Viking

-

Posts

6,052 -

Joined

-

Last visited

-

Days Won

78

Content Type

Profiles

Forums

Events

Everything posted by Viking

-

Interesting tug of war going on in oil markets. Fundamentals (supply and demand) vs financial markets (futures activity - net speculative demand is down substantially and short interest is up substantially). The winner? By July/Aug we should know. I am betting the fundamental side wins out… yesterday i was happy to add to SU the last 2 days close to C$40. - “hated bull market” - music to my ears. - Josh thinks we might see an economic slow down in 2H and much higher oil prices.

-

@Luca On the Chubb call yesterday Evan Greenberg sounded pretty confident that 2023 would be another solid year in terms of top line growth (high single digit). This suggests to me that that the hard market is slowing - but we are still in a hard market. What comes next? Looking at history i think it is normal after the hard market to get a couple of sideway years (not hard or soft). And then a soft market. No one really knows… so we take it one quarter at a time.

-

Fairfax has grown their excess and surplus lines insurance in the US by about 80% over the past 2 years. They were the 4th largest player in 2022, up from 7th in 2020. What is excess and surplus lines insurance (E&S)? Progressive explains it well: Excess and surplus lines (E&S) insurance is a market that protects high-risk businesses that standard insurers won’t cover. This market is also known as surplus lines or non-admitted insurance. Companies with unusual or elevated risks often need E&S insurance because the admitted market considers them too risky to cover. These businesses could get a policy through a qualified E&S carrier. https://www.progressivecommercial.com/business-insurance/excess-and-surplus-insurance/ ---------- Excess & Specialty - US Top 25 – 2022 Top US excess and surplus carriers see premiums surge, market share slip in 2022 https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/top-us-excess-and-surplus-carriers-see-premiums-surge-market-share-slip-in-2022-75096783 “Fairfax Financial was the lone company among the top 10 that picked up market share in 2022, rising to 5.0% from 4.8%. The company also experienced a 26.6% surge in premiums.” ----------- Excess & Specialty - US Top 25 – 2021 Most top E&S insurers see market shares decline in 2021; premiums rise YOY https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/most-top-e-s-insurers-see-market-shares-decline-in-2021-premiums-rise-yoy-70287307 “Fairfax Financial Holdings Limited, the fourth-largest insurer in the rankings, was the only company among top 10 players to log a year-over-year increase in market share. The insurer's share of the E&S market rose to 4.77% from 4.50%. Fairfax Financial jumped two spots in the rankings, thanks to a 40% increase in premiums to $3.0 billion from $2.14 billion a year ago.”

-

I re-wrote my conclusion to the article i posted yesterday. This is more on-point. Conclusion: So after all this, what did we learn? The management team at Fairfax has been masterful at taking advantage of the changing environment - both the external (in the insurance market) and internal (at Fairfax). Their planning, creativity and execution over the last 8 years has built Fairfax into a global insurance giant that is exceptionally well positioned in the current environment. What does this mean for investors? Growth investing is identifying and investing in companies with above average growth prospects compared to the industry/peers. Over time higher growth - leads to higher earnings - leads to a higher stock price. For growth investing to work the company needs to be successful; does the growth and higher profitability actually happen? What does this have to do with Fairfax? Well the growth has already happened at Fairfax. And profitability is spiking. And yet little of this is reflected in the stock price - yet. Investors in Fairfax today are getting years of growth that has already happened (top and bottom line) for free. That, of course, sounds preposterous. But it is true. How can that happen? Its not that complicated. The current narrative around the company is completely wrong. Fairfax is a great example of how dumb the ‘smart money’ can be at times.

