Spekulatius

-

Posts

19,043 -

Joined

-

Last visited

-

Days Won

39

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

How do you get to $100B for $DIS ex DTC? EV is $220B and I don't see DTC worth $120B by a long shot. Furthermore, since DTC is part of the flywheel, you can't segregate parts of it or do a SOP, imo. You have to evaluate DIS as going concern. As for DTC, I expect it to eventually trade for a single digit EBITDA multiple. In the past, these streaming business have traded more based on subscriber growth metrics, but I think at some point this will switch to old fashioned profitability metrics. Reading the transcript, in 2023 their DTC spent will be >$30B. This years DTC revenue was $19.6B so if it increases by 20% that would be $23.5B. that would mean about $6.5B in operating losses next year compared to ~$4B. Maybe revenues grow quicker, but I see almost no way that the DTC losses go down next year compared to 2022. I also think their linear network earnings ($8B operating earnings) will go down compared to this year. Parks likely should be flat due to recessionary trends. This all does not look all that great to me. They made $1.75/share this year in operating earnings for a $87 stock. This can easily hit $60 or below, imo if cord cutting worsens and their DTC subscriber growth is a bit weak. Again, i have no deep insight other than this does not look all that cheap or like a great setup at current prices to me.

-

$DIS problem is the same problem that $WBD and $PARA are having, lack of profitability in their DTC business and shrinking topline with linear networks. The bottom line was actually fine for linear networks. For DTC not so much.

-

LOL, my son know a few fellow high school students who are in the "Socialist club" as well as a self proclaimed communists. I think these kids think it's cool to be a communist. Most of these kids drive nice cars and live a sheltered life. I think they just like being contra conventional wisdom. None of them would last in a true communist society much less enjoy it.

-

The last earnings reports had a lot of focus on FCF and it’s easy to see why- their FCF went almost to zero in 2021 with a huge inventory buildup. As a rule of thumb, when you turn around a business, the first focus is almost always on FCF first and earning a second. This is because it’s game over when a company is running out of cash (and the ability to borrow more) rather than when it shows large losses. Also, reducing inventory will generate cash, but probably make earnings worse due to “under absorption” and probably some discounted liquidations etc. While the plan makes sense in a high level, the current CEO (since June 2022) was coming from a CFO role at SWK and shares some of the blame, imo. The current CFO is interim, which I don’t think is ideal either. Quite a mess and it’s not because the business is in a steep downturn really. The former management screwed up operations and lost control of their supply chain so to speak. other companies in similar business have done much much better than SWK. I think there is some real risk here that shareholders get permanently impaired (dilutive capital raise etc).

-

Doesn't any vaccination increase inflammation markers? I think I have seen the same thing about influence vaccines. Like this study: https://www.ahajournals.org/doi/10.1161/01.ATV.0000248534.30057.b5 I don't know if this is comparable or not but those issues are part of safety studies. Also see above study about mortality of COVID-19 unvaccinated vs vaccinated cohorts for non-COVID-19 causes. Anyways, the vaccine is almost certainly not to blame for excess death here. There are likely other leading causes like deferred medical care, long COVID-19 fatalities, increased drug overdose death at play here.

-

I was in this at higher prices (small position) and sold out for a loss. I do agree with the thesis, but I think they are seeing significant reduction in demand while prior troubles were more self inflicted with supply chain troubles anf also cost inflation out of control. Compare how TTC managed through the cycle so far as a comparison. That said, I am watching SWK closely but I am leery of continued misses that just seem to keep on coming.

