jfan

-

Posts

861 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by jfan

-

Bought some CSU, LB

-

not sure. I've heard of his name in the past but never really paid attention. I think he focuses on energy and geopolitics. Pretty active on X, and runs a consulting/media business. I thought the debate was actually decent. It was cordial, professional, factual. Not sure if he is a permabear, but it didn't come across so. He did mention he invested in an AI start-up, so maybe not so bearish in our brave new world.

-

@NnnnotSoSmart There was a podcast (Thoughtful Money with Adam Taggart) January 2024 with Doomberg and Gorozen discussing peak cheap oil which was really interesting. Doomberg was arguing cheap oil for longer and G&R was arguing the opposite. The difference really had to do with time horizon. They both think there is plenty of global reserves that can be mobilized relatively easily if the politics get out of the way. After a couple years, looks like Doomberg was more correct but worthwhile reading G&R latest paper, which discuss their modeling errors on the permian wells.

-

On a similar vein, one of the fathers at my kids school quit his job to do stock day trading recently. Might a sign of the times where wages aren't keeping up to the cost of living, people are desperate to escape.

-

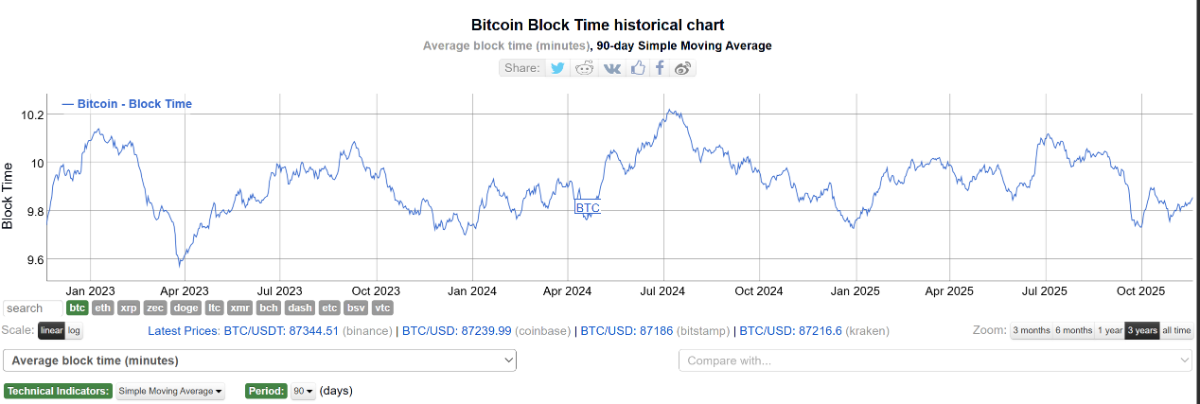

The difficulty adjustment occurs every 2 weeks, so that if the mining rigs are guess the hash to quickly, the network makes its more challenging, and vice versa. The programming has worked remarkably well. Bitcoin Block Time Chart This link has a bunch of charts that you might find useful. @UNF2007

