Xerxes

-

Posts

5,688 -

Joined

-

Last visited

-

Days Won

9

Content Type

Profiles

Forums

Events

Everything posted by Xerxes

-

you are missing Toronto Stock Exchange

-

From Gemini Why Deutsche Börse unique in the pack. While most exchanges facilitate trading, Deutsche Börse (DB1) has built a unique business model that functions more like a global utility and a software house than a traditional stock market. Here is what makes it unique "above and beyond" its peers: 1. The "Vertical Integration" Powerhouse Most exchanges specialize: Nasdaq is great at technology/listings; CME is the king of derivatives. Deutsche Börse is one of the only operators in the world that owns the entire value chain in-house: • Pre-Trading: It owns SimCorp (investment software) and ISS (ESG data), providing the tools fund managers use to decide what to buy. • Trading: It owns Xetra (cash equities) and Eurex (one of the world's largest derivatives exchanges). • Post-Trading: It owns Clearstream, a massive international central securities depository. • Unique Edge: Because they own every step, they capture a fee at every single click of a professional investor's mouse. 2. Clearstream: The "Bank for Banks" This is Deutsche Börse’s "secret weapon" that rivals like Euronext or Nasdaq do not have at this scale. • Asset Custody: Clearstream holds over €18 trillion in assets under custody. • Interest Income: When interest rates are high, Clearstream earns massive "interest income" on the cash balances held by its clients. In 2024–2025, this became a major profit driver that helped Deutsche Börse outperform exchanges that rely solely on trading fees. • The "Plumbing" of Europe: It is essentially the back-end infrastructure for the Eurobond market, making it systemically important to the global financial system. 3. Eurex: The Global Monopoly on Euro-Derivatives If you want to hedge interest rate risk for the Euro or trade futures on the German DAX, you almost must use Eurex. • Regulatory Moat: After Brexit, European regulators pushed for "Euro-clearing" to move from London to the EU. Deutsche Börse was the primary beneficiary of this massive shift, capturing market share that was previously held by the London Stock Exchange Group (LSEG). • High-Margin Collateral: Eurex’s clearing house requires traders to post "margin" (collateral). Managing this collateral is a high-margin, low-risk business that generates steady cash flow. 4. A Pivot to "SaaS" (Software as a Service) While other exchanges are buying data companies, Deutsche Börse is trying to become a software provider. • With the SimCorp acquisition, they now provide the "operating system" used by major pension funds and insurance companies. • This makes their revenue far more predictable. If trading volumes drop, people might stop buying stocks, but they won't stop paying their SimCorp software subscription.

-

Not for me. I have been reading history books long before I got into investing. I would say it is investing that has made reading history books immensely more valuable.

-

I have read them all. The Prize is a phenomenal history books above everything else. I actually didn’t enjoy New Map, and I think I posted my comment in this board. The Quest was good read. In between the two. The other book that you didn’t mention that he wrote is called “The Commanding Heights”. Nothing to do with oil but rather on how either the state or private sector took control of the economy and how that transition happened or didn’t happen. Covers the whole globe.

-

Sad though, 20% of global GDP just before British rule, … just a shadow by the time they ran it to the ground circa 1947

-

he is awesome !!

-

thank you

-

I have not listened to this yet but I believe Ben Watsa is the guest https://podcasts.apple.com/ca/podcast/the-rock-and-turner-investment-podcast/id1772482719?i=1000727211431 I believe there is also a TedTalk with Ben Watsa. But I can’t seem to find it.

-

Next few working days before retirement, Buffett is going to walk the office shake people hands, offer to exchange personal Gmail and ask them to connect to his LinkedIn.

-

I am more than half way through the book. And I really like it. I would highly recommend. Sure a lot of people are familiar with the story. But nothing works like a book that goes back to the 1990s and takes you to the present, and lays the foundation. For those of you seeing perhaps a glass half full, think of it as research, the next book (by whoever) will build on this book and explore other avenues of the story. There is the opportunity for those interested to take the pen. At one point the hypothetical 10th book can even do some Sun Zsu Art of War Kang-Fu stuff.

