SafetyinNumbers

-

Posts

2,825 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

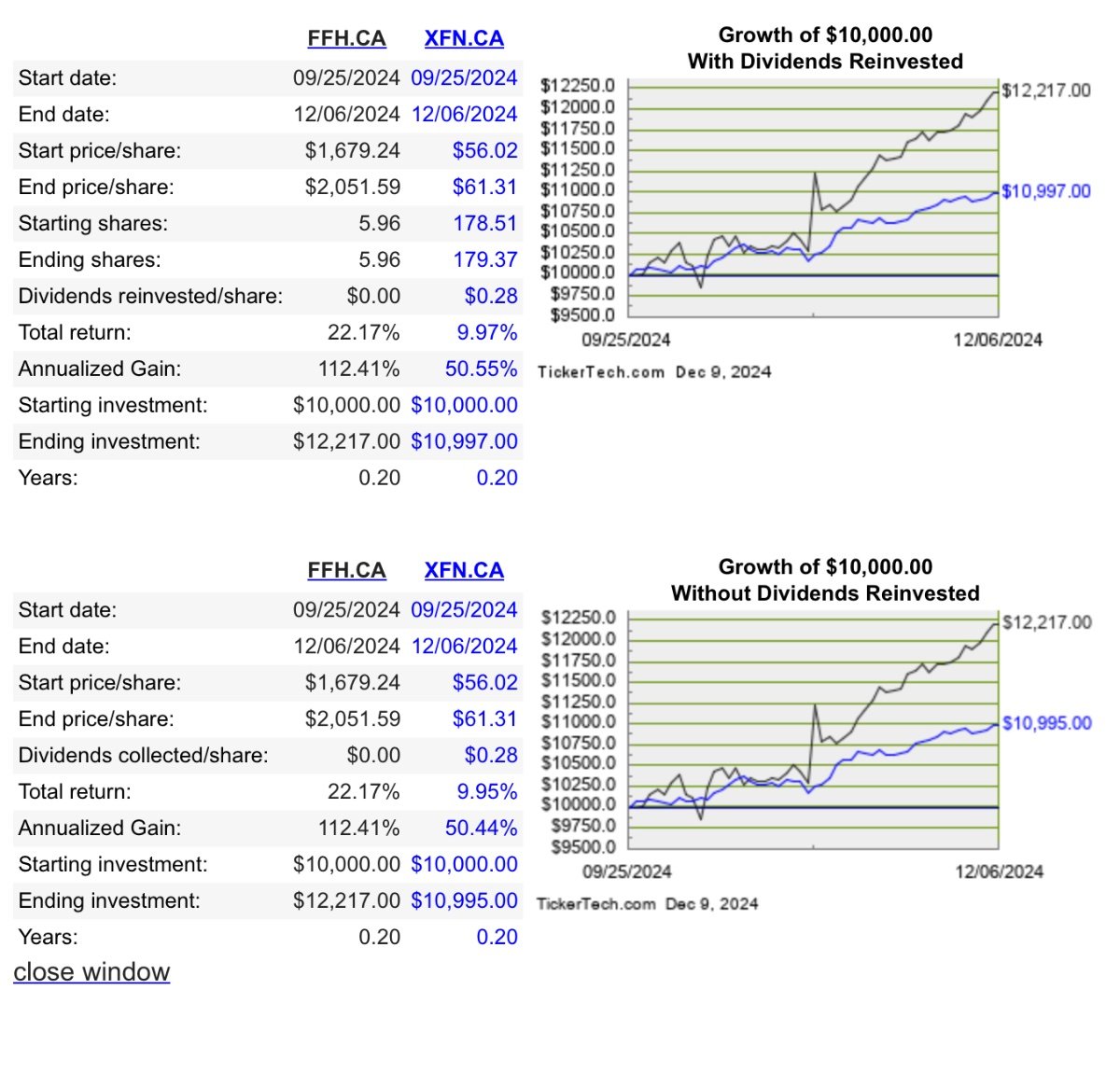

You have high return expectations than most. I think FFH goes up 2-5x in 5 years which is well above my hurdle rate of 10%. If we get multiple contraction then I may be wrong.