-

Dug in a bit more on this name, and as with most things, there are some favorable and unfavorable features. - ~ 85% of their sales relate to domestic Japanese customers, where @Dalal.Holdings is quite correct in that it will face challenges in population decline (-1% per year), with a projected drop in population from 123 million to 100 million by 2050. The saving grace is that the Confectionery consumption (yen - based) has been pretty steady over the past 10 years. The population forecast is shown below: The per capita purchases ~ 20,500 yen per year per person (~ $160 USD), undoubtedly this will be challenged to grow from a volume standpoint due to a declining population but would be somewhat mitigated by price increases. With Kotobuki, already ~ 2-3% of the market currently, and most other popular brands occupying < 4% of the market each. Kotobuki would need to 1) gain domestic market share and/or 2) improve sales and production efficiency moving forward. Kotobuki operates a holding company with multiple brands, focused on the more premium market, that owns and operates their own manufacturing facilities, but uses a combination of both their directly-owned retail outlets, pop-up stores in department stores, and wholesale channels (grocery stores, airports, ports, and other large transportation hubs). In the past 5 years, they've been about to grow revenues, gross profits, operating profits, and net operating assets by 40%, 60%, 120%, and 12% (ex-all their cash) respectively. Their gross margins of 60%, operating profit margins of 25%. Their ROE (with cash reserves equal to 30% of sales) is 30%+ over the past few years. Amusingly, they disclose their cost of capital as 9.5%. The growth levers that they plan to pull include: 1) increasing production efficiency (moving from 12 - 16 hours worth of shifts ie 1.5 shifts to 2 shifts --> 3 shifts per day per manufacturing plant) 2) increasing sales efficiency (better transport hub sales locations at ie airports, shifting to a large proportion of regular vs temporary employees, better sales on-ramping, mentoring, sharing of best practices). 15% of their sales is at international airports and is tied to the volume of tourists traveling to Japan. Japan's Tourism Agency is aiming to increase the visits from 40 million to 60 million by 2030. With better locations, larger tourist volumes, they hope that these revenues will also increase. 3) increasing the efficiency/speed to introduce new products/eliminate poorly performing products, and increased front-line feedback in product design using their PDSA methodology They have tried to expand overseas, and have encountered slivers of success in Australia, but headwinds in Taiwan, China and Korea. They recognize that their best chances are in their home market, but continue to test and try different things to expand internationally. They have a FY 2030 management plan that will increase their sales by 10% per year, achieve 30% ordinary profit margins with 35 billion yen in ordinary profit. To get there, they will reinvest 30-40% of their operating cash flows, target cash levels at 30% of sales (they will unlikely load any debt to which it is currently de minimus), and return 50 - 60% to shareholders. The founding family owns 30% of the outstanding shares. They started in 1950s, and in 1999, decided to transition from a wholesale and manufacturing model, to their current manufacturing/retail model with progressively steady improvements on ROE from single digit to 30%+ with a pretty linear upward trajectory (except during covid). It doesn't look like a bargain deal right now, more like a fair price for a well-run business with a management that has skin-in-the-game, with demographic headwinds in the long-term. It's business success depends ultimately on the success of consolidating the market under multiple brands to achieve increasing economies of scale.

-

Just found the name, haven't done much work on it other than looking at TIKR data and a few investor presentations, will let you know once I read a bit more. That's fair. I'm up here in Canada. Right now its a bit cheaper to look for businesses in Japan than it is in the US, and despite many cheap Canadian resource companies, they are not so much in my wheelhouse. As a broad over-simplification, Japanese balance sheets seem much stronger relative to North American companies, and pre-tax returns on capital of 20 --> 40% that are consistent +/- improving. Keeper's directly owned LABO stores have unit economics of 25% pre-tax returns on operating assets and 20% operating margins. They become profitable after 3 years. Their PROshop partners (25% of all gas service stations in Japan) have pre-tax returns on assets of 70 - 100% with operating margins of 25%. However, there is little growth here due to a decline in service stations, hence their in-roads with auto OEM dealerships (over weighted average 6% share of new Japanese cars among their partners, with Subaru already up to 25%) to get their products into new cars. With the franchising partnership, they can continue to growth their distribution touchpoints with no capex, which should continue to improve their margins over time. Coupled with a recent sale of stock in a partners business (soft99), they will be quite flush with cash. Management has been opportunistic with their buybacks, with a large deployment in 2021, and most of their excess distributable cash paid out to shareholders as a dividend. With a 16x exit multiple in 5 years, i think it is likely 80-85% of intrinsic value for what appears to me a well-run business with decent ownership skin-in-the-game. Then you get the free option of Singapore, Taiwan, and a move into household cleaning. I think their service has a certain degree of sustainable demand, given the population density, and lack space for people to detail/wash their cars. Thanks for the Elan tip, will explore.

-

I've learned over the years of investing my savings, that I need to try to keep an open mind and not look at the PE multiple as a first pass filter. If it looks like a business I can comprehend, and the economics look reasonable, I dig a bit. TBH, after digging into some of these Japanese companies, I think there are a number of high quality mid-cap businesses that are conservatively run, good historical returns on capital, with what appears at least from my North American armchair, run by managers that understand the value their product and services. Many of these companies have been operating for decades doing the same thing over these years. There seems to be a longevity to them, and they are willing to share excess distributable cash back to shareholders. 21x EPS with excess cash on the balance sheet, 10x sales, expanding both gross and operating margins, with positive cash flows over 10+ years every year, it seems cheap relative to all our magnificent 7, with all their capex spend, and much wider dispersion of future economic outcomes.

