SafetyinNumbers

-

Posts

2,819 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

Fairfax is Canadian and I don’t think moving to the US is something Prem wants to do. I’m not advocating for the 60 add. It’s just something that’s going to happen.

-

I think that’s right, the key is the high quality insurance operations although I still find investors who don’t think FFH has high quality insurance businesses. It’s worth searching Buffett and float on YouTube. Lots of great clips from the AGMs over the years.

-

I think we can estimate float off of the quarterly balance sheet by taking insurance liabilities less reinsurance assets held. That was ~$39b at the end of Q3, up from ~$35b at end of 2023. On the float value, I agree with Buffett.

-

Using expensive paper helps with margin of safety, no question.

-

I’m curious when you did the exercise did you factor in the related float and how much the earnings were from that? I’m curious what the total return has been so far.

-

So he should have known better based on what he knew at the time and still went ahead?

-

You didn’t ask me but that has never stopped me before. I think this is a question that’s really about estimating intrinsic value. I use three methods to triangulate FFH’s intrinsic value range. 1. Normalized PE. 15x is generally considered a fair market multiple and FFH is a better than average business so 15x FTM EPS seems reasonable. While consensus is $155, it’s probably too low, it still gives us $2325 or ~66% above current prices around $1400. 2. Relative P/B multiple. There is an exponential relationship between P/B and ROE which makes sense. A high ROE compounds much faster so it makes sense to pay more than 2x for a 20% ROE vs a 10%. When looking at FFH peers, an ROE between 15-20% should command a P/B closer to 2.5x. With so much in the multiple we can just use trailing BV instead of making the adjustments to FV etc. 2.5x BV is ~$2585. 3. Buffett method. This is the sum of BVPS and float per share. Buffett has made it pretty clear that float in the hands of a high quality insurer is worth at least the amount of the float. This makes sense because the income associated with the float accrues to the insurer and consistently grows over time. For FFH this is ~$2800. That leaves me with an IV range of $2325-2800 which is wide but well above the current price offering large margin of safety.

-

It’s a pretty bifurcated market. Parts are inflated and parts are depressed. Although most people can never buy the depressed parts because of heuristics.

-

Perhaps they are considering an IPO if the valuations are favourable at some point?

-

This is resulting though isn’t it? Buffett issued expensive stock to buy Gen Re and clearly expected a better result than what he got. Execution is the hardest part of probabilistic investing. Everything I buy is clearly cheap if the companies execute as expected but about a third of the time they don’t. Thankfully the winners more than offset the losers over time (at least so far).

-

The 20% ROE for four years straight in the late 90s for FFH and BRK’s returns were based on very strong equity markets. That’s not the case for FFH right now. It has much higher earnings consistency now than it ever has because the float to equity ratio is so high and the insurance business so profitable. May/e we can’t achieve multiples like other high return insurance companies like KNSL or RLI because our earnings are too volatile but if the conditions ever existed to do it, it’s over the next 5 years. I’m not sure what the odds are but it’s better than none.

