SafetyinNumbers

-

Posts

1,570 -

Joined

-

Last visited

-

Days Won

5

Content Type

Profiles

Forums

Events

Everything posted by SafetyinNumbers

-

Bloomberg is reporting Stelco is considering a bid for US Steel. I assume the partner is not Fairfax but perhaps an international steel company. Others might assume otherwise and sell their shares in fear of a drawdown. I assume if they go ahead, it’s because it’s very accretive. https://financialpost.com/pmn/business-pmn/canadas-stelco-holdings-is-said-to-weigh-bid-for-us-steel

-

I assume that journalists were going to break the story anyway and after what happened with Chinese election interference, I’m not sure they had much choice but to disclose it. The companies that are applying for approvals are Indian so it might be a stretch to assume it’s going to slow approvals. They were pretty darn slow to begin with.

-

I think that’s the right way to interpret the data but I’m not an insurance expert. Using stock at 1.3x book value to get scale in insurance is part of the Singleton playbook that investors generally don’t focus on but it’s part of why the stock got so depressed (a lot more shares for investors to absorb) and why the opportunity is so good now.

-

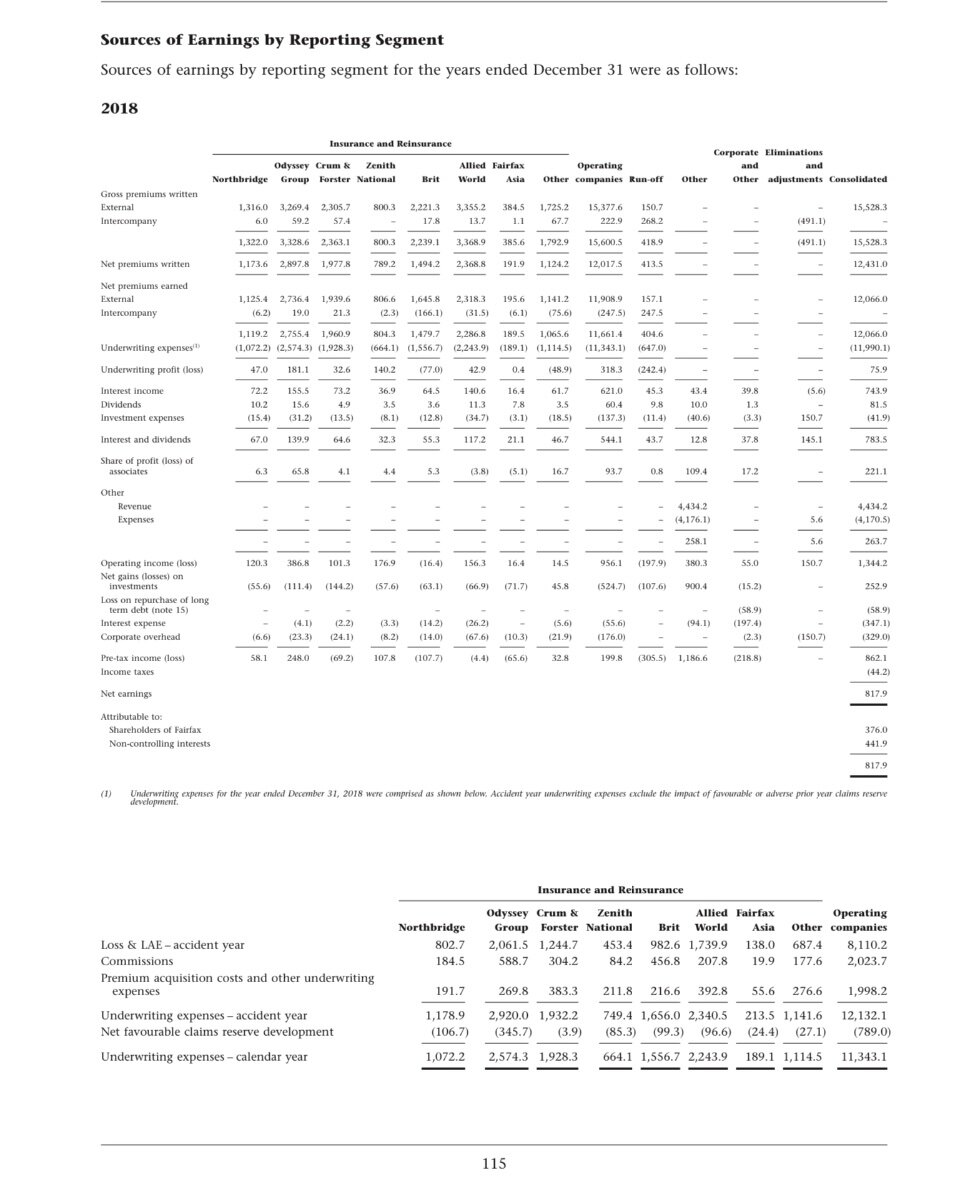

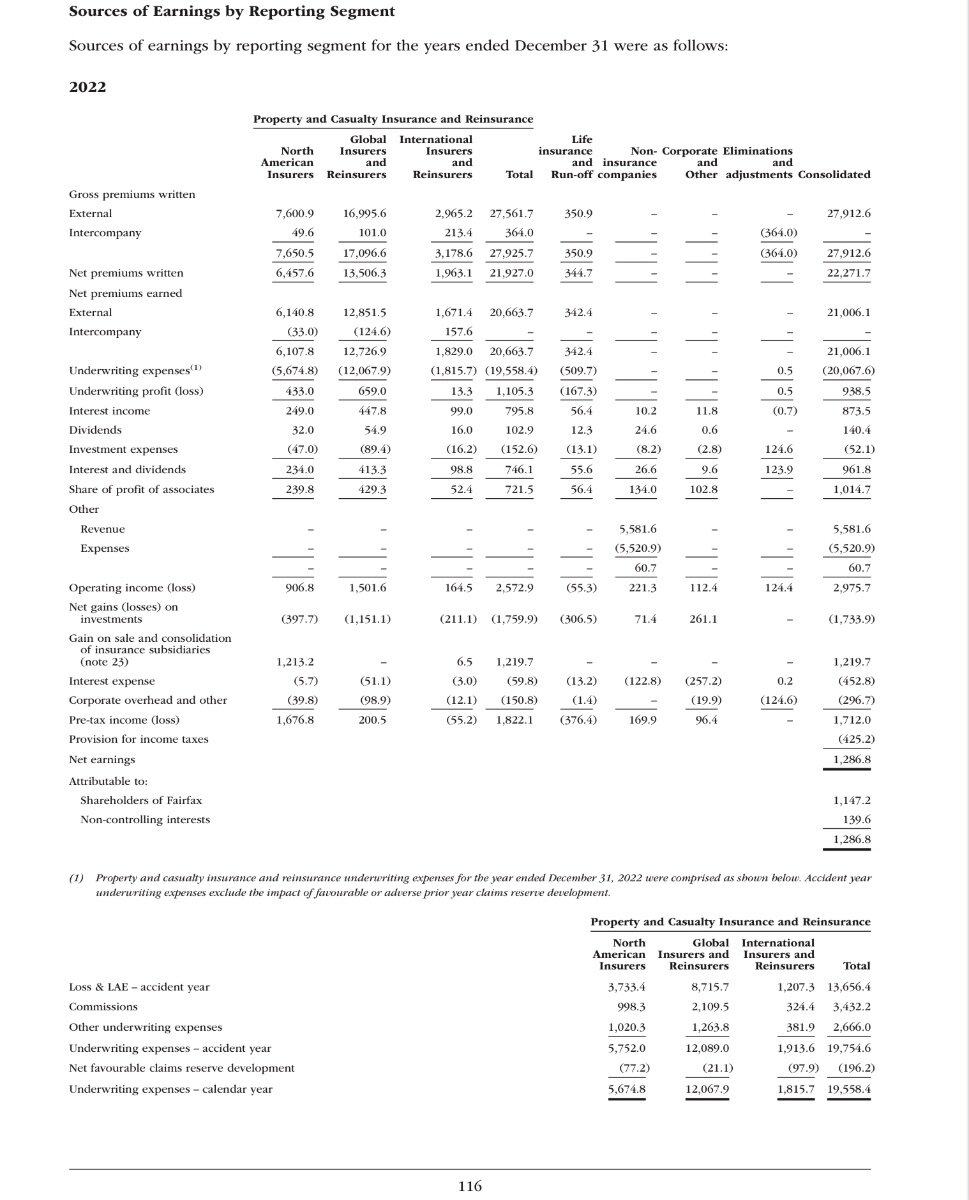

In 2018 ~$2b in other underwriting expenses vs ~$12b in net premiums. In 2022 ~$2.7b in other underwriting expenses vs ~$21b in net premiums. Not sure how that compares to others but it’s a material improvement in the expense ratio.