-

Intrinsic value is some multiple of book value to say that multiple expansion is irrelevant doesn't make sense to me. I think FFH is trading well below intrinsic value. It's fine if you think we are there or above it already, that's what makes a market.

-

I like Fairfax because it’s cheap and growing fast. The multiple expansion is a right tail that can dramatically increase returns. I know most value investors ignore it and it’s why most of the professional ones are out of business or have become quality investors. The only types of buyers that don’t care about the value factor are passive, quality/quant/heuristic and yield buyers. I think when a big buyer that doesn’t care about price is going to buy we could have price discovery as the rest of the shareholders who care about the value factor have a decision to make. That’s why I started this thread in the first place. I want to appreciate how extant shareholders think about selling as it might help me appreciate the clearing price. In the short and long term, it’s still about supply and demand. I’m not sure if we would have had the run we have had without FFH clearing out 7m out of 27m shares (including TRS). I’m also not sure how high the multiple can get if FFH puts up 8 years of 15%+ ROE (halfway through that now) and gets added to the 60. I want that exposure to the upside and it’s hard for me to see a lot of downside.

-

That might be true but a broad market pullback likely lifts forward ROE for FFH if they reallocate from the fixed income portfolio to quality equities. FFH can also be aggressive with buybacks given the low P/B multiple and fast growing BV which will help stem a broader decline and also increase forward ROE. I don’t consider price volatility as risk the way most market practitioners do but everyone is on their own idiosyncratic journey.

-

Nothing leaves the 60 unless it’s bought out or gets too small. Neither seem probable for FFH once it gets in. It’s a new 4% shareholder that buys stock every week. It encourages all of the active managers that are benchmarked to the index to take a look at FFH which may also increase demand. For investors that don’t own any FFH yet, it makes sense to pay attention to what might increase the multiple. I think stock prices are about supply and demand but others think the market is efficient. To each his own.

