changegonnacome

-

Posts

3,854 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by changegonnacome

-

Well all I'll say @james22 is that 24hrs ago when the Qatar plane grift story was just an ABC report....debunking it seemed important enough to you to warrant going off to X to let us know it was all just fake news. Now when confirmed by the President himself.... its a nothing burger . Not a psychologist but I believe this is called 'cognitive reframing'.......consciously shifting how you interpret or think about a situation to make it more psychologically tolerable. Seems like its worked out for you. Whataboutism. Got it.

-

that part I’m gonna pretend is a brain fart he had….. I don’t doubt ABC/WSJ reporting so this idea was/is being kicked around by him which is bad enough…but if starts coming out with that part and defending it….we are truly not in Kansas anymore. But just the basic concept…taking a plane from Qatar as a gift to the Dept of Defense…speaks to incredibly poor judgement and a complete lack of moral and ethical clarity from the Commander in Chief and the Leader of the Free World….i think even @cubsfan would agree here….America don’t need handouts from any State and certainly not one with as poor a track record as Qatar

-

El Prez himself confirming ABC, WSJ reporting….he’s something else….what a lowlife to get United States & the office of the President involved in a gutter transaction like this with a counterparty like Qatar (of all people, the same money that paid for this plane also paid for Hamas’s tunnels). When somebody TELLS you who they are you should BELIEVE them. Trump via $trumpcoin & now this has laid his cards flat on the table on what Trump 2.0 is about. Two acts in an hundred odd days that are simply indefensible…both centered around the direct enrichment of the President of the United States.

-

Spoke too soon…..WSJ pretty much confirming the outline of ABC reporting - https://www.wsj.com/politics/policy/trump-administration-in-talks-to-accept-new-air-force-one-as-gift-from-qatar-14b29357?st=auU5X6&reflink=article_copyURL_share The fact folks in the Dept of Defense legal department are spending ANY time on this (as confirmed by the Qatari official quoted) is something else. Ive worked for firms and dealt with firms (Fidelity Investments for example) where accepting a gift even a lowly coffee was effectively banned by the company . If anybody has studied even basic psychology they’d understand why….i laughed when I first heard this policy….as the years go by it’s undoubtedly the correct posture for a firm….to say nothing about the right posture should be for a Federal gov employees, let alone the President.

-

I’m not seeing a rebuttal of the ABC reporting…just confirmation a week ago that a Qatari plane is the centre of Trump’s affection right now… Let’s see….glad to see that even Trump supporters feel a need to refute the ABC story online…cause it would be so beyond the pale that it would end up for his personal use at the end of his term under the banner of his Presidential library is beyond beyond.

-

Trump administration poised to accept 'palace in the sky' as a gift for Trump from Qatar: Sources https://abcnews.go.com/amp/Politics/trump-administration-poised-accept-palace-sky-gift-trump/story?id=121680511 Seriously?

-

Yep - you break it, you own it. Success too- I wish him well...hope he pulls off whatever the hell he's trying to do (which I'm still unclear on)..but thus far this is not what success looks like....economy slowing down, hesitancy everywhere you look housing, consumer...dollar weakening....nuking decade long alliances....this is not a good start and the time decay on his political powers is aggressive given he's second term President & advanced age.....folks will start, very soon, looking over his shoulder for JD Vance's nod of approval....its gonna drive him nuts.

-

With the exception of illegal immigration - I'm not seeing Captain Chaos tidy up much..........immigration being the simplest of the so called problems facing the US.....and even there his solution is rooted in unlaterism & executive orders and so by its nature its a temporary fix to a permanent problem....when a woke populist leader of the left comes to power the floodgates will open again. This is why you need Congress and a root and branch reform of how immigration (legal and illegal) is structured. On the most important issue facing this Presidency - getting the fiscal house in order - it appears to me that its more of the same which is to say preach fiscal prudence and spend like a drunken sailor....in this respect Trump is a genius, using Elon Musk as a useful idiot to create alot of noise with DOGE around cutting costs while in reality most of it gets given back in the budget bill soon to be signed in D.C........6%+ fiscal deficit for 2025 is guaranteed now.....same or larger projected for 2026......expect to hear alot about dynamic scoring of the budget once a copy starts circulating. It's the same trick they used for the TCJA which absolutely factually did not end up paying for itself*.....rather it contributed to a growing fiscal deficit......that COVID and then Biden blew out. As I've said cubs - we've got numbers to measure this President his reality distortion field can't hit facts (though it wouldn't surprise me if we started to see an assault on the very statical apparatuses that measure things like inflation/GDP growth it would be kind of predictable banana republic populist behaviour stuff....to call into question the fundamental measures of the economy if they started to move against him blaming a conspiracy of "deep state" statistician "liberal loonies" that do up the GDP figures. Its going to be very interesting to see 2026,2027 across the major measures one can use to measure the health of the economy and the health of the fiscal. *GPT: Did the TCJA pay for itself via dynamic scoring? No. While there was a modest, temporary GDP growth bump in 2018, the tax cuts significantly reduced revenue, and deficits rose sharply even before the pandemic hit. In 2019 growth dropped back to its 2010-2017 average. The promised “self-financing” via enhanced growth never materialized.