-

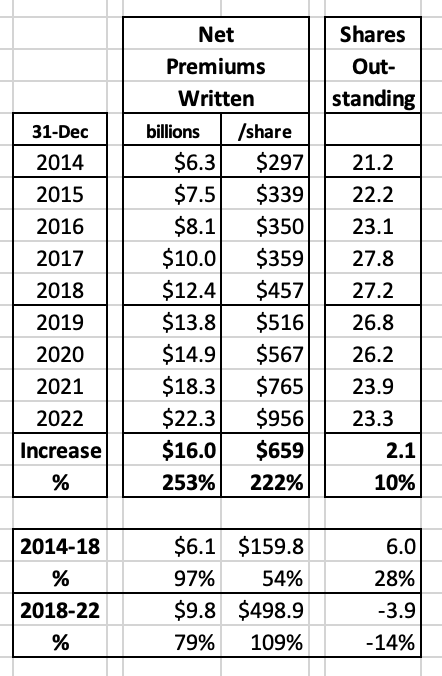

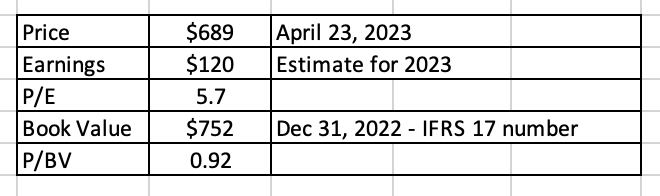

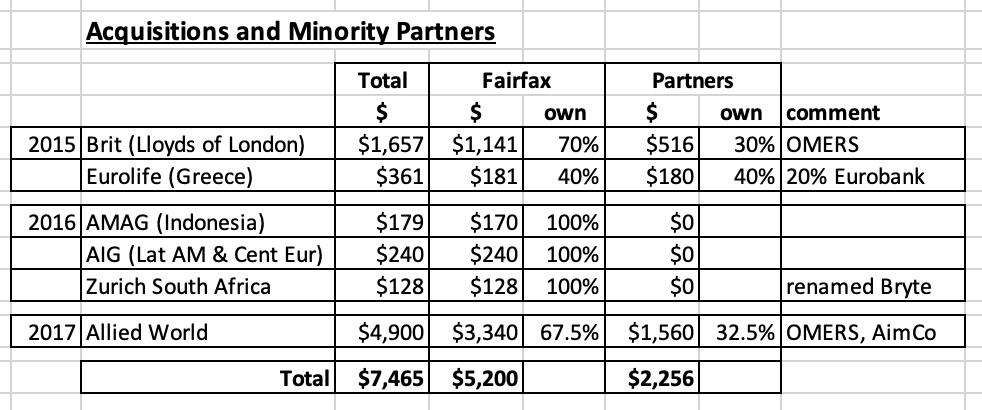

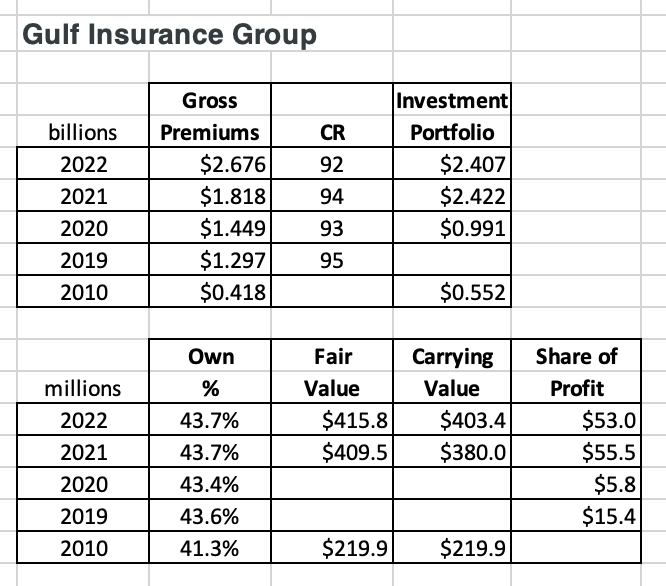

Is Fairfax a growth company? I realize that sounds like a dumb thing to ask. I mean this is Fairfax after all. But hey, just for fun, what do the numbers say? Fairfax has compounded net written premiums from $6.3 billion in 2014 to $22.3 billion in 2022, which is a compound growth rate of 17% each year for the past 8 years. And my guess is we will get around 10% growth for each of the next two years, which would give us compound growth over 10 years of +15%. Really? That performance is pretty impressive. Guess how many large cap Canadian companies have grown their top line by +15% per year for 10 years? Not many. Apparently not many P&C insurance companies either. Like a goat going up a mountain, Fairfax has been nimbly and quickly climbing the rankings of the largest global P&C insurers… last year they were top 25 and this year they quietly moved into the top 20 list. So let’s ask that question again… is Fairfax a growth company? Yup. WOW! A Canadian company that is competing against the best the world has to offer… and not just playing the game (that participation award thing we love here in Canada) but actually winning? That is crazy. Canada must be so proud! Like invite Prem to Ottawa. And hold a parade and celebrate! Except… ummm… no one in Canada seems to know that Fairfax exists let alone that it has been growing like a weed. It looks like most investors are also in the same boat. Because how does Mr. Market reward a fast grower’s stock price? Fairfax’s stock price price is dirt cheap. Makes no sense to me. But, hey, we all know Mr. Market is always right. Right? Except of course… when Mr. Market is completely wrong. (That is called a fat pitch by some country bumpkin who lives in Omaha). But hey, that is a story for another day. Today, let’s dig into what happened at Fairfax over the past 8 years to drive all that top line growth. And why I am optimistic over the near term (even thought the hard market looks like it is slowing). ———— The 17% growth in net written premiums that Fairfax has delivered over the past 8 years has happened in two pretty distinct phases. Then i will take a stab at what might come next: phase 1: Acquisitions (2015-2017) phase 2: Organic - hard market (2019-2023) phase 3: Take-out of minority partners (2022-2025) As one would expect, there is some overlap with these phases. So let’s peel back the onion a little bit and review what happened in each phase. What did Fairfax do? What was the cost? Was it good for shareholders? By digging a little deeper, we can learn more about Fairfax. And better evaluate the performance of the management team. Phase 1: Acquisitions (2015 to 2017) Fairfax has used acquisitions to help fuel its growth through its entire existence. And unlike many P&C insurers, Fairfax has long had an international presence. Over a three year period, from 2015-2017 Fairfax made 6 separate acquisitions that cost a total of $7.5 billion. How did Fairfax pay for the acquisitions? At the time, Fairfax was short on cash as the investment side of the business was underperforming (losses from equity hedges… yes, sorry to keep picking that scab). Fairfax funded the purchases though: stock issuance = $3.34 billion (7.225 million shares at $462/share) minority partners = $2.256 billion (see above) asset monetizations = Bank of Ireland, Ridley, ICICI Lombard, First Capital The deal with the minority partners is interesting: From 2015AR: “In the case of both Brit and Eurolife, we expect to be able to acquire the interests back within the five years after closing, after providing OMERS with an acceptable return. The team at OMERS has been a pleasure to deal with.” Allied World is structured similarly. Finding a temporary partner was a very creative funding solution. I think the partners make an annual rate of return (of around 8% per year?) and Fairfax is able to buy the stakes back when they have the cash and at an acceptable price (negotiated when the deal is struck, I think). Timing? In hindsight, 2015-2017 was a good time to buy insurance companies. Reasonable prices. Right before the start of the hard market. The timing was likely not a fluke. Fairfax was being opportunistic. How much did Fairfax grow? Net premiums written increased from $6.3 billion in 2014 to $12.4 billion in 2018, for total growth of 97% over 4 years (see the table at the bottom of this post). Yes, the share count did increase quite a bit so growth per share was lower at 54% (more on this later). Growth by acquisition can be good but it carries risks. Do you overpay? Are there hidden issues (such as poor reserving)? Are there integration/culture issues? What is the best way for an insurance company to grow? A hard market. And that is what started in the second half of 2019. Phase 2: Organic - hard market (2019-2023) Hard markets for P&C insurers are exceptionally rare. The last one was in 2001-2004. What makes a hard market so good? The opportunity to charge higher premiums. And to apply more stringent underwriting (more favourable terms and conditions). For well run insurers like Fairfax a hard market is like a gift from the insurance gods. Fairfax was positioned perfectly for the hard market that started in 2H 2019. And they have been taking full advantage of it for close to 4 years now. How much did Fairfax grow? Net premiums increased from $12.4 billion in 2018 to $22.3 billion in 2022, for total growth of 79% over 4 years. However, during this period the share count decreased quite a bit so growth per share was higher at 109%. That is rocket ship emoji type organic growth in 4 years time. The hard market is the best way for an insurance company to grow but they do not last forever. And it certainly looks like the current hard market is slowing. My guess is Fairfax will post mid to high single digit growth in net premiums written in 2023. Does that mean the growth story is over? No. Because Fairfax has set the table nicely for what will drive the next big phase of growth for the company: the buying out their minority partners. Phase 3: Take-out of minority partners (2022-2025) Fairfax started executing this strategy over the past couple of years. But it picked up steam in 2022 with the Allied World transaction. 2021 Singapore Re: paid $103 million to increase ownership from 28.1% to 96% (now 100%) 2018 & 2021 Eurolife: increased ownership from 40% to 50% and then to 80%. The last 30% was purchased from OMERS for $143 million. 2022 Allied World: cost $733 million to increase ownership from 70.9% to 82.9% Why is this strategy picking up steam? Fairfax is now generating around $2.5 billion in free cash flow per year. It started in 2022 but was masked in the reported results by the large unrealized losses in the bond portfolio. As we begin 2023, we are going to see reported earnings spike higher. My conservative estimate is Fairfax is going to earn $120/share in 2023 = $2.8 billion. The biggest chunk of this is interest and dividends at $1.5 billion. The next biggest chunk is underwriting profit of $1.1 billion. The quality of the earnings are the best in Fairfax’s history. So what will Fairfax do with this Smaug like mountain of gold that is rolling in every quarter? Let’s quickly review capital allocation: strong financial condition: while debt levels are a little elevated, shareholders equity will be spiking over the next couple of years. So no need to pay down debt. support growth of subsidiaries in hard market? As the hard market slows, this will not be needed. buy out minority partners - bingo, we have a winner share buybacks - well, we actually have two winners And what just got announced? Fairfax is buying out Kipco and increasing its ownership in GIG from 43.7% to 90%. It is interesting how the deal will be financed: $200 million at closing and $165 million each year for the next 4 years. GIG’s earnings will likely come close to covering each of the annual payments due to Kipco. So the total cost of $860 million is being spread over 4 years. Very creative. In GIG’s case, yes i realize Fairfax bought out the majority partner. Same with Singapore Re. Both deals fit the theme perfectly. Moving forward i expect Fairfax to continue buying out their minority partners in the insurance businesses. These transactions are very low risk (Fairfax knows the assets) and they offer a solid rate of return (what ever was being paid to minority partners; likely around 8%?). Taking out the minority partners also simplifies Fairfax’s structure and makes the company easier to understand. Some on this board have stated buying out minority partners is kind of like doing a share buyback. Because shareholders get an even bigger piece of Fairfax’s growing earnings. Share buybacks: With all the free cash flow Fairfax is generating we should also see more significant share buybacks moving forward. If Fairfax repurchases 600,000 shares per year (about $420 million/year at the current price) we could see total shares count drop to 22 million by the end of 2024. This would return the share count to where it was in 2015. In turn, this will boost net written premiums per share. Conclusion: So after all this, what did we learn? The management team at Fairfax has been masterful at taking advantage of the changing environment - both the external (in the insurance market) and internal (at Fairfax). Their planning, creativity and execution over the last 8 years has built Fairfax into a global insurance giant that is exceptionally well positioned in the current environment. What does this mean for investors? Growth investing is identifying and investing in companies with above average growth prospects compared to the industry/peers. Over time higher growth - leads to higher earnings - leads to a higher stock price. For growth investing to work the company needs to be successful; does the growth and higher profitability actually happen? What does this have to do with Fairfax? Well the growth has already happened at Fairfax. And profitability is spiking. And yet little of this is reflected in the stock price - yet. Investors in Fairfax today are getting years of growth that has already happened (top and bottom line) for free. That, of course, sounds preposterous. But it is true. How can that happen? Its not that complicated. The current narrative around the company is completely wrong. Fairfax is a great example of how dumb the ‘smart money’ can be at times. “One more thing”: Fairfax owns a significant amount of Digit Insurance. Who is Digit? Digit is one of the fastest growing general insurance companies in India. We may see an IPO in 2023. But that is a story for another day. ————— Allied World (17.1% = @ $1 billion?): “The company has the option to purchase the remaining interests of the minority shareholders in Allied World at certain dates until September 2024.” Odyssey ($900 million): “The company has the option to purchase the interests of CPPIB and OMERS in Odyssey Group at certain dates commencing in January 2025.” Brit ($375 million): “The company has the option to purchase OMERS’ interest in Brit at certain dates commencing in October 2023.” ————— Let’s quickly review share count. Fairfax issued a total of 7.2 million shares in 2015, 2016 and 2017 to help fund its aggressive international insurance expansion. The new shares were issued at an average price of $462/share. At December 31 2022, the ‘effective shares outstanding’ at Fairfax has fallen to 23.3 million shares. Over the last 5 years (2018-2022), Fairfax has reduced its share count by approximately 4.4 million shares or 15.9%. The average price paid to buy back shares was $464/share. The average price paid for the shares repurchased by Fairfax over the past 5 years is the same price that the shares were issued at from 2015-2017. Fairfax’s book value at Dec 31, 2022 was $658/share (old BV). Bottom line, Fairfax was extremely opportunistic and was able to repurchase a significant quantity of shares at a very low price - and offset most of the dilution that happened from 2015-2017. Of interest, in 2021 Fairfax sold 10% of Odyssey Re for $900 million to help fund a buy back of 2 million shares of Fairfax at $500/share. Fairfax knew their shares were crazy cheap at $500. But they did not have the cash at the time. So they put together another deal with OMERS structured the same as the Brit and Allied deals. Creative. Opportunistic. ————— A Fairfax company did make one large insurance acquisition in 2021. Gulf Insurance Group (GIG) practically stole AXA’s gulf insurance business. AXA was kind of a forced seller and GIG got a great price (who in their right mind would buy an insurance business in the middle of covid… yes, a company affiliated with Fairfax). The acquisition increased GIG’s size by about 80% and gives them considerable scale in MENA - they are now one of the largest P&C insurers in the region. —————

-

@glider3834 It is looking more and more to me like what Fairfax has done with their $38 billion fixed income portfolio over the past 18 months is perhaps going to be recognized, in time, as one of their best tactical moves ever. in Q4 - 2021 going to 1.2 years average duration on Dec 31, 2021 with hedges as interest rates bottom and now pushing average duration over 2years (let’s hope) and removing the hedges as interest rates peak out. They are going to make close to $900 million per year in incremental interest income in the coming years (from what they earned in 2021) from these moves. 2021 = $568 million 2022= $874 Million 2023E = $1.43 billion That is a material improvement in the company’s prospects. This is just another in the long line of examples of what an exceptional team Fairfax has managing their fixed income portfolio. They are wicked smart. ————— We all know book value is everything when it comes to properly valuing P&C insurers… so how did this crazy good move impact book value? The fixed income portfolio had an pre-tax unrealized loss of $1.1 billion in 2022 = $47/share. So if an investor felt Fairfax stock should trade at 1 x BV at Dec 31, 2021 and the same 1 x BV at Dec 31, 2022 (it is the same company after all) then they would correctly assume the stock is now worth $47/share LESS year over year - just looking at the fixed income portfolio. The problem with book value as a metric is it is not forward looking. The fact the $1.1 billion in unrealized losses will largely reverse in the near term is ignored. The fact that future interest income has exploded to more than $1.5 billion in 2023, and is likely to remain at these levels for at least the next 3 years, is ignored. With the move in interest rates in 2022, book value tells you Fairfax is worth less as a company. Of course this is completely wrong. The reversal of the unrealized losses combined with the steady, predictable stream of $1.5 billion in cash from interest income makes Fairfax a much, much more valuable company at the end of 2022 than it was at the end of 2021. Of course, people who closely follow the company know this. But most people don’t follow the company (yet). So they blindly use book value as their primary valuation tool. Which in turn causes them to misunderstand and undervalue the company. ————— From the AGM, it sounds like Fairfax has extended the duration of the bond portfolio in Q1. It also sounds like the run rate for interest and dividends is higher than the $1.5 billion guide they provided when they released Q4 results.