-

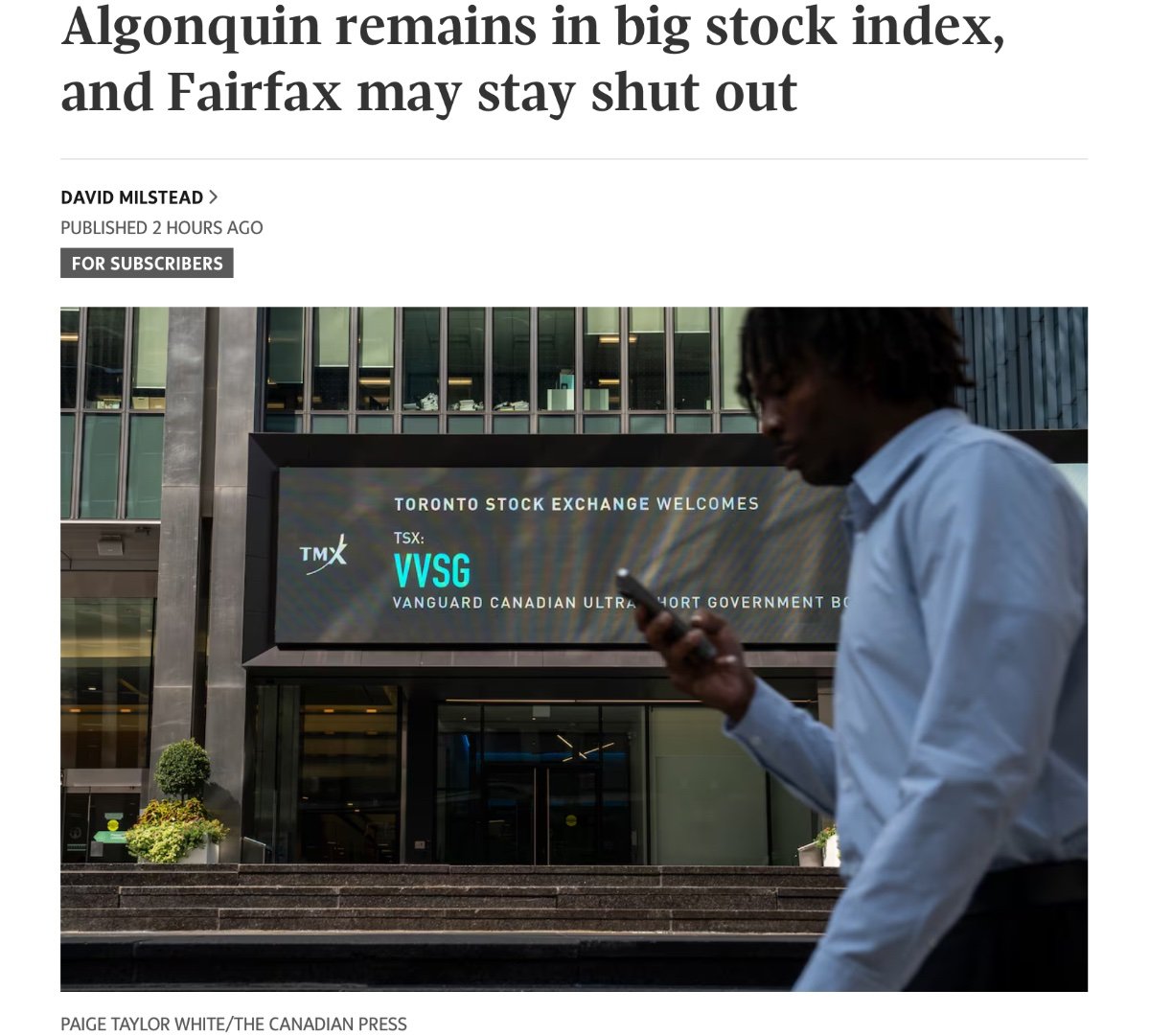

Hard disagree. The index add has the potential to result in long term multiple expansion. The higher the multiple, the more resilient FFH is to shocks. That’s a very good thing for very long term shareholders. If Berkshire wasn’t in the benchmark it would probably have a much lower valuation today, FWIW. Also, here’s your headline, courtesy of Scotia and the Globe and Mail.

-

The question was meant to ask if you didn’t own it already would you start a position now? Try putting yourself in the shoes of someone who wasn’t as smart or lucky as you who just happened upon FFH today. It doesn’t have to start at a 25% weight. Let’s say 5% for arguments sake.

-

I post a lot explaining the short term moves because that’s what I got paid to do when I was at UBS. I figure I might as well share it to get feedback and appreciate other perspectives. I don’t trade my position and have only added to FFH on pullbacks usually after I understand why it’s pulling back. The last four years all of the pullbacks have had nothing to do with intrinsic value shrinking, this pullback being no exception. Parsad, it sounds like you wouldn’t start a position now if you didn’t have one already. Is that fair?

