changegonnacome

-

Posts

2,703 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by changegonnacome

-

Maybe headline CPI drops to those level (sub-4)......but what the Fed is watching is 'supercore'.....or what I just outlined on services....its unlikely to move without a significant move up in the unemployment rate Making people feeling poorer.....or acting with recessionary mindset such that they rein in their spending, up their savings....is part of Fed's game here.......the USA spending monster needs to be put back in its cage for a while, but its a mighty beast and isnt stopped easily!......Wall St/Tech St will help for sure......the banking failure headlines reminiscent of 2008 are helping here too for those on Main St. who remember.......but spending numbers, big picture, are led by Main St......and some pain has to flow through there unfortunately.

-

The month over month data is showing specifically services as the single biggest problem.....if you look at my posts from months ago you'll see me speak about domestically produced goods and services as the source of the problem and given that America produces actually very few goods it consumes and is mainly a service led economy this is where the inflation is showing up....Why? Because services costs are mainly driven by domestic wages. And we have unusually high wage increases. In the last inflation report just released service costs are continuing to rise at 0.5% monthly clip......not in 2022, not during COVID, not in weird base effects or YoY quirks .........right here, right now........that's 6% annualized.......service items include things like package delivery, haircuts, hotels, gardening services etc etc. Its a long long list....if it doesn't come off a factory line, its a service. So thats services..........the problem with inflation and the story from previous inflationary bouts is that if it present in one significant sub-category long enough, say services in this case, it in time transmits or flares back up in other categories........inflation has its own long and variable lags across categories.....services inflation sitting at 6% as it is........almost ensures in time that we will see domestic goods prices 'flare up' again later this year. Inflation then since Spring 22 on a YoY basis, moment in time......across all categories averaged out is likely running at 5.x%ish....modestly below the YoY prints with a higher numbers we are seeing in headline CPI. Based on current MoM reports and seeing really services as the problem....and knowing services make up ~77% of the USA economy as per 2021 data.....short hand, back of the envelope math then would be 6% inflation in services with other categories CURRENTLY showing modest inflation or none..... 6% haircut by its proportion of the US GNP (77%) = 4.62% is my estimate of CURRENT contemporaneous inflation driven almost wholly by services. That 4.62% estimate lines up pretty well with my model of looking at only two other data points.....nominal spending/income/wage growth (BLS data) against productivity growth.........again the delta there suggests we should have mid-4's inflation in 2023...simply based on the MoM payroll increases we saw in Jan.....against the common sense idea that the USA does not have any easy output (productivity) wins left with unemployment at 3.7%. As much as we may want it to - inflation is not just going to 'go away' by itself that idea is not supported by the data....it will require a change in aggregate nominal spending and/or a productivity output miracle....if we rule out miracles.....its going to require spending to fall significantly...given there are only two sources of funds for spending in the real economy.....credit & income (jobs).....credit needs to get whacked......but credit fueled spending is only a small part of TOTAL spend.....income from jobs is the most important source of spending........hence JPow might not say it......but creating some level of unemployment is going to be required here to rein in spending growth such that it exceeds productivity growth by only 2%...and we get 'back to 2'

-

Absolutely - I think of it like this.........the asset side is all about culture and management....and its this side of the biz that ordinarily get the common equity holder zeroed..........you need uncommon common sense mgmt and prudence to run the asset side of bank....you need an underwriting culture........this is the hard part to be sure of in bank anyalsis. The liability side in some ways is easier IMO - does the institution display an ideally seasoned/historically verifiable low cost sticky deposit franchise.....diverse, un-concentrated, geared to stable or growing sectors/geographies such that you can model out that deposit base. SVIB in some ways unusually got zeroed on both sides of the b/s......they messed up the asset side with duration risk........while not realizing they had a hugely correlated, concentrated and digitally flighty deposit base.....it was a fatal mix.