-

Has anyone done analysis on the administrative expense of underwriting i.e. the part of the combined ratio that does not include claims paid? It seems like Fairfax insurance businesses have grown so much recently that should result in scale advantages which all else being equal makes the combined ratio structurally lower. A point or two really matters.

-

Ultimately, it doesn’t really matter if we think it’s under or overvalued. Current supply is probably from those that think it’s fairly valued. Most of those likely sold earlier in hurricane season (why not if it’s fairly priced in their opinion) and perhaps that explains why volumes have diminished recently. Active buyers might wait until we are through hurricane season before becoming more aggressive and I think they will be accompanied by index huggers who buy on VWAP (that buying never stopped). There seems to be relatively high certainty despite the consensus estimates that book value is going to be at least 50% higher in 3-5 years and as long as the stock tracks book that means the weighting in the index will be going up all else being equal. It’s at 87bps now and based on the near term earnings, it seems likely the stock will be through 100bps soon. At that point, it will be much harder for the PMs that “hate Prem” to not take another look. It’s a much easier decision to buy than chasing CSU as a value manager in 2018 when it crossed 100bps but now that everyone is a quality growth manager they will have to find a way to forget the past and buy FFH based on its quality growth. Analysts will get bolder with their estimates and will start to model in growth in earnings. Instead of declining ROEs, they might model a steady 15% which they know will be wrong but shows growth year over year based on compounding. That will bring quant investors in droves which will invite every other active investor left to take a look. My concern is selling too early in this process. Momentum is more pronounced than it’s ever been given the popularity of passive and quants. Things could get out of hand and I’m here for it.

-

I’m wondering how much the discount can close in the 3 months before the VWAP period begins! Might still take an SIB to make a meaningful difference.

-

Ben Watsa went on BNN on Friday and while he wouldn’t give a stock pick he discussed how many airplanes India has now and where it’s going based on existing orders. It doesn’t take a lot to connect the dots that BIAL is a net beneficiary of the network effect of going from 700 planes in the country for domestic travel to multiples of that over time. He’s also tweeting @benwatsa Perhaps it’s just a coincidence that the performance fee is due at year end and closing the discount prior to that would help make it less dilutive to FIH shareholders but I doubt it. Maybe management would prefer not to have to use liquidity for buybacks as they see investment opportunities. It will be interesting if Canadians get the message and buy FIH.U while it’s on sale. https://www.bnnbloomberg.ca/video/you-can-compound-at-a-good-rate-by-investing-in-india-fund-manager~2767937

