changegonnacome

-

Posts

2,694 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by changegonnacome

-

Never heard of Bob........but he might be my brother from another mother

-

Dude - i didnt acuse you of lying....your being hyper-senstive.....I said even if true....exactly cause I couldnt be bothered to check.......because if thats the case in NY or anywhere else.....it isnt changing the productivity/output/wages math in any timeline that matters....maybe over 5-10 year period we get a federal/state fiscal crisis or something thats get you the cathartic cleansing of lay-abouts your dreaming about.....but it aint fixing inflation this side of Christmas! Like think we can agree on that? Anyway did not mean to be offensive to your point it was simply I dont think its gonna help with this inflationary bout we are dealing with, thats all.

-

It isnt the monthly's & it isnt decimal points here as I've said........its nominal aggregate spend increasing substantially in 2022.......while output remained flat = inflation.........yearly 2022 figures are in, it aint MoM noise.........the base level economic characteristics that would suggest 2023 would be different than 2022 in terms of wages, spending & productivity aren't there yet...............so 2023 is shaping up to look alot like 2022.......wages up, nominal spend up & productivity flat = inflation........this is the Fed's problem.....they know the math has to change somewhere........wage increases need to moderate, aggregate spending growth needs to decelerate and/or productivity needs to skyrocket. If things stay like this 2023 will have a CPI figure in the 5's........something has to give.......whatever can give in the variables I've outlined is not good for the market. If you really believe in a productivity miracle for the USA to get us out of this........I'm really sorry......that part is completely deluded.....social security programs are not getting cut........the diversity and inclusion, ESG cult is not going away......and what fat exists in silicon valley......is not all of sudden going to show up in factories in the Rust belt......or chicken processing plants in Idaho. Bear market rallies can be epic.......i agree that everybody needs to stick to their knitting.......very few people in history, like Druckenmiller or Soros, have shown an ability to be able to profitability trade market psychology/gyrations around a base macro thesis. The moves can be too epic that you get shaken out. I remain a slightly less than fully invested bear.....with some macro-esque bear-ish hedges. It made me money, at the margins, in 2022........and I expect them to make me money in 2023......as of today I'm re-opening some shorts on fallen angels, that turned back into angels for a while.......the much higher, for much longer trade is here.

-

What odds would you give that this fact, even if true, is going to change any time soon such that productivity is going to sky rocket? I rest my case. I deal in reality......not fantasy.

-

Fed’s Preferred Inflation Gauge Accelerates, Adding Pressure for More Rate Hike https://www.bloomberg.com/news/articles/2023-02-24/us-pce-inflation-accelerates-adding-pressure-for-more-fed-hikes?srnd=premium&sref=7zqHEcxJ This is what I expected based on BLS wage data from Jan - workers/social security retirees took their newly minted 2023 pay increases..............and unsurprisingly turned pay increases into aggregate nominal spending growth.........the increase in NOMINAL spending of course, and this is the PROBLEM, flowed into a basket of REAL domestic goods and services that had increased not at all over the prior year because..........well everybody with a pulse is already working and in a developed economy like the USA there are no easy productivity enhancing PP&E investments to be made anymore. The USA is not Nicaragua where you automate a production line for the first time & get a productivity/output windfall....all those types of investments were made long ago....and if they werent made long ago.....they were certainly made during ZIRP where the hurdle rate for any PP&E productivity investments was basically 0% so they got green lit. We are hitting, as I've said before, the sticky underbelly of monetary inflation..........the Made in China, Energy, supply chain disinflation was real but it masked a core domestic monetary inflation problem that wont go away.....it was a head fake around a linear fall to 2%........as we've talked about the journey from 5% inflation to 2% is gonna be a bitch. It can only be achieved really, given what I've said about poor prospects for productivity growth, by reducing aggregate nominal spend significantly......reducing credit creation which turns into nominal spend wont do the job on its own..........you've got to get the consumer to moderate spending......unfortunately thats usually achieved by putting a proportion of the population out of work & then those remaining in-work fearful enough that they begin to save more of their income.....reducing overall aggregate spend. Its more commonly referred to as a recession.