-

-

-

I think the word “battleship” is really nod to the fact that it will the most powerful surface vessel that is not an aircraft carrier. The pictures shown doesn’t have anything remotely “battleshipy” about it. It is effectively a larger version of what was Kirov-class “battlecruiser” in the dying days of the Soviet Union. Note that there was nothing “battlecruisy” about Kirov-class, either. Battleship and battlecruiser are old concept. With the latter sporting the guns of the former but thin armour of a cruiser. Kirov and Trump class are just weapons platforms that serves to project ego and power, in that order. On the naming convention from wiki: The Trump class name, would challenge the United States ship naming conventions —albeit unevenly applied— of naming aircraft carriers after Presidents and battleships after States. Nearly all of the service's current aircraft carriers are named after former commanders-in-chief, including the USS Gerald R. Ford

-

I listened Trump speech: Trump-class Battleships !?! First two, and then maybe 10 but potentially 25. Reinvigorating the industrial base. Reference to “Victory at Sea” documentary with Spruance and Haley leading battle groups not from aircraft carrier but battleship Golden Fleet,,, ?! and nod to Roosevelt’ Great White Fleet ? But I keep thinking about Austin Powers. Defence contractor coming under pressure to change dividends/buyback capital allocation policy Implicit statements: Monroe 2.0 doctrine in full display with Venezuela and Greenland.

-

Not at all. I would say that GE/Safran unveiled the horse (open-rotor fan) before the horse (airframe), during the early 2020s. Airbus is keen on it. Boeing is way more conservative giving all that is going for it and prefers a traditional engine/nacelle approach. That is the picture today but can definitely change from here. Both airframers may go with the traditional airframe, all depends with risk appetite.

-

Definitely true on TDG. On your comment about GE dominance: A long time ago PW had dominance and was engine supplier on 737 (many don’t know that). It was its dominant position that let is slip, and gave GE/Safran consortium the upper hand, …. And the rest is history. In 2011, Rolls-Royce made a strategic error of exiting the narrow body market. As they sold their equity in IAE JV. That created the duopoly. Two strategic mistakes. The first gave rise to GE/Safran consortium, and the second removed Rolls-Royce. All this to say that while the moats you mention are enormous. Their enormity sometimes is overcome by the incumbent making strategic blunder. (Think Boeing going after Bombardier, which had the effect of making Airbus owner of C-series for very little cost) Today, new narrow body platform are being thought about by Boeing and Airbus. Boeing has no stomach for open-rotor fan design; Airbus is thinking really hard about it. Unlike the previous narrow body era, these cannot have dual engine suppliers (an aircraft designed for open-rotor cannot take traditional engine and vice versa). So it will be winter takes all with exclusivity. GE/Safran consortium are betting on open-rotor; while PW/MTU consortium are less interested in open-rotor. Will PW gain back Boeing on the next platform ? While GE/Safran consortium gets exclusivity with Airbus for open-rotor. The decisions made in the next 5 years or so will write the next chapter for the next 20-30 years, while shifting moats around.

-

yes. Definitely if we are comparing moats between engine-OEM and the likes of Heico and TDG, there is no comparison. Heico and TDG moat are similar in that they operate in the cracks within the OEM & A/M value chain. But also very different in that HEICO leaves money on the table for the other guy (customer) while TDG gobbles up. That said i am not sure I understand your last phrase. Why are you equaling HEICO and RR

-

TDG and its mini-TDG-clones do not compete on their product/services. But they may compete on acquisition target. Even then the M&A targets that TDG is interested, the mini-TDG doesn’t have the financial wherewithal to buy, and the targets that the mini-TDG are interested are just too small for TDG. Both sides of scale presents advantages and disadvantages both to the incumbent and the new kid.