-

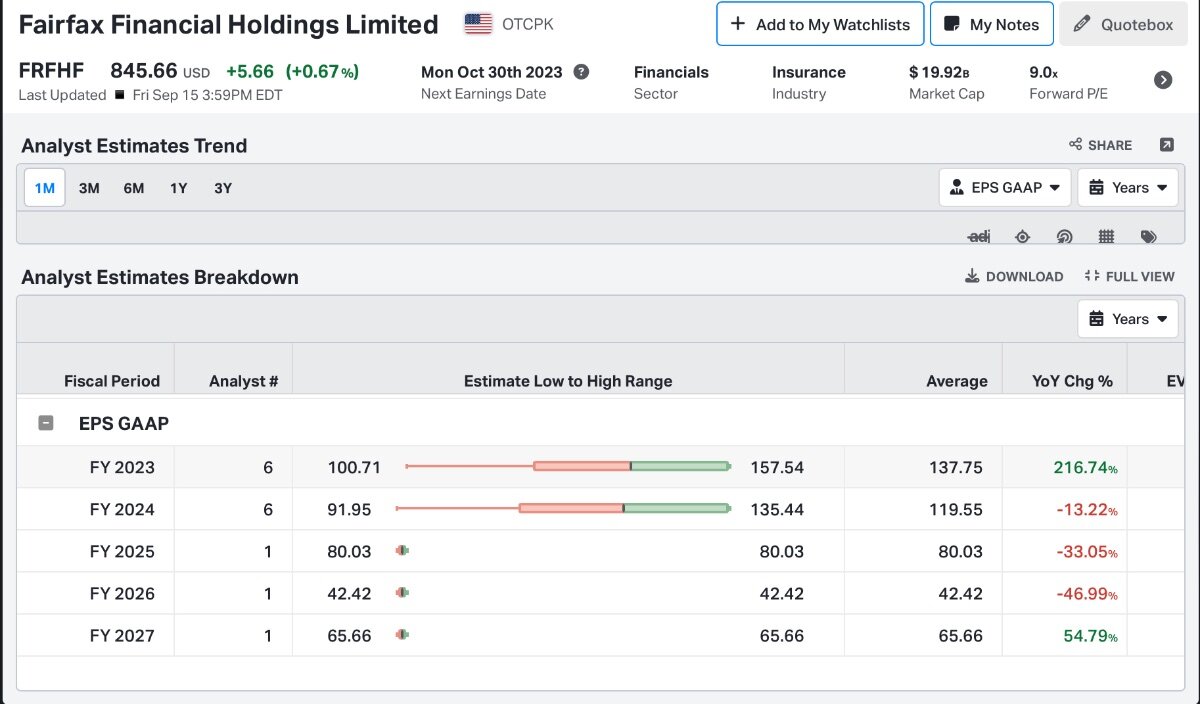

The source of the analyst estimates is Koyfin.

-

Just a reminder that consensus is much lower and if you are wondering which analyst has the low estimate for the next 5 years (only for the last three), it’s our friend at Morningstar. The declining earnings estimates (and historical volatility in earnings) basically makes it unownable for quants and for active institutional investors who use the same screens as quants in order to compete with them.

-

I think his task as future Chairman will be to maintain Fairfax’s culture and having grown up in it, he’s probably best suited to do so. Hopefully Prem still has a long tenure and it’s not a role, Ben, will have to takeover any time soon giving him that much more experience when he does.

-

Lauren Templeton just dropped a new podcast featuring Ben Watsa https://podcasts.apple.com/ca/podcast/investing-the-templeton-way/id1604395168?i=1000627607421 It’s a terrific listen for long term Fairfax and Fairfax India shareholders. He makes a very good case why India is a tremendous investment opportunity and provides comfort that Fairfax will have controlling shareholders that keeps the culture that his father has fostered.

-

Mr. Market can embarrass the best. If it was just FIH.U that had a big discount, I can understand being frustrated with the BOD but it’s across the board. Look at E-L Financial, they bought back over 40% of the float, paid two special dividends and increased the regular dividend by 300%. Its discount has grown from ~45% to over 50% in the past 3 years. Their portfolio is even more liquid than Fairfax India as it’s ~80% liquid stocks. There are numerous examples. Please share if you have them. Seems like a good way to find cheap businesses to buy but not necessarily great stocks in the short term. The only way the discount financially matters is with the performance fee. It’s why I think an SIB is likely before year end and potentially next week based on the June 15, 2021 tender announcement. But they could wait until later in the year so the VWAP has a better chance of being at or near the tender price. At the very least it negates the impact of the performance fee dilution but more importantly for the share price it removes another big chunk of float. Also, given all of the private marks, to complain about the book value growth is to argue for more aggressive marks and higher performance fees sooner. Sure that would help performance (or make the discount bigger) but it’s not in the best interests of long term holders. It is, however, potentially in the best interest of short term holders.

-

They are definitely not priced as low but arguably cheaper based on the outlook. Durability is arguably up a lot too which reduces risk and allows for a higher multiple. I’m not saying I can win these arguments.

