothing to suggest that well-run younger countries will not remain the best places to invest.

-

https://www.bloomberg.com/news/articles/2022-03-07/fairfax-is-said-to-weigh-selling-stake-in-iifl-wealth-management Fairfax Financial Holdings Ltd., the Canadian investment firm run by Prem Watsa, is exploring the sale of its stake in Indian financial firm IIFL Wealth Management Ltd., according to people familiar with the matter. The Toronto-based firm is in early-stage talks with potential bidders for the stakes, said the people, who asked not to be identified as the information is private. Other major shareholders including General Atlantic could also consider joining Fairfax in selling their own stakes, the people said. IIFL Wealth shares fell 1.2% on Monday, giving the company a market value of around $1.7 billion. A vehicle controlled by Fairfax holds about 13.6% of the firm’s shares, while General Atlantic has a 21% stake, according to data compiled by Bloomberg. Deliberations are ongoing and the investors could decide not to proceed with the sales, the people said. Representatives for General Atlantic and IIFL Wealth declined to comment, while Fairfax didn’t immediately respond to requests for comment outside business hours. Founded in 2008, IIFL Wealth offers solutions for high and ultra-high net worth individuals, family offices and institutional clients, according to its website. The Mumbai-based firm has more than $44 billion in assets under management.

-

You raise very good points about why investing in an authoritarian country like China differs from a more free-market one like the US. With that being said China trades 11.5x forward PE vs US at 19x, partly as a result of sentiment being absolutely terrible towards EM right now. My feeling would be valuation + China easing COVID zero policies + Chinese monetary easing provides a decent setup for Chinese stocks right now.

-

https://www.cicnews.com/2022/02/canada-immigration-levels-plan-2022-2024-0221165.html#gs.p4r2bw The Canadian government has just announced its Immigration Levels Plan 2022-2024. Canada is increasing its immigration targets yet again. It will look to welcome almost 432,000 new immigrants this year instead of its initial plan to welcome 411,000 newcomers. The announcement came today at approximately 3:35 PM Eastern Standard Time. Over the coming three years, Canada will target the following number of new immigrant landings: 2022: 431,645 permanent residents 2023: 447,055 permanent residents 2024: 451,000 permanent residents Also a reminder that over the past 12 months the MLS Housing Price index is up 26.6% (https://www.crea.ca/housing-market-stats/mls-home-price-index/hpi-tool/).

-

Here it is

-

I think I heard on Bloomberg Radio that the full interview gets released tonight at some point.

-

Well obviously if you get a 10yr yield at 10% stocks will probably be lower. However, it would seem from the history that US 10yr yields could go up another 300bps to 5% (this would truly be an enormous move, and I doubt the economy could really handle it -> inflation wouldn't be a problem) and stocks could still do ok.

-

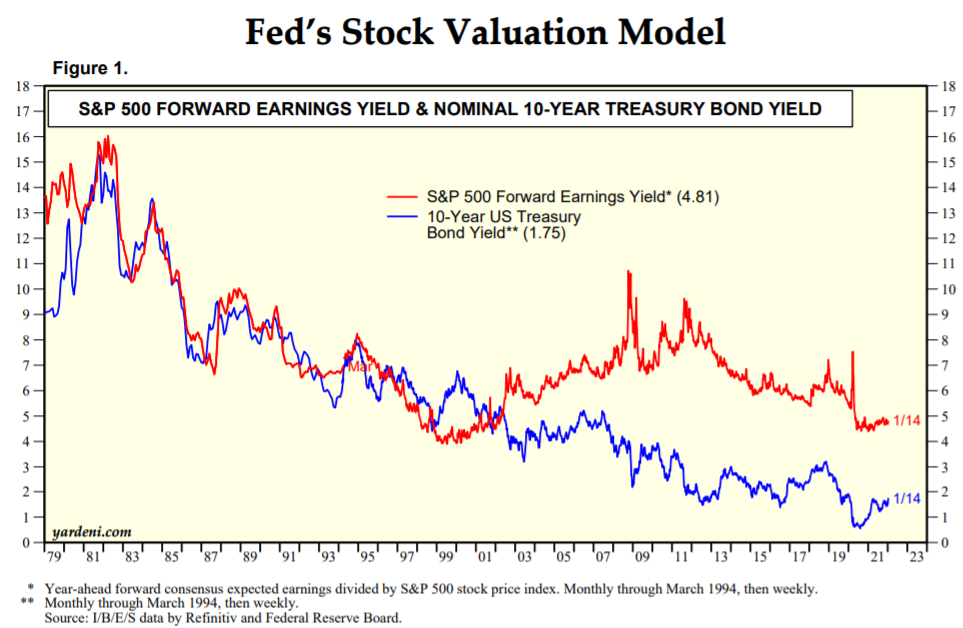

Whenever I get nervous I just look at this chart. Sure the Fed tightening is helping inspire a selloff, but at the end of the day stocks still look good relative to the alternatives out there. https://www.yardeni.com/pub/valuationfed.pdf

-

Investments Benefitting from Higher Interest Rates

maplevalue replied to maplevalue's topic in General Discussion

Thank you for all of the terrific suggestions. It has given me a lot to think about. One that hasn't been mentioned that has piqued my interest is BDCs. They all differ, but they tend to provide floating rate financing to mid-market companies. So as rates go up your income is protected. Here is an article which talks about them https://www.kiplinger.com/investing/stocks/dividend-stocks/602058/need-yield-try-these-5-best-bdcs-for-2021. I need to do more work since many of them are externally managed (general negative), and of the internally managed ones many trade at rather high P/B ratios (MAIN trades ~1.85 PB). -

Never said immigration would create more per capita wealth or would inflate wages. What immigration does do is make more people compete for the same amount of land, bidding the price up. In places like the GTA there are a host of restrictions on building new houses, so the only way to build is up, which makes existing houses (i.e. ones with a backyard) more expensive.