-

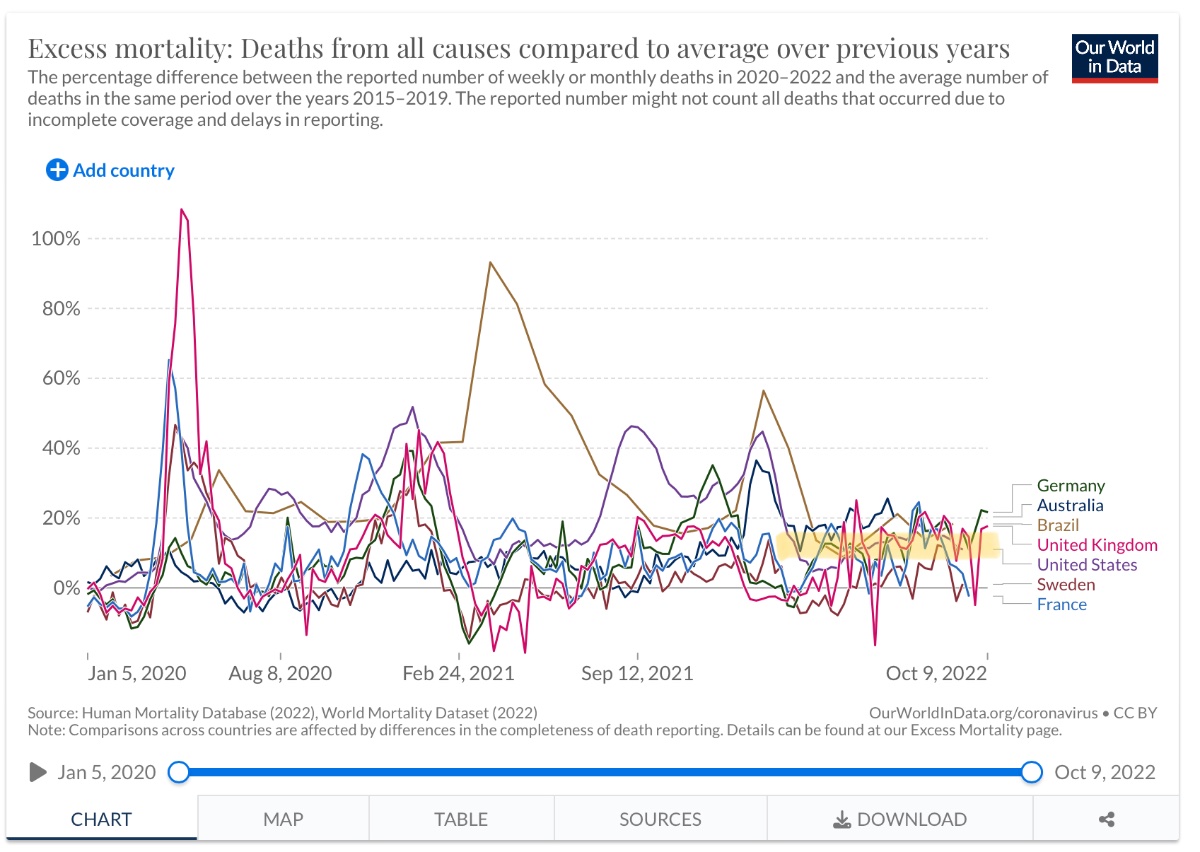

@KJP and @xxx1313 thanks for the additional data. It does seem like the reason for the increased is multi casual. I do feel that an 15% increase in excess death is a big deal, no matter the cause and probably should get more attention than it does currently. With 2.84M death that means that more than 430k people die in the US than statistically predicted. I guess the hope is that it’s transitory? What if we get higher excess death for longer? Unless you operate a funeral business, it’s bad news for everyone. Some life insurers seem to have taken note of this trend as well.

-

Studies have been done on this apparently. I don’t think it’s it’s directly vaccine related. https://www.kp-scalresearch.org/new-study-looking-at-millions-of-vaccinated-and-unvaccinated-people-found-no-increased-risk-of-death-among-covid-19-vaccine-recipients/

-

COVID-19 death don’t explain the increase in mortality, at least does not only most of it. I think the theory that makes more sense is that it‘s fallout from the epidemic. In particular many people did not get or did not seek timely treatment for chronic diseases and now show increased mortality. This one discusses the issue from the UK perspective: However, it’s just a theory right now. I personally have more questions than answers.

-

Putin is a classical example of a Pascal mugger. In exchange for giving him Ukraine, he promises no nuclear war. That‘s the fallacy that many here are subscribing who say we can’t fight him because he has nuclear weapons. Of course, after we would appease him , he still would have his nuclear weapons. https://en.wikipedia.org/wiki/Pascal's_mugging Who would give a Pascal‘s mugger some of his money? I certainly would not.