-

Here are some random thoughts from the AGM. First, thanks to all the board members who organized events and were such great hosts to newbie’s like me. I had a great trip and it was due mostly to your efforts. Thanks as well to all the other board members who reached out to say hi. Lots of people are getting an enormous amount of value from ‘Corner of Berkshire and Fairfax’ and we all have Sanjeev to thank for that. I was able to attend this year so some of my comments below are also from some random discussions. “Fairfax has been transformed over the past 5 years.” Top 20 P&C Insurers in the world; Fairfax is actually #12 (only looking at like companies) Significant growth happened in hard market… took share from competitors. Effective cycle management. Prem has put together a very strong senior leadership team - insurance and investments, including external CEO’s (Allied, Eurobank etc). The duration of the bond portfolio was extended in Q1. This is a big deal in that it extends the runway for ‘$1.5 billion in interest and dividend income’ - 2023, 2024 and now 2025. Interest and dividend income in Q1 may come in over $1.5 billion run rate: “actually a little more” Operating income of $100/share for next 3 years Ben Watsa gave an impromptu short speech at one of the small dinners. He talked briefly about the benefit of being a family controlled company. The example: in 2021 ( and the years before) Fairfax went extremely short duration on the fixed income portfolio. Doing so carried a material short term cost. This would have been very difficult to do if they had not been family controlled due to the short term impact on reported results. He seems like a capable, nice kid. The hard market in insurance is likely in the 9th inning; top line growth for 2023 might slip to mid single digit levels (property cat reinsurance higher); we might see peak CR in 2023, slowly rising CR in future years. Odyssey CEO: shifting from a growth story to a margin story. Significant rise in property cat rates. 2024 and beyond will be about protecting margin. Allied World: monster year in 2022: 12% growth; 90.7CR, $338 million in underwriting income. We are at a very predictable place in the cycle (top). Rate continues to exceed cost inflation. Company was dramatically scaled up in size on purpose the last couple of years; as a result, currently has a very low expense ratio. GIG: dividends paid to Fairfax from GIG will largely pay $165 million payments due over each of the next 4 years. Eurobank: guiding to euro 0.22/share earnings in 2023 (euro 0.18/share in 2022) and ROE of 13% in 2023 to 2025. Starting modest share buyback of 1.5% in 2023 and targeting a 25% payout ratio in 2024 (mostly as a cash dividend). Fairfax India: future acquisitions in India will be funded internally or perhaps with an external partner (someone in India or Fairfax, the parent). Fairfax India will not issue shares (and dilute existing shareholders) given extremely low share price. AGT: 60% Fairfax, 12% OMERS, 28% management Bauer: Hockey share about 50/50 with CCM; Lacrosse: small business (less than 10%); leader in NE US

-

@bluedevil extending the average duration of the bond portfolio in Q1 is a big deal. Especially if they were able to push it over 2. I think Fairfax has to keep $9 billion of their $38 billion portfolio largely in cash (very short term). So that only allows them to extend $27 billion. This suggests to me the $27 billion could be over a 3 year average duration. We will learn much more when Fairfax reports Q1 results in a couple of weeks.

-

Some random thoughts on the GIG purchase: This purchase is a great example of a couple of under-appreciated strengths of Fairfax: 1.) international - this has been a growing part of Fairfax’s insurance business for 20 years. 2.) partner with leading organizations- in this case Kipco. 3.) long term focus - this transaction was incubating for 13 years. Total purchase price: Kipco 46.32% $860 million = $200 million + $165 million x 4 ($660) Price paid to Kipco values all of GIG at $1.856 billion. Takeout of 10% minority ownership: cost = $186 million Is Kipco getting a premium to sell to Fairfax? Yes. This is a quality asset with an impressive track record since inception in 2010. It should sell at a premium. the question now is does Fairfax get the remaining 10%? I would assume yes given the KWD 2.00 price. Potential total cost to Fairfax for 100% of GIG is $386 million upfront plus $660 million (over next 4 years) = $1,046 million. What is present value of payment stream of $165 million per year over next 4 years at 8% discount rate? Less than $660 million. Financials: upon close, bump to book value of: Fairfax owns 43.7% Dec 31, 2022 carrying value $403.4 million Suggest Fairfax current stake is now worth $811 million = gain of $407.6 million = $17.50/share pre-tax Paying for the purchase in instalments over 4 years is a big win. In 4 years time, GIG will be a much larger organization. Fairfax could use earnings from GIG to fund a large part of the future payments. GIG reported earnings of $125 million in 2022 (92CR) investment portfolio is $2.4 billion at Dec 31, 2022 gross premiums were 2.7 billion in 2022 Strategically, this secures Fairfax’s position in MENA. This is a big deal. This could also be viewed as a play on oil/energy. If we are in a decade long secular bull market in energy, Gulf economies are going to be strong growers. A young and growing population is another tailwind. Growing economies should be good for insurance businesses.

-

We can add GIG to this list. I see Fairfax buying another chunk of Allied World this year. They have an enormous amount of cash to invest: - Resolute sale just closed $625 million - Ambridge sale is pending $400 million - interest and dividend income in 2023 = $1.5 billion - underwriting profit = $1.1 billion (95 CR) - earnings from consolidated equity holdings (Recipe etc) = $250 million - additional asset sales / monetizations

-

Here is a little more information on GIG. Fairfax continues to take out partners. This is an asset they understand exceptionally well. I have been wondering what the end game of their investment in GIG was… i was thinking Fairfax might be a seller. Wrong. I like the move. Fairfax has an enormous amount of cash coming in this year and next. I will be very happy if they use the cash on purchases like these (low risk solid return).

-

So what kind of an investor is Fairfax? (For those who have not seen it before, here is another old post.) Bottom line, it looks to me like The team at Fairfax does a little bit of everything. It would be interesting better understand how Hamblin Watsa is run. Especially how it has evolved over the past 5 years. Fairfax’s investment portfolio has doubled in size over the past 10 years to $55 billion - this is a significant amount of money. My goal with the list below is to try and capture the full range / types of investments Fairfax has made over the years. Successfully investing in each bucket requires a very different skill set. Yes, some positions could be included in more than one bucket. ---------- Not included below is the usual buy/sell large cap US/Can stocks (too many buys and sell to try and list everything). With the list below I am trying to highlight what Fairfax is doing in addition to this traditional strategy. ---------- 1.) Fairfax is a venture capital investor: funding given to startups or other young businesses that show potential for long-term growth ICICI Lombard (1994) - sold for @ $1.2 billion 2017/18 Quess - formerly IKYA (2013) - via Thomas Cook - still owns - home run Digit (2016) - IPO likely coming in 2023 Davos Brands, Rouge Media, Blue Ant Media (2016) Farmers Edge (2017) - looks like a big miss Boat Rocker (2018) Ki (2020) 2.) venture debt investor: using warrants as sweetener. pre-2016 i think there were lots of these deals; too many to list. EXCO Resources (I think) APR (2016) Chorus Aviation (2016) Mosaic Capital (2017) Altius minerals (2017) AGT Food and Ingredients (2017) Westaim (2017) Seaspan (2018) - massive $500 million Leon’s (2020) 3.) Incubator/accelerator investor: fostering early-stage companies through the different developmental phases (including funding to accelerate growth) until the companies have sufficient financial, human, and physical resources to function on their own. First Capital - Singapore (2002) - sold for $1.7 billion 2016 Riverstone UK - run-off (GFIC 2010) - sold for @ $1.5 billion 2020/21 Group (2013) & Pet Health (2014) - sold for $1.4 billion 2022 Others? 4.) distressed/bankruptcy investor: don't have the cash flow to service their debts and are fighting the clock Bank of Ireland (2011) - sold for +$1.4 billion 2014-17 Eurobank (2014) Golf Town (2016) - merged with Sporting Life Performance Sports (2017) - Bauer/Easton/Cascade Carillion Canada/Dexterra (2018) - merged with Horizon North 2020 Toys “R” Us (2018) - sold retail operations 2021 - now a real estate play 5.) Real estate investor Kennedy Wilson (2010) - ongoing, growing and very successful partnership Grivalia - Greece (2011) - very successful; merged with Eurobank in 2019 Grivalia Hospitality (2022) 6.) asset manager Fairfax India (2015) - ownership has increase from 28% to 42% Fairfax Africa (2017) - merged with Helios 2020 - spectacular failure 7.) private equity investor (via external fund managers) - funds allocated here continue to meaningfully grow BDT Capital (2009) ShawKwei JAB JCP V investment fund (2022) Lots more 8.) turnaround investor: not fighting the clock. Many of Fairfax’s investments became ‘turnaround’ situations after Fairfax made their initial investment especially 2015-2017 vintage. Sandridge Energy (2008/09) - bankrupt 2016? Abitibi/Resolute (2008) - sale closed 2023 The Brick - merged with Leon’s 2012 - sold Leon’s 2021 Blackberry (2011) - still owns full position Torstar - sold 2020 Reitmans (2013) - sold 2019 EXCO Resources - bankruptcy - take private 2019 (Fairfax owns 44%) Fairfax Africa (2015) - merged with Helios 2020 APR (2016) - sold to Seaspan/Atlas 2019 AGT Food Ingredients (2017) - take private 2019 Mosaic Capital (2017) - take private 2021 (not managed by Fairfax) 9.) Resource investor International Coal Group (2006-09) - coal play - sold for big gains Sandridge Energy (2008/09) - bankrupt 2016? Abitibi/SFK Pulp/Resolute (2006-09) - paper, pulp & later lumber - sold 2022 Tembec (2015) - lumber - sold 2017 EXCO Resources - natural gas - bankruptcy/take private 2019 Altius Resources (2017) - resource royalty play Ensign Energy Services (2018) - oil and gas services Stelco (2018) - steel play Foran Mining (2021) - copper play 10.) international investor (2014 was a big year) Bank of Ireland (2011) Grivalia (2011) Mytileneos (2013) Eurobank (2014) Thomas Cook (2014) CIB Bank (2014) IIFL John Keells 11.) Cannibal investor: opportunistically increasing ownership in businesses it already owns. Low risk / high return. 1.95 million shares in Fairfax (TRS) @ $373/share 2 million shares in Fairfax (stock buyback) @ $500/share Increased ownership in Allied World from 70.9% to 82.9% for $733 million Increase stake in Recipe to 84% for $346 million ($100 from Recipe) Increase stake in Grivalia Hosiptality from 33.5% to 78.4% for $195 million Kennedy Wilson preferred equity = $300 million Increase stake in Eurolife from 50% to 80% for $143 million Increase stake in Singapore Re from 28.1% to 100% for $103 million Ownership in Atlas was also increased over this timeframe Fairfax spent another $300 million increased their ownership in the following companies: Fairfax India, John Keels, Mytilineos, Foran Mining, Altius, Ensign