-

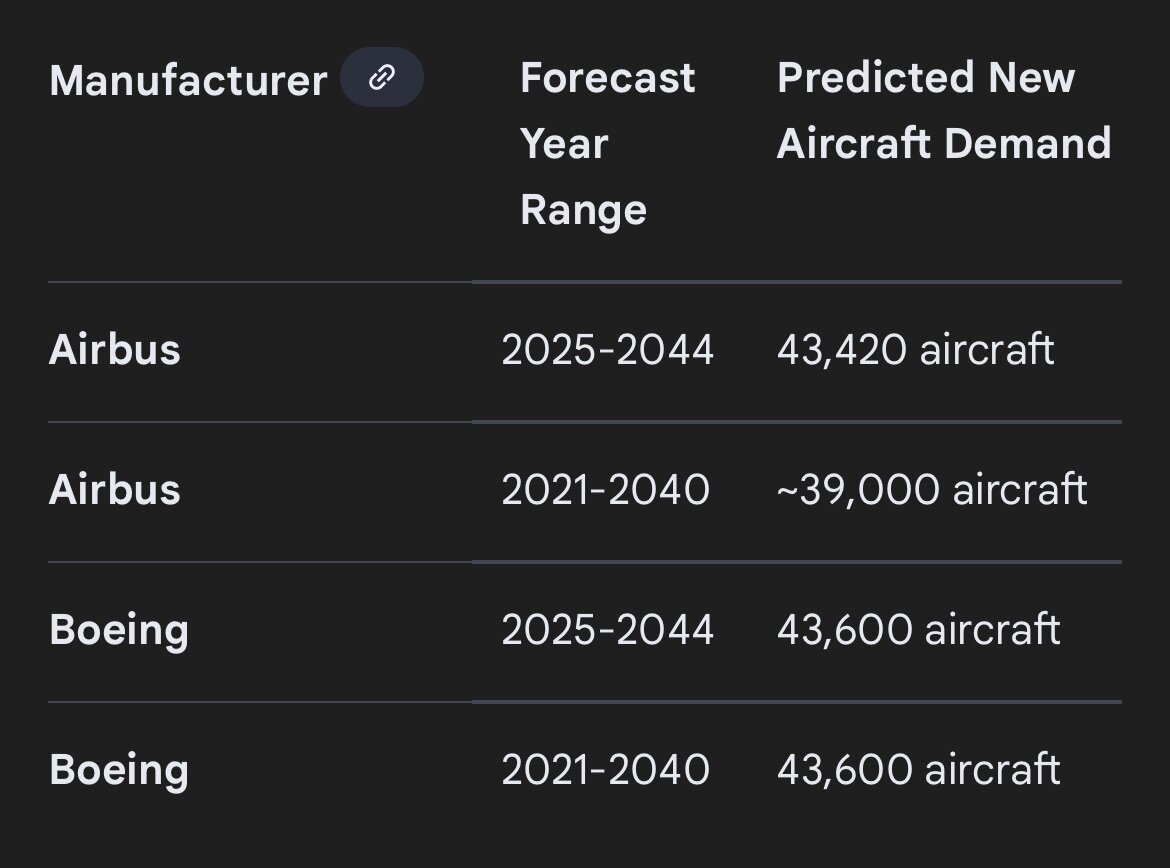

the long term OEM forecast says it all. With half of them just replacing current aging aircraft. So the secular long term trend is there. But these views above were also there in Jan 2020, (a month before Covid lockdowns) meaning that there is always that singular event that may come out of the left field, upsetting what seems today a non brainer. Point being there will always be something coming out of the left field that may present us with an actual opportunity

