SafetyinNumbers

-

Posts

2,822 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

I’m sure most people passed on the gold stock idea (most people invest only in quality and junior gold stocks are the furthest thing from quality) but MKO just announced a deal in Arizona risking only $5-10m to buy an operating gold mine out of bankruptcy. If they are able to optimize the mine it could double the existing corporate production run rate within 6-12 months. Given it’s less than <3x OpCF without it that’s a big improvement. The stock is up a bit since the announcement but this is a play for the cycle with a small amount of capital as gold mining has plenty of execution and geopolitical risk but the upside is multiples of capital given the right tails on production, resource size and the gold price.

-

That’s how I interpret the articles I attached above. I’m not a lawyer so could definitely have it wrong! I’m wrong a lot as I’m always trying to fill in the blanks when provided with incomplete information. This sort of structure does make sense and is consistent with other deals Fairfax has done except with this option to IPO. It’s really brilliant if that’s in fact the intent. It’s a home run for FFH and BX so it makes sense that’s how it works. I took a screen shots of some key parts in the articles that influenced my thinking. I figure we’ll learn more at the AGM at the latest so it’s not that important except it highlights the abundance of material right tails that are in the portfolio.

-

Thanks Viking for all of your hard work. It’s very much appreciated. I’m much more optimistic on the total return CAGR. 15% is low end average ROE and with no multiple expansion the stock would return 15% ignoring dividends to make it simple. Given the high level of core earnings I think it’s really hard for ROE to fall below 15%. We know that FFH has high return opportunities for excess capital like buybacks and minority interests in the insurance businesses. The portfolio also has a lot of optionality and I think most would agree a market disclocation is likely over the next four years. That will be an opportunity to accelerate returns. Plus, there are so many insurance (Ki, Digit) and non-insurance (FIH/BIAL, EUROB, TRS) right tails and likely many more that we don’t focus on. Its arguably more likely for ROE to average 20% than 15% over the next 4 years. Maybe 25% is just as possible as 10%. BVPS CAGR is what determines the stock price and buybacks have helped BVPS more than double in 4 years. If it doubles in the next four years again won’t the multiple continue to expand as it has for the past 4 years (albeit unevenly)? If on Jan 1 2029, BVPS is $2200 and the stock price is up 4x, the multiple will be only 2.5x P/B a discount to Intact Financial which trades at ~3x P/B now. I realize that discussing the right tail possibilities is not polite in most value investor company so please be kind when you tell me why I’m wrong and why FFH is too expensive to start a new position.

-

Not if existing shareholders will be locked up for some time. Plus its Anchorage that is supposed to IPO, not BIAL, directly.

-

Maybe but they use that capital to win infrastructure contracts. They probably have other deals to bid on which will have higher returns and they probably were convinced by BIAL that they will have the future business there despite no longer being a shareholder.

-

Some people don’t know a fat pitch when they see one. Still surprised how many investors own BRK and MKL but no FFH.

-

The filings are available here: https://find-and-update.company-information.service.gov.uk/company/12594708/filing-history?page=2 Articles attached. Ki Articles of Incorporation 9.23.20.pdf

-

My BIAL math was overstated but I don’t think the Siemens price is very relevant to where BIAL will trade once it lists. The whole FIH is marked at a fraction of intrinsic value. The spread might not be $100/share but it’s pretty big.

-

FFH owns 20% of Ki via Class A shares but 50% of the shares outstanding are preferred shares (Class C) similar to what FFH just bought back from OMERS in Brit. They are structured to be paid back with new shares at the listing price so effectively FFH has 40% ownership which will be diluted on IPO. I do think 5-10x premiums is not unreasonable for an AI powered insurance startup growing premiums exponentially backed by Blackstone. I didn’t previously appreciate how these minority interest structures were materially understating FFH economics. Those benefits will also come in when Allied World and Odyssey are bought back in over the next few years.