-

Inflation at 6%......probably coming down to 5.x% in a couple of Q's......Fed Funds at 4.57%.......so we are STILL after all the baloney, bank blowups and ink spilled have a negative REAL inflation adjusted Fed Funds rate. People don't borrow at the Fed Funds I hear you say! Exhibit A - Personal Line of Credit from FRC no less @ 3.95%......inflation is at 6%!!!!!! Thats a negative 2.05% cost of carry for this debt that you can pull down and spend on goods and services today....in an economy with an inflation problem. Remember the classical defintion - too much money chasing too few goods and services! Does that PLC strike you as financial conditions that are too tight? https://www.firstrepublic.com/personal-line-of-credit?gnav=globalheader;personal-personal-line-of-credit In terms of tighter financial conditions themselves......we are getting there - post SVIB blow-up....... a deposit interest rate war is likely to start & a flight to treasury's......NIM's will get killed......banks will react by either curtailing credit creation or raising the rates they charge meaning the TAM for loans on a DTI basis or just loan demand itself will just fall of a cliff. This is the PLAN - the Fed could have done without SVIB blowing up but they definitely want credit creation to be curtailed. SVIB is going to accelerate credit getting whacked. So back to the basics: Remember only two sources of funds that become nominal spend in the REAL economy are - credit & income/wages. Remember the USA is at 3.7% unemployment...way below the natural rate....with horrible demographics and a dysfunctional immigration system...so whatever productivity growth miracle dreams you have forget them. Productivity is not surprising to the upside here to help FIX inflation. How could it...forget fantasies about kicking bums of medicare....or free childcare for everybody. It aint happening in the next two years if ever. Period. Remember that the inflation rate is the delta between the growth in nominal aggregate spend & the growth in productivity (or put another way an increase in the REAL volume of goods & services being produced YoY against the volume of additional spend occurs). So you can see the only way to reduce the delta between nominal spend & productivity is if you've hit the only two things you have any control hope over controlling - credit & wages. SVIB is likely a credit event in system.......that will markedly change credit creation dynamics moving forward. Less credit driven spend will in turn lead to lower spend, lower spend results in a need for less workers....which hits that second source of funds - wages/income that turns into spend. Post SVIB I think its possible the terminal rate will not need to go as high as previously thought.......the terminal rate question is kind of pointless guessing game at this point......25-50bps or there about's.....who cares exactly.......its headed to 5.x%-ish as JPow knows it needs to be there to at least be restrictive or neutral (inflation adjusted!)....the effect they are looking for & their resolve is the most important dot plot to watch out for.....and what I see is a Fed that isn't likely moving that rate until unemployment moves meaningfully into the 5% range....and what folks are going to find IMO shocking is how they are going to hold the Fed funds there and for how long.....as people, commentators, folks inside the beltway squeal murder......and the indices roll over & corporate profits roll over. The Fed is very likely to make a 'new' mistake, they are only human after all.....but they wont make the 'old' one......which is cutting too soon! There is too much institutional knowledge still around from the 70's to do that and JPow has spoken enough on this point to suggest to me he will in the future be accused of lots of f-ups...the most glaring will be the late 2021/early22 accommodation/transitory stuff....the one f-up they wont pin on him is cutting too soon in 2023 such that inflation flares back up in 2024/25. It aint pretty this, as we've seen that with SVIB.........but there isn't another way out of this setup. If you got any workable* ideas write him to me here I'd be interested to hear them.......and then post them to Constitution Ave., Washington D.C. * a workable solution is not one where you claim inflation doesn't exist and its a hoax.............the second non-workable solution is to do a JPow 2021 impression and claim its all transitory and inflation is already over

-

-

You've nailed it in Charlie Munger style conciseness - beautifully put - its unpopular but its 100% true. The Fed has two mandates - price stability & more recently employment........they will never say it out loud but they know and their public pronouncements confirm that one mandate supersedes the other........their 'real' goal is to maximize employment inside of the 2% inflation target because they know that doing so actually minimizes aggregate misery in the short run & optimizes stability and future growth of the US economy in the long run. Its hugely desirable.

-

Lots of chatter out there around why Signature Bank was so aggressively shut down when it seems it was still able to meet deposit demands. The story goes that regulators now want crypto exposure expunged & lanced from the US banking system. Why? Because they are beginning to come to the conclusion that a collapse in the crypto ecosystem (FTX) jumped like a virus into the traditional banking system compounding over time via Silvergate into the SVIB collapse. So the story goes that US regulators........are beginning to trace the SVIB bank run......back first to FTX......which caused a run on Silvergate as crypto bros all demanded their money back ASAP & where Silvergate had asset-liabilty mismatches and collapsed. This effectively began a search for 'Silvergate like' bank balance sheets and SVIB fit the bill.......and well the rest is recent history.............just shows that risks have a strange way of compounding and the 'tiny' crypto market long considered NOT systemic too small to matter can end up mattering alot. In this instance one can argue that the crypto tail started wagging the US financial system dog.