-

To be clear I am not saying that! Nationwide BLS wage data from January + 2022 Productivity data speaks to an inflation problem across the nation.......as we've talked about.......in a full output/employment economy with flat productivity......you cannot pass through ~4-5% annualized nominal pay increases, that then translates into nominal spending increasing by a similar amount against effectively a relatively fixed (due to poor productivity) basket of domestic and goods services that even if they are increasing its barely at all..........and then turnaround and expect prices of those goods and services to rise at about 2%......like you cant get simpler than that........based on those figures your looking at a pretty in-grained 5% inflation rate on what the Fed calls core non-housing services.....I refer to the same thing as domestic goods and services. I've said it before to help folks understand it.....but think of nominal wages/spending.....as kind of like shares in a company.......increasing the share count (wages/spending).....does nothing to change the underlying amount of goods/services being produced in the economy........it only serves to change the quoted price of those goods/services.......in the exact same way that issuing new shares in a company simply serves to dilute existing holders of shares........it does nothing to change the underlying economic intrinsic value of the entity in question. The pizza and slices analogy is the most commonly used with stock splits.........and its equally as applicable to the current macro economic situation......the pizza isn't really growing at all (output).........but increases in nominal wages translating into nominal spending growing are in a significant way......and all its really doing is slicing the USA Inc. pizza pie into slimmer and slimmer slices.....manifesting in your dollar bill YoY commanding less and less. Your dollars 'slice' of goods & services is getting smaller.

-

https://www.bloomberg.com/news/articles/2023-02-23/fed-powell-worry-about-south-s-inflation-fueling-job-market?srnd=premium&sref=7zqHEcxJ Single digit margins businesses when they have to pay their workers more pass through 100% of the increased labor costs to the underlying prices of the goods/services they sell.......why wouldn't they........accepting lower margins in this sector of the economy is akin to becoming a not-for-profit charity organization. When you think about where the bottom one third of households by income actually spend the majority of their income....its mainly with businesses that operate in this minuscule margin economy.....and so this bottom one third "feels" and actually experiences inflation to a greater degree both in nominal terms (the prices they see) and in relative terms (the proportion of their income that is exposed to rising prices). People wonder why the consumer sentiment surveys are coming back with such negativity.....but is it any surprise when you overlay the above.

-

Yep hate to do it…..but it’s really the stock market here Im bearish on….why?…….cause there’s not really a scenario I can credibly play out in my mind where SPY doesn’t get run over on the journey to getting back to 2%….. …….if you think about the soft landing scenario in the context of what I’ve said Re: wage growth, nominal spend, output & prices.…..and how you square the circle of bringing inflation back to 2, maintaining unemployment where it is and modest positive growth……..it’s really the corporate sector that has to pay the price via shrinking margins…..done by not pushing price while simultaneously delivering pay increases = earnings getting whacked……..and that’s like the best case scenario for the economy and the soft landing everybody is dreaming off. In my mind soft landing for the economy is actually bad news for SPY……and to a certain extent it’s already happening……it’s corporate America that’s beginning to suffer an earnings recession…..while the consumer…and broad economy still does OK…..the only problem of course is when the corporate sector feels earnings contract it reacts by cutting cost….done by a company in isolation it works beautifully to restore margins/earnings…..done simultaneously and broadly across the economy it doesn’t work at all.

