SafetyinNumbers

-

Posts

2,824 -

Joined

-

Last visited

-

Days Won

38

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

FFH has been putting its excess capital into share buybacks so it’s been shrinking and trades a lot cheaper than BRK did in 1995.

-

No ELF would have been a drag. I never owned it in the TFSA. Part of why the TFSA has done much better than my unregistered accounts. In terms of profits contribution FFH ~30%, MKO ~20%, FISH ~10%. The rest was pretty spread out and nothing over 5%.

-

I’m assuming a lot - they build Guyana and expand Nicaragua by 2028. Run.rate would be about ~180k oz at $1800-2000 margins potentially. I think it’s naive to think there won’t be more deals before then though. If those are accretive then it could be much better than that. It’s a bet on execution and commodity prices to a much lesser extent that seems very mispriced. My core Mako position is about 10% of my net assets. I don’t recommend anyone own any let alone that much but I like the risk reward and can afford to make mistakes.

-

My guess would be equity accounted. Did the financials just come out? If so, maybe we see that reported in Q2.

-

Your blue sky is about 3x 2028 OpCF all else being equal and assuming they don’t do any acquisitions or expand Nicaragua by then. By then it should be more liquid, in the GDXJ and listed in the US. That should result in multiple expansion instead of contraction but we’ll see.

-

I think the NAV of Eagle Mountain is up to $1.2b at these gold prices from $290m at $1850 gold when they bought it. The shares they issued are worth $50m now. At this level of cash flow it seems unlikely they will need to raise equity. They can borrow at the corporate level or at the project level to fill in the gap if needed.

-

H/t to @nwoodman for posting this article by Adam Waterous on the Strathcona Resources board https://macleans.ca/economy/want-to-bulletproof-the-economy-build-more-pipelines/

-

Probably something to do with month end. That being said, it’s a good strategy to get a stock up.

-

They are going to make more mistakes.

-

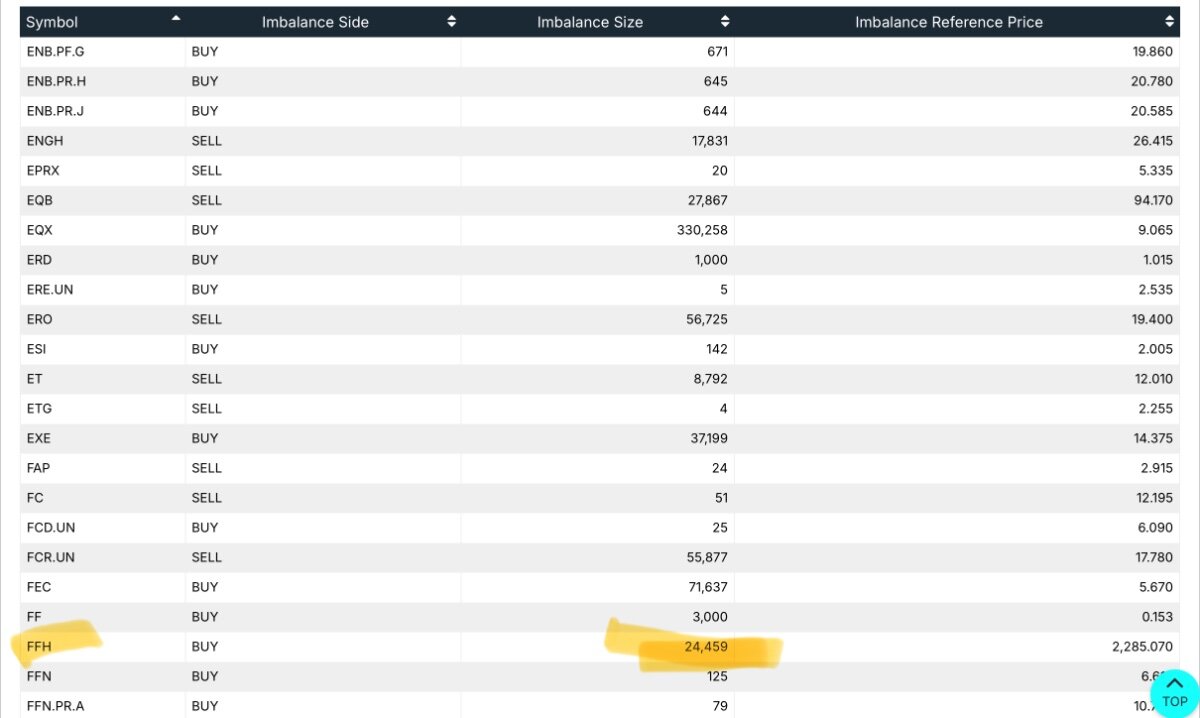

Big MOC buy

-

Thanks for posting. I continue to spread the gospel of Fairfax Gift link if anyone is interested: https://www.theglobeandmail.com/gift/b04eb1bcd666173196423362ad31a8785d529ba1ad1cee14b25891c6ca2ccfbf/G3PN2B5YXJDDHEOB4QK4JLQX7Q/

-

BRK is an interesting comp because the model is the same but it had a lot less float to equity back then than FFH has now. BRK returns came mostly because Buffett picked stocks so well. If FFH picks stocks that well, the returns could be much better. Like you pointed out Viking, one of the benefits is not having to pay up for the potential while BRK was well above 2x BV back then.