-

Lots of chatter out there around why Signature Bank was so aggressively shut down when it seems it was still able to meet deposit demands. The story goes that regulators now want crypto exposure expunged & lanced from the US banking system. Why? Because they are beginning to come to the conclusion that a collapse in the crypto ecosystem (FTX) jumped like a virus into the traditional banking system compounding over time via Silvergate into the SVIB collapse. So the story goes that US regulators........are beginning to trace the SVIB bank run......back first to FTX......which caused a run on Silvergate as crypto bros all demanded their money back ASAP & where Silvergate had asset-liabilty mismatches and collapsed. This effectively began a search for 'Silvergate like' bank balance sheets and SVIB fit the bill.......and well the rest is recent history.............just shows that risks have a strange way of compounding and the 'tiny' crypto market long considered NOT systemic & too small to matter can end up mattering alot. In this instance one can argue that the crypto tail started wagging the US financial system dog.

-

This is the same Jason Calacanis from "All In" fame - that was doing Mad Max tweets over the weekend begging that SVIB be rescued.........that it was the backbone of the US economy! Silicon Valley Bank its clear was a cookie jar with a banking license attached for the VC community.........it seems it stopped operating as a true bank years ago.....it had become a lapdog for its VC/founder clients......its business model was predicated on ever higher and higher tech valuations & 'exits'. The reason nobody is stepping into buy the bones of SVIB USA - is that the business model was an uber-leveraged play on the tech bubble.....in short SVIB's loan book, I'm guessing, for those that looked it over is an inter-tangled mess of correlated personal and business loans in VC land......in short a prudent bank would think about SVIB for five seconds and know its likely a toxic steaming pile of crap thats unravelling day by day.

-

Good thread below and kind of what we talked about before……sweetheart deals for your company loans…..and sweetheart personal banking deals for the execs at the company to buy homes, planes and boats When people say this isn’t a bailout……they need to understand that SVIB was a Silicon Valley circle jerk/cookie jar where everybody made out like bandits using a banking license……..that turned out to be too big to fail…..people are saying bond holders and equity holders are getting wiped out….partially true…..what they don’t say is that Roku was an effective bond holder in SVIB and is getting made 100% whole! They and lots of other ‘founders’ risked company cash for preferential personal and corporate lending benefits….and lost……these were not mom and pop depositors. I understand the greater good argument and on balance something had to be done here…..but man it sure feels like the well heeled gambled, benefited, lost and are getting bailed out again.

-

The Fed has created a two tier banking system…..GSIB’s and everybody else……FDIC deposit insurance should explicitly be doubled or tripled for these regionals and quickly…..the man on the street doesn’t understand MBS lending facilities……but he understands the credit and faith of the US gov.

-

Feels like this whole debacle is gonna aid the Fed’s aim of hitting/reducing aggregate demand via reduced spending……a deposit interest rate war is about to ensue in the banking sector……growing the asset side of a bank balance sheet would be imprudent moving forward…..I expect lots of credit creation restraint….credit is about to whacked….and given credit turns into spending in the real economy this will be meaningful. In short SVIB has done in two days to ‘financial conditions’ what the Fed had failed to do in months. IMO SVIB isn’t the end….but it is the end of the beginning. To steal a phrase! Q - ”Is the Bottom Almost Here?” A - “Almost, but not yet”

-

Yeah the way I think about it they turned a bank run into a bank walk……but they haven’t saved banks with shitty biz models & screwed b/s forever forever…they will shrink/die over time….this funding window is for a year….think of it like a controlled detonation as opposed to a dirty bomb.

-

Buffet suggested this many moons ago.......that a bank account would come with FULL mandatory deposit insurance coverage.....that insurance being provided by a private entity incentivized to assess the risk of each bank model when providing coverage fee quotes......the rational of which would say that deposit account insurance premiums would rise on banks displaying riskier or more flawed business models......and reduced for those whom were very likely never to have to call on said insurance. The FDIC system, to my understanding has some small differentiation of risks in its premium calcs, but in reality it has a bit of free rider problem.........imagine pretty much everyone getting charged the same for car insurance.......your DUI saddled uncle & your aunty who never goes over 40mph paying pretty much the same.