-

I have no interest in the world market..........as I've outlined previously..........what makes the US indexes such a bad bet (or interesting opportunity) right now IMO is a kind of toxic mix of three things not really found in other markets: (1) high absolute multiples being paid relative to high interest rates/risk free rates....and especially relative to my permanently higher inflation/rates thesis which is a conversation for another day (2) Earnings that reached a cyclical perfect BOOM peak in 2021 on the back of unprecedented fiscal stimulus....and are absolutely declining in nominal terms....but actually much larger declines when one inflation adjusts EPS figures.....for example when Home Depot today says SSS are gonna be flat this year....they really mean they will decline in real terms ~5% given the outlook for 2023 inflation....if you arent growing your topline in an inflationary environment....your bottomline is screwed! (3) then finally and most importantly for equity returns......you've got Monetary inflation which has unfortunately IMO embedded in the economy.....as I've repeated.....wages (Jan BLS wage data confirmed my fears), nominal spending increases (Jan retail sales data for example) are ALL happening against the backdrop of full employment/max output economy with terrible productivity growth...........it is ultimately the definition of of inflation......too much money (wage increases/spending increase) chasing a finite fixed level of domestically produced goods and services that just arent growing as quickly as wages/spending are....................such that broad prices HAVE to exceed the inflation target. Putting the monetary authorities in a horrible bind. THIS is the most important thing right now, cut out the noise....the fact stock market multiples remain high here, when the truth is so clear. Is amazing to me. You can absolutely pick your spots in this market.........but the reality is.....the bitches brew I've outlined above does not speak well for the prospective returns of SPY/QQQ for the next couple of years......so your dealing with shitty beta & your dealing with a Fed that needs to engineer a serious deceleration in nominal spending growth & wage growth. The question of the thread is the bottom almost here - which I take to mean was the ~3500 on SPY seen last year the low.......my answer......not a chance.........the low will come, most likely based on past history....only after the Fed has begun to cut rates to try to revive an economy it put on the skids on purpose.......we've got based on the recent data a Fed that I think probably has to get terminal rates up closer to 6% now.....and will hold them there even as unemployment accelerates up to 5+%.....its gonna be very jarring for a market so used to the Fed put. We'll rip through 3500 IMO very easily in that scenario. Let's see.

-

& thats the opportunity......the underlying components of the thesis are playing out.....yet 'the market' has ignored the poor performance of E to date.....by actually paying a higher & higher multiple for those earnings just to standstill in this ~4000 area......so where do we go........ (1) I guess earnings could improve, in the next 12-24 months, such that they grow into the current multiple (very unlikely IMO) (2) I guess the Fed could get back to 0% fed funds as per the pivot/zirp delusion....such that the current multiple is justified relative to FUTURE investment alternatives (unlikely IMO) We are left I think with two reasonable outcomes both with good positioning opportunities if one wants to take them. The two outcomes are (1) SPY declines significantly from here reflecting the new post ZIRP & earnings reality (2) SPY stays flat in nominal terms for many many years to come and what actually occurs is that in the REAL terms SPY's return is abysmal, even negative. 2010's - dont fight Fed.......stocks go up....earnings expand and multiples expand Early 2020's - dont fight the Fed......stocks struggle to go up, they struggle to stay up........earnings are being eroded as consumer weakens, margins get squeezed & multiples have nowhere to expand too, in fact alternative asset classes that aren't equities are competing aggressively for flows (fixed income/checking/savings accounts). Basic trading strategy: In the 2010's you buy OTM calls on SPY/QQQ Today you sell OTM calls on SPY/QQQ

-

What should be taken seriously is falling nominal earnings (worse in real terms).......can we start admitting that E getting whacked thesis is playing out? We are pretty much done now with Q4 earnings....in aggregate they weren't good. https://www.wsj.com/livecoverage/stock-market-news-today-02-17-2023/card/earnings-check-in-q4-reporting-season-nearly-complete-evZim9wC9NMm7CtxSvv8 From above - "Profits are set to decline 4.7% in the fourth quarter from the year prior" As I've mentioned however 4.7% nominal decline is for kindergartners & the deluded......that nominal decline in earnings happened in a 6% inflationary environment......in REAL terms earnings YoY declined 10%.