-

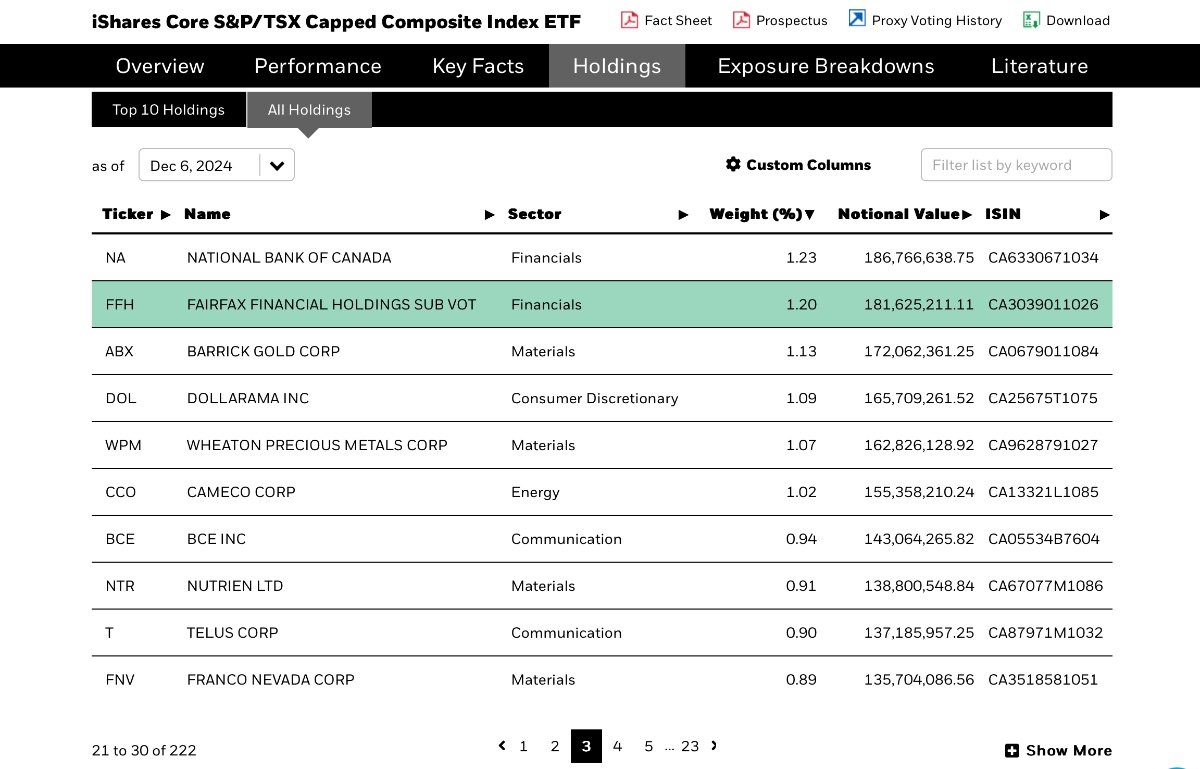

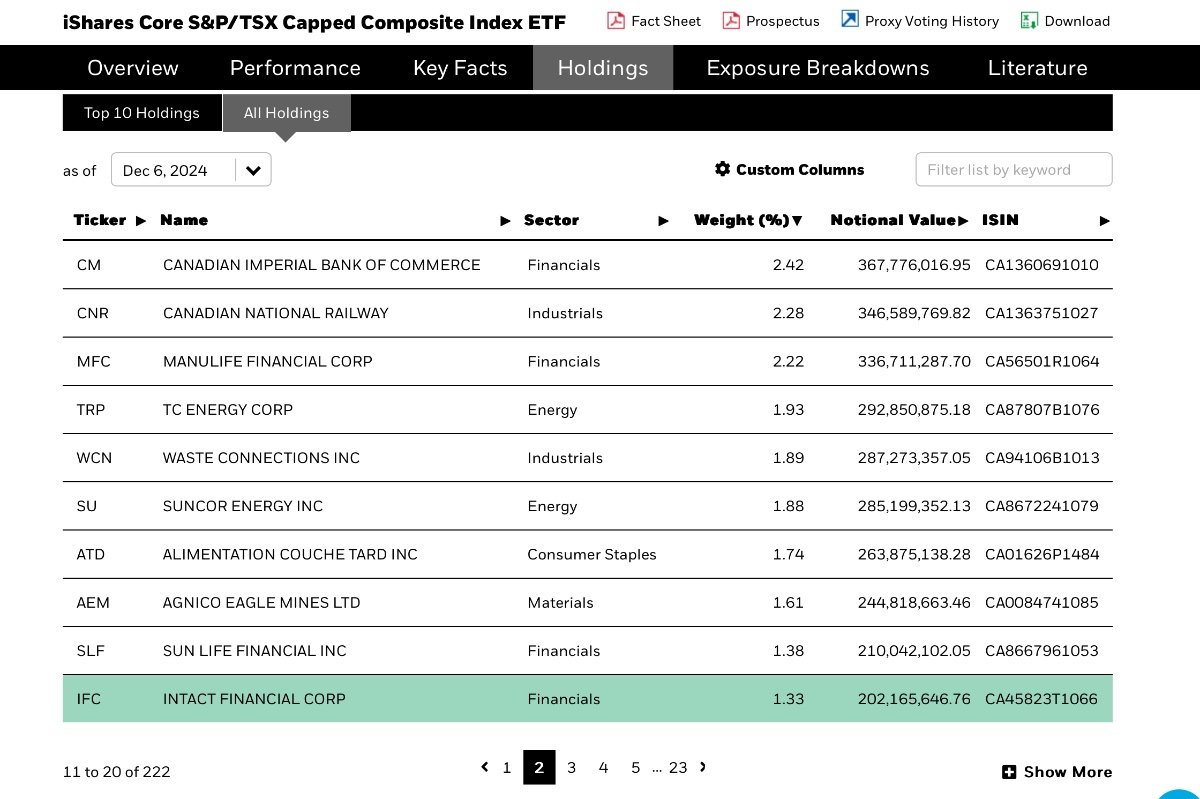

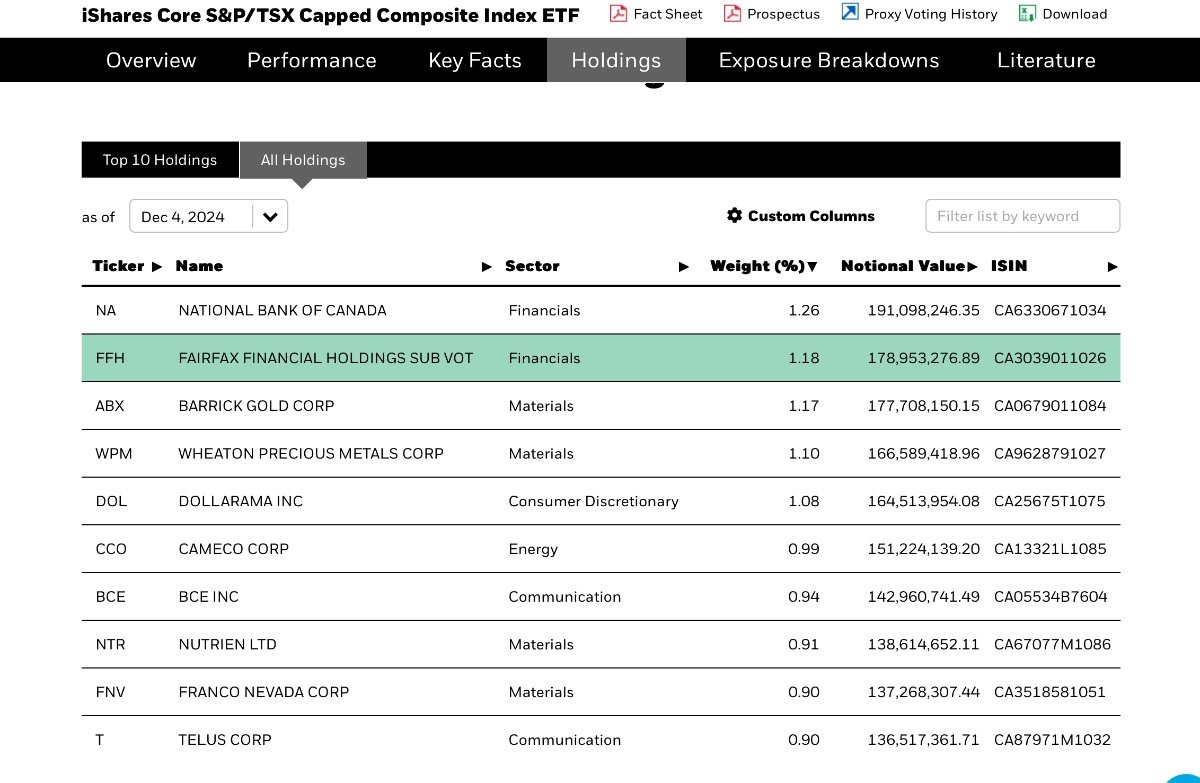

I think the focus should be on float cap, not market cap. On that basis, FFH is 22nd as of Friday’s close. I think FFH has a shot of passing IFC in the next 6 months, which is another catalyst as it’s really going to make every fund overweight IFC reconsider staying underweight FFH. I think the index committee was worried FFH was gamed after they tipped off the brokers that size matters more than sector representation on Sept 25. Deferring a quarter solves for any potential gaming and perception of preferential treatment for some of their biggest customers i.e. the brokers.