-

The obliquity of porcelain

-

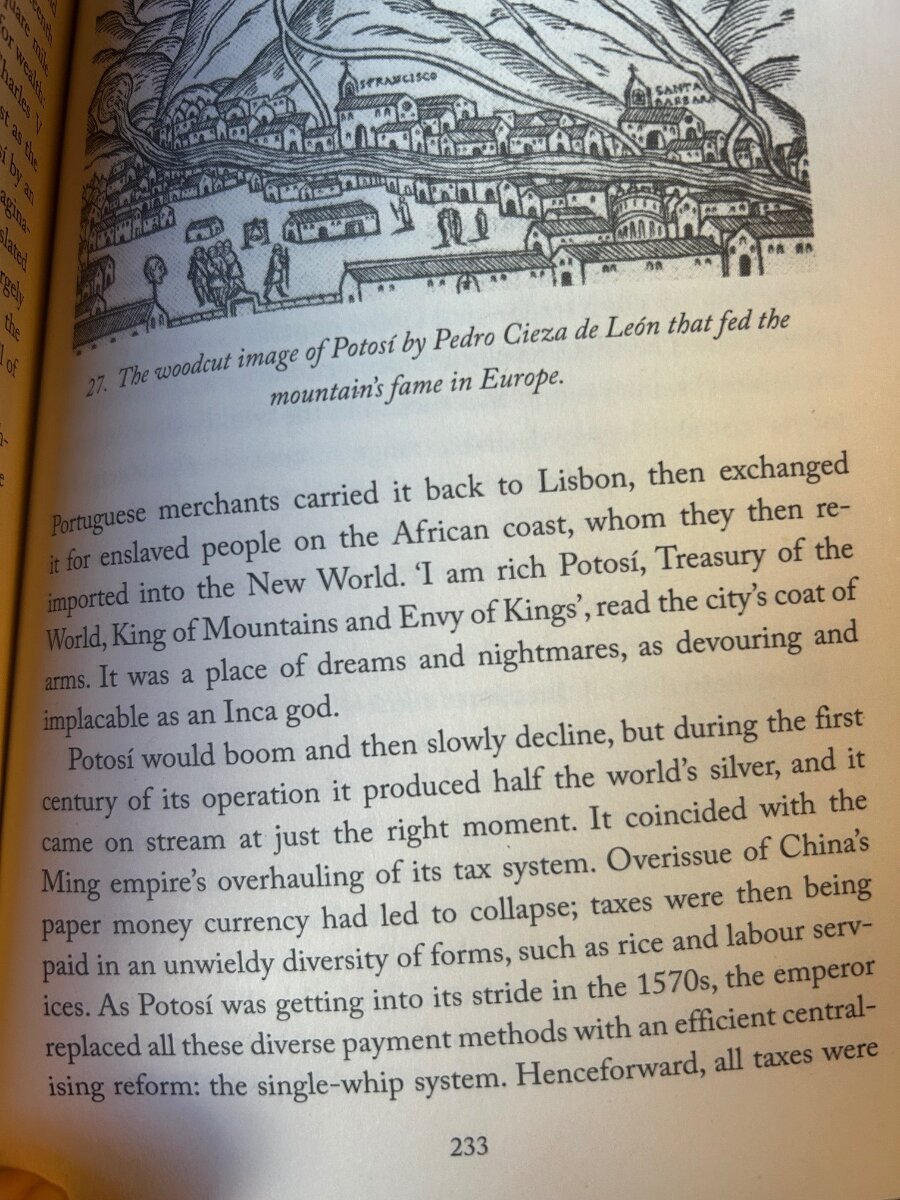

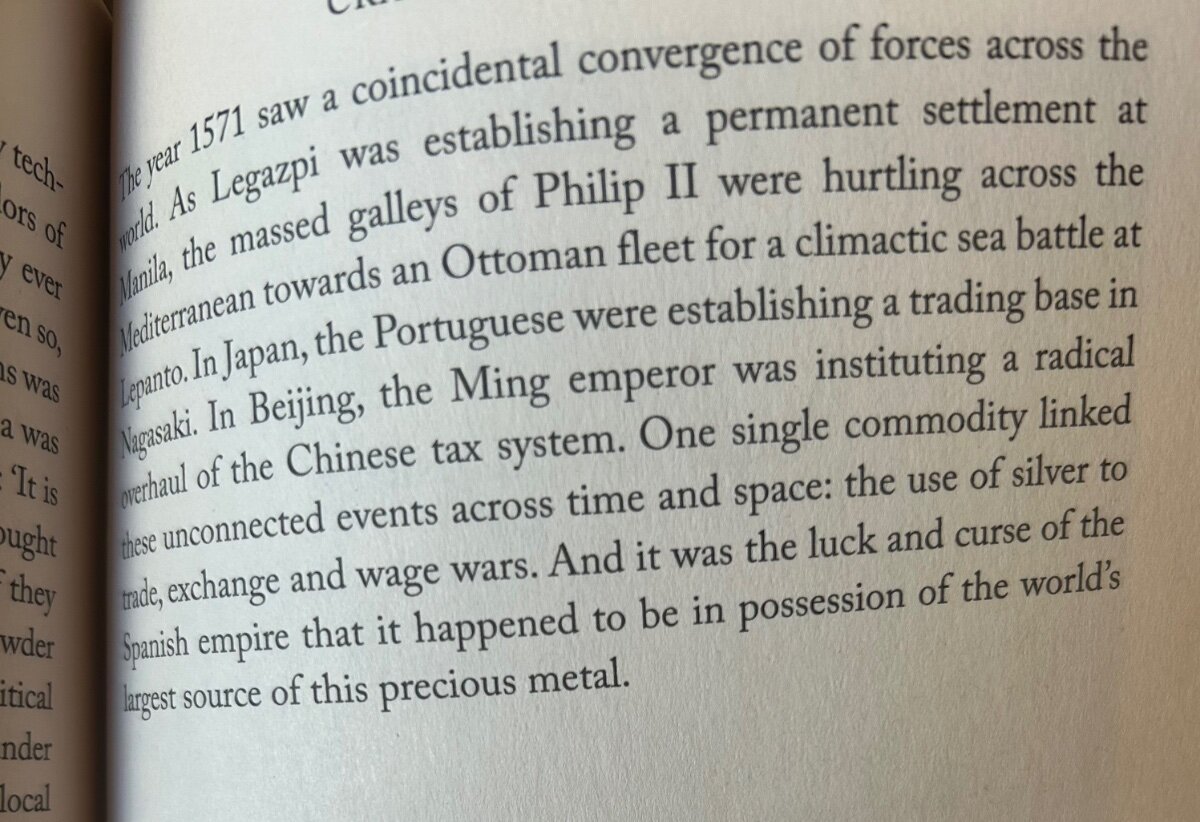