-

Guys, great discussion on IFRS 17 as i was having a hard time understanding its impact on different pieces of Fairfax. The 4% pop in the stock price is interesting.

-

@Dudley i am warming up to the purchase of Recipe. It WAS a terrible investment for minority shareholders forever. However, what investors in Fairfax care about today is how will the investment perform for Fairfax moving forward? How much free cash flow will Recipe be able to deliver each year moving forward? I think it will be able to get back to historical free cash flow levels of around C$130 million (US$95 million) per year to Fairfax (their 84% share). This earnings stream should also be pretty consistent year in year out, and should grow nicely over time. In the near term i am interested to see what Recipe does with their free cash flow. We now know US$100 million of the US$340 million purchase price was funded by an increase in debt at Recipe. So perhaps free cash flow at Recipe in the near term is used to pay down this additional debt. Longer term it will be interesting to see if Recipe uses free cash flow to expand (likely US) or if they pay it out to Fairfax - who then invests it. I am hoping it goes to Fairfax. Recipe might be a great example of a company that needed to go private to reach its potential. Being a publicly traded company has its weaknesses. Recipe did so many major acquisitions over the past 10 years it likely has some work to do to get systems etc fully integrated and working seamlessly. Fairfax hinted as much as a reason for the take private deal. Recipe also has some hidden assets like real estate. Bottom line, Fairfax was likely very opportunistic with this purchase. The minority shareholders were the ones left holding the bag. As a reminder, Fairfax paid C$20.73 for the shares in Recipe it did not own. Here are the capital raises done by CARA/Recipe over the years: 2015: CARA IPO C$230 million raised at C$23/share 2015: Phelon family sells $103 million at C$37.75/share 2016: capital raise to fund St Hubert: C$230 million at C$29.25 2018: capital raise to fund Keg: C$95 million at C$24.93 For those who want more history on Recipe, below is a post from last year. =========== Sept 5, 2022 (from the Recipe thread) What follows is a very long post… everything you wanted to know about Recipe and Fairfax. On Sept 1, 2022 Recipe agreed to be taken private by Fairfax. Shareholder approval should come in Q4. The cost to Fairfax? C$465 million = US$354 million. Fairfax will own 84% and Cara Holdings (founding Phelan family) will own 16%. Ownership after take private: Cara Holdings (Phelan) = 9.4 million Fairfax currently = 27.0 million Fairfax to buy = 22.4 million @ C$20.73 = C$465 million Total shares outstanding = 58.8 million @ C$20.73 = C$1.22 billion market cap Total net debt = C$340 million; Enterprise value = C$1.56billion ————— Why is Fairfax doing this? Fairfax sees Recipe shares as being significantly undervalued at C$20.73. Is Fairfax right? The problem is covid has wreaked havoc on results of restaurant operators in Canada since Q1, 2020, especially full service dine in restaurants (the largest portion of Recipe’s restaurant count). Repeatedly locking down an economy is not good for business, especially for restaurants. So looking at Recipe’s financial results the past 10 quarters is not very helpful. What about going back 2017 to 2019? Free cash flow (before growth capex, dividends, and NCIB) at Recipe was: 2017 = C$144 million 2018 = C$164 million 2019 = C$156 million Clearly, Fairfax expects Recipe in the coming year or two to get back to a run rate of around C$150 million in free cash flow. If this happens then this will become a very good purchase for Fairfax shareholders. The earnings from Recipe, while cyclical, should also be relatively consistent year to year providing some stability and important diversification from Fairfax’s other large portfolio holdings. ————— What is Fairfax’s total lifetime cost for 84% of Recipe? My guess is US$354 + $348 = $702 million (my guess) I base my above estimate on two data points: 1.) cost to Fairfax to take out minority shareholders of US$354 = 22.4 million @ C$20.73 = C$465 million 2.) total $ amount Fairfax invested in Prime/Cara/Recipe from 2011 to present to establish their current ownership stake of 46%. At the time of The Keg merger with Cara/Recipe in 2018 Fairfax said they had invested a total of $348 million over the years. My guess is Fairfax did not put any more money into Recipe after 2018. Recipe did pay a quarterly dividend from after the IPO in 2015 until early 2020. It Started at C$0.0917/quarter and finished at C$0.1177 Because Recipe received wage benefits from the government during the pandemic it is not able to pay a dividend until 2023 (if it did it might have to pay back the benefits received from the government during covid). If not for the government restriction i think it is likely Recipe would have reinstated the dividend when Q2 results were released. Instead Recipe has been using free cash flow to pay down its long term debt. At Dec 31, 2019 net debt was C$440 million. Q2-2022 net debt was down to C$340 million. I wonder if Fairfax will have Recipe increase long term debt to help fund part of the C$465 million in cash needed in the take private transaction. ————— Fairfax has been investing in Canadian restaurant stocks since 2011. The Prime Restaurants purchase was the start of a massive consolidation by Fairfax of the full service restaurant industry in Canada that would culminate in 2018 with the merger of Cara with the Keg (the last large purchase) and the rebranding of the company from Cara to Recipe. Bill Gregson (formerly the CEO of The Brick, a former Fairfax holding), who had lead the massive roll up of full service restaurant banners, retired in 2018 and was replaced by Frank Hennessey, who remains CEO today. Frank’s job the past 4 years has been one of digesting all of the large acquisitions made the previous years. More recently, we have seen Recipe shedding non-core brands like Milestone’s, shedding underperforming locations/franchisees and paying down long term debt. Today Recipe has more than 1,200 restaurants and is the largest full service restaurant operator in Canada. The bottom line is Fairfax understands Recipe and the restaurant industry in Canada exceptionally well. Clearly, Fairfax sees a significant value opportunity in taking Recipe private at C$20.73/share. ————— Much can be learned about Fairfax by looking at its involvement the past 11 years in Prime/Cara/Recipe. Long term focus (a vision to consolidate the restaurant business in Canada). Build long term relationship with equity partner (the Phelon family since 2013 and continuing post take private). Mis-steps (Cara overpays on acquisitions). Persistence (multiple, large acquisitions over more than a decade). Adversity (covid from 2020 to 2022). Very opportunistic - minority shareholders beware (take private Sept 2022). ————— Fairfax began investing in Canadian restaurant stocks in 2011 with two separate purchases. In Dec 2011 Fairfax invested US$10 million in Imvescor Restaurant Group’s recapitalization. Imvescor banners: Baton Rouge, Pizza Delight, Scores, Toujours Mikes, Ben & Florentine. Fairfax added to their position in Nov 2012 ($1 million) and then sold their entire position to GMP Securities in April 2013 for proceeds of $26 million. The second purchase was the start of an 11 year journey with many twists and turns that is now culminating in Fairfax’s C$1.2 billion take private offer for Recipe. 1.) Initial purchase: In Nov 2011, Fairfax outbid Cara (oh, the irony) and purchased 81.7% of Prime Restaurants (East Side Mario’s, Casey’s, Prime Pubs and Bier Markt) for US$69 million. 2.) Cara merger: Oct 2013 Prime was merged with Cara Operations (Swiss Chalet, Harvey’s, Milestones, Montana’s and Kelsey’s). Bill Gregson named CEO. Fairfax invested a total of US$157 million (including its stake in Prime) and owned 49% of Cara which was privately held at the time (Phelan family owned 51%). “Cara has solidified its position as Canada's largest full service restaurant company with iconic brands that deliver unique dining experiences for Canadians coast to coast. This combined family of restaurants significantly increases Cara's scale, strengthens its market position and provides opportunities for growth and acquisitions.” 3.) Dec 2014: Cara buys majority ownership (55%) in Landing Group, Southern Ontario based, high-volume, upscale casual restaurant concept. Remaining 45% ownership was purchased June 2015. 4.) Cara IPO: April 2015, Cara went public. Post IPO, Fairfax owned 40.7% (53.2% voting control) and Cara was debt free. IPO raised raised C$230.1 million (US$180) = 10 million shares @ C$23/share (including over-allotment). I think this is when Fairfax obtained voting control of Cara from the founding Phelon family. Fairfax would be driving the strategic direction of Cara from this point forward. 5.) Aug 31, 2015: Cara purchases New York Fries. “With 120 locations in Canada and another 36 abroad, New York Fries is one of Canada's most successful QSR concepts.” “Cara is acquiring New York Fries for cash consideration which will be funded through Cara's existing credit facilities. The acquisition is accretive for Cara shareholders. The addition of New York Fries also helps diversify Cara's portfolio of stores into shopping centers where Cara's existing 10 brands currently have limited presence.” 6.) Dec 2, 2015: Phelan family sells 3 million Cara shares @ $34.75/share (in secondary offering) for C$104 million. Fairfax continues to own 40.5% of shares and now has 57% of voting rights. 7.) Quebec expansion: March 31, 2016 Cara purchases St-Hubert for C$537 million (US$406). "The acquisition provides Cara with a restaurant chain that resonates with guests in Québec as well as with a food retail solution for the Cara brands – these are two areas of Cara's existing business where we have tremendous opportunities. It also provides Cara with a head office in Québec, manufacturing facilities, and a skilled management team that will grow and manage the Cara Québec restaurant expansion and national retail food initiative." Includes a valuable real estate portfolio consisting of 28 owned properties including 2 manufacturing plants. St-Hubert generated approximately $620 million in System Sales, including the food operations division, and approximately $44.8 million in Operating EBITDA. 8.) To fund St-Hubert acquisition, Cara raises C$230 million (US$174 million) = C$29.25 x 7.86 million shares. Fairfax purchases 3.487 million shares for C$102 million (44% of newly issued shares). 9.) West expansion: Sept 1, 2016: Cara purchases Original Joe's for C$93 million (US $70) - Original Joe's Restaurant & Bar, State & Main Kitchen Bar and Elephant & Castle Pub and Restaurant. “With its proven restaurant-pub concepts and its understanding of the casual, full-service foodservice space, Original Joe's is a natural fit for Cara. The majority of Original Joe's restaurants are located in Western Canada, an area where Cara is currently under-represented." “Original Joe's 99 restaurants generate approximately $250 million in annual System Sales and approximately $14.7 million in Normalized Operating EBITDA before synergies.” 10.) Last big acquisition: Feb 2018 The Keg merged with Cara. Cara pays C$200 million (US$154) = C$105 million in cash and C$95 million in shares = 3.8 million new shares issued at @ C$24.93. Cara changes name to Recipe - Fairfax 51% interest in Keg sold to Recipe for $7.9 million + 3.4 million Recipe shares (Fairfax ownership of Recipe = 43.2%) - Total Fairfax investment to date in Cara = $348 million 11.) April 30, 2018: Frank Hennessey appointed CEO of Cara. Bill Gregson steps down as CEO to become Executive Chairman of the Board. 12.) Oct 24, 2019: after additional C$4 million purchase, Recipe owns a total of 29.15% of units in Keg Royalties Income Fund (traded on TSX) 13.) Dec 10, 2019: Bill Gregson retires as Executive Chairman of the Board of Recipe Unlimited. Paul Rivett, President of Fairfax Financial Holdings Limited, will assume the role as Chairman of the Board of Recipe Unlimited. Mr. Gregson commented, "Thanks to the hard work of all our amazing teammates and franchisees, we have built a business that today generates $3.5 billion in system sales and over $200 million in EBITDA. Today, the company has a strong balance sheet and a solid business process foundation. Now with the CEO transition to Frank Hennessey complete, the company is planning its next evolution to prosper in an ever changing world. 14.) May 6, 2021: Recipe completed the acquisition of Crave It Restaurant Group's ("Crave It") ownership interest in both The Burger's Priest and the 'Fresh – Crave It – Recipe' joint venture for new market growth of Fresh Plant Powered ("Fresh Restaurants"). “Both The Burgers Priest and Fresh Restaurants are dynamic omni-channel brands that have very loyal customer followings. Recipe is excited about the future potential of these dynamic brands.” ————— About Recipe Founded in 1883, Recipe Unlimited Corporation (formerly Cara Operations) is Canada's oldest and largest full-service restaurant company. The Company franchises and/or operates some of the most recognized brands in the country including Swiss Chalet, Harvey's, St-Hubert, The Keg, Milestones, Montana's, Kelsey's, East Side Mario's, New York Fries, Prime Pubs, Bier Markt, Landing, Original Joe's, State & Main, Elephant & Castle, The Burger's Priest, The Pickle Barrel, Marigolds & Onions, and 1909 Taverne Moderne.