-

We get the truth truth..... Have made some nice returns on a basket of stocks that got beat up post-liberation day......PDD and other China-cos.....at the time the market was overly pessimistic what was likely to happen....returns have been spectacular relative to whats actually happened.....what I would say now is the market is too optimistic for a Trump/China pivot...and is underestimating the chance we get a damaging elongated standoff as Xi I think decides to create the right dynamic to open discussions with Captain Chaos....i.e. Xi wants to wait till some real Main St. USA level pain is visited on the US economy before even thinking about engaging in a negotiation.......happy to take some profits now and see what happens.

-

Certainly on the highway to there........hopefully some off ramps before we get to banana town......based on the current momentum feels like a crisis of some sort will be required to snap both parties back to reality cause right now the space cadets have their hands on the steering wheel (on both sides of aisle).

-

Well if its any blessing Captain Chaos sure is helping US politics get to the bottom in an accelerated way.....I'll give him that.

-

I dunno cubs in your world it seems two wrongs can make a right..... - these firms are scummy....sure...so that makes it OK for the President of the United States to shake them down by withholding security clearances and in return he gets to collect millions and millions in free legal services that he secured by using the Presidency itself and parlaying it into a hoard personal flying legal monkeys he can unleash on people. - Biden crime family we're up to tricks before sure....totally scumtastic what Hunter was doing....... so its ok for Eric and Donald to run around the middle east enriching themselves & launching memecoins. This type of thinking is exactly how you end up with banana republics.....