Potosi-China-Silver

-

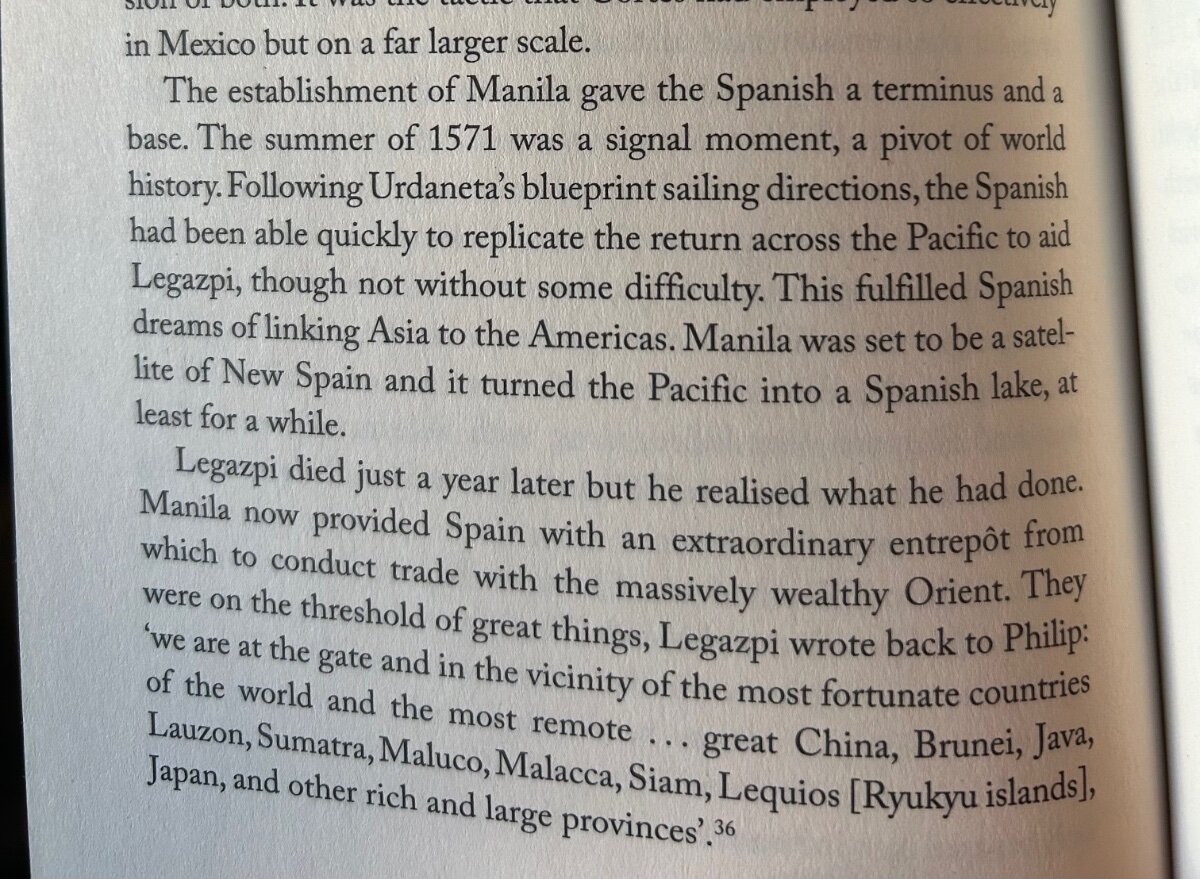

Establishment of Manila :