-

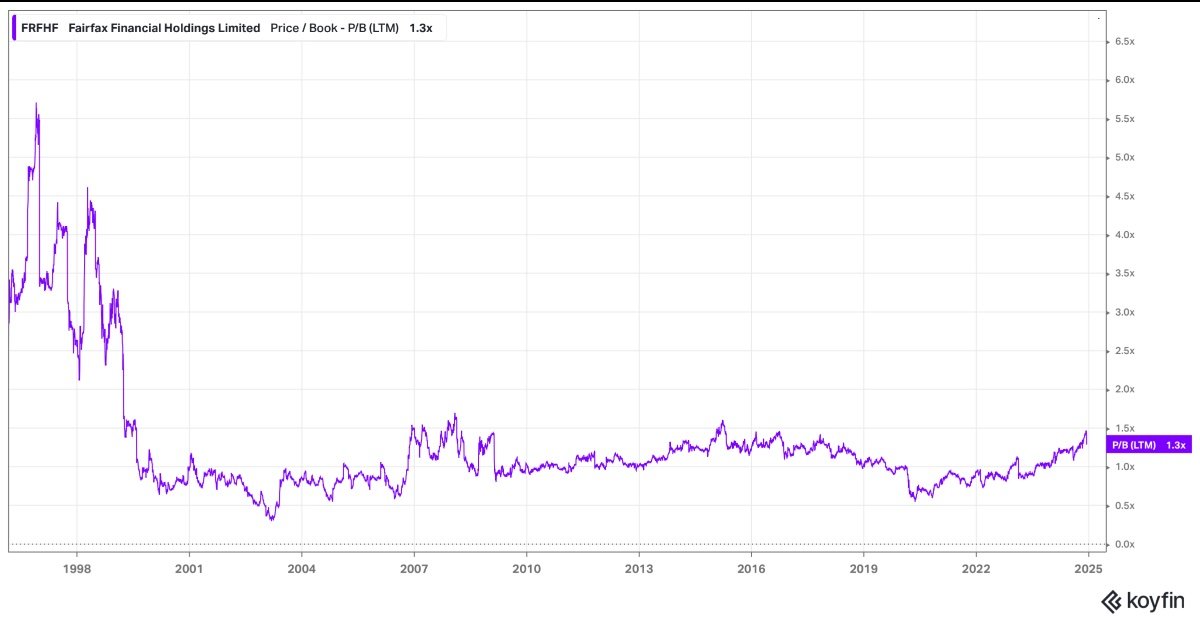

I’m not in accumulation mode. It’s 45% of my portfolio. I don’t want to keep adding but it keeps getting better and giving me chances. I’m also trying to encourage others to take a look and to appreciate the right tails and not assume that the risk/reward is not favourable to consider starting a position at this price. That being said maybe Parsad will be right and the forward return won’t meet their hurdle rate. My hurdle is only 10% so I have more margin of safety. I remembered the high end of the P/B being 6x on this chart but I think I rounded up. I didn’t pick a fantastic number for the sake of it. I based it on history. I’m not saying it’s going to happen again but I am saying it can. Which is why my sell criteria is growth based and not valuation based but I concede it will get difficult to hold on if multiples do start going north of where I’m comfortable adding if I didn’t own any but I’m certainly not going to complain about it.