-

If you are looking for top shelf capital allocation skills in oil, I suggest checking out Strathcona’s Investor Day presentation. The first 48 minutes is a master class by Adam Waterous on energy investing through a value/quality lens. At $70 oil, they plan to return C$26/sh to shareholders over the next 6 years while growing production over 50%. WEF, the private equity fund founded by Adam, controls 91% of the shares and plans to start passing them through to LP holders in March. The increased float will make SCR eventually eligible for the S&P/TSX Composite which should help with a rerate closer to NAV but I plan to hold on for a long time. WEF also recently took control of Greenfire Resources, another oil sands company with a strong growth profile. That company is undergoing a strategic review so I expect we’ll see some news over the next 3-6months. SCR and GFR are ~6.5% & ~5% positions, respectively, for me.

-

What do you calculate as Fairfax’s ownership? What listing price are you assuming in the calculation?

-

Maybe you can share your own assumptions on BIAL and Ki as they seem high to you, you must have something in mind.

-

4 years ago I didn’t appreciate what a move in interest rates was going to do for base ROE. We hadn’t had the hard market yet either so premiums were a lot smaller and I didn’t know they were going to be able to grow so fast. The margin of safety on earnings is higher now than it was back then even if the stock is now trading at a premium to book vs a discount. Eurobank may have sustainable ROE of 15%+ which means it’s probably worth north of 2x BV. I’m not saying anyone will pay it anytime soon but it does mean buybacks can meaningfully improve EPS. They may also be able to continue doing accretive deals like Hellenic which seems very accretive. Ki and BIAL are also $100/sh+ opportunities in gains potential each when they IPO. That’s on top of the current FV over CV close to $100/sh. I think you are correct that it’s an attractive compounder. Forward ROE is likely somewhere between 15-25% over the next 5 years but it makes a big difference where it lands in that range to total returns especially if multiple expansion is has correlation with ROE. Not everyone invests the same though. That’s what makes a market.

-

I added a small amount yesterday too. I really shouldn’t at a 45%+ position but the more I learn, the more excited I get about the prospects of 20%+ ROE over the next 5 years given the H4L rates, high return reinvestment opportunities (buybacks, minority interests buy ins) and all of the right tail options in the non-fixed income portfolio (Ki, BIAL, EUROB…). I don’t expect every call to be right just that it is logical in the context in which it was made.