-

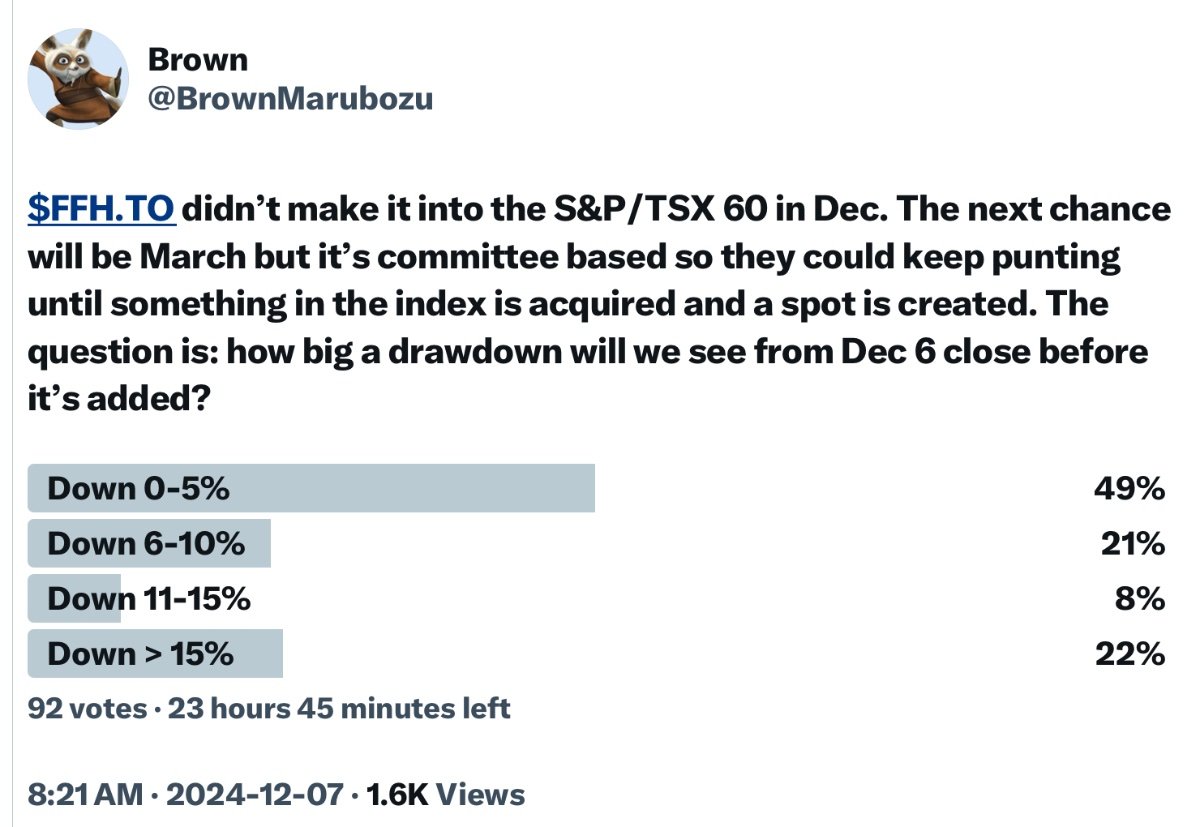

Just asking what the maximum drawdown will be between Friday’s close and if it’s added in March. I expect it to be higher by then as well, perhaps even by the end of this week. However, if an active investor was still looking to add it may be interesting information for how aggressive they should be if the opportunity presents itself.

-

Running a poll over on Twitter and so far it’s about half expecting a drawdown below 5%. If there are funds accumulating, the index committee did them a big favour by deferring. Presumably, FFH is live to be added every index review going forward (March is next) or if any companies are acquired in the 60.

-

They had some available at the AGM last year. I wish there was a PDF copy. I think it would be popular.

-

Thanks. I have heard Jake Taylor mention it a couple of times on Value After Hours in passing. I started posting on Reddit about it as BrownMarubozu as well so that might be me.

-

Which podcasts are you referring to? I would like to listen if I haven't come across them already. I'm in the FFH echo chamber so I don't think I have a good gauge of where Fairfax sits in the zeitgeist. Most investors I bring it up with bring up Blackberry pretty quickly.