-

This past post from @Dazel remains as relevant as ever. With their fixed income portfolio, Fairfax is a total return investor. Interest income + investment gains. It really is amazing the wealth of information that can be found in the various Fairfax threads. Yes, they are long. But over the past 2 years pretty much every part of Fairfax’s business has been discussed and debated (sometimes vigorously).

-

@Dudley the short answer is Fairfax definitely has their own style when it comes to investing. Some describe it as deep value. Has it changed to “buy wonderful businesses at fair value”? I don’t think so. In recent years, i really don’t know how to describe it. When i look at the investments made the past 30 months i would describe it as cannibal investing. They are eating anything related to Fairfax. Actually they have been gorging themselves. Just look at how much in the list below (well over $4 billion). And across so many companies they are involved with: 1.95 million shares in Fairfax (TRS) @ $373/share 2 million shares in Fairfax (stock buyback) @ $500/share Increased ownership in Allied World from 70.9% to 82.9% for $733 million Increase stake in Recipe to 84% for $346 million ($100 from Recipe) Increase stake in Grivalia Hosiptality from 33.5% to 78.4% for $195 million Kennedy Wilson preferred equity = $300 million Increase stake in Eurolife from 50% to 80% for $143 million Increase stake in Singapore Re from 28.1% to 100% for $103 million Ownership in Atlas was also increased over this timeframe Fairfax spent another $300 million increased their ownership in the following companies: Fairfax India, John Keels, Mytilineos, Foran Mining, Altius, Ensign Deep value? Sure. In their circle of competence? Definitely. Are they being opportunistic? Definitely. And i love it. Bottom line, they have done an excellent job deploying capital in recent years. The list above is just one of many examples.

-

@SafetyinNumbers great point. My deep dive into the equity portfolio excluded (on purpose) the insurance holdings. The equity portfolio at Fairfax gets most of the attention. The real jewel at Fairfax is the insurance business. It has grown in size by 420% since the end of 2009 (organically and acquisitions). Net premiums written increased from $4.3 billion in 2009 to $22.3 billion in 2022. Fairfax has demonstrated they are excellent at seeding new insurance companies/management teams and then getting out of the way. They are also good at integrating acquisitions. Andy Barnard was put into his role in 2010 - managing the insurance side of Fairfax. He manages the business through 200 profit centres… which indicates just how decentralized the insurance operations are… separate insurance businesses all over the world that are quietly growing year after year - some for decades. Lots of the value that has been building in this group for decades is NOT captured in book value - for people who need convincing see the list below. Over the past 6 years Fairfax has opportunistically monetized a few of their insurance businesses and has booked significant pre-tax gains on these sales of more than $4 billion (see list below). Yes, Digit, seeded in 2017, has become a home run. Ki, seeded in 2020, is growing like crazy. Gulf Insurance Group, seeded in 2010, has quietly grown into a very large insurance company in the MENA region. So much is going on under the hood with the insurance business at Fairfax. As i have said numerous times before: Fairfax has three engines that drive results and all three are performing exceptionally well right now: insurance (hard market), fixed income (high interest rates) and equities (much improved portfolio of holdings). Importantly, the macro environment has also aligned (value investing, cyclicals, commodities, energy). Investors in Fairfax have never had this set-up before (with everything working together at the same time). We are seeing the early benefits of the flywheel effect at Fairfax. Except their transition has not been one from good to great; rather, their transition the past couple of years has been one from bad to great (yes, the cumulative losses from the equity hedges from 2010-2020 were bad). The company is generating record levels of free cash flow. In turn, that is driving record levels of spending on (good) investments. My tracking sheet for Fairfax says they invested a record $2.4 billion in 2022 across 20 different companies. I expect more of the same in 2023. And more again in 2024. Compounding is a beautiful thing - when it is done well. I think investors continue to underestimate the results Fairfax is going to deliver in the coming years. The stock is trading today at 1 x trailing BV (Dec 31, 2022) and at 0.95 x March 31 BV (est $690) and 5.5 x 2023E earnings (est $120/share). Despite the run up the past 18 months, the stock still looks crazy cheap to me. And that is because the business results keep getting better. And the story keeps getting better. So, despite the big run up in price, the stock stays cheap. Yes, i know… makes no sense. Peter Lynch loved these situations. ————— The flywheel effect: The Flywheel effect is a concept developed in the book Good to Great. No matter how dramatic the end result, good-to-great transformations never happen in one fell swoop. In building a great company or social sector enterprise, there is no single defining action, no grand program, no one killer innovation, no solitary lucky break, no miracle moment. Rather, the process resembles relentlessly pushing a giant, heavy flywheel, turn upon turn, building momentum until a point of breakthrough, and beyond. - https://www.jimcollins.com/concepts/the-flywheel.html ————— 1.) ICICI Lombard - India Seeded in 2001 Sold in 2017 (down to 10%) and remainder in 2019 for about a $950 million pre-tax gain Fairfax had to sell ICICI Lombard (down to 10%) to invest in Digit 2.) First Capital - Singapore Seeded in 2002 Sold in 2017 for $1.02 billion after-tax gain delivered a compound rate of return of 30% since 2002 3.) Riverstone Europe - runoff sold in 2020 & 2021 for proceeds of $1.3 billion (+$230 million contingent value instrument) 4.) Pet Insurance seeded with two purchases in 2013 and 2014 sold in 2022 for a $992 million after tax gain 5.) Ambridge Partners purchased by Brit in two transactions in 2015 and 2019 sold in 2023 for $275 million pre-tax gain (hasn’t closed yet)