-

The data is in every annual report but it’s not in chart form

-

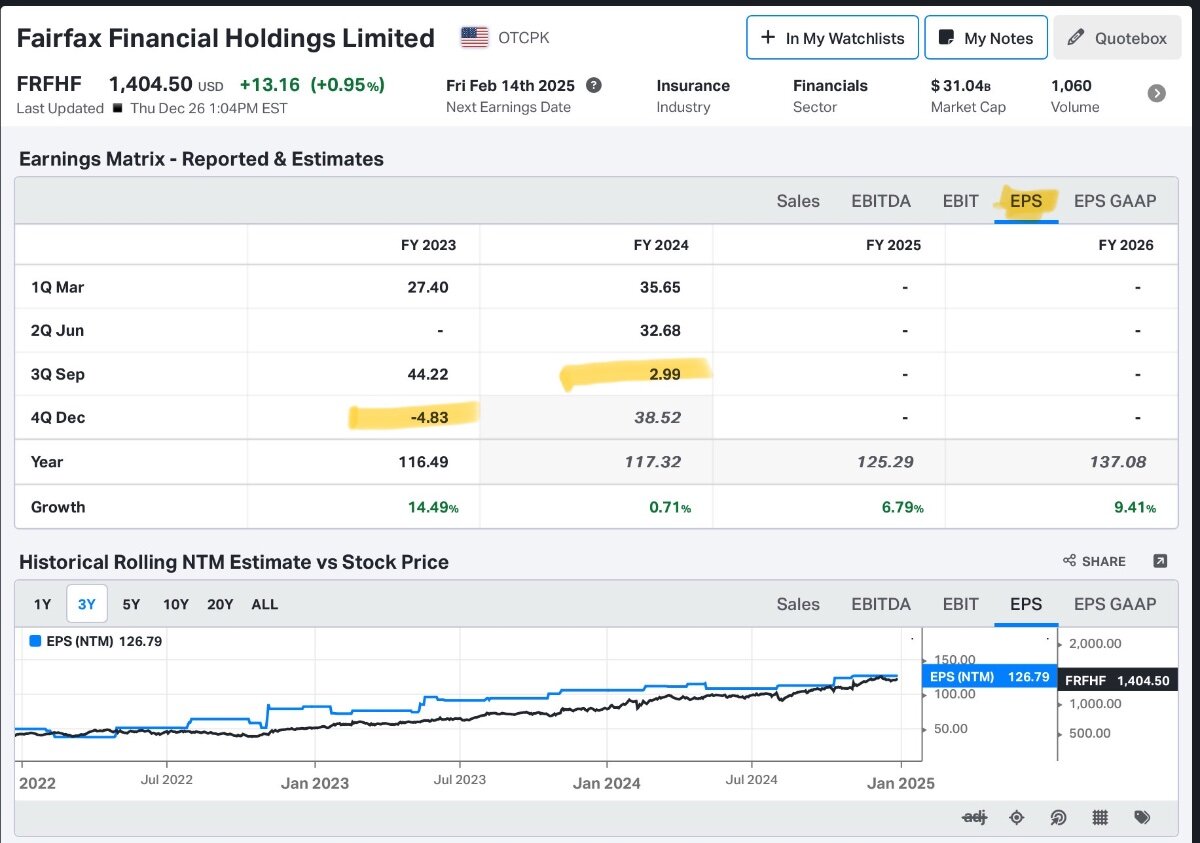

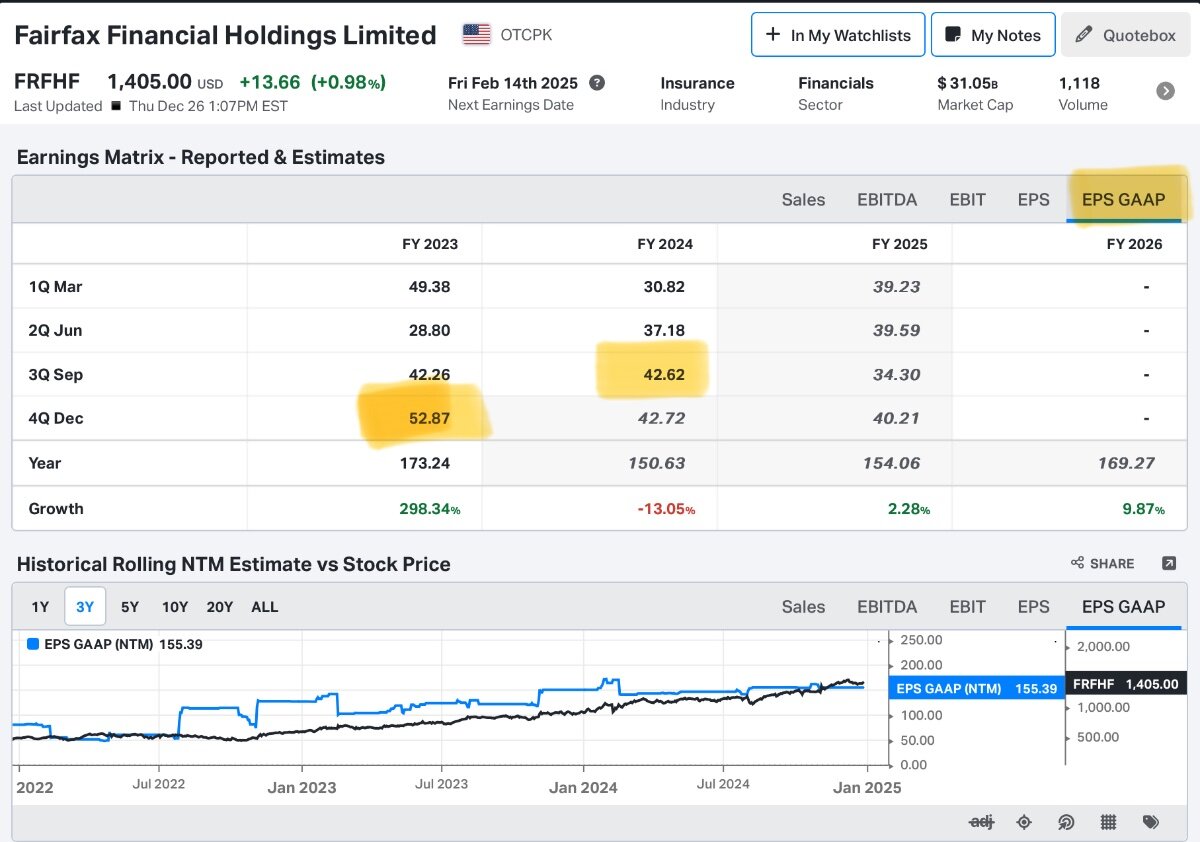

This spike in yields is super interesting if you are like me and focused on not just the fundamentals but also multiple expansion. One way multiples expand is if there is price insensitive buying like quants and passive. That’s why earnings beats/misses often result in outsized moves. I have written previously about the quirky way that FFH reports making it look more expensive than it actually on a forward P/E basis. To recap, FFH only reports IFRS EPS unlike most companies that report adjusted EPS. Unsurprisingly, for most stocks adjusted EPS has a higher correlation to stock price movement so most screens ignore GAAP/IFRS EPS. Seven financial analysts cover FFH. All seven have GAAP EPS estimates. Two analysts have adjusted EPS estimates, Morningstar and RBC. Morningstar has the same estimate for Adjusted EPS and GAAP EPS but RBC reports core earnings in that spot which excludes gains/losses. When FFH is screened on trailing core earnings it looks like it trades at 21x trailing which doesn’t seem very cheap. Plus FTM EPS looks like it’s $127 which is 11x earnings with low predictability. Adjusted EPS was particularly weak in Q423 and Q324 because interest rates declined significantly. Under IFRS 17, that forces FFH to revalue their insurance liabilities higher which hurts underwriting profit. The gains/losses on the bond portfolio more than offset on an economic basis but they aren’t captured in core earnings. Both quarters look like misses but we can see they were very healthy on an IFRS basis. In Q424 as @gfp highlighted rates are up a lot so this quarter should be the opposite. Underwriting profit should be up a lot and take adjusted EPS along with it while bond losses will be in IFRS EPS. There are also lots of equity gains (STLC, PAA, FFH TRS) so it’s possible both numbers beat consensus by a decent margin. In theory earnings beats bring buyers so we might get some multiple expansion.

-

They have the same business model i.e. using insurance float for “leverage” to make equity investments so that’s why a comparison is interesting. Just like any investor that invests in equities on an absolute return basis though their idiosyncratic returns will be unique. I’m using BRK to open my mind up to the possibilities with FFH. The more time I spend on it, the more right tails I get excited about so one can see how ROE can average way higher than anyone expects. Investors selling it at 1.4x BV because they think that’s fair might miss out like those who sold BRK in early 1985. The odds FFH can compound BV at 25% a year for the next decade, like BRK did from 85-94, are probably pretty low but they are not non-zero and could be north of 10%. I like free/cheap optionality.

-

No, not inflation adjusted. Just based on market cap at the time.