-

Next Thirty Years - Real Estate or Equities?

maplevalue replied to valueinvestor's topic in General Discussion

I would agree on the comments of it depending on your expected future cash flow. If you have a stable-ish job, and expect to be paid uninterrupted for a decade or so, and are happy living in the same place it probably makes sense to own real estate. In Canada the first 5 years you will have a mortgage of 2%, and inflation will be 2%, so you are effectively borrowing 'for free'. There would be two other considerations I might point out taking money from equities to real estate. i) Future taxation - In Canada I just cannot see how real estate does not get taxed more heavily in the future, especially at the high end (what could be more politically appealing in a left leaning country like Canada than a mansion tax!). Governments are massively in debt and have to pay for baby boomer healthcare somehow. One of the things higher prices have done is increase the proportion of renters in society, particularly in the GTA, so the political opposition to increased property taxes is probably less than in the past. ii) Correlation with the 'everything bubble': At least with equities, particularly if you take a value approach, you can construct a portfolio that can perform decently even in adverse market/economic conditions. With real estate you are praying that the QE induced asset price inflation we have seen over the past decade continues into the future. In the event that monetary policy is forced to becomes more significantly more restrictive the value of your real estate will become exceptionally sensitive to the whims of a bunch of PhD bureaucrats at the Fed/BoC. So you want to make a determination how comfortable you are with that. -

CAD govt in particular can always lean on increasing immigration. Current target 400k/year; they could just do 500k and voters would probably not care (voters do not really care that they have ratcheted it up to 400k already). Many of these people move to the GTA. Same amount of land + more people = soft landing for real estate.

-

With the Fed about to begin a hiking cycle, I would be curious to hear the community's thoughts on investments that will do well in a higher rate environment. Specifically ideas that would do well if the Fed had to hike significantly faster than what is priced in. Right now Eurodollar futures have the Fed hiking to ~2% by 2024, so I am thinking of what would do well in a scenario where the Fed has to hike to 5% in a similar timeframe (for context the Fed was at 5.25% before the 2008 financial crisis). Rates at 5% could mean GDP growth is good, or GDP growth is bad, so feel free to share ideas for either case. Some 'textbook' ideas include insurers, banks, and commodity producers. Although with many of these breaking out to new highs it would be interesting to hear some more niche names/sectors that could stand to benefit and are less in favour than the aforementioned sectors. For example, a more niche idea is rate reset preferred shares trading at a discount (since they trade at a discount as rates go up their coupon increases more than the rate increase).

-

Is there a value rotation going on today?

maplevalue replied to BG2008's topic in General Discussion

The move over the past few days feels like a bit of a headfake. Classic scenario where market goes into a new year and everyone has read year ahead pieces talking about higher interest rates, tech is overvalued, bull market in commodities, blah blah blah. The market may move that way over time but it feels like it has moved a little too fast this week. -

2021 IRR of 14.02% across whole portfolio; was a decent year considering ~33% of my portfolio is EM. Just looking at my single name stock picks it was 26% (about 1/5 of my portfolio). Was more active this year thanks in part to being part of this great community. Hope to get more active in 2022.

-

Truly amazing to read this book in the context of the massive past, and continuing, government (including the Federal Reserve) intervention in the economy since March 2020. Some summaries/quotes below (from the IEA edition) Pg15 government has no resources of its own, the only way a government can give one person money is to first take it from another person…doing so represents the forcible using of one person, through the tax system, to serves the purposes of another. That is a form of immorality akin to slavery” Pg20 his greatest contribution lay in the discovery of a simple yet profound truth: man does not and cannot know everything, and when he acts as if he does, disaster follows. He recognized that socialism, the collectivist state, and planned economies represent the ultimate form of hubris, for those who plan them attempt – with insufficient knowledge – to redesign the nature of man. Pg35 the more the state plans the more difficult planning becomes for the individual Pg42 when economic power is centralized as an instrument of political power it creates a degree of dependence scarcely distinguishable from slavery Pg49 democratic assemblies cannot function as planning agencies. They cannot produce agreement on everything – the whole direction of the resources of the nation – for the number of possible courses of action will be legion. Pg49 to draw up an economic plan in this fashion is even less possible than, for instance, successfully to plan a military campaign by democratic procedure. Pg54 to make a totalitarian system function efficiently it is not enough that everybody should be forced to work for the ends selected by those in control, it is essential that the people should come to regard those ends as their own. This is brought about by propaganda and the complete control of all sources of information. Pg57 hence the familiar fact that the more the state plans the more difficult planning becomes for the individual Pg59 no difficulty about efficient control and planning were conditions so simple that a single person or board could effectively survey all the facts. But as factors which have to be taken into account become numerous and complex, no one centre can keep track of them….under competition – and under no other economic order – the price system automatically records all the relevant data Pg60 any further growth in economic complexity far from making central direction more necessary, makes it more important than ever that we should use the technique of competition and not depend on conscious control Pg68 with every grant of such security to one group the insecurity of the rest necessarily increases. If you guarantee to some a fixed part of a variable cake, the share left to the rest is bound to fluctuate proportionally more than the size of the whole Pg70 the guiding principle in any attempt to create a world of free men must be this: a policy of freedom for the individual is the only truly progressive policy

-

NTDOY

-

"Bankers know that history is inflationary and that money is the last thing a wise man will hoard." - The Lessons of History by Ariel & Will Durant (one of Dalio's favourite books)

-

+1 (although technically it will be even better than a treasury since it has inflation protection!)