-

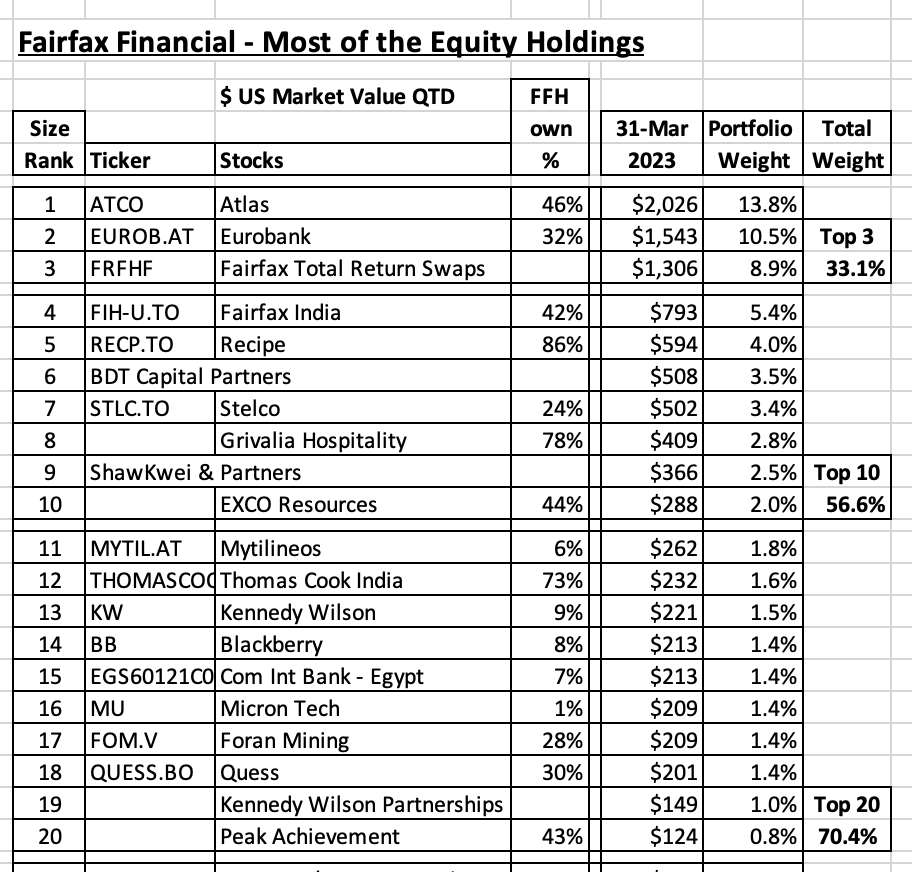

To close the loop on my deep dive into Fairfax's equity holdings, here is an approximate size ranking and portfolio weightings to March 31 2023. I removed Resolute Forest Products ($626 million) from the list given that transaction has closed. The largest private holding not on the list is AGT (we have not been given a current value from Fairfax in a while). For perspective, a $150 million investment (sounds big) is now = 1% of the equity portfolio - which is pretty small. Top 3 holdings = 33%. All are poised to do very well. And if the big dogs perform... Top 10 holdings = 57%. Top 20 holdings = 70% $2.8 billion = 20% of holdings is in 'smaller holdings' + 'other limited partnerships, associates, consolidated'

-

As a follow up to my previous post on Fairfax’s equity holdings let’s now review the 10 largest equity purchases made from 2018 to today. As a group, these investments have already delivered considerable value to Fairfax shareholders. And they like they are just getting started. 1.) Fairfax Total Return Swap (TRS) - equity derivative (2020): Late in 2020 and early in 2021, Fairfax purchased TRS giving it exposure to 1.96 million Fairfax shares at an average cost of $372.96/share. Fairfax shares closed Friday at $658/share. This puts the gain at $285/share (+71%) = $559 million (before cost to carry TRS). That is amazing return over 28 months. Fairfax shares, trading at 1 x trailing BV, are still very cheap. My estimate is this investment will deliver another $250 million return to Fairfax shareholders in each of the next 2 years; if this happens, this would put the total return at over $1 billion. This investment is quickly becoming one of Fairfax’s best ever. 2.) Fairfax (2021): in the fall of 2021, Fairfax invested $1 billion in Fairfax, buying 2 million shares at $500/share. Fairfax’s book value at Dec 31, 2022 was $658/share. My guess is book value at Dec 31, 2023 will be about $770/share and Dec 31, 2024 it will be $880/share. Stock buybacks should only be done when your shares are trading at a discount to intrinsic value. This investment already looks very good for shareholders. These first two investments show Fairfax at its very best. Value investors. Opportunistic. Creative. Aggressive (with position size). Timed perfectly. 3.) Seaspan (2018): In February 2018, Fairfax made their first investment in Seaspan (now Atlas). Why? David Sokol. Atlas is Fairfax’s largest equity holding today. Fairfax owns 131 million shares of Atlas (43% ownership) with a carrying value of $1.5 billion ($12.39/share) and a market value of $1.865 billion ($15.34/share). The first 76 million shares Fairfax invested in Atlas were purchased at $6.50/share. In the 2022AR, Prem said as the new-build strategy is executed Atlas may hit EBITDA of $1.75 billion in 2025; in 2022 adjusted EBITDA was $1.135 billion. In 2022 Atlas delivered share of profit of associates of $258 million to Fairfax. This number looks likely to increase to over $300 million/year in the coming years. This investment looks poised to be another $1 billion winner for Fairfax. 4.) Stelco (2018): in late 2018, Fairfax invested $193 million for a 13.7% stake in Stelco. A steel producer? At the time I did not like the purchase. It screamed ‘old Fairfax’ to me. Boy, was I wrong. Steel went to record prices. The CEO, Alan Kestenbaum, is exceptional. Stelco has paid regular and large special dividends. Fairfax’s position is now worth $470 million; they own 23.6% of Stelco. With all the infrastructure/energy transition/home-shoring plans - steel looks to be in a secular bull market. This investment has been a home run for Fairfax shareholders with lots of runway left. 5.) Foran Mining (2021): in Aug 2021, Fairfax invested $78 million in Foran Mining. Pierre Lassonde is another large shareholder (founder of Franco-Nevada). Foran is developing a large copper mine in Saskatchewan. As we execute the EV transition, looking out only a couple of years, it is expected demand for copper is going to exceed supply. Right about when this mine should be starting up production. Market value of Fairfax’s position is currently $220 million. It the mine works out, and copper prices move much higher, this investment is going to go much higher. Yes, lots of risk. 6.) Recipe (2022): in Aug, 2022, Fairfax invested $342 million (with $100 million coming from Recipe) to take Recipe private (Fairfax owns 84%). Fairfax has been a major consolidator of the Canadian restaurant industry starting in 2012. They understand Recipe very well. They got the asset at an attractive price (at a covid discount). Recipe has a carrying value of $594 million for Fairfax. Recipe generated free cash flow of about $110 million each year from 2017-2019 (pre-covid). They should be able to get back there, which would deliver about $95 million/year to Fairfax. This could become a meaningful and predictable cash generator for Fairfax moving forward. 7.) Large cap stocks (BAC, OXY, CVX, BABA, Micron): Fairfax invested $380 million in a number of large cap, mostly US, stocks in Q2 and Q3 of 2022. Banking. Energy. Technology. Solid companies. Good core, long term holdings. Should deliver a solid return for Fairfax shareholders in the years to come. 8.) Grivalia Hospitality (2022): in July 2022 Fairfax purchased Grivalia Hospitality from Eurobank for $195 million. Here is what Prem had to say in the 2022AR: “Recognizing the outstanding results achieved at Grivalia Hospitality by George Chryssikos, Vice Chair of Eurobank, in 2022 we increased our ownership to 78%. Grivalia Hospitality is a leading investor in Greece’s booming ultra- luxury hotel space, with three operating assets and seven under development. You will remember that George ran Grivalia Properties, a public company of which we owned 51%. Eurobank and Grivalia Properties merged in 2019 when Eurobank needed capital. The gains from Grivalia Properties and the Eurobank shares we acquired on the merger have resulted in a total gain to Fairfax of approximately $1 billion. We gratefully add George’s name to Richie Boucher’s from the Bank of Ireland, who was our first billion dollar man.” Fairfax has done exceptionally well investing alongside of George Chryssikos. Let’s hope George’s Midas touch continues to the benefit of Fairfax shareholders. 9.) Dexterra/Carillion/Horizon North (2018): in March of 2018. Fairfax purchased Carillion Canada out of bankruptcy protection (it was the UK operations that were in trouble). In May of 2020, Dexterra engineered a reverse takeover of Horizon North. Fairfax owns 49% of Dexterra. Dexterra has a near term target to get to C$100 million in EBITDA. They are funding their growth internally which is encouraging. 2022 had some near term challenges (inflation and labour) in Modular Solutions and Facilities Management units. Carrying value is $103 million. Market value today is $121 million. There is a reasonable chance company could get to its C$100 million EBITDA target in 2023. 10.) Toys “R” US (2018): In 2018, Fairfax purchased Toys “R” Us Canada out of bankruptcy for $235 million. At the time of purchase this transaction was a bit of a head scratcher. However, in 2021, Fairfax sold the retail operations and kept the real estate and the transaction made much more sense. Not sure what the current value is.