-

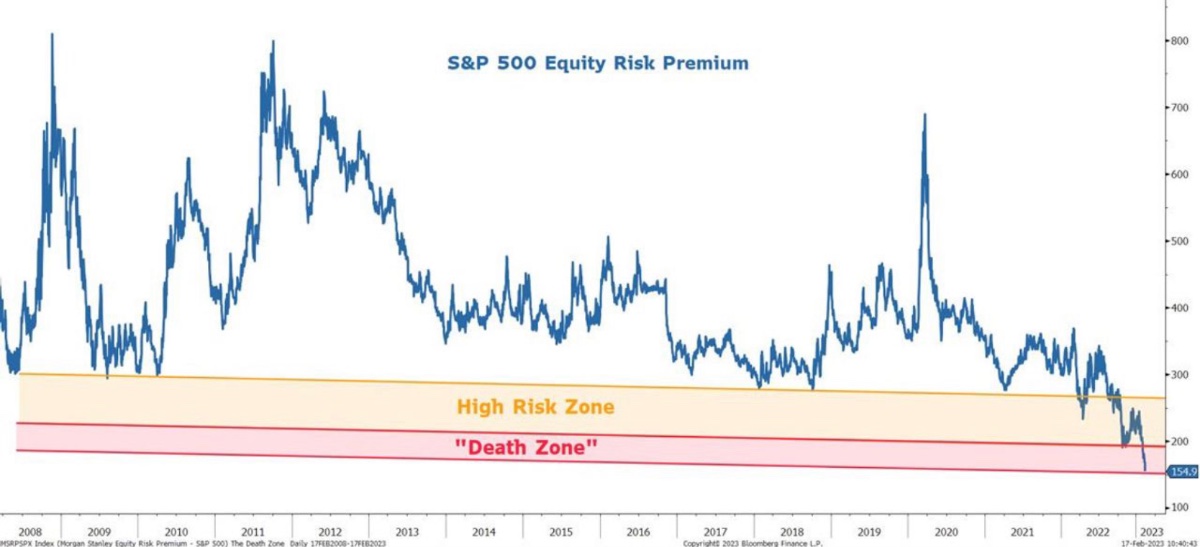

https://www.marketwatch.com/story/investors-have-pushed-stocks-into-the-death-zone-warns-morgan-stanleys-mike-wilson-dcef3c63 Pretty much my thoughts about where we are right now - when the pause/pivot delusion unwinds it’s gonna be interesting to watch.

-

A little bit through this - but good review of where we are.

-

Unbelievable - the EU got lucky for sure with the winter........but I'll give credit where its also due......the EU as a political economy has shown a level of solidarity, unity & coordination on the energy crisis that is impressive.....people have poo poo'd the lack of a Federal Europe......but on this matter, COVID and after much torture the post-GFC period......the EU political institutions have turned out to be way more robust than I would have imagined. Its impressive.

-

Yep Its exactly like I would expect - and we talked about before........middle to high income earners are able to be navigate the cost inflation (1) cause their household budgets have room for a little upward movement in prices (2) the've the ability to negotiate & secure CPI vicinity salary increases. Businesses that provide services (and credit) to more sub-prime/lower income customers are feeling it from what I can see..........MSGE does not sell $40 vodka sodas to these folks!!! Picking your spots right now is 100% the right way to navigate things!

-

Troubling signs emerge as credit card debt hits record high https://finance.yahoo.com/news/troubling-signs-emerge-as-credit-card-debt-hits-record-high-160607906.html I'm sure someone else will post...........on the surface its concerning...........but being internally consistent the nominal level of credit debt reaching a record high is mis-leading.........we've had a couple of years now of inflationary pressure.........knowing this one would expect aggregate nominal credit card debt to be posting records!!!!!!!!............the same way I would expect nominal spending levels to be hitting records too.....the numbers attached to everything have gone up (incl. wages) and so too should numbers like this. Missed payments as % of outstanding payment is a more important metric and this report show they are a little higher than the last two years.......yeah of course they are!.....the last two years were historically unprecedented low in delinquencies cause everybody and their mother were getting cheques every two weeks so they paid their credit cards. I put articles like this firmly in the bear porn that folks talk about......headline scary....underneath the surface its kind of a nothing burger.

-

Me too - hard hard landing that would endanger current banks equity capital such that common shareholders gets diluted ala GFC or whatever is very very very unlikely. The GFC was fundamentally a balance sheet recession.......everybody got levered up and paid dumb prices for stuff......and a tiny move in the value of the underlying destroyed what little equity there was in the banks AND households. This is a scenario where defaults for just about everything (not just housing) go through the roof as people throw in the towel on all debt and declare bankruptcy. What we are likely to experience, in an adverse scenario, is kind a little of what we are seeing already which is a household income statement recession.....wages failing in real terms.....household budgets getting stressed......more folks in trouble at the margins........unsecured sub-prime lenders I would be concerned about here.....but prime secured stuff IMO should be OK.

