changegonnacome

-

Posts

3,854 -

Joined

-

Last visited

-

Days Won

7

Content Type

Profiles

Forums

Events

Everything posted by changegonnacome

-

So much grift......its a slippy slope from Nancy Reagan, Barbara Bush to Melania Trump and $Melania coin I guess two things can be true at once......the Trump family are doing amazing things for the United States.....but lets be clear they are also enriching themselves to a level never before seen in history by any First Family.

-

I always like to say some positive things about Captain Chaos when they are so obviously positive. So its quite the achievement IMO to get the European's to up their defense spending to 5% of GDP.....many Presidents have tried and they've all failed at this....Trump got it done.....and all things being equal American military forces can be re-deployed over time from Europe to East Asia which is their highest and best use given the strategic important of containing China. Great job by Trump.

-

Thanks John - Trump supporters have a tolerance for his BS’ing passing it off as some kind of acceptable personality quirk…fine no problem from me…..when it concerns crowds sizes and trivial things. The status of Iran’s nuclear capability post a US military attack is not a trivial matter. If his supporters can’t make that distinction they either have TDS or they are implicitly saying that on matters great or small they have no expectation that Trump the President of the United States is truthfully accurate in what he says. Saturday night confirms my central thesis of the Trump presidency (which has proved to be immensely profitable for me this year) - he remains fundamentally the guy who spent many hours of his formative years more concerned about creating the public impression of being a billionaire versus the hard & difficult work of becoming a billionaire….as this pertains to policy (liberation, Iran on down)….one should assume, always, that Trump is more concerned with giving the impression of changing things versus the hard work of fundamentally changing things. This heuristic works best the more complex the issue at hand (Trade, Gov spending, Deficit, foreign affairs etc). He believes his propaganda skills are limitless (why wouldn’t he they got him to White House!) the reality is his execution skills or one should say his stomach & skill for executing difficult complex tasks is not there. Put more succinctly he’s a President more interested in giving people the IMPRESSION America is being made great again versus doing the hard work of actually MAKING America great again. That is the Achilles heel and crux of this President. Trade accordingly.

-

No — it's a fundamental question of whether Iran does or does not retain any nuclear capability. That’s not a semantic distinction, it’s a categorical one. Hence why the administration/Hegseth continues to tie itself in knots over what Trump said Saturday night and the news cycle around it hasn't stopped. The President spouted complete and utter bullshit to the American people on a deeply deeply consequential question. Like a child that's been caught out in a fib - the President & his team can't quite seem to find a formulation of words or a position that doesn’t expose the utter absurdity of the original claim.

-

Nah just conforming to reality will do me - Trump, ever the fantasist salesman, on Saturday couldn't help selling a bullshit assessment of a mission to the American people on TV when an actual assessment was completely unknowable at the time he decided to make one.......I mean rooms buried deep inside giant mountains are devilishly hard to assess from 7500 miles away or from space...and so the President of the United States and his underlyings have spent the last three days tied up in word salads justifying, to put it kindly, an inaccurate statement he made on a very important matter of national security.....this is not how you run a railroad. I mean all the guy had to say Saturday night was something like this: "Tonight the United States bombed three Iranian nuclear facilities in an effort to make the Middle East and the world a safer place. The mission was completed with great bravery and skill by our US Air Force pilots using the most advanced military hardware in the world that only the United States has. We hit all the targets exactly as planned and we will know in the coming days assess the damage that was done to Iran's nuclear aspirations. I'd like to thank the Air Force and our Defense department tonights mission is a testament to the strength, bravery and skill of our military forces. God bless the United States." It's so unbelievably simple to execute on the above communication for somebody operating in something approximating reality......that Trump couldn't execute on it confirms what we already know......he's a bullshit artist on the little things (crowd size) but a bullshit artist even when it comes to the most important things like national security.

-

Indeed any Iranian public assessment meets the same level of credibility as Donald's assessment a couple of hours after the B-2's dropped the bomb.....which is to say complete and utter bullshit.

-

For sure - I'd put it like this.......its very hard for us to know the current exact status of the Iranian nuclear capability if the Iranian's probably don't even know yet.