-

I had the chance to sit next to Nav at a dinner recently and was thoroughly impressed. I also went on the Fairfax trip to India with Gopal and felt the same way. I don’t think I have met anyone at Fairfax that hasn’t been impressive to be honest.

-

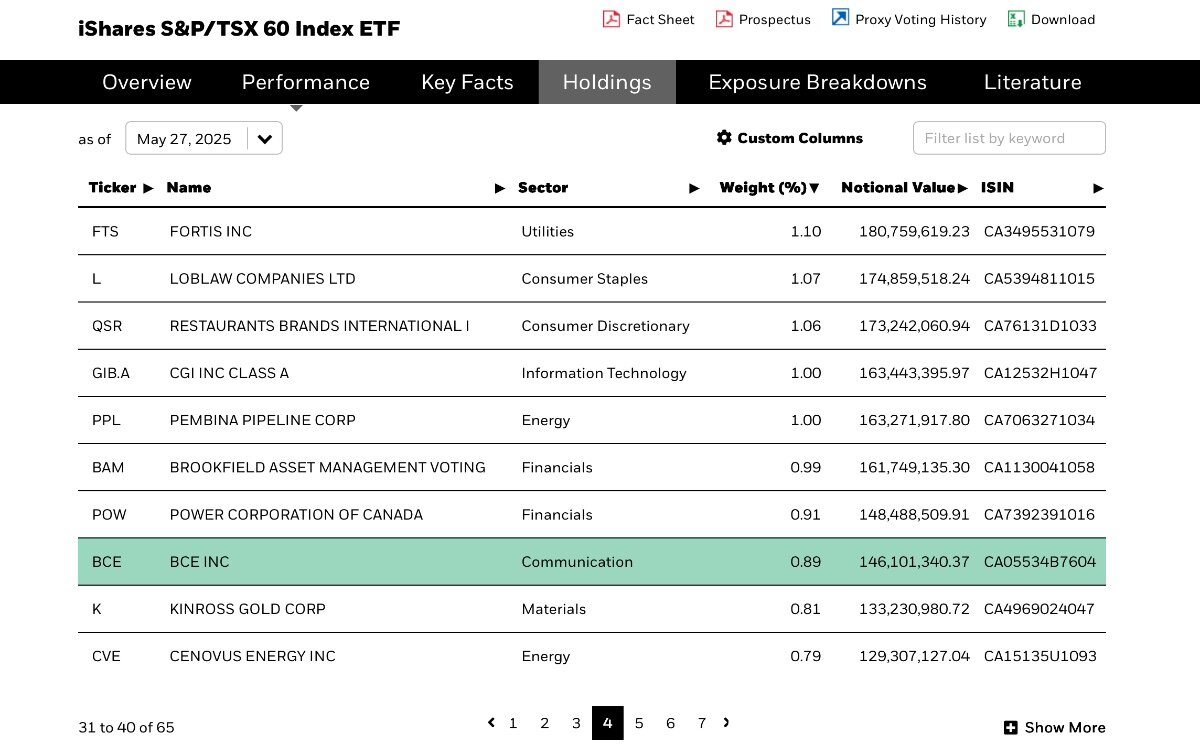

Just a few indices like the 60 b/c ifs Canada’s contribution to the S&P Global 1200 which also has an index committee. The Canadians are unsurprisingly more conservative on changes. It’s also a rare period with no major acquisitions announced of the 60 for some time. For example, with FFH holding SCR, they qualify for the S&P/TSX Composite as soon as they have the float cap and liquidity. No committee opines.

-

Loblaw is Canada’s better run Kroger and CVS all wrapped into one.

-

The index committee will only remove something if it becomes so small that it doesn’t move the index much or if forced to because something is acquired. That’s why the focus is on AQN being removed as its ~20bp which has historically been a rule of thumb as too small.

-

Announcement after the close on June 6. Rebalance date June 20 at the close.

-

basically what if is. Just long instead of short.

-

Thanks for the hat tip Viking but you did all the work! A really great note as usual! I haven’t asked Prem but I think he bought those shares on margin given the size of the trade. To get all of his outlay back and keep a bunch of “free” shares is another masterful move but on a personal finance level in this case!

-

I’m less confident than I have been on the last three reviews so probably? AQN has been hanging around 20bp the whole time and S&P made a change to allow RBA to qualify so there is more competition.

-

CIBC index analyst also highlighting today FFH is their top pick for the 60 if the index committee decides to delete AQN. That might be helping too. Each time the index arbs decide to play, they find there are less shares available to buy.

-

Thanks for sharing @MMM20. The P/E and P/B don’t adjust for FX so it makes the multiple look higher than they are but still screens cheap. @mananainvesting also pointed out to me that they expect share issuance every year which seems unlikely as they tend to buyback enough to offset the vesting of stock awards with buybacks for treasury. That being said, it seems like being added to Valueline helps BRK shareholders switch some of their holdings over which may be helping with recent momentum.

-

How does it look?

-

Great podcast episode recommendation thread

SafetyinNumbers replied to Liberty's topic in General Discussion

Thanks! I did listen to it when it came out. -

What’s Allied World worth now? 15x 2024 earnings is 12.75b. I assume it’s paid a lot of dividends too.