-

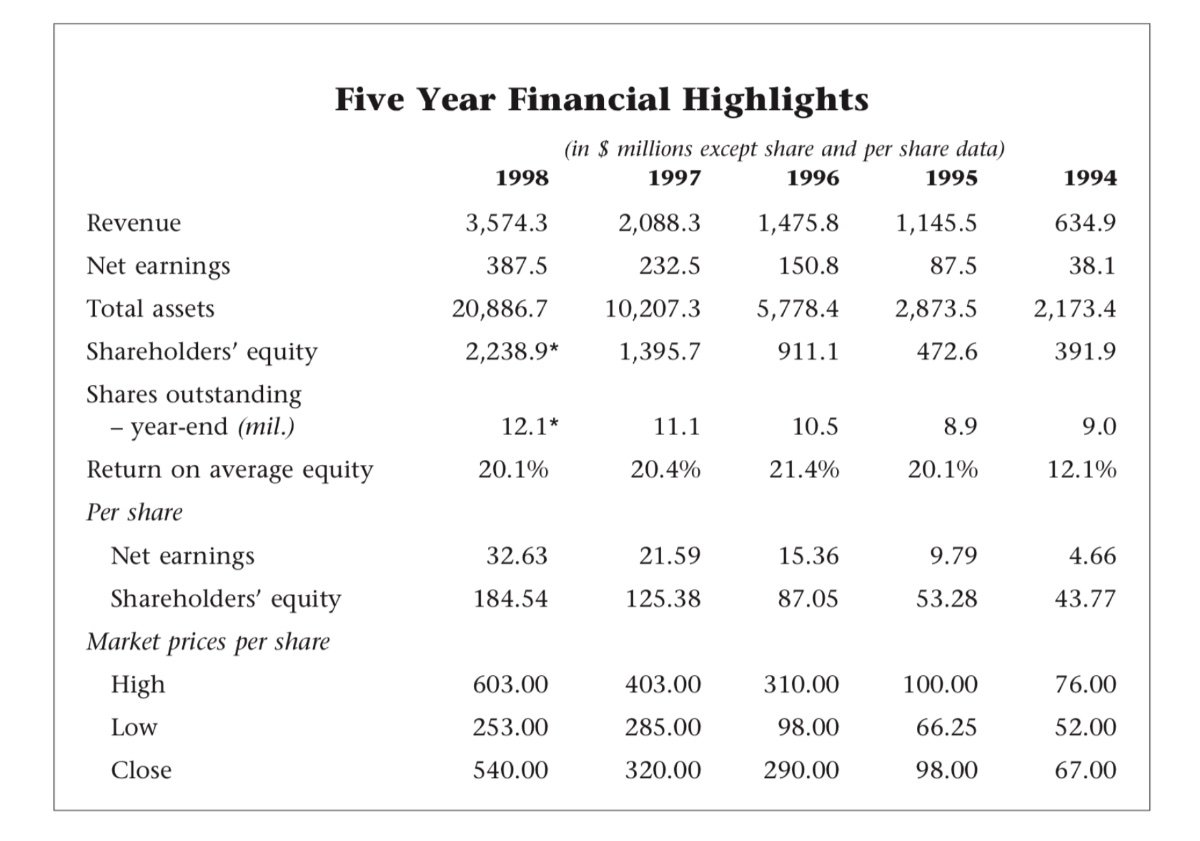

All good points. Most market participants think markets are efficient. Premium analysis is used by investment banks and their corporate clients to justify the sale of a company well below intrinsic value. Companies also use overvalued paper often to raise cash or to buy companies. AOL/Time Warner is a classic example. FFH did the same thing Berkshire in the late 90s. They bought struggling insurance companies with high combined ratios and large floats by issuing equity. The shares outstanding went up by more than a third and more than half of book value growth was from issuing shares at a premium to growth. if we are business owners or if we are investors, why wouldn’t we want that to happen again?

-

That’s fine and maybe we all should even though it might be on its way to 6x BV. As Parsad said, the goal is to grow intrinsic value and it grows faster if issuing equity well above intrinsic value or if doing accretive things with the proceeds. Prem’s not selling and the company will be worth more if they take these actions. I just don’t understand why anyone would be disappointed if the multiple went up a lot from here but you both seem to be.

-

I think you are confusing margin of safety which refers to each individual investor’s capital at risk with drawdown risk. If one is investing like a business owner the selling shares at 4x BV is going to be incredibly accretive to book value and likely returns assuming whatever is being bought with the proceeds has a reasonable return. If I’m a business owner, why wouldn’t I want that?

-

I don’t see why not and it’s what they have done in the past. Hopefully to buy a high quality business at a fair price. If FFH traded at 2x BV when Alleghany was in play, it could have easily outbid Berkshire and it would have been a very accretive deal that also let Y shareholders defer their gains.

-

It reduces margin of safety for an investor buying at a high multiple. For a business owner that bought at a much lower multiple it increases resilience to shocks and increases the odds of accretive acquisitions. I think FFH is a good capital allocator so I want them to have more tools in their tool box in the very long term.

-

I consider intrinsic value as the price from which I can earn a 10% return going forward. The discount rate that is used is very important and something you failed to mention. I’m not buying FFH at 4x BV and I wouldn’t suggest anyone else do it but the stock issued back then by the company to buy insurance businesses is part of the reason we have the opportunity we do now. It was also incredibly accretive to book value. For the shareholders who bought at a much lower multiple, it’s worked out quite well.

-

5x is compounding the book at 20%which is possible given the equity portfolio and optionality on the asset allocation and a doubling of the multiple. Cheers!

-

You have high return expectations than most. I think FFH goes up 2-5x in 5 years which is well above my hurdle rate of 10%. If we get multiple contraction then I may be wrong.

-

Intrinsic value is some multiple of book value to say that multiple expansion is irrelevant doesn't make sense to me. I think FFH is trading well below intrinsic value. It's fine if you think we are there or above it already, that's what makes a market.

-

I like Fairfax because it’s cheap and growing fast. The multiple expansion is a right tail that can dramatically increase returns. I know most value investors ignore it and it’s why most of the professional ones are out of business or have become quality investors. The only types of buyers that don’t care about the value factor are passive, quality/quant/heuristic and yield buyers. I think when a big buyer that doesn’t care about price is going to buy we could have price discovery as the rest of the shareholders who care about the value factor have a decision to make. That’s why I started this thread in the first place. I want to appreciate how extant shareholders think about selling as it might help me appreciate the clearing price. In the short and long term, it’s still about supply and demand. I’m not sure if we would have had the run we have had without FFH clearing out 7m out of 27m shares (including TRS). I’m also not sure how high the multiple can get if FFH puts up 8 years of 15%+ ROE (halfway through that now) and gets added to the 60. I want that exposure to the upside and it’s hard for me to see a lot of downside.

-

That might be true but a broad market pullback likely lifts forward ROE for FFH if they reallocate from the fixed income portfolio to quality equities. FFH can also be aggressive with buybacks given the low P/B multiple and fast growing BV which will help stem a broader decline and also increase forward ROE. I don’t consider price volatility as risk the way most market practitioners do but everyone is on their own idiosyncratic journey.