-

I guess you could call it a 'adjective disputing'.....but back in the real world its called lying and bullshitting.....if you say you're going to destroy Iran's nuclear enrichment facilities, green light a bombing mission to do so and then address the nation from the White House afterwards and tell them that the "strikes were a spectacular military success. Iran’s key nuclear enrichment facilities have been completely and totally obliterated."......and it turns out they weren't well I dunno I'd say you were bullshitting at best, lying at worst. Donald Trump, White House, Saturday June 21 - https://apnews.com/article/trump-iran-speech-transcript-text-ff4b286992309ec1337e04260247bb1e I mean when he dropped that speech on Saturday it was (a) unknowable at the time what the damage was done & (b) that statement in time has turned to be completely inaccurate assessment of what was achieved..........and somehow its TDS to call the President of the United States out for bullshit? The latitude you give this guy is the true derangement..I support much of his agenda, for all his faults......but if Jorge at Saint Joe stood up at the AGM and said he'd "completely and totally sold 200 acres of woodland for $50m" which later turned out to be complete freewheeling bullshit and a lie.....you'd be the first to slate him and call for his resignation.....Trump does it........and it's folks with TDS disputing adjectives. You know words matter Greg, he's the CEO of United States....and he's addressing the nation after bombing another country....and he's up there BS'ing and now he's got caught out BS'ing and he's now doubling down on the BS via Hegseth and Witcoff mouthpieces.

-

Donald’s ‘obliterated’ damage assessment….is being obliterated…that old NYT’s spreading fake agenda infused news again I guess and the Israeli’s assisting them now with additional reporting being fed to CNN. How crazy is it - that President of the United States so consumed with PR optics that he just had to say “obliterated” in his Saturday night victory lap when it was simply impossible for him or anyone to know the outcome at the point…is now contradicting his own defense intelligence reports and Israeli reports cause he’s basically BS’d the American people on Saturday night.

-

Perhaps - but at their core they are the best we've got in terms of the production of a raw material I'll call "news reporting".....the WP/NYT/WSJ/FT....staffed and resourced as they are have by far away the deepest and widest network of 'little birdies' in D.C and throughout the world and nobody comes close......to say or think there is some superior alternative to an amalgamation & triangulation of this group for news reporting is not a credible argument.....literally the majority of other 'news' outlets re-report news reports from these guys....to say nothing about the alternative media guys who never leave their podcasting studio bunkers and have never talked to a 'source' in their lives. Now if Donald above wants to keep going against the real 'experts' in our own Defense Intelligence Agency's assessment (the ones leaked to NYT's) cause Donald's ego is all wrapped up in a retarded statement he made on Saturday when he wanted to take a live TV victory lap with all his "obliterated" talk.....like let's think this through.....anybody with half a brain would realize of course that it's impossible for anyone to know what was obliterated or not so soon after a remote operation 7,500 miles away done by air power that involved targeting a centrifugal hallway 90 metres down inside a god damn giant mountain You are living in Narnia if you don't realize that Trump was selling bullshit on Saturday night TV with all his obliterated talk and is now doing what he always does.....doubling down on his bullshit in the face of counterfactual news reports. Listen if Trump wants to keep repeating that the centrifuges we're obliterated (like he repeats the 2020 election was stolen) ...that's kinda fine with me....I'm all for this particular BIG LIE.....as it shut down Bibi's pathway to sucking us in further to Iran. Yep I agree Donnie....amazing success....we gave Bibi everything he wanted....the Middle East/iran is his problem now....lets get back to East Asia where American security and global dominance is actually being threatened.

-

You continue to mix up news with opinion….not sure we’re having the same conversation here.

-

Nobody is saying the gold standard - is perfect…not a chance….but it’s like these socialist morons railing against capitalism…yeah sure it’s not perfect…but show me something better morons?!?!?? So I’ll ask you again - what is a better source of raw news (not opinion) than some combination/triangulation of the NYT, WSJ, FT, WP…..there just isn’t a better alternative…so shit on news from those sources if you like but until you can suggest something superior your literally howling at the moon living in an alternative news media world that you believe is better but objectively isn’t.

-

I asked for a better source for raw "news"...not opinions...what you seem to rail against alot is opinons.....the problem with all the alternative media guys....is I'm yet to see how a podcaster with 1.5 employees is an upgrade to the NEWSrooms of the NYT, WSJ, WP, FT..... The New York times article I dropped - is a news report......alternative media has a place where the raw news is interpreted differently and can bust consensus narratives that sit on top of the raw news etc. We'll find out in a few days how accurate the NYT 'news' is.....my guess is pretty damn accurate....cause whether the centruguges floors in Fordo collapsed isnt a matter of opionion its a matter of fact/news.

-

Name me a better source?