-

We wait until March for the next opportunity or if something in the 60 gets acquired before then it will open up a spot.

-

Usually 5:15pm but as late as 5:39pm, the last few years.

-

I think the only size that matters is the float cap given it drives the index activity. In that case, FFH, is now 22nd biggest weight in XIC.TO.

-

Presumably Siemens wants to turn that capital over to generate sales from building and supporting new infrastructure. The returns on that are conceivably much higher than hanging onto a BIAL stake plus management probably has goals on recycling that capital so there may be other incentives. I think it’s fair to say FIH got a bargain given everything we know.

-

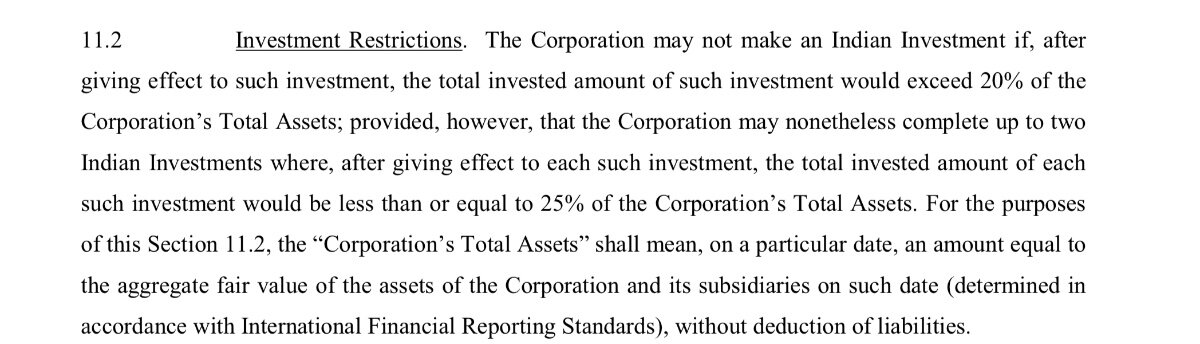

Maybe because of the concentration? Bylaws are here: https://www.fairfaxindia.ca/wp-content/uploads/Corporate-By-laws.pdf

-

The index buys a fixed percentage of the float for all companies in the benchmark so I don’t think it’s technically true that they buy more as the weight goes up. It’s certainly worth more but they only buy more shares if money is flowing into the benchmarks (which it usually is). Fairfax does benefit from having a lower than average dividend yield especially if it gets in the 60. XIC yields 2.5% and XIU yields 2.8% and FFH only yields 1%. When dividends are paid out, the buying is spread out over the entire benchmark proportionately favouring below average yields. Another source of buying that does in theory increase as the weight goes up is from active managers trying to compete with the benchmark. I don’t have good data on this but I think FFH is still under owned by significant pension funds, brokers (RBC, BMO etc..) and the large bank-owned money managers. After 4 years of crushing the XIC, if FFH gets added to their actual benchmark XIU, they might finally decide to get to market weight to avoid underperforming.

-

Each situation is idiosyncratic so I wouldn’t trade off of that conclusion but I’m sure some will. That being said, IFC was at ~1.8x P/B when it went in 2.75 years ago and it’s at ~3x now. If FFH can add 1.2x multiple points in 2.75 years, that would be very welcome. Ultimately however it’s up to shareholders just like us to decide when to provide supply.

-

As a long term holder that wants to see maximum multiple expansion, l’m hoping it’s long term Canadian funds that don’t own Fairfax but are buying it because it’s about to go in their benchmark and it’s too risky to be underweight.

-

True for all of us if we are lucky enough.

-

Annoucement, if there is one, will be on Dec 6 at around 5pm. Dec 20 is also options and futures expiry so volume is normally quite high. They pick the third Friday of the month for a reason.

-

Does everyone have a different definition of intrinsic value? I think about it as the price I can earn a 10% return forever. I’m not sure what that is for Fairfax but it certainly is a lot higher than where it’s trading. I try to estimate fair value with various measure which I think of as an intrinsic value range. The simplest for FFH is BV + Insurance Float but also 15x FTM EPS or 2.5x BV all seem like reasonable fair value estimates. I’m also happy to keep the discussion here.