-

Nothing leaves the 60 unless it’s bought out or gets too small. Neither seem probable for FFH once it gets in. It’s a new 4% shareholder that buys stock every week. It encourages all of the active managers that are benchmarked to the index to take a look at FFH which may also increase demand. For investors that don’t own any FFH yet, it makes sense to pay attention to what might increase the multiple. I think stock prices are about supply and demand but others think the market is efficient. To each his own.

-

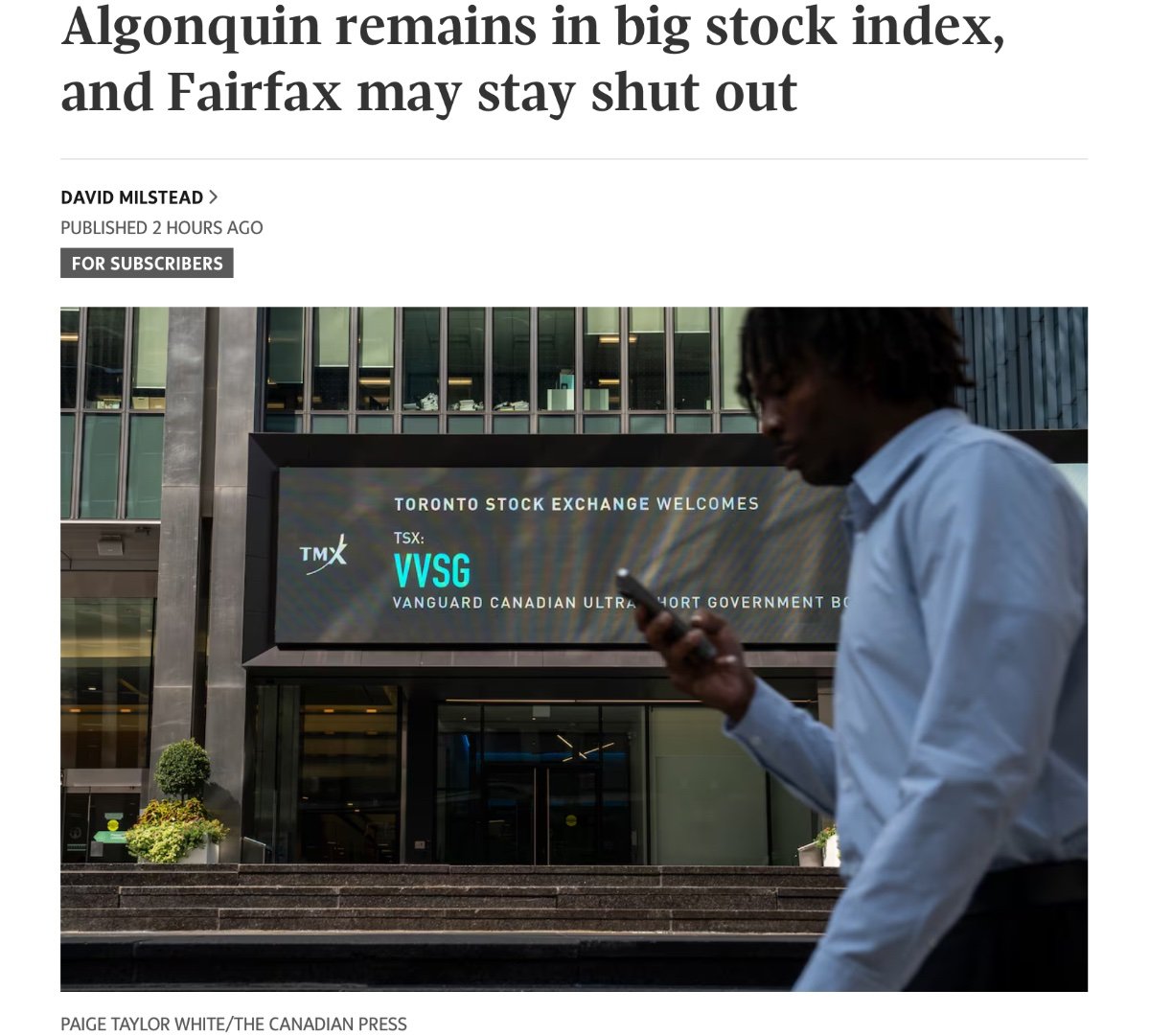

Hard disagree. The index add has the potential to result in long term multiple expansion. The higher the multiple, the more resilient FFH is to shocks. That’s a very good thing for very long term shareholders. If Berkshire wasn’t in the benchmark it would probably have a much lower valuation today, FWIW. Also, here’s your headline, courtesy of Scotia and the Globe and Mail.