-

Your lumping of sources into one generic bucket........is a false equivalency @Gregmal..........there is a substantial difference in both resources, sources and methods and journalistic standards between say the New York times and I dunno some anon account on X or Breibart news......I guess you might call them all "sources" but they really aren't the same thing.....in the same way that a Ferrari and a Toyota corolla aren't really the same thing (but I guess are both cars). You might not like to hear it cause it doesn't fit your narrative but the New York times along with the Washington Post remain the gold standard in journalistic fidelity.......do they get it right all the time - hell no - do they have a bias.....you bet they do ......but in a world where you cant be a full time citizen journalist and so have to rely on the 'news sources' from somewhere.....on balance even with biases and mistakes I'm going to go with the well resourced newsroom where the Editor ensures the information is coming from high level sources in the Government who could actually have knowledge of the matter in question and that the same editor waits to run the story until a second unrelated NYT's source confirms the same thing. But dont take my word for it........what papers moves the market the most?......maybe the ones you dont like or dont agree with their biases......but they move markets versus say the NYPost's relative inabilty to move markets.....because the NYT/WSJ/CNN are whether you like it or not, on average, the most likely to be bringing you a version of reality that comports most closely with reality (imperfect as they are). So on the balance of paobabitlies from various contemporaneous sources on the extent of the damage done by this attack as of today June 24th...........I can assure you (as of today) the New York Times has the highest probability of being proved accurate hence my putting some stock in it.....but again I'd like to see some additional confirmations too which will be incoming soon....not by the President....who is likely to say this is fake.....but by underlyings who will dance around it afraid to piss off Trump....but who by what they dont say....will give an accurate take on the damage....... On a scale of Trump's "obliterated"...........to the New York times.....entrance damaged.....I'm leaning towards the NYT's having a more accurate take on this.

-

Bibi is gonna have a field day with this intelligence report.......its a perfect outcome for his full on regime change aspirations....Trump/US pot committed in principle and action via bombing (that failed to stop the nuclear program) and which will inevitably require further commitments. Trump's error was to explicitly and publicly agree with Bibi stance that Iran was headed for bomb immentitily and something had to be done about it.......Trump miscalculation was that he thought he could be one and done with a few B-2 bombs.....the reality of the situation is much more complex......they have 60% enriched uranium stockpiles.....and they have the knowledge on how to build centrifuges (but based on this report they don't even need that).....regardless they have the centrifuge knowhow....... .....they have the rockets knowhow.......and the last I checked you can't bomb knowhow with B-2 bunker busters. "We were -- knee deep in the Big Muddy, But the big fool said to push on."

-

So predictable......."obliterated" meant the entrances got damaged...... Strike Set Back Iran’s Nuclear Program by Only a Few Months, U.S. Report Says Classified findings indicate that the attack sealed off the entrances to two facilities but did not collapse their underground buildings. https://www.nytimes.com/2025/06/24/us/politics/iran-nuclear-sites.html?smid=nytcore-ios-share&referringSource=articleShare

-

Wild

-

Agree - outstanding result if he can pull it off.

-

Time for some talking I guess......obvious move for US and Iran....Bibi not so much.....hopefully Donald shuts down this conflict and gets a deal in place that puts Bibi and Khamenei in a straightjacket so tight neither can wriggle out of it......the most interesting next move isn't Iran's its Bibi's (for all the reasons I spoke about up thread).

-

The frog gets boiled slowly….the biggest hurdle IMO has already been overcome ….a unilateral United States attack on Iran….the next military commitment, and the one after will cause Trump less anguish & consideration….we have….to put it bluntly entered a new phase in our relationship with Iran….and the story of escalation ladders is just how unpredictable and prone to large jumps in commitment levels they are…to the point where political leaders (even war haters like Trump) very often wonder how the hell they got to the point where they find themselves at.

-

In the story I tell above…a not implausible story…. Do we have time to wait around for what you suggest which could take months, years? In my story Bibi in a few weeks time explains that Mossad has confirmed that Iran managed to move enough enriched uranium off-site, that they still retain enough functioning centrifuges for 90% enrichment and are now hell bent on enrichment & ignition as a means to survive. We’ll, for example, start to hear about suitcase nuclear bombs in the absence of confirmed ICBM capabilities (classic threat inflation). Listen Bibi is one of the finest politicians I’ve seen in my life….you are watching a masterclass in political calculation and state craft….this Iran attack carried out by the USA is really a culmination of his life’s work….he will not rest on his laurels now re: Iran and will continue to skillfully press for ever deeper US commitments to secure regime change…make no mistake about it Bibi will begin to build a case around “finishing the job we started” over the next number of days, weeks, months. I hope the evidence of capability destruction is so immense that Bibi won’t have any credibility when the above threat inflation begins again let’s see.