-

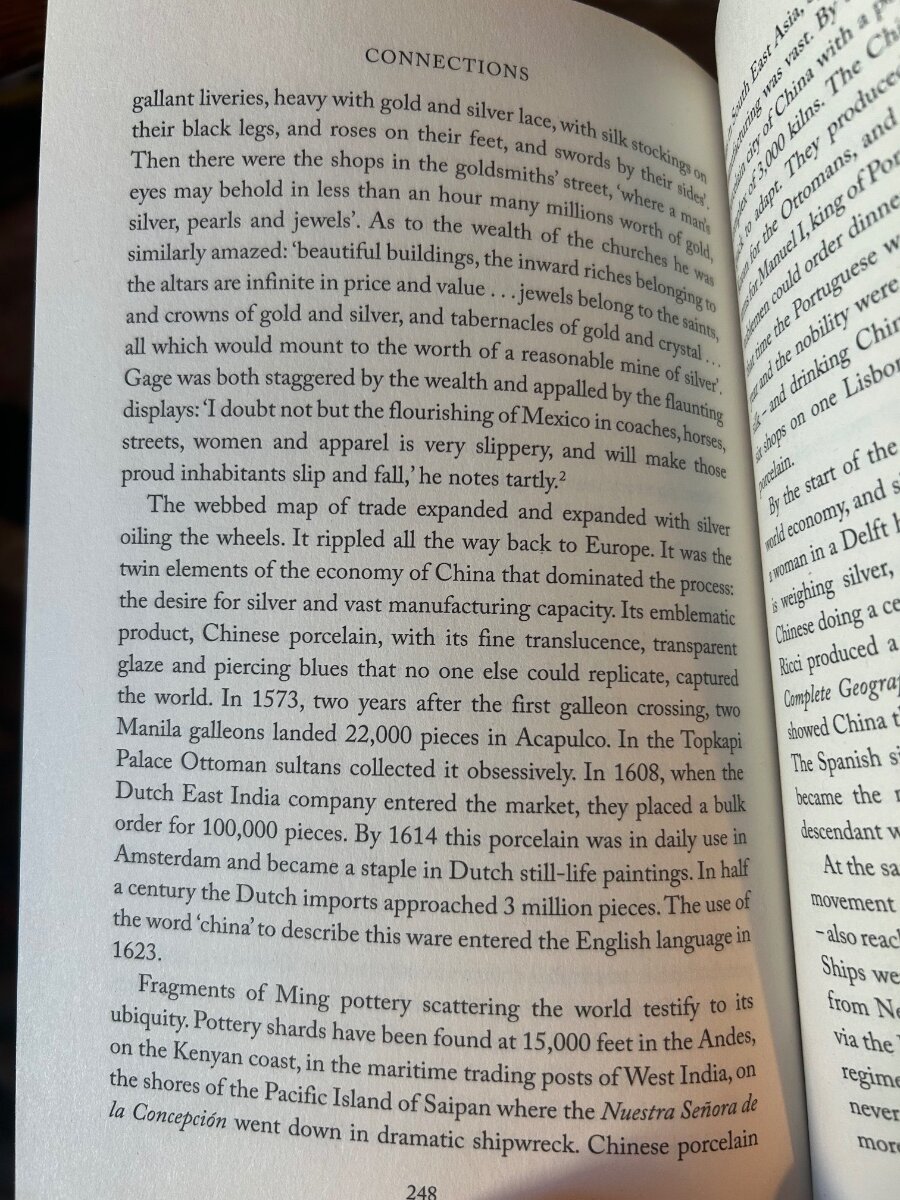

I would recommend this book for its sweeping historical narrative centring around spice trade in Asia. I have read all of Roger Crowley book. His work excels when looking at historical arc, but works less when he focuses on specific topic. For instance his work on siege of Constantinople and his other book on siege of Acre, was a tad boring. In contrast, his work on Venice, and the other book shown above were memorable to me. This specific book is a new one that got published. When you read the second half of the book you realize how important manufacturing capacity of China was to the world in 16th century, before its fall. How silver was important to facilitate that trade. How the giant silver mine (Potosi) found in Americas were important to source the silver, how “traders” and then-nation-sponsored-Glencore of the world were important to lubricant the system. Here are some passages from the book:

-

I love General Electric and SAFRAN, but I think these are more "continue to hold through 2026" if you were wise enough to purchase them in 2022-23 as oppose to 2026 best IRR buy on a clean sheet of paper ?

-

I like Dara as well. I think Josh Brown does the best job articulating his views on Uber.