-

My biggest add in the past 3 months is SCR.TO or Strathcona Resources. It’s buy and hold investment in oil which most people aren’t comfortable with but this is a growth and capital return story with top of class management. If you have a spare 48 minutes I suggest watching Adam Waterous present at the SCR Investor Day on Nov 14. The stock gapped up that day and has since pulled back below to where it started as oil markets have been a bit squishy and everything else was going up faster. https://www.strathconaresources.com/investors/#presentations

-

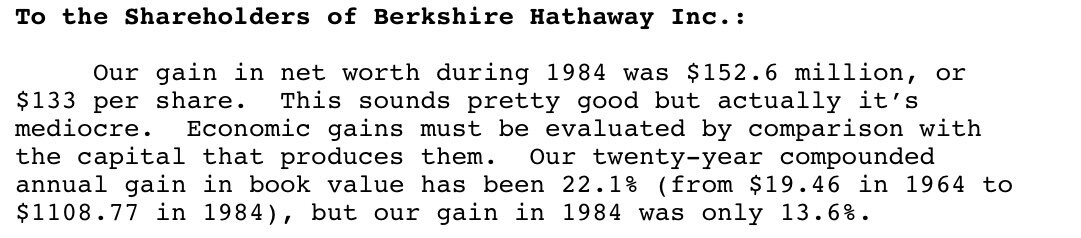

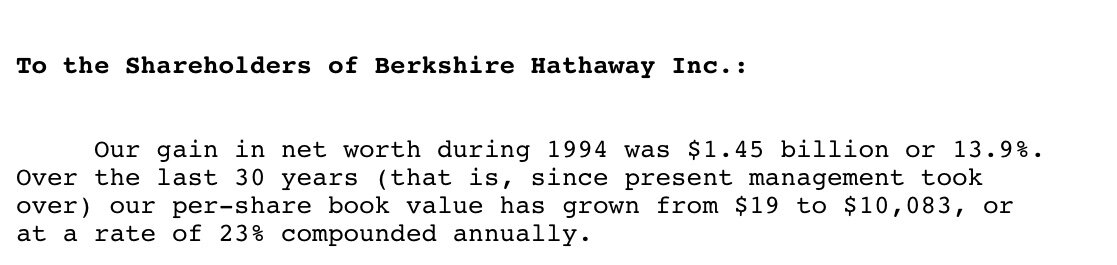

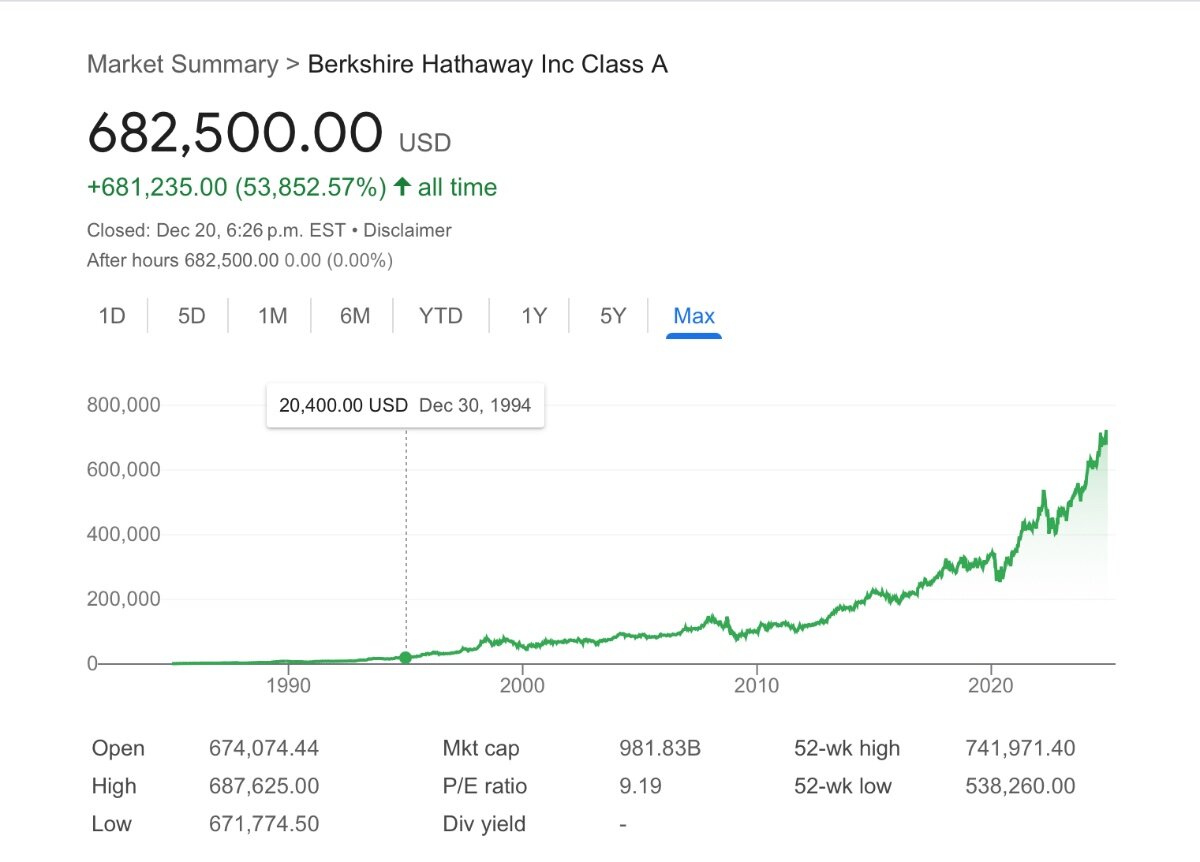

Thanks for sharing! I love these analogs because it opens my mind up to right tail potential. 1984-1994 is where a lot of the magic happened. BRK’s BV went from ~$1100 to ~$10000 or a ~25% CAGR and the multiple went from ~1.35x to ~2x. Combined that was a ~30% CAGR. Since then it’s been closer to ~12% which is still great but well below most quality investors hurdle rates. Fairfax is a lot bigger than BRK was in 1984 and is actually a lot closer to BRK’s size (market cap) at the end of 1994 but given the set up, it’s not out of the realm of possibility that FFH can match that decade over the next decade. My hurdle rate is 10% so to have that right tail potential with margin of safety is very compelling to me.

-

Very few stocks available that benefit from higher rates, a stronger USD and a sell off in quality stocks. FFH price might go down with it in the short term (as holders either need liquidity or think they are switching into something cheaper) but expected forward ROE is probably going up. It also looks there is a plan to IPO Ki. I don’t know it well but it seems like BX has 80% of the equity (Class B & C) but there are different classes with different rights. The Class C appear to be cheap leverage with an 8% preferred