changegonnacome

-

Posts

3,854 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by changegonnacome

-

On the contrary - rolling over saves this administration a bloodbath at the midterms.....the tolerance for economic pain in the USA is basically zero.....its why the debt & the deficit is so bad....one can view it as the cumulative deferral of pain over time Not much at all.......the information bubble in China is all encompassing.....Captain Chaos can cast a reality distortion field around maybe 25% of the US population.......Xi manufacturers reality in China his algebra is much much different.

-

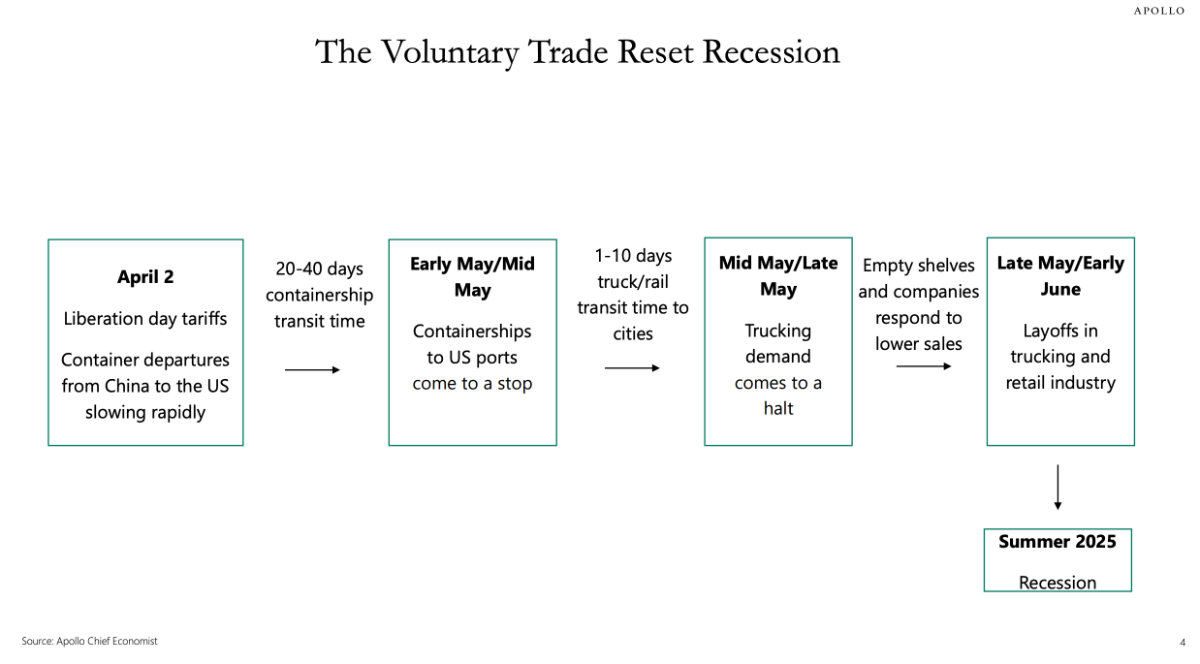

Poor Scott - trying to side step the White Lies from the White House re: negotiations......seems to me like China is calling Trumps bluff on this......and Captain Chaos is going to fold first (already has to a certain extent).....China must know they have him where they want him when Trump feels the need to effectively makeup bilateral contact between the two sides on the negotiation when there's been it seems basically none. I know there's an asymmetry on the % of the economy exports make up for each side and on the pure math side the USA 'wins'- but I think what we are seeing now is that you can measure economic pain and come up with the wrong answer......the question is rather pain thresholds......and the pain threshold for the American population/leadership is just so much lower as compared to what the Chinese population/leadership will endure these are folks working 9-6-6 in a surveillance state. Xi has 99 problems but getting forced to roll over isnt one. @Spekulatius posted this from Apollo along with a bunch of other charts - https://www.apolloacademy.com/wp-content/uploads/2025/04/042625-ConsumerandFirms_v2.pdf

