Spekulatius

-

Posts

19,051 -

Joined

-

Last visited

-

Days Won

39

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

Anyone tried Turbotaxing the sequence? Turbotax is the ultimate tax authority. LOL. With many brokers (Wells Fargo, Fidelity) , you can sell specific lots. It is some what hidden in Fidelity, but the functionality is there. I think IBKR has this functionality too, although i have never found or used it in the mobile app (which is what I am using).

-

I actually think that energy is going through the same COVID-19 whiplash like other commodities and this has very little to do with ESG. ESG isn't helping but it has little impact on crude supplies, imo. We will see a rapid rise, followed by a rapid fall, imo.

-

Marketwatch is the new Dear Abby column for financial advice. Entertaining, but mostly a waste of time.

-

Simulate the transaction sequence in Turbotax and if you get a the right result, you should be good to go. That would be my poor mans legal opinion.

-

@lnofeisone thanks for sharing. To me, your method makes sense. The end result is the same than a wash sale, but the IRS tax code has build in a path dependence (via effectively selling a covered call) which is exploited to materialize a tax loss. Is there any timeline in which steps 2-4 need to occur? Can you just execute those the same day?

-

Adding a bit to $FISV here below $106.

-

This is true for so many self help gurus - they are utter frauds in a sense that they live their own life much different than what they teach. What they teach makes sense and often isn’t really that complicated. But living it consistently is an entirely different matter, which typically the self help gurus don’t follow themselves. Just look at pretty much any Tele evangelical or Robert Kiyosaki of “Rich Dad, Poor dads” fame. The core message of his book can be summarized in 2 pages, the rest is just repetitive and terribly written. So you can get inspiration from the message, but it probably should stop there and you need to find your own path and not follow the mostly fabricated stories and half truth, because often enough what they teach beyond the simple core message is mostly scam..

-

I typically just do a dirty hedge - sell the loss position and buy a similar security or a correlated ETF and hold it for a month, then switch back I to the stock if you still desire.

-

This above article is dated (year 2000) and incorrect. The wash sale rule does apply to IR purchases buy/sells of the same security in taxable/IRA‘s are not deemed unrelated. https://www.investopedia.com/articles/retirement/09/ira-wash-sale-rule.asp Does the Rule Apply to IRAs? In 2008, the IRS issued "Revenue Ruling 2008-5," in which it addressed the question of whether the wash-sale rules apply to IRAs. In the ruling, the IRS explained that when shares are sold in a non-retirement account and substantially identical shares are purchased in an IRA within 30 days, the investor cannot claim tax losses for the sale, and the basis in the individual's IRA is not increased.2

-

Let‘s just say, I have little confidence in my own predictions, but I keep them in mind as far as my portfolio is concerned, as well as dealing with individual positions. I believe that FFH is quite sensitive to the overall health of the economy, so it is important to keep this in mind.

-

In my opinion FFH is trade not a LT hold. It's a volatile stock and currently more things go right then wrong for the business and in addition it's cheap. That makes it a good trade. We will see how it goes, but as soon as the economic outlook dims, I expect a lot of the business that FFH owns to shit the bed, so to speak. I hope they sell some to bolster FFH's balance sheet. I am not uber bullish on the economy like many here. I would not be surprised if we get a slight 2015/16 style recession in 2022 - a result of the COVID-19 stimmy hangover. You don't want to hold FFH in that environment, I think.

-

The direct savings by not listing on the NYSE are immaterial. However, a lot of companies hate the disclose, the pesky SEC, having to file insider trades given FFH byzantine structure, Sarbanes-Oxley etc. I don't think they would enjoy the SEC poking around. Just may guess of course and FFH isn't the the first foreign company to abandon an NYSE listing for this reason. I don't think it's that big of deal, but it does make FFH less investable for some.

-

I am pretty sure FFH doesn't list in US exchanges due to the onerous SEC requirements.

-

The mistake wasn’t to make John Chen CEO, the mistake was to get involved with BB in the first place, since it was a tech company that was dying and it is common knowledge that tech turnaround are hard. Furthermore, FFH really doesn’t have domain expertise. FFH has a tendency to chew off more than they can handle. I am not sure they learned much in this regard. Just recently, they invested 100CAD in a mining venture. Do they really have expertise here? Maybe they do, I have no idea. Other than stopping shorting, ( which is significant) I am not convinced they have learned really anything. What they really should do is that management defines a circle of competence in a way that makes sense and can be easily communicated. This should come with a promise that future investment lie within this circle of competence and that current investment outside will be liquidated in time. Somewhere upstream it was mentioned that FFH IR isn’t good. While this is correct, the underlying reason is that there isn‘t really a great strategy to being with. If there is any, it would be 1) We are an insurance holding 2) we buy pretty much anything as long as it looks cheap to us. The problem with above is that it is not a great story, especially with thr mixed track record the last ten years. It seems about half the time, they don’t really know what they are buying and then it often doesn’t turn out to be cheap either. They have got to make some changes at the top and with their strategy and this is not just an IR problem.