return that gets repaid at the listing price meaning they may result in a big increase in Brit/FFH’s equity stake. These are like OMERS shares in Brit which appear to be 6% and understated FFH’s economics. Ki might attract a very healthy multiple to book value and/or premiums given the nature of company (fast growth/AI) and the players (BX). Ki will likely do north of $1b in annual premiums soon so it could be material to FV over CV if it lists at 5-10x premiums. Ki Articles of Incorporation 9.23.20.pdf

-

I think FFH was mentioned in passing so I will go with my second biggest position Mako Mining MKO.V MAKOF. Mako is a gold producer trading < 3x OpCF and <1x 2028 OpCF. They are taking the FCF and investing it in exploration and building a new mine in Guyana. Gold companies are the furthest thing from quality but they enjoy enormous right tails given that the gold price also enjoys enormous right tail potential. I oversized Mako because I’m a big fan of the management team and the controlling shareholder Wexford Capital. Wexford also created Diamondback Energy (they like animal names) in 2007 and took it public in 2012 as their oil play. Since then it’s compounded at ~24%. Mako is their gold play and the cycle is just beginning. In full disclosure, I’m on the board of Sailfish Royalty FISH.V which spun out of Mako a few years ago and has a royalty/stream on Mako’s project in Nicaragua. FISH is also controlled by Wexford. I’m excited to see how Mako can compound over the next 5-10 years as every time the deal it will be accretive. The risk of course is on execution and geopolitical which is true for any gold stock.

-

Looks like Northbridge is putting up most of the cash for the buyout. I bought some at 7.5 cents when the deal was announced. Seemed like a low risk arb.

-

Looks like they made 6% on this one.

-

I agree but I did think this financing was more expensive. Happy to be wrong.