-

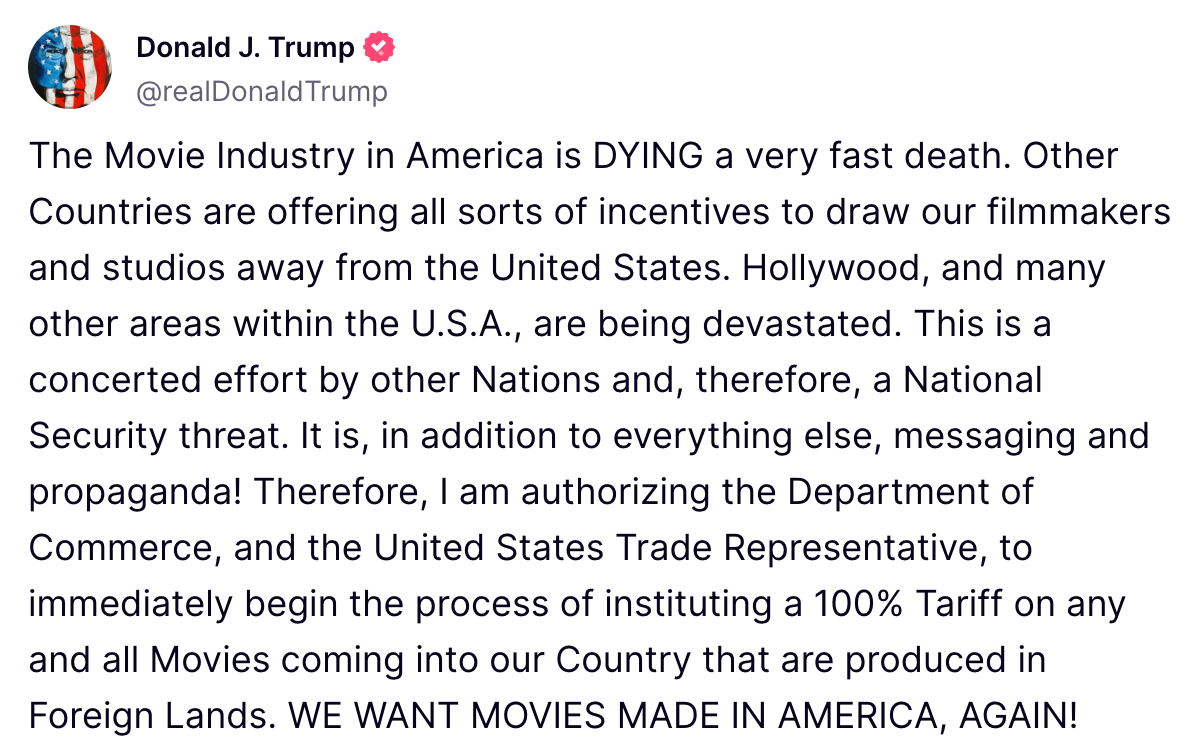

Captain Chaos strikes again National security threat cause sometimes Toronto doubles as Manhattan for movie location shoots Where the hell are the lawsuits putting Captain Chaos back in his box re: invoking national security. I guess this is why he needed to shake down a bunch of DC law firms for millions in legal services......imagine the poor lawyers trying to build a case that movie location shoots outside the US are a threat to the Republic. Tough gig.

-

For sure - no double standards here.....plain wrong what Hunter was at and that Joe didn't stop him or tell Burisma to kick him off the board makes him complicit. But you know what these guys are at now is quite something - - shitcoin launch 48hrs pre-inauguration with millions of tokens in reserve to be sold at anytime to people unknown with no underlying KYC/AML/FARA framework - stablecoin launch - which is the functional equivalent of the First Family of the United States opening a bank AFTER the patriarch is elected - now Eric running around the Middle East doing deals for the family.....with his daddy coming in 14 days after him This stuff is a disgrace. I guess Hunter's only crime was he was thinking too small.....$50k p/m from Burisma is cool, but you know whats cooler a few bn. We've talked about it before @cubsfan but the Trump crime family with this stuff is slowly but surely creating a populist movement of the left.....this stuff is fuel in the fire for that. I try to give Trump his due when I can. But cant help but feel that TDS is a mental crutch that Trump supporters desperately need to overcome the cognitive dissonance that must occur when their idealistic view of the President meets with the reality I laid out above.......easier to dismiss the messenger than deal with the horrible facts that "your' guy isn't an angel that fell from heaven. Quite the opposite.

-

This is simply embarrassing for the country........Hunter was an embarrassment too with his ridiculous board roles make no mistake about my feelings on that.....but at least that was relatively low-key, low dollar amount.........Eric the Prez's son and Steve Witkoff's (Special Envoy to the Middle East) son Zach and World Liberty Financial are running around the globe parading their monetization of the Presidency in full unashamed public view......shit coins, stablecoin vehicles that can accept billions in deposits......all connected to the President and his family........and surprise surprise Trump is headed there in two weeks. I was embarrassed when the details of Hunter came out - Burisma etc.....shameful....$50,000 a month retainers for being the President's son is something else......both these things are grfit.....but the scale of grift around this Presidency from inauguration to today is on another level At a Dubai Conference, Trump’s Conflicts Take Center Stage https://www.nytimes.com/2025/05/01/us/politics/trump-cryptocurrency-usd1-dubai-conference-announcement.html?unlocked_article_code=1.D08.hIXz.D9Bw9Sj9ueUf&smid=nytcore-ios-share&referringSource=articleShare&sgrp=p

-

For sure I'm insulating them - they should be ashamed of themselves.....they went out of control with spending & give-aways listen USA under Trump and Biden was the doing on a relative basis just GREAT....lets just admit......my concern is Trump is taking a good economy and recklessly introducing a set of policy goals that have a high probability of fucking that up.....its a brave or foolish strategy depending on your persuasion.....we'll start getting answers soon and the metrics above are way better than opinions.....stats dont lie.....and the trajecotry the economy was on when he took office was pretty clear 2025 was gonna be another good year for the US.....lets see if it ends up so....but more importantly I'll give the guy a bit more time than call judgment at the EoY....but EoY 2026 we'll start getting a good view on things.

-

As is TWS (trump worship syndrome).....we'll get our answer who's right in four years time.......think we can both agree cubs what a failed Presidency looks like based on numbers- - unemployment up - inflation up - SPY down - growth below trend / recession - annual fiscal deficit maintained at ~6-7% or increasing - Debt to GDP growth continuation with acceleration These things aren't a matter of opinion - 100 days is not a good yardtsick....but I think 6M report cards on the above are fairer....we'll get 8 such report cards on Captain Chaos who I may need to upgrade to Captain Mayhem if the trend in the numbers continue......look forward to his first six month report card sometime in July