-

-

Mr Market is a like drunk, going forward and backwards and not getting anywhere. Typically not a good sign at current elevated levels, Imo.

-

I totally agree. This would be watering the weeds and pulling the flowers. I really would like them to liquidate BB, RFP and Stelco, be it outright sales or special dividends from Stelco and RFP. Digit has a lot of potential and they got in at the ground floor due to personal relationships Prem build over the years. That’s an real edge that they should build upon. They don’t have a real edge in commodity plays or BB. As @rkbabang said up thread, the reason they invested in BB (for example) was likely personal connections with BB’s founders as well, not a real insight into the business or other edge. With a turnaround play, that can be a liability while with VC like investment, personal connections can be an edge.

-

This may be an incredible stupid question but after looking a bit in this space (and particularly Boo. L) what is the ESG concern here?

-

Nope havn’t sold. I do trade, but not for < 2% gains, I am thinking more 20%. We also get a dividend in a few month and I want to put that one in my pocket as well. If things go in the right direction, there is potential for much more. The real money generally isn‘t made on rerating alone, it is made on a combination of increasing asset value and rerating.

-

It is great that we found some ancient scrolls telling Prem’s tales of buybacks in his gleeful years: Most of us are more the “what have we done for me lately” kind of fellows. Not much action on thee since 2004.

-

I agree. If FFH would get an family outsider CEO with a good reputation, the stock would move 10% and probably never look back. Sort of like when Occidental Petroleum stock ripped when Armand Hammer broke his rib getting out of the bathtub. https://www.latimes.com/archives/la-xpm-1987-06-18-mn-8023-story.html

-

Sold MRK pre market. I get the oral COVID-19 pill, but is it really a gamechanger? The study looked good, but sample size was small. Interesting enough, in message boards, some claim that Ivermectin works better. I guess soon, we have something for everyone.

-

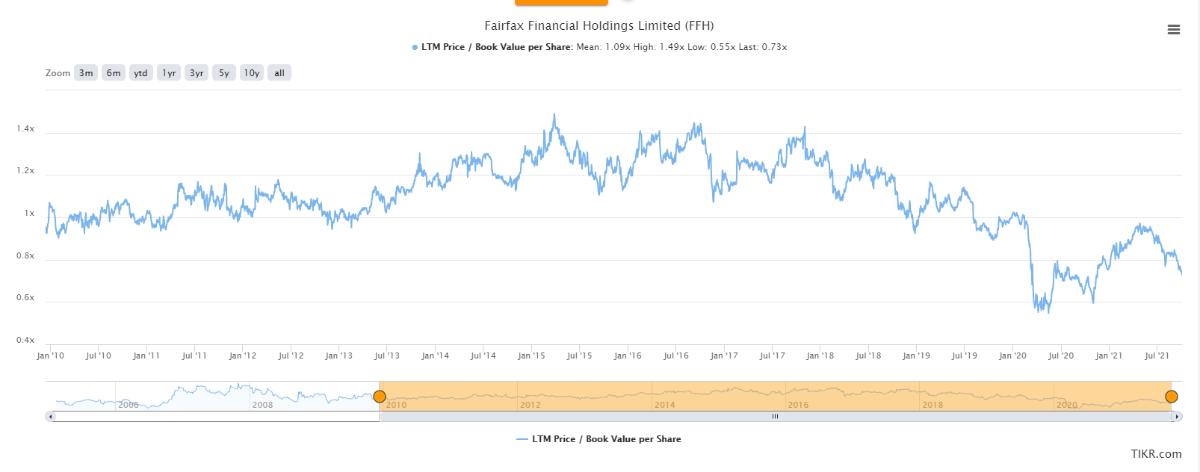

I think it's the troika of 1) mixed execution & track record 2) family control 3) complexity that is keeping the valuation low. Improve any of the three or even 2 or 3 out of the 3 and the valuation will improve, everything else being equal. I think the FFH Morningstar report card gives a good view of the market perception of FFH. There are well managed family controlled conglomerates that trade at a discount to NAV. Exor and even Berkshire come to my mind as well, as some Malone entities come to my mind. ELF also has an issue with lack of liquidity on top of the above. Someone pointed out that FFH did trade at 1.2x book a few years ago in 2018. I checked it out and FFH definitely trades at below pre-COVID-19 multiples. For me, it's a rerating trade. If we get to 1.0x book and book keeps rising at a decent rate, one could see a 40% return from here, plus some dividends.

-

All this seems to imply that offices need to be more WeWork like, since the social aspect and connecting in addition to representation is the only thing really left. Maybe open a bar after 5pm with free beer helps people attract back there. It would certainly work for me. NYC needs to get people back into town otherwise it becomes a ghost town like Dallas Texas downtown back in the day (I haven’t been there since 2005 or thereabouts, so I have not idea what it’s like now).

-

Buffett/Berkshire - general news

Spekulatius replied to fareastwarriors's topic in Berkshire Hathaway

LOL. Does he “pray” to Adam Smith invisible hand every night?