-

The precautionary principal would suggest that anybody with a brain would not keep a penny in these banks over the $250k limit......end of story......so I expect the banks with question marks over them to see significant deposit flight.....they wont fail now like SVIB/SBNY with the additional lending facilties backstopping asset/liability mismatches on MBS portfolios .......but whatever profit expectations existed for them last week is out the window now......their funding costs are going to go through the roof and RoA/RoE will plummet

-

Or at least the taxpayers should get 'dealt in' on all various initial coin offerings moving forward.....seems fair......we clean up the shit in exchange for shit coins

-

Most likely & most virtuous explanation.......is that Roku had some corporate lines of credit/revolvers with SVIB that REQUIRED them to maintain corporate cash balances in SVIB accounts & not sweep as part of the covenants on the loans etc.. If not.......its just incompetence or else skullduggery......the least flattering reason would be a scenario where the CFO/Treasury functions in these institutions effectively got kickbacks on their personal banking relationships with SVIB (mortgages, POC's etc.).....money is fungible......and so to can be 'rewards' for clients/customers

-

“Enjoy the Academy awards” Bill deserves an academy award for his performance as a concerned citizen over the last 48hrs!

-

Good man Bill Ackman- planting the idea of bank runs in peoples heads is how you start a bank run! Beautiful - when folks compare Ackman somehow to Buffet, I laugh.....imagine Buffett out there on Twitter spaces, shooting from the hip and predicting catastrophe & calamity. He'd never dream of it, even it were true....lest he contribute to making it come to pass. Bill on the other hand....whom people listen to and follow......saying Monday is basically bank run starting gun. Its a wildly selfish way to get attention & feed his ego (at best), wildly cynical if has some position on that stands to benefit.