-

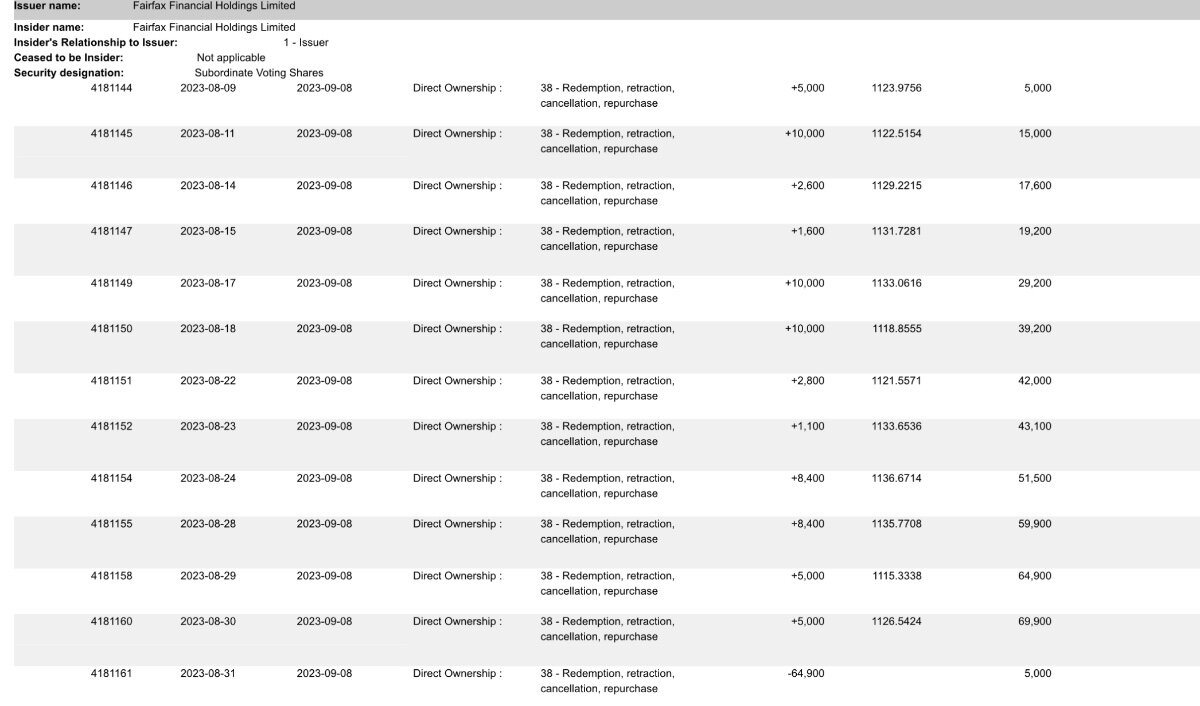

Fairfax buybacks in August

-

I think your thesis on why the discount grew is actually just a narrative that masks the technical change in markets as so much money has flooded to passive, quant and crypto/meme. Anything liquid has bounced back post Covid, airport stocks have high valuations and BIAL is doing fine. I don’t mean to discourage ownership but I don’t expect Fairfax to ever take FIH.U private. There is too much optionality in being public for an asset manager and the capital treatment is better inside the insurance companies. I think there are a couple of ways, FIH closes the discount or gets to a premium. First, FFH gets to a big premium and as PMs come up with their reasons for finally buying it at 2x+ P/BV one of them will be because of India exposure so they might add a little FIH on the side. Second, the Anchorage IPO goes well, and it becomes a growth vehicle for FIH in India as it has a much lower cost of capital. NA investors may buy FIH to get exposure to Anchorage but also because FIH could then grow much faster. The next 5 years will be interesting.

-

I did look at your earlier post. I also noted that since June 2011 the CAGR was only 7.56%. I haven’t done the math but seems like the performance was so terrible between June 2011 to July 2013 that it pulled returns down by over 600bps for the full 12 year period from the 10-yr number you cited. Maybe that’s why they only manage $35m in the strategy despite India’s recent popularity. The discount only started 5 years ago and since then the company has bought back over 15m shares at a discount. Way more than they have issued in performance fees so it doesn’t hurt as bad as you make it seem. They are doing their part to close the discount. The problem is the world changed and investors switched to passive and quant strategies both of which want nothing to do with Fairfax India which isn’t in any benchmark and doesn’t screen well. The hurdle rate for active investors went up considerably and many investors (perhaps like yourself) think markets are efficient. They tend to analyze growth in price instead of intrinsic value so a security price that goes sideways while IV goes up is bad instead of an opportunity which just helps reinforce the discount. The group that really let us down so far are the original shareholders (OMERS, Markel etc…) that negotiated the original terms. They are supposed to close the discount every three years in front of the performance fee by buying stock and unfortunately they have abdicated their responsibilities it seems although they still have 2.5 months left. I continue to think we’ll see an SIB or a large buyback before year end which will offset the performance fee and shrink the float, giving us a chance to close the discount but it takes active investors to actually close it. As for the Anchorage IPO, the value has only gone up while waiting to list it which I assume has been held up by regulatory delay. Whatever the reason, the opportunity that has been created is what’s important going forward (to me at least).