-

@hobbit and @glider3834 thanks for the info and links. Very helpful. Prem has talked a out investing billions in India in the coming years. We are seeing some smoke… I also wonder when we see the price of Fairfax India get a little more realistic. It is such a head scratcher for me.

-

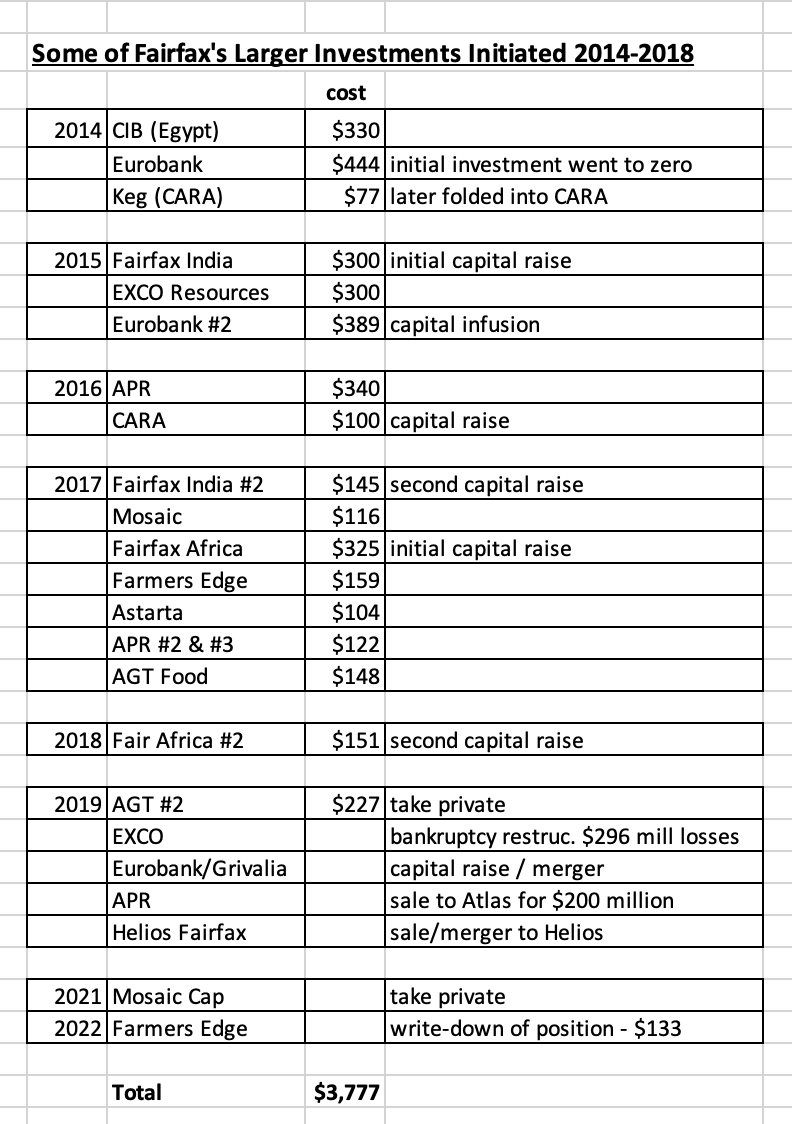

Fairfax’s equity portfolio looks very well positioned today. Most of the equity holdings purchased since 2018 have been performing well. And, after years of hard work, the poor performing equity holdings (many purchased from 2014-2017) have largely been fixed and are now performing well. In fact, the equity portfolio looks better positioned today than at any other time in Fairfax’s recent history (in terms of size and quality). We are increasingly seeing the benefits in improved reported results. The best recent example is ‘share of profit of associates,’ which spiked to more than $1 billion in 2022; the previous high was $402 million in 2021. What happened? Four things: 1.) Fairfax learned lots of lessons from the poor purchases they made from 2014-2017. They are putting a premium on management. Hamblin Watsa has decided it is not a turn-around shop - looking to actively run poorly lead/challenged businesses. They are not a piggy bank for poorly run companies in search of cash. It appears to me that Fairfax has tweaked their methodologies used when allocating capital. Others on this board argue that: 2.) the Fed and the ending of easy money (zero interest rates/QE) is a key driver in the stronger performance the past 2 years of Fairfax’s equity holdings. Value investing is back! 3.) the timing of the cycle is finally working in Fairfax’s favour and this is driving the stronger performance of the equity holdings. Value, resource and commodity stocks are all in a secular bull market. 4.) opportunities available in recent years are more in Fairfax’s wheelhouse (i.e. TRS on Fairfax shares, buying back shares of Fairfax India at 60% of BV etc). At the end of the day, all of the above is likely partly responsible for the improvement we have seen in Fairfax's equity holdings in recent years. ————— It can be instructive to look into the past so we can learn. This helps us understand what has been baked in to past results. In turn, this can help us understand what may happen in the future. What happened with the purchases from 2014-2017? 10 investments are briefly reviewed below. Fairfax invested a total of about $3.5 billion in these 10 investments over the years. Over the past 8 years my math says Fairfax booked losses in these 10 investments of about $1.5 billion (about $200 million, on average, each and every year). For example, in 2022, Fairfax wrote down its investment in Farmers Edge by $133 million. Stuff like that. Of course, the far bigger cost to shareholders has been the opportunity cost. Prem says repeatedly that Fairfax expects its equity investments to deliver returns of 15% per year. Applying a more modest 10% target, the $3.5 billion in investments (made 2014-2017) should have doubled in value by now to $7 billion. Clearly that has not happened with these investments. The opportunity cost of the poor investments made from 2014-2017 is likely an additional $2 billion. This is actually a good news post. The good news is: 1.) the equity purchases made from 2018 to April 2023, as a group, look very good and are performing well. 2.) as I will review below, the problem investments from 2014-2017 look like they are not only fixed - they are also (mostly) poised to deliver solid returns for Fairfax shareholders moving forward. An 8 year long big headwind has now become a big tailwind. As a result, I expect Fairfax’s $16 billion equity portfolio to generate a much higher total return (percent and absolute) in the coming years than it has delivered over the last decade. Given its current construction, I think it could well compound at 12% over the next couple of years = $1.9 billion/year in earnings: dividends = $120 million share of profit of associates = $900 million consolidated earnings = $240 million mark-to-market investment gains = $650 million (not including fixed income) —————- Below is a short review of 10 large investments made over the 4 years from 2014-2017. 1.) EXCO Resources (2015): Fairfax’s initial investment was $300 million in 2015. We have since learned that shale was a bubble and it eviscerated something like $5 billion in capital up until 2020. Fairfax reported cumulative realized losses of $296 million on EXCO in 2019 (that’s what they said in the AR). Learning: old economic model for shale was a sham. The good news: energy looks like it is in a structural bull market; new economic model for shale looks good - focussed on shareholder return. 2.) APR (2016): Fairfax invested a total of $462 million in APR in 2016 and 2017. In 2018 they sold it to Atlas for $200 million (in Atlas stock). The first thing Atlas did was replace the CEO. Learning: Terrible business. Poorly managed. The good news: APR is now Atlas’ problem. 3.) Fairfax Africa (2017): launched with much fanfare in 2017, Fairfax invested a total $476 million. Two short years later Fairfax exited its management of the business and moved the assets to a fund managed by Helios. The value of the Helios fund today is about $100 million. I am not sure what the total financial loss was for Fairfax on this investment but it was significant. The damage to Fairfax’s reputation was also significant. Learning: Hubris on steroids? Terrible idea. Worse execution. The good news: Fairfax is partnered with Helios and looks well positioned moving forward in Africa. This is now a small investment for Fairfax. 4.) Farmers Edge (2017): Fairfax invested $159 million in Farmers Edge in 2017. Farmers Edge completed its IPO in 2021 and in the 2021 AR Fairfax said their total investment in Farmers Edge to that point was $376 million. CEO ‘stepped down’ in April of 2022. In the 2022 AR, Fairfax said Farmer’s Edge had a carrying value of $71 million, after taking a $133 million write down in 2022. Market value of Fairfax stake was $5 million at Dec 31, 2022. My guess is this investment, because it performed so terribly post-IPO, has caused Fairfax some damage to its reputation (given Fairfax was the majority shareholder). Learning: Yup, SPAC’s were a bubble. The good news: carrying value is $71 million. This is now a small investment for Fairfax. 5.) Eurobank (2014): Fairfax invested $444 million in Eurobank in 2014. This initial investment went to close to zero later that year when the ECB came in and mandated a 1 for 100 reverse share split. What was the problem? Greece was in the midst of a depression. What did Fairfax do? It doubled down and invested another $389 million in Eurobank in 2015. in 2019, Eurobank executed a capital raise / merger with Grivalia. Greece elected a pro-business government in 2018. Eurobank fixed its balance sheet. Learnings: Just because the strategy worked in Ireland doesn’t mean it would also work in Greece. The good news: Greece’s economy is very well positioned. Eurobank, always well managed, is executing well and earnings are spiking: share of profit of associates for Eurobank was $263 million in 2022, increasing from $162 million in 2021. Prem estimated Eurobank could earn €0.20/share in 2023; if so, Fairfax’s share of profits for Eurobank could be well over $300 million in 2023. This investment is looking like it will turn into a home run for Fairfax in the coming years - a Greek tragedy turns to triumph! 6.) AGT (2017): Fairfax invested $148 million in AGT in 2017. In 2019, as AGT was experiencing financial difficulties, Fairfax took AGT private, spending another $227 million (I think). Learnings: It takes much more than a dynamic Canadian founder to succeed. The good news: from 2022 Fairfax AR: “AGT, run by founder and CEO Murad Al-Katib, had a record year in 2022, with EBITDA of over Cdn$150 million. This is a dramatic improvement from the time of the take-private transaction almost four years ago when the business was generating slightly over Cdn$60 million in EBITDA… Fairfax has an approximate 60% stake in AGT.” 7.) Commercial Industrial Bank (CIB) Egypt (2014): Fairfax invested $330 million in CIB in 2014. Today the position is worth about $240 million. Great company. Solid management. What is the problem? Egypt’s economy has been a slow moving train wreck for decades - with constant currency devaluations. Learning: Constant currency devaluations (like 50% in the last year) hurt equity values. The good news: the bank is well managed. 8.) Mosaic Capital (2017): Fairfax invested $116 million in Mosaic in 2017. In 2021, Mosaic was taken private (not by Fairfax) with Fairfax owning 20% of the new investment. This investment went sideways for may years (that opportunity cost thing). Learning: not every investment you make is going to work out the way you plan. The good news: Fairfax found a partner where Mosaic will hopefully be a better fit. 9.) Recipe/CARA (2014 & 2016): Fairfax also made a couple of restaurant investments from 2014-2017: $77 million in the Keg in 2014 (later merged with CARA in 2018) and $100 million in the CARA capital raise in $2016. Recipe/CARA was a poor investment for minority shareholders over its lifetime. Learning: the restaurant business in Canada is a tough business. Consolidating it proved to be even tougher. The good news: In the take private deal in 2022, Fairfax purchased Recipe at a covid-low price. Recipe has a solid collection of assets that should be able to produce significant free cash flow for Fairfax moving forward. 10.) Astarta (2017): Fairfax invested $104 million in Astarta in 2017. Today that investment is worth around $45 million. I know very little about this investment. I wonder if it is not a similar situation to CIB, with opportunity cost being the big issue. Honorable mention: Torstar was initiated as a position before 2014 so I did not include it. However, Fairfax added to its position in 2014, 2016 and 2017 (yes, small amounts). In 2020 it sold the business and booked a $52 million loss. I see lots of self inflicted wounds in the investments listed above - the list reminds me of the Monty Python skit “tis but a scratch" (see bottom on post for some entertainment).