-

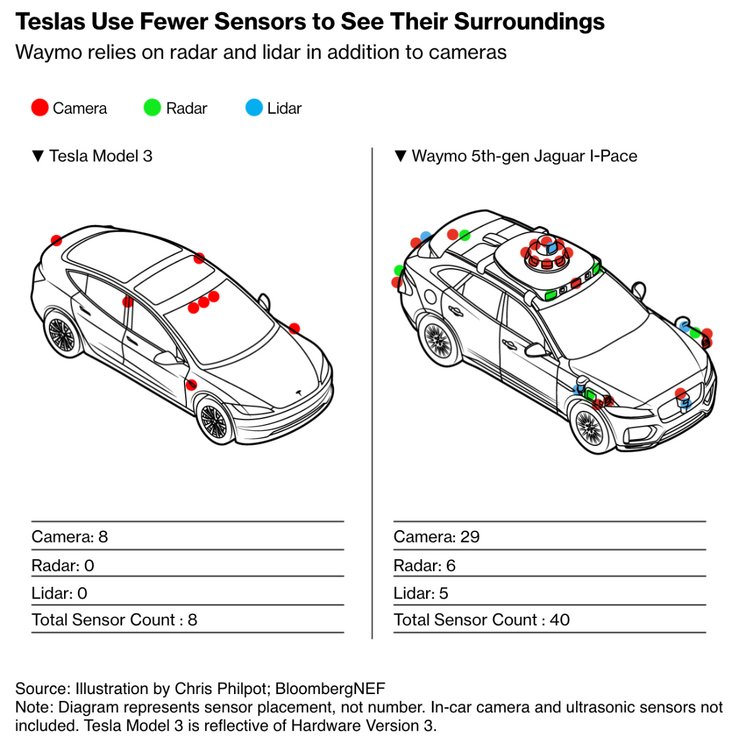

There are two parallel paths to widespread adoption - statistical safety outperformance & political/regulatory acceptance.......the car on the left above may one day get to statistical safety outperformance.....the question is will it outperform the car on the right?.....and therefore what becomes the widespread political and regulatory standard for sanctioned widespread autonomy. Ask yourself.....as a regulator, politician tasked with coming up with the greenlight rules/legal framework when lives and public safety are at stake.....do you sign off on the car on the left or the car on the right as the minimum safety standard.....its an easy choice IMO and an obvious one.

-

How can you be so sure its been "done" because Donald said it was? It's simply unknowable right now and I'll note Pete Hegseth gave a much more measured and cautious assessment of what the bombing achieved this morning at his press conference versus Trumps "obliterated" rhetoric last night. I'll also just remind folks that Iran has 400 kilograms of 60% uranium stockpiled....it was undoubtedly moved to a location away from the nuclear sites....Iran is now a regime in full on existential panic mode...maybe they wave the white flag and seek forgiveness as means to survive but maybe they choose a different more aggressive path - an accelerated no holes barred race towards 90% enrichment & ignition. Even if the US destroyed 95% of Iran's 15,000 centrifuges last night (a hugely successful outcome by any military standard) I can assure you that is not enough centrifugal capacity destruction to stop 60% uranium going to 90% in a sufficient quantities for a bomb in a relatively short period of time. The other piece of 4D chess one should begin to consider now is what is Bibi's next move as the Prime Minister of Israel?....its almost as important as what Ayatollah Khamenei does under the catergory of what the USA's exposure is here now. If I was Bibi, with the bit between my teeth and the United States pot committed in actions and principle to a no nuclear Iran.....I would now use all my perasauve powers & not a little threat inflation to make the following case > - that while the B-2 bombing last night was successful at degrading Iran's nuclear capability that it still remains in place (as per my point above - 60% enriched uranium stockpile plus a few hundred undamaged centrifuges remaining equals a viable nuclear threat) - in fact I would argue, as I just have, that the regime are now more determined than ever to get a bomb and so in fact the nuclear threat instead of being diminished by the B-2 bombings last night has actually, in reality, greatly increased. - with this increased threat I would indicate that the only way to ensure a no nuclear Iran would be regime change and the installing of an Israeli/US backed regime committed to a non-nuclear Iran - I would also point out that the record of regime change being achieved by aerial bombardment alone is effectively zero across recorded history - Bibi having said all of the above, all quite logical....would then say the obvious.....to remove the nuclear threat from Iran forever and for certain......."we Israel, the US & a coalition of the willing, need to commit ground forces to invade Iran and topple the regime".

-

100% and those taking a victory lap today and calling this a great success and obvious move.....are like a chess player declaring 'checkmate' after moving king pawn two squares up in their opening move.....multiple ways things can develop, good, bad and disastrous from here....including lest anyone accuse me of cassandra thinking...is a blue sky outcome of regime collapse in Iran and new golden age in the Middle East.