-

Everybody is also conveniently forgetting to inflation adjust falling nominal earnings........I'm not claiming inflation is 9%.........but it isn't 2% either.......I'd be comfortable saying one should take whatever your nominal fall in earnings is and adding 4-5% on to that to come up with the REAL fall.........or put another way if your equity stub isnt growing earnings ~5% YoY in the current climate it isn't growing its earnings power at all. Simply another reason why one, in a inflationary & higher interest environment, should be seeking companies with higher than normal FCF yields and ideally companies that have positive FCF per share growth YoY in REAL terms. Put another way value beats growth in this environment because its a better vehicle for preserving purchasing power......with less risk of being killed by multiple contraction which haunts many equities I see still. Value provides way less ways to get hurt right now IMO.

-

Lake side lots are what the crypto nuts think bitcoin is - until you can sit on the porch of your bitcoin, have a beer and create life long family memories........I'll take the lake side lots all day long!

-

To go from macro musing to actionable insights $VWO is exactly the type of vehicle I have my eye on if/when the Fed gets the economy roll over........the US gets to fix its inflation first....that is its right as the worlds reserve currency.....via dollar strength etc.......exporting some of its inflation to rest of the world in the process......hurting EM worst........if we are close to 'being done' with inflation and cuts are just around the corner.......VWO will rip with the dual tailwind of currency appreciation against the dollar and underlying company earnings power growth against what likely to be trough earnings..........EM if you can get the timing right (not easy!) is like a coiled spring!

-

Nice - yep looked at HOPE before (you've reminded me to look again, thanks).......those customers pay back their loans more than most!........and all things being equal HOPE participates in the success of that demographic.......and at the risk of sounding anti-Caucasian (which I feel I can be as I am one!)......those Asian folks play hard & work harder......and wherever they plant their flag they do well over time. On the banks - in general.........I'd really like to buy them in size if/when the next recession comes.......everybody will have GFC 2.0 disease......when you and I know these things are now built like the Rock of Gibraltar!!!

-

My man! I nibbled on some Wells....curious what banks are on your radar?

-

100% agree......the most leveraged version of this in a way is European banks....in oligopoly markets. https://www.bloomberg.com/news/articles/2023-02-06/steve-eisman-of-big-short-fame-sees-a-new-paradigm-unfolding-in-markets?sref=7zqHEcxJ Steve Eisman had a good appearance on Odd Lots Podcast last week worth listening too........and he touches on the banking sector post-Dodd Frank and GFC reform........these are institutions stuffed to the gills with regulatory capital with assets categorized by risk weights (RWA's).....forced at the first sign of trouble to forecast and take FULL!! provisioning on expected losses on loan books.........these aint grandmas GFC banks, where the story just keeps getting worse till common shareholders get diluted in an equity raise... ....his take which chimes with mine......is that they are priced as if a modest US recession would send them into negative earnings territory or worse.......in reality I think the banks with large deposit franchies like you say will actually make a profit through the cycle in anything but the worst of the worst economic depressions. What happen to their valuations once that reality gets proved out......that are now kinda of anti-fragile......well they need to trade closer to a market multiple.......and when some are earning 16% RoE and are trading below tangible book thats a long way up to get you that market multiple. Then add in secularly higher rates due everything we've discuced.

-

Anyway getting fixated on report to report is not particularly useful. What it does point towards is the higher for longer thesis - and if you dont think that matters relative to the prospective earnings of many public companies over the short-medium term well, OK. Rates at these elevated levels for a sustained period of time has never not done damage to the US economy. For every month that Fed Funds sits at 5%+ one should think of the cumulative scar tissue building up inside the US economy - projects being paused, financing deals failing leading to defaults, M&A deals not getting done, housing/investment commencements being postponed, consumer purchases being deferred. Not saying sell everything but pick your spots - anti-fragile resilient companies are my key overlay these days.

-

Difference between coming down and it being at target - is I'm afraid night and day. I mean I'm trending upwards towards being a billionaire........but I'm not signing the giving pledge next week......ya know what I mean!