-

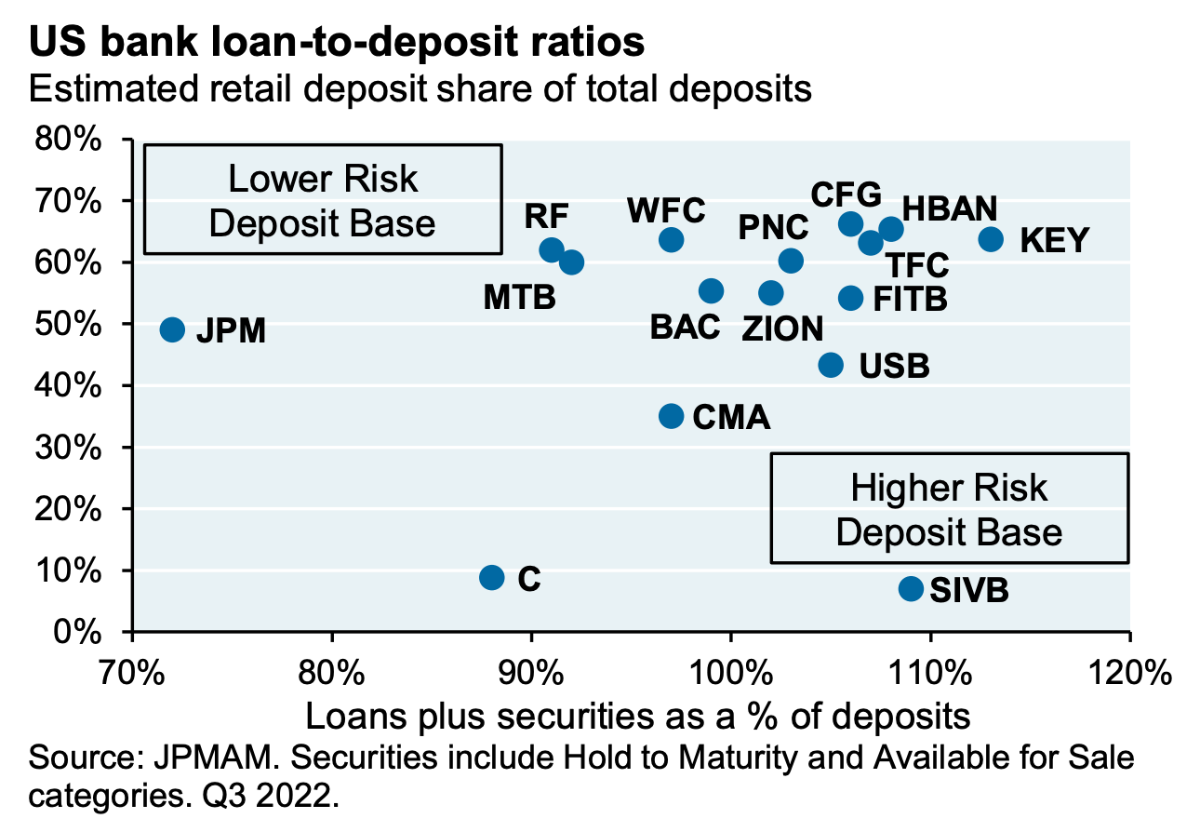

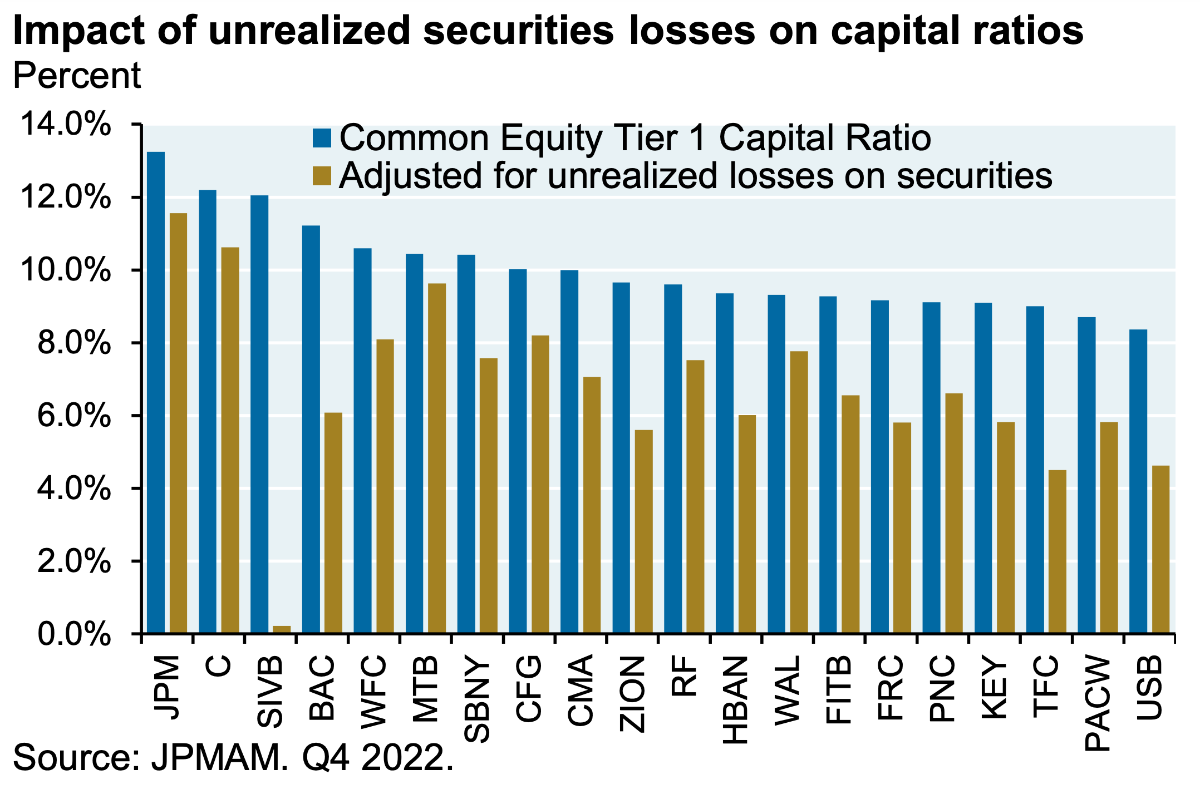

You can see here just how far offside SVIB was relative to peers - whatever way you frame this.......its gross management incompetence bordering on criminal negligence. https://am.jpmorgan.com/content/dam/jpm-am-aem/global/en/insights/eye-on-the-market/silicon-valley-bank-failure-amv.pdf

-

Agree - loading up with that stuff back in 2020/21 because "what else are you gonna do" was crazy.......unless you had to hold long dated paper specifically the answer was to take your bumps in shorter duration stuff and leave some NIM's on the table and let lesser men pick up that paper...........like what were 10yr MBS gonna do.....go to 0.5%!. They were asymmetric trades.....just not the good kind.