-

Thanks for the insights. Here are a couple more, not net nets, but seem to be decent quality boring companies: 1) KeePer Technical Laboratory (6036)- services cars by washing and applying a joint developed resin that repels water and dirt via a distribution channel that comprises of their own stores, independent gas station service shops for after-market applications and recently gaining traction with new Japanese (and Volvo) dealership to apply it on new cars. They are also moving into a franchise partnership with a Japanese integrated oil and gas company (with their own service stations). Little footholds in Taiwan and Singapore, as well as moving into household products. Net cash balance sheet, excess earnings distributed as dividends, no stock buybacks, retained earnings reinvesting in growth, mid 20% post-tax return on capital, 25% owned by founder, and his 2 Co-COOs, operating since 1985, trading at 13-14x next years EPS. 2) Kotobuki Spirits (2222) - Just digging into this one. Makes premium Japanese candy and cakes, sells it via its own storefronts, airports. Founded in 1952. The son of the founder is running the company. Gradual improvement in operating margins and ROE, net cash balance sheet, trading at 21x next year's forecasted EPS.

-

How do people thinking about sizing their Japanese basket? I've been poking around, and there seems to be a number of very good businesses in addition to the statistically cheap stuff here. There is certainly some informational limitations doing research from a North American armchair, and their disclosures are much more sparse in some ways but transparent in other ways. I'm always leery to size positions to 15-20% on a single name given my analytical/behavioral short-comings, but the businesses here seem robust at attractive valuations, with a move to be more shareholder friendly, 10% in a 5 - 7 companies feels about right. @Spekulatius thanks for the tacima idea, looks interesting

-

Came across $4980 - Dexerials doing some TIKR screening I would like it to be a bit cheaper. Missed the Liberation Day pull back and trading a bit higher than I like. It makes electrical conductive films for smartphones, laptops, as well as car touchscreens and cameras. They are rolling out products for optical semiconductors for data centers. Some of their products have 90% market share and have been around since 1977. Point72 showed up on their latest earnings call. Only trades on the Japanese exchange. They were spun out from Sony chemicals in 2015, struggled a bit, but one of their internal hires got promoted and has made a big turnaround since 2018. Rote of 40-60%, roic of 24-27% over the past 4 years. Most of their sales outside of Japan, so there is a currency conversion risk, but the management is addressing this with a partnership with an electronics distributor. They have a conservative 5 year plan, which will double their EPS in the next four years. They've always been conservative forecasters, to the tune of 25%. They've got excess cash on their balance sheet greater than the usual 12% of total assets that most Japanese companies have. At the current price, discounting the dividends that are projected to receive, coupled with no terminal value multiple expansion at year 4, in a more bearish FX scenario, probably a 11% IRR. Management seems shareholder focused with combination of buybacks and dividends, with a flexible re-investment mindset only if the ROC is there.

-

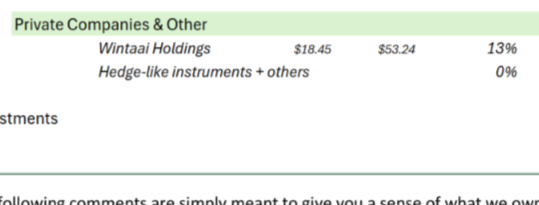

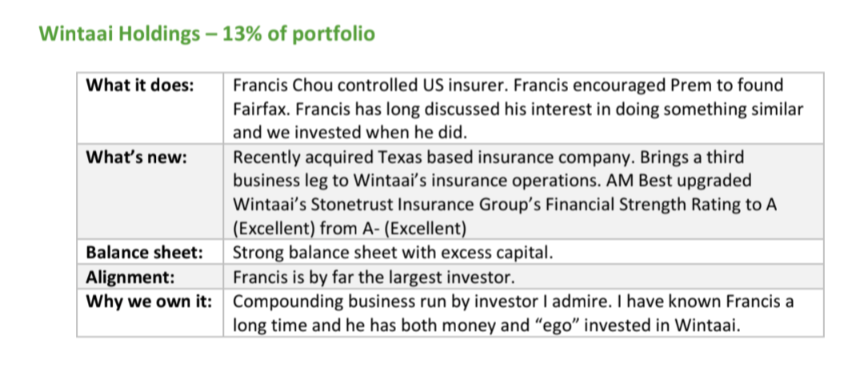

Not that it matters a whole lot, but this was in his semi-annual report. He's never included this statement before, I wonder why all the sudden this disclosure? Totally agree. He and his team are hidden gems.

-

Lol...I've got one the first one posted up in my office. I'm waiting for someone to start selling the bronze bust version of him. The youtube videos of his interviews at ivey business school are quite informative of his thinking process. I lost my spreadsheet on analysing his rolling three year returns for his Chou associates fund but what I recall is that he is that he is a 10-11% investor but with narrow spreads or distribution over time. No large home runs of 50% then drawdowns of 30%, despite running a fairly concentrated portfolio. I think that's hard to do. With his permanent capital vehicle, I think he will do even better over time without temperamental fund investors complaining about shorter term frame outcomes. Interesting he stated in this report that Fairfax was an 18% fund holder since early 2000s.