-

Right - and I cant remember where I saw it but somebody took the assets Fred Trump left him (something on the order of $1bn in todays money).....and worked out, if he was such a good businessman, how the hell was the guy so relatively poor by the time he got signed up to play a businessman on TV (at the time the "Trump Org" as it was called had smaller headcount than local plumbing company). Trump didn't compound capital through business acumen (his record here is terrible, possibly negative)......he did compound attention into fame to then play a businessman on TV which he then parlayed into the Presidency.....its a remarkable achievement no doubt about it..... but folks are mistaken when they think he's a great businessman......his superpower was spotting the emergence of the attention economy on the New York tabloid scene in the 80's, his great insight/genius is knowing that media needs narratives and characters to fill pages and the truth is malleable...when the twitter/facebook emerged later he was well prepared for the full scale attention economy....for example a good subset of real billionaires don't really want attention, they dont want to be on the Forbes rich list.....Trump told Forbes he was billionaire (when he wasnt) cause he did want attention and they needed someone to profile/interview. Trump 1.0 had real business people around - Gary Cohn, Wilbur Ross, Steve Mnuchin - Trump 'faked it till he made it' all the way to the Presidency. Unchecked now by Congress/GOP don't be surprised when a country run by a fake successful businessman starts to underperform economically.

-

Don't confuse transparency with competency.

-

-

I kind of agree but only because the democrats still have a populated enough centrist element to them - the Republican party has been hollowed out of centrists over the course of the Trumpification of the GOP which is coming up on a decade now........and so Congress provides very little to any checks on the President (as the constituent envisioned)......Kamala might not have been a rocket scientist.....but if she pulled some of the dumb stuff Trump is now the House/Senate Democrats would have literally shut her down in her microseconds.....the compliancy of the House and Senate Republicans is quite scary as Captain Chaos does one dumb thing after another during this trade debacle.

-

Beautiful thing about GDP growth, inflation, fiscal deficit, debt to GDP, unemployment numbers is that they remain factual - I'll judge this President over the medium term.......quarter here, quarter there doesn't matter. The current trajectory seems clear but we wont pre-judge it as I expect a U-turn - - GDP growth is contracting - inflation is going up - while unemployment is most certainly likely to go up - the annual fiscal deficit (as best I can tell) for 2025 and 2026 is going to remain at the same crazy levels Biden got us too - debt to GDP (because of falling GDP growth) is actually going to accelerate now The US economy is on a kind of a knife edge - it doesnt take much economic slippage for the fiscal to start printing 10% deficits here....very normal for the budget deficit to grow 300bps as the automatic stabilisers kick-in and tax revenues contract. My best guess right now (but knowing the old man can change on dime) is that Trump is currently accelerating the country towards a fiscal crisis not away from one.

-

The most important manufacturing the US needs to be doing right now is producing homes - last I checked Temu can't post you 3-bed starter home in the mail. I get the impetus around strategic & dual use industries. Knock yourself out build resilience around vaccines, chips etc. but this wholesale manufacturing dream does not comport with the demographic reality in the US....there isn't enough working age men. And if homes are predominantly produced by working age men aged 18 - 45 (which they are)........I dont want these scarse folks headed into nice air conditioned manufacturing hubs (which the evidence shows they will do all day long versus site work).....you really need them out on building sites building homes.

-

https://www.bloomberg.com/news/articles/2025-04-28/us-shoppers-pay-for-trump-tariffs-on-temu-doubling-some-prices This stuff is the administration's worst nightmare........across ecommerce it seems folks are going to come across alot more discreet tariff surcharges called out front and centre at checkout......it's just terrible politics full stop....but coming off the back of the recent COVID inflation pain which got Trump re-elected its close to insanity......on current trajectory GOP is going to get slaughtered at the midterms......now folks might say but the tax cuts are coming etc etc.....but behavioural economics is clear.....folks feel a loss 2.5x more than they feel a gain......every tariff surcharge a consumer/voter comes across on receipts is going to really really piss them off. @Gregmal mentions why folks feel the need to buy crap on Temu......I could expand it out and ask why American culture is so indexed to the consumption and pursuit of material things.......I'm not sure what the answer is but deferred gratification of goods is not a hallmark of the US consumer the opposite in fact.....so the reality can't be ignored.....consumerism but more precisely over consumption is part of the zeitgeist here more so than anywhere else that I'm aware of.....Captain Chaos is going to find out at the ballot box how deeply cherished folks right to buy cheap crap is......I dont think we get there.....Donald knows the answer already.

-

Yes - and your always less than 24 months away from being meaningfully able to express your frustration at the ballot box. Its both a feature and bug of the US system and one of the big reasons why the deficits & debts are where they are......American politicians and their parties live in a constant state of electioneering.