-

It would be interesting to know how much float there was too. Berkshire bought Alleghany float for free and Brookfield has been buying up cheap float too.

-

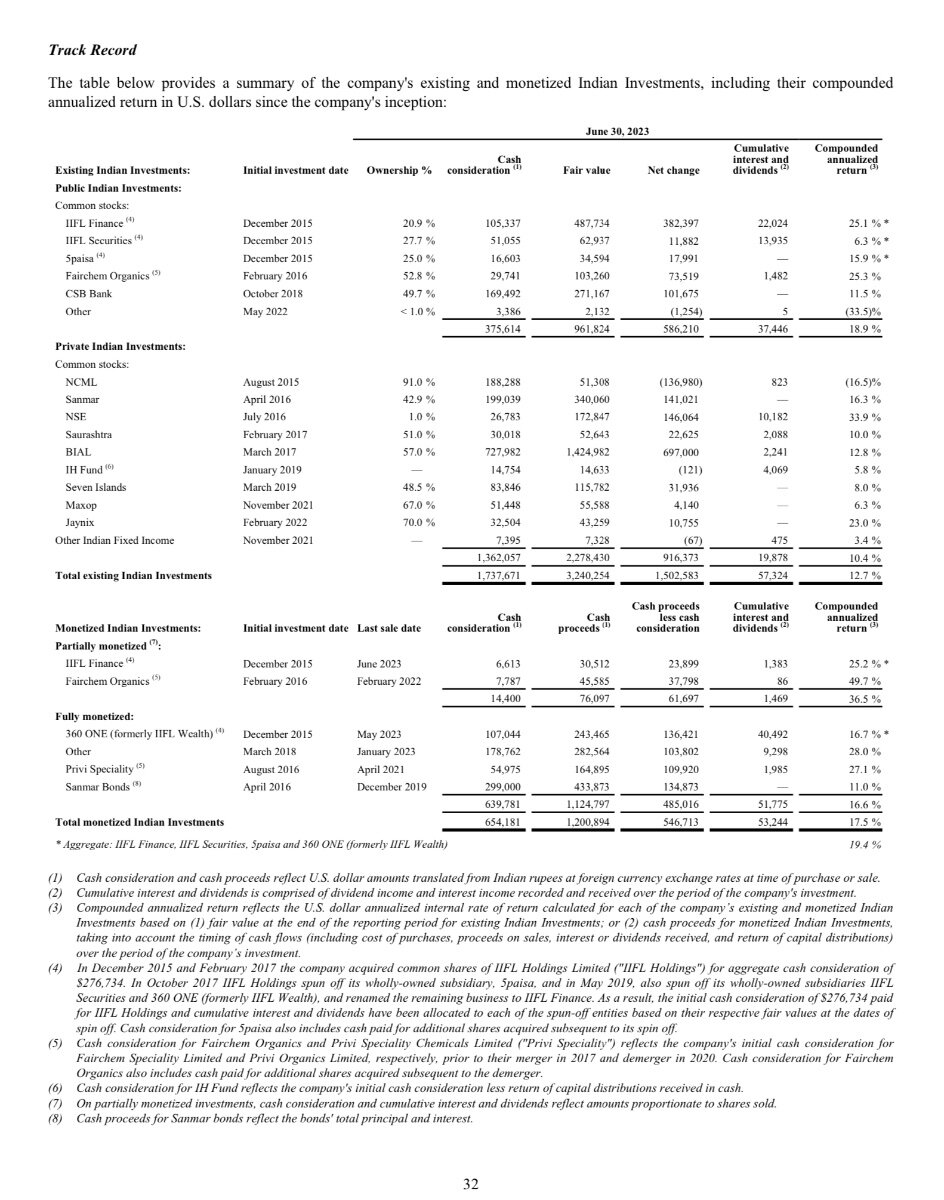

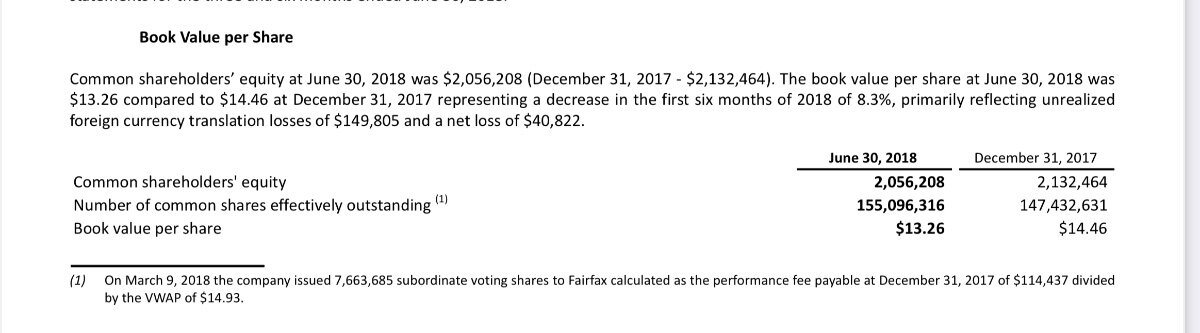

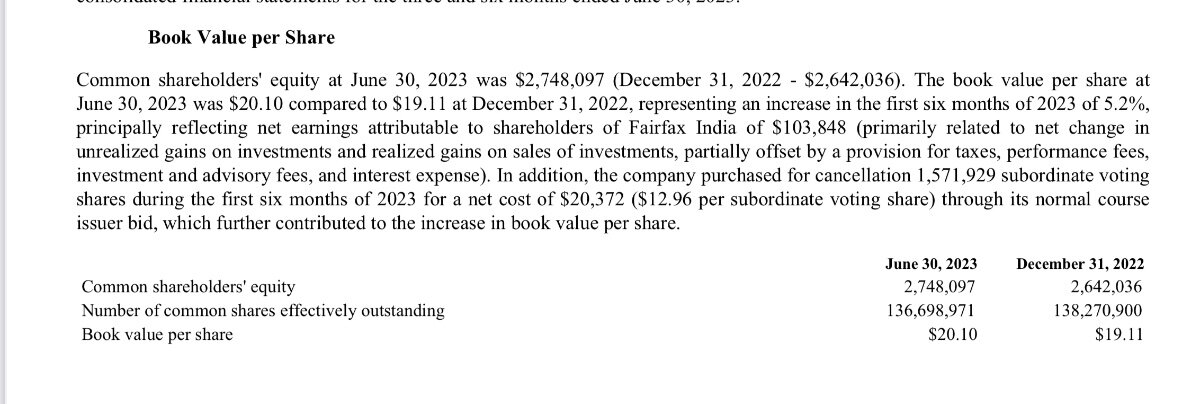

They are playing a different game but comparing prices for a fund that trades at NAV to one that doesn’t and using that to analyze management performance doesn’t make a lot of sense to me. BIAL is a big chunk of returns but actually has performed below the return on public investments. FIH is playing the public markets game better than Matthews. At June 30, 2018, BVPS was ~$13.26 and with it likely still over $20 now, the returns aren’t that different over the past 5 years. You seem to own it because you think BIAL is marked too low and I think it’s likely that’s true for the rest of private book too. On that basis FIH returns have destroyed Matthews returns and they are doing it with almost 100x more capital.

-

INDA (MSCI India ETF) just hit a new 52-week high today while FIH.U sells off. It’s a great example of nervous active investors which represent the entire shareholder base of FIH (no quants, no passive, not much institutional) trimming while asset allocators keep buying passive exposure to India.

-

That’s great analysis! Thanks for highlighting. Given Fairfax’s 32.2% is marked at US$1.77b, that contributes to ROE at 20%+. It really helps pull ROE higher. The street is for the most part ignoring earnings from the investment portfolio and they will likely keep getting surprised since it’s already too cheap based on the insurance operations alone, there is no need for reasonable expectations on the investment portfolio.

-

And they partially financed it with stock issued around 2.5x book. Trisura also recently issued equity at similar multiples. Smart moves by the management teams. It’s the easiest way to grow book value!

-

For FIH.U, the stock going sideways while intrinsic value grows used to be what investors looked for as an opportunity but now mostly everyone thinks the market is efficient. I don’t think Fairfax let investors down here. They did their job in terms of buybacks and additional purchases by Fairfax as soon as the shares started trading at big discount to BV. With the third performance fee period ending on Dec 31, I think the odds are decent (50-50 at least) we see another SIB before year end which would effectively pre-fund the performance fee and shrink the float. The group that let us down are the original institutional shareholders who negotiated the fee structure on our behalf. OMERS, Fidelity and Markel (I think) were presumably supposed to close the discount every three years so that shareholders wouldn’t risk dilution on paying the performance fee and so far they haven’t shown up (and I don’t expect them to).