-

https://a.co/d/fmB3NbT Market masters by Robin Speziale has one of the few rare written interviews of Francis. I think he does discuss his earlier years.

-

That's based on book value. I think this could be easily 2x that number, and that would be still conservative.

-

Courtesy of Tim mcelvaine

-

The other aspect of scale economies shared is that ultimately it is a volume game. It is trying to entice existing customers to not churn away while simultaneously attracting new cost conscious customers. It only works up to the point that there are customers to capture aka reinvestment runway and industry volumes have muted economic cyclicality.

-

This is a new research paper from the Journal of Economic Behavior and Organization on Miner competition and transaction fees. It gives confirming evidence that as block rewards go down, total transaction fees per block move upward by miners including more transactions within blocks as well as more miners coming online. The interesting finding was that incumbent miners deliberately assemble blocks below the block limit to deter new entrants into the mining space by reducing total transaction fees available because there is a cost to enter the mining space. This lowered total fee makes it harder for new entrants to justify their cost to compete, allowing the incumbents to maintain their monopolistic positioning. From this the average fee paid per transaction remains the same, but the incumbents deal with decreasing block rewards, by introducing more transactions into the block. Miner competition and Transaction Fees.pdf

-

Hermes has their earnings call the other day. They grew a bit relative to their competitors but when asked about China, axel said there is no immediate signs of a turnaround. The customer there is still quite cautious.

-

How do you think about position size (for individual stocks)?

jfan replied to Viking's topic in General Discussion

My one other thought is that concentration can give you some very extreme outcomes, positive or negative. The other consideration is that maintaining a slightly above average return for a very long time, will put you into the top 5% at the end. Surviving is more important than winning -

How do you think about position size (for individual stocks)?

jfan replied to Viking's topic in General Discussion

These are some of the considerations I use for position sizing individual stocks 1) how much personal free cash flow do I have coming in now and into future? Which is in part related to the remaining life of my day job (not running other people's money). It makes sense to concentrate early in life where blowing up is a small percentage of one's lifetime of earning. 2) the degree I understand and can predict the evolution of the business's key important unit economic metrics (3,5,10+ years). Ie will the behaviours of participants change? Is the degree of technological change or business model change too rapid? Is competition becoming more or less intense? 3) how much trust do I have in managements capabilities to provide per share value? As well as their idea of what long term means? This obviously is different if you have the ability to influence the economic drivers as a control investor, which I'm not. Based on these, preference to defer taxes, my own ability to change my mind and enter and exit positions, I usually try to find better businesses with better managers to hold for the long term (5-10 years), and cap them off at 5% at cost, allowing them to earn their way into concentration. That said, I do have some crappier businesses that are cheap with some shorter term catalysts as a trade as well as small illiquid micro caps that are cheap that I can hold onto like venture capital positions. That said, my most concentrated position is 40% with a manager that I trust, that started around a 15%-20% cost. But this is an exception vs my norm. -

With the Yen/USD at 145 today, which is the top end of the trading band since the 1990s, and the bottom around 100. Some of these Japanese companies like Nintendo, have a significant amount of sales outside of Japan (earning USD) and costs (denominated in Yen). A reversion back down to 100, would put alot of pressure on margins from reduced revenues when re-patriated back to Japan. With all this talk on de-dollarization vs US exceptionalism (Trump winning), how do people manage their Japanese positions whose business model is dependent on exporting?

-

More LB

-

Landbridge

-

I'm reading Adam Mead's book on Berkshire and the section(s) on See's seem quite relevant. 1) "Fanatic insistence on expensive natural quality control and cheerful retail service" 2) Full control of its candy distribution, owning all its stores and handling distribution to those stores itself 3) Refusing to lower its unit costs if it compromised its quality and fresh ingredients 4) Ability to raise prices despite chocolate consumption per capita going down over time in addition to no ability to expand its geography How does this relate to the luxury industry? - The brands that focus on quality of product and control of the customer experience will do better than mass market/aspirational where unit costs are more important (Hermes, Goyard, ?Patek Phillipe) - LVMH is quite diversified, has a bunch of levers they can pull (grow, shrink brands), cross-sell/advertise, that they will probably do ok in this environment - The mid-market stuff or unfocused aspirational brands are the most vulnerable imo