-

@valuesource The big difference I see at Fairfax today compared to 2 years ago is the size of future earnings for all important buckets is materially higher: underwriting profit + interest & dividends + share of profit of associates + investment gains (this is the most volatile). When I worked at Kraft and Saputo I used to spend weeks every fall building the next years annual business budget for the business I was managing at the time. My experience was if you get the 'big rocks' right your final forecasted numbers tend to be quite accurate (all the pieces move around but the final number comes in remarkably close at the end of the following year). To get the 'big rocks' right the key was quantifying the puts and the takes (the changes - the big business gains and losses, new products etc). I try and do the same logical build with Fairfax. Everyone can see my building blocks. And therefore can make adjustments as they see fit. I am constantly making adjustments to my Fairfax estimates - it is, after all, simply an educated guess. As new news becomes available, the estimates change. What is nice with Fairfax is interest and dividend income is now the biggest component of earnings. The run rate at Dec 31, 2022 was $1.5 billion and I expect this number will be higher when Fairfax reports Q1 results. This bucket is pretty predictable quarter to quarter and should provide a nice anchor to reported results.

-

@hobbit thanks for posting. Do you have any thoughts? 1.) is IDBI worth pursuing? 2.) what would the approximate cost be? - my assumption is FIH would need partners. 3.) how does FIH pay for it? Without current shareholders getting thrown under the bus? - or could they fund it by contributing CSB and cash ($300 million or so?) and parters pony up the rest? Is it possible for Fairfax India to do a capital raise? With shares trading at around $13 and BV at $19? Or do we see Fairfax India sell some more of the companies they currently hold? ————— Do you have any thoughts on Anchorage? Will we see something happen on this front in 2023?

-

@Munger_Disciple When i put together my forecasts for Fairfax (any company) i tend to look one or perhaps two years out. Too many variables change to try and look out 3 years and more with any precision. My current estimate is for Fairfax to achieve a 95 CR in 2023 and 2024. Same as what my estimate was for 2022. With most forecasts i usually start with the trend and then incorporate new news. Each quarter i tweak my estimate based on actual results. Too aggressive? We will see. As i get new news i will adjust my estimate. The average the past 10 years has been 95.7 and the average the past 2 years has been 94.9 (and cat losses have been quite high the past 2 years). We are still in a hard market (yes, it is slowing). Reinsurance hard market looks like it just started (property cat) - this could be very beneficial for Odyssey. We will find out with Q1 results more on this front. Fairfax continues to improve as an underwriter. Brit has been a problem in recent years and Fairfax has said they will be significantly reducing cat exposure for Brit in 2023. I think Andy Barnard has done a fantastic job over the past 10 years, including integrating all the large purchases. In terms of using a 95CR in my previous post… it was just used as a random example. I was trying to show the change in underwriting profit over 13 years.

-

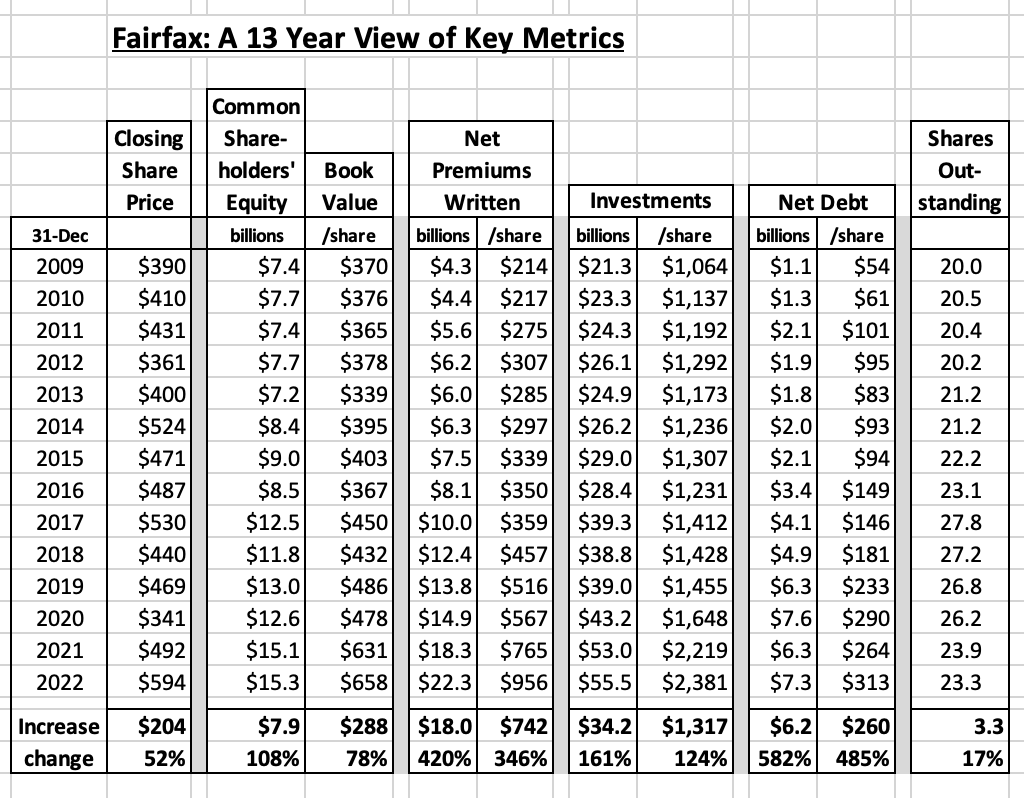

Below is a 13 year history of a few key metrics for Fairfax. What are the key take-aways? 1.) Fairfax's most important business, insurance, has grown 420% (350%/share). This is a crazy amount of growth. And has vaulted Fairfax into the top 20 of global P&C insurers. 2.) Fairfax's second most important business, investments, has grown 160% (125%/share). Not as impressive as the growth in the insurance business, but solid. What is the math? Let's assume a 95CR and a 6% return on investments: underwriting + investments = total (millions) 2009 $214 + $1,276 = $1,491 = $75/share 2022 $1,114 + $3,329 = $4,442 +200% = $190/share +156% 3.) Fairfax's book value has increased 78% over the past 13 years. 4.) Fairfax's share price has increased 52% over the past 13 years. It doesn't look to me like Fairfax's BV or share price over the past 13 years have kept up with the increase in intrinsic value. --------- Yes, I am ignoring the significant increase in net debt. For reference, interest costs at Fairfax will run about $500 million in 2023. I am also ignoring minority interests (Odyssey, Allied and Brit). Cost of $200 million per year (8% of $2.5 billion)? Thoughts?