-

It’s the same security whether held in Canada or the US so there are no ADR fees and no economic difference. I know for Canadians, we can get margin on the CAD ticker but not the pink sheet.

-

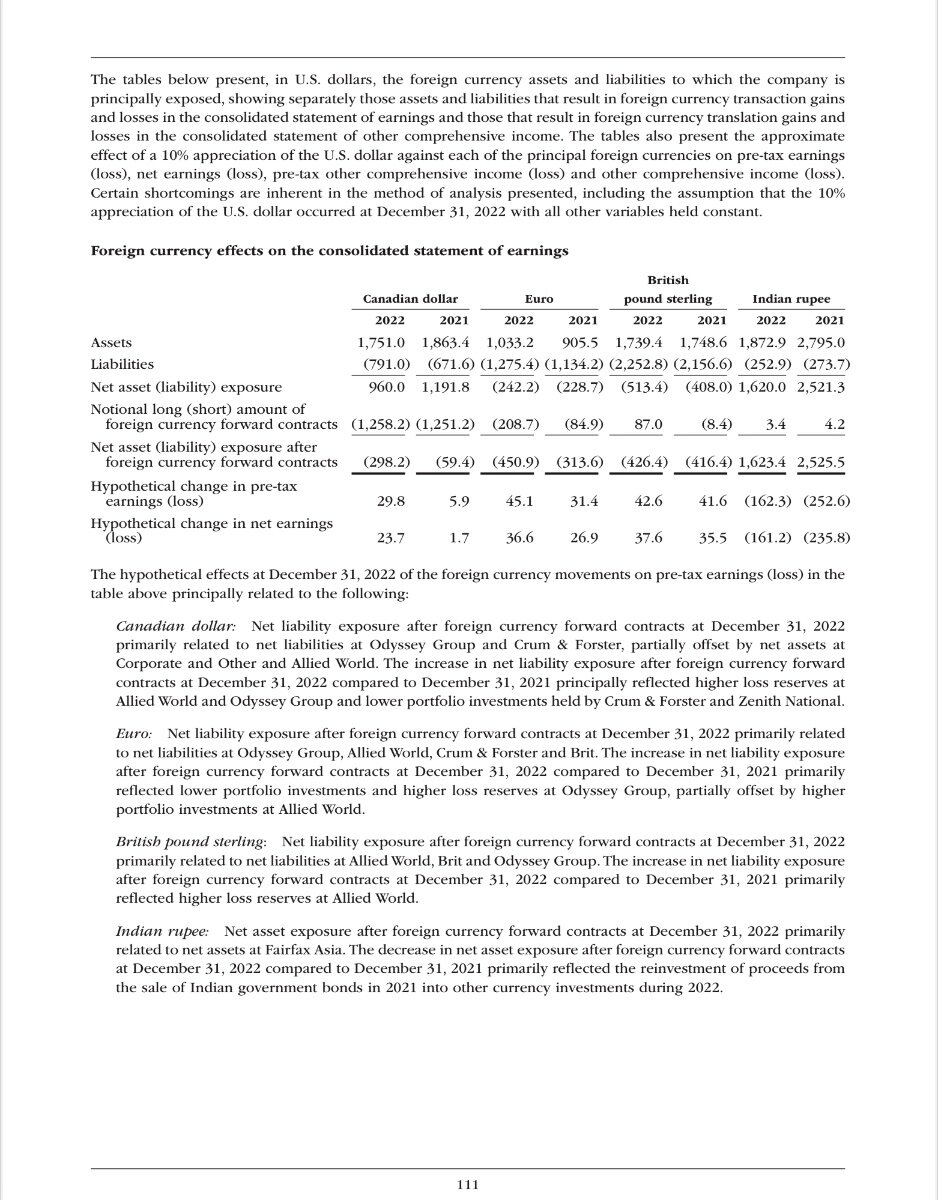

I doubt they explicitly currency hedge but there are a lot of natural hedges. This is the sensitivity analysis they provided in the 2022 AR. It must be a constantly moving target. Is currency exposure something that concerns you?