-

Yep Trump dropped a tweet yesterday saying "makes me think that maybe he (Putin) doesn't want to stop the war, he's just tapping me along, and has to be dealt with differently, through 'Banking' or 'Secondary Sanctions?'" You think Donald? You think maybe your approach of dunking on Zelensky helped that maybe? Trump's initial capitulation strategy re:Putin was always a terrible maneuver to end the conflict.....all it did was ultimately provide encouragement to Putin that all he needed to do was stay the course and the Americans would drop out.....clear now IMO that the correct thing was to escalate to later de-escalate (maybe we still do that)......a side on the ascendency on the battlefield, as Russia is, has little incentive to get to the negotiating table and even if they do come they are likely to have outrageous demands as is the case now.

-

Lets see about all this democracy stuff. Reality is this buffoonery is creating a lot of market opportunity for which I'm eternally grateful to Captain Chaos for......all bets are off if he sends the global economy over the cliff....but we arent there yet.....right now we're in the buffoonery stage.....which is vol paradise......my base case remains that Trump is a man of no real principals except a need to be the centre of attention and liked/lauded.....this type of man isn't say a Paul Volker will to do painful things....principled, committed, steadfast in what needs to be done.....Trump is an inflatable tube man......the prevailing winds blow his opinions , 'principles' and actions around.....and strong winds are brewing from the East......his trade 'war' with China is toast...cause it needs to be....its economic suicide and those midterms are just around the corner

-

I taught Trump was trying to stop the use of "they/them"

-

Totally agree - the old two party system has started trading constituents.....and so things aint what they used to be....the BIG question is whether the MAGA constituency can be held together after 'the big guy' isn't around anymore......my gut is Trump's inherent narcissism wont allow for the rise of a successor who can hold the group together......caveat to that is I think he would do succession its dynastic - so Don Jnr. being the obvious one. I wish Trump success on this tariff gambit cause if he messes up the economy, stokes inflation my biggest fear remains he creates a successful populist movement of the left that comes to dominant the democratic party and gets AOC or worse into the WH with a congressional majority that allows really stupid things to happen to taxing, regulation and spending.....we are getting closer to that everyday this trade war escalates.

-

I dunno - I dont think you give him enough credit if anything the old man has shown a lot of flexibility over the years to do 180's on issues and claim it was always so. I think Trump has a lot of ideas loosely held as Munger would say.....he is not fundamentally anchored to a political philosophy (outside accumulating money, attention & holding on to power) he has IMO a lot more mental wiggle room than most traditional politicians who are slavish idealogous.

-

For sure.....and you'll like this.......I blame the democrats the most....cause aren't they fundamentally the wealth redistribution party? The issue with the democrats is they've been run fundamentally by technocratic coastal elitists who had no idea how bad things had gotten outside the bubble of NY, Boston, SF etc.

-

Trump says we are in talks with China China says what talks? there are no talks occuring What a shit show - but make no mistake Trump is trying to figure out an off ramp here.......small and medium sized businesses with inputs from China are in the process of going to wall........sticker shock at Target, Walmart & DG are a few weeks away........and that ~June annualized MoM 6% CPI print is incoming. I hope some genius in the admin is also deducting from the tariff 'windfall' the Social Security Cost-of-Living Adjustment (COLA) that are going to flow through to seniors on foot of the increased inflation....an incremental 400bps of inflation captured by COLA would cost an additional $56bn annually in social security payments or half a trillion over ten years!

-

Indeed - the rust belt turned into a dystopian nightmare not because of China and trade but because of a failure of US politicians local, State and Federal to recognize those communities needed incremental support to help transition to new industries and activities (education/re-training/subsidies etc.). Its quite convenient after 40 plus years of quite astounding economic progress for the United States with unequaled aggregate wealth and prosperity created in that time & by extension taxable pools of resources (much of it from globalization) to now turn around and blame trade, globalization & China in particular for what is fundamentally a failure of statecraft to stop whole communities slipping into poverty & fentanyl laced despair.