-

Yep I wonder all the time. I think an incestuousness exists in the Valley in big tech that is under appreciated............at the bottom of conveyor belt of VC funding, pass the parcel and mark to next round paper gains............is GOOG & META selling access to the clicks, installs and users required to make the 'blue sky' growth math work.........it is predicated, always on the greater fool theory, but once the greater fool doesnt show up.........well coughing up for clicks/installs starts to look more like a fools errand. The quantum of this type of "CAC your way to VC heaven" spend is hard to figure out.....but it aint zero......

-

Inflation is stealing a little bit of everybody's job daily but especially those on the poorer end of the spectrum. Economists talk about a 'misery index' which is simply the unemployment rate added to an economies inflation rate. I think that little number is actually quite important and speak to the more nuanced point you seem to miss....presently we are at about a score of 10 (~6% inflation & 3.5% unemployment).....pre-pandemic we had misery index score of 6.....THAT was a great economy.......having a job but being unable presently or in the future to cover your household expenses is indeed miserable.......folks talk about a great economy simply on one measure alone 'unemployment'....its myopic & stupid.....how do I know.....look at consumer sentiment survey's, political polling.....a 3.4% unemployment with that jaundiced view should be screaming positivity and happiness......but it isn't....people are miserable.........why........cause inflation is picking peoples pockets & they feel insecure about the future. I think Greg you simply consider inflation to be a nothing burger....that a 5% inflation rate is a 'whatever'.........with that framework of course you look at the Fed raising rates, engineering a slow down & creating unemployment......as some kind of monstrous act pointless destruction. If you don't believe its a problem....ultimately......we have been talking past each other these past few months. However in my world when you balance the pros and cons..........the pros of 2% predictable inflation on investment, aggregate household budgets, societal stability etc........getting 'back to 2' is a hugely important, hugely desirable and the noble thing to do.......JP & I are in crushing agreement. Lets see if he follows through once the going gets tough!

-

Exactly - inflation manifests itself in different inputs, at different times in unpredictable waves for a producer.....inflation is a mental overhead tax for a business......just ask someone running a enterprise in Argentina for the last 40yrs............its why, all things being equal, inflation is barrier to long run planning & investment......the future trajectory of prices/inputs/margins becomes unpredictable.....at the edges corporates back away from making productivity enhancing capital investments as the IRR on projects, always foggy, gets foggier still. You dont miss your water till your well runs dry.......and you dont miss 2% inflation until............

-

I dunno Greg - I think your seeing conspiracies where none exist.....rather what we have is a bunch of participants in the political economy acting at points in time as you would expect them too..........voters/the population were scared by COVID, politicians acted to 'protect' them, in doing so people (voters) needed to be bailed out, the politicians responded with bailouts, the bailouts were widely popular with voters........and so the politicians tripped over themselves to do even more....so they could get re-elected in 2021/22.........they did too much for too long & we got inflation....the monetary authorities too lest they be accused of not doing 'enough' to fight COVID in that period, kept financial conditions too loose for too long....they messed up now and are trying to fix it. You put the too together and you begin the chain reaction of monetary inflation we have now which is self-reinforcing. Indeed the next cognitive policy error is where the monetary authorities...........getting beat up by Elizabeth Warren on TV a few more times & becoming widely unpopular as unemployment climbs up to 4-5%.........fools themselves into thinking that the inflation fight is complete and they begin to cut rates too early & inflation returns. The other expected policy error with the fiscal authorities to come next is to continue to espouse their hate for inflation.....while simultaneously fueling it.......CPI like increases to social security.........more borrowing/more spending bills etc. I don't see a conspiracy here.......I see what I usually see.......people doing what is expedient and repenting later.