-

This is all very interesting and will grab headlines. The real political brick wall for Trump though will be when annualized MoM CPI prints start heading back into first 3% then 4% range.....then eventually 6%....haven't checked the data myself but apparently CPI fixing markets are pricing in that 6% annualized CPI print for the June release. IMO its politically untenable for a politician who was elected to 'fix' inflation, spoke about fixing it ad-nauseam to then turn around and drive inflation up ~3x in his first six months in office.

-

The biggest impediment to Trump's MAGA agenda remains Trump.......when you read the accounts from various folks who've worked for him and with him......everybody from Paul Ryan to Gary Cohn and now even the recent reports re: Scott Bessent.........what emerges is something very much akin to Boris Johnson in the UK.......an unbelievably astute election winning politician completely unable to translate campaign rhetoric into cohesive political execution. By the time Boris Johnson was toast - the majority of his cabinet in texts referred to him with a trolley/cart emoji - because dealing with him was like trying to handle a shopping cart rolling down a hill....it could go in any direction at any time. Sound familiar?

-

Indeed - my litmus test for whether somebody is even worth debating with re:Trump policies is to garner their view on whether the launch and continued 24hr trading of his meme coin with large outstanding reserve tokens to be sold into that 24hr trading market is (a) totally fine with them (b) problematic to outright wrong.....if they answer anything in the zipcode of answer (a) I know they have jumped the shark with Captain Chaos and we can't have a debate because they have TWS (Trump Worship Syndrome)

-

Nope - Captain Chaos is negotiating with the man in the mirror each morning - the one who holds the hairspray and the fake tan. Sometimes Scott Bessent applies the hairspray such that he can get in Trump’s head before Peter Navarro does that day. Scott has been getting up very very early recently. But to be clear Xi never reached out, never called. As I said many pages back - what can’t continue, wont…..and here we are….climb down after climb down re:China since the liberation day debacle. I’m getting to like this Captain Chaos guy….for somebody supposedly unpredictable, he’s kinda very predictable. I admire his ability to do outrageously dumb things and then with a kind of PR flourish & some Truth Social nonsense posts papering over the cracks walk them back and claim a victory.

-

A Democratic congress will be a check on Captain Chaos.......the Republican caucus has failed in its duty as co-equal branch of government to check the Presidents unwarranted expansion of authority.....if your a Republican senator or Congressman you are afraid to speak out against the President (never mind voting against him & with democrats....remember Jan 6th....well every Republican politician remembers what would have happened if some of that mob had got their hands on Mike Pence)....they live in fear of Trump unleashing his flying monkeys, especially the monkey called Elon who will drop unlimited money into your district to destroy your constituency support...so the GOP is not an effective chaos mitigator. Now on to China......China succeeds best in a world of predictability and global growth.....Captain Chaos's adventures have harmed both.....see its involved in capital intensive industries with long capital cycles.......chaos is bad for China's business model.......a hobbled lame duck Donald Trump and politically frozen D.C. is in China's best interest.....the reputational loss of trust as a partner has already occured....that 'win' is in the bag so to speak for China.....best now if predictability and global growth prospects can be returned and that is best served by freezing up D.C. with a divided government.

-

How sensitive do you think "network growth" which I assume is another word for adoption is to the economic cycle? Isn't a new user/wallet purchase of BTC kind of the ultimate in consumer discretionary spending? Which is to say highly economically sensitive?

-

Agree thats kinda my base case - i think you get negotiating theatre coming from the Trump side (already have).....there will be some vague rumors leaked to the press about China conceding on a number of things.......Trump will then say given the amazing deal thats coming together he's going to pause the tariff's.....and boom you've got an off ramp..... Having said all that - Trump has taken some serious pot shots at China......I suspect whats in the best interest of China now is to still leave some pain on the table....perhaps rare earths or something else......its in the best interest of the CCP to see Congress flip Democrat at the mid-terms......I suspect they'll find a way to ensure this tariff chaos doesn't slip the mind of the American electorate when they head for those mid-terms.

-

the inhabitants of Trumpistan swallow whatever narrative he and his proxies ram down their necks…..but I think this particular narrative- that the Fed tanked the economy - will be blown up by the concurrent rise in sticker prices at Walmart / Target etc due to tariffs…when at the same time the economy starts to tank….people will swallow a load of bullshit but not when the truth is right in front of their eyes at the store. IMO I think the get out of jail for Trump remains a China capitulation ….which is the only scenario in which the negative GDP prints later in the year can be blamed on somebody else Powell/Fed etc…put another way Trump desperately needs to avoid sticker price shock flowing through to Walmart / Target in the coming weeks…..with annualized MoM CPI prints in the 6% range coming in perhaps May/June. He’s screwed and China knows he’s screwed….the question is whether China gives him a defensible climb down position.

-

Ah yes the classic Four Seasons press conference how folks let this three ringed circus back into WH is beyond me!...in fact things are much much worse now....MyPillow guy and Laura Loomer only got into the WH at the chaotic last 60 days as the rats abandoned ship.....all while Gary Cohen et al kept the train on the track for most of Trump 1.0.....this time Laura Loomer is in there in the first 100 days getting senior folks sacked...but the old Captain Chaos deja vu must be creeping back in for some folks who'd kinda forgotten all this under a cloud of the "economy was good back then" and before COVID times......need to do the math properly but at a quick passing glance it certainly looks like SPY & QQQ (inflation adjusted) and using today's close has delivered negative to at best flat real returns since their respective intraday highs from 2021....not very exceptional at all.

-

Yep - the frustration I have with Trump is he generally lands in the correct broad zipcode from a policy point of view......but is completely unable to build a coherent strategy to address the correctly identified issue.....and if that weren't enough even the execution of the poorly thought out or non-existent strategy is operationalized in a ramshackle way.....given he's prioritized loyalty over competency in his second term administration I expect to see even more of this ramshackle-ness. In some respects its his achilles heel- its why he's good at winning elections, good on twitter.......and simply terrible at governing......its the populists disease seen everywhere from South America to Africa....simple solutions to complex problems sound attractive.....but when a populist engages with reality and their progress is frustrated by the inherent complexity of the problem relative to their simplified solution....they tend to, as Trump has, to blame the deep state, the Fed and anybody else except the man in the mirrors solution. Trump is in the process of getting his head handed to him by the stock market, bond market and soon if he continues the economy......hopefully he reacts with the mental flexibility he's shown in the past.....but I can't help but feel that voices of reason that surrounded him in the past are in the minority now......its Laura Loomer, Peter Navarro, the my pillow guy and Kid Rock shaping the Presidents impression of reality now.....let's hope the Kid Rock 'put' holds up!

-

The emerging marketization of the United States continues.................

-

Appreciate that - and sorry for your loss - what I said I think is the truth but nobody wants to talk about these complicated underlying issues when there are 'bad guys', perp walks & gangs to go after.

-

100% Fentanyl isn't the problem - the problem is much more complicated & nuanced than that......and its something along lines of what kind of society/ political-economy you have where taking Fentanyl could appeal to such a significant portion of the population......put another way..........the precursor ingredients to Fentanyl are manufactured right here in the USA.....and they are lack of education, untreated mental health issues, lack of opportunity/community, poverty etc etc.....these are the REAL precursor ingredients to Fentanyl.

-

Another example of Trump getting in his own way. What purpose does goading the Fed for interest rate cuts do?.....Zero....they won't listen to you anyway on short rates......and at the margins, your lack of respect for Fed independence, is putting upward pressure on long rates.

-

Terrible to see it - and example of how Trump gets in the way of even his own agenda.....like he genuinely wants to end the war (of that I have no doubt)......but if your Putin listening this.......why the hell would you agree to any genuine ceasefire/peace now.......Trump is happy to let Ukraine bleed out on the battlefield......a better 'deal' for Putin is 12,18,24 months out from here.....more territory will fall, Zelensky may fail poltically and be replaced all while Ukraine will be even more indebted & damaged nation by then which fits in with the aim of making Ukraine a dysfunctional rump state at the end of this. For the folks that think there is 4D chess happening re:tariffs....you should see how Trump the peacemaker can't get out of his way in attempting to a broker a peace in Ukraine/Russia. Its laughable.