-

I came about this through a fellow looking at excess death in the UK. However it‘s not just the UK, there are excess death almost everywhere. I picked up a few countries in this website and virtually all of them have excess debt, by about 15% above the excepted run rate. Are this due to LT pandemic effects or is there something else going on! I have no clue and neither seems anyone else. I am surprised that 15% more people dying isn’t news but I think it should be. If it stays it means that the average life expectancy will go down significantly. The excess death seem too every age any age group. This is not meant to be a political post, but I feel it’s important data. https://ourworldindata.org/grapher/excess-mortality-p-scores-average-baseline?country=USA~GBR~DEU~FRA~SWE~BRA~AUS

-

Berkshire vs Brookfield vs Fairfax

Spekulatius replied to CanadianMunger's topic in General Discussion

I think BAM will outperform both unless interest rates go up from here and stay high. The reason is that BAM‘s business model is able to get higher returns on equity. -

Found this one on Reddit. Some presentations from a Greek value investing conference. Looks like some interesting stuff there: https://greekvalueinvestingcentre.com/index.php/ben-graham-centres-2nd-european-value-investing-conference/

-

I have no idea. The outgoing CEO was definitely lousy but Adidas has structural problems and Yeezy business going away and there are no easy solutions for both.

-

Berkshire vs Brookfield vs Fairfax

Spekulatius replied to CanadianMunger's topic in General Discussion

@RedLion I think private equity will always adapt to higher interest rates, but it will not be a pleasant journey. In the 80‘s private equity deals worked because valuation were much lower. It is one thing to operate at higher interest rates which over time go lower, but another to go from higher valuation/ lower interest rate Regime to one where valuations are lower and interest rates are higher. So my view is that private equity will be more impacted than most other business, since they tend to be more leveraged by design. Just a high level view. I do have a small position in KKR -

I don't know the US, but Germany needed real interest rates of 3% to get rid of inflation in the early 80's. Germany never got as bad as the US in terms of inflation and I think in 1982 Germany was running ~6% inflation and you could buy 9% 10 year bunds. I don't think it will get that far, but I think it's very difficult to kill inflation without having real interest rates after inflation.

-

My favorite oil tycoon was Armand Hammer (Oxy petroleum). stock trades like crap, but he had fun doing his thing. https://en.wikipedia.org/wiki/Armand_Hammer If I recall correctly, one day the stock jumped and it turned out the news was that Armand had slipped and broke a leg or hip when trying to step out of his bathub. Wall Street can be a cruel place.

-

Sold $ADDYY on CEO change news. I was hoping for a go private when i saw shares jumping or something like similar.

-

It's an opinion. Consumer good companies like Hindustan lever seem to trade at nosebleed levels (50-60x earnings) and the big conglomerates trade at ~30x ballpark. that's very high given the interest rates being 6%. of course this is a superficial analysis but I think one has to be careful assuming that GDP growth will translate into stock market returns. It's probably a great environment for a private investor building something from the ground up, but the public market seems like it' s pretty rich. With India, there is also a fair amount of political instability adding some hard to quantify risk.

-

The Fed can pay 5% interest rates with a 7%+ inflation forever. In fact even with 5% inflation, they would pay zero. Their income from the tax base increases with inflation. Now real positive interest rates could be a problem, but just nominal interest rates are meaningless unless inflation is subtracted.

-

India looks more like a bubble than a market worth investing. no doubt that money invested in China will move there, but it seems like the market is too small to absorb that much funds. I am guessing that as a whole those allocating now to India will do poorly.

-

NKE looks incredible faddish to me at 30x earnings. It's not luxury either or bullet proof regarding economic pressures, just a well managed consumer good company. Significant exposure to China as well.

-

Yes, the ~5% loss in income was about 6 month ago. Now we see salaries catching up with rising inflation. That's exactly how an inflation spiral works unfortunately, unless the whole thing quickly peters out.

-

Today will be another interesting day. As for unemployment - there is no signal yet that higher interest rates have affected the labor market. https://www.cnbc.com/2022/11/02/adp-jobs-report-october-2022.html The 7.7% rise in wages points to higher core inflation.

-

Berkshire vs Brookfield vs Fairfax

Spekulatius replied to CanadianMunger's topic in General Discussion

I am fairly confident that higher interest rates hurt the private equity model, which is what the likes of BX, KKR, BAM etc are perusing. the private equity model needs high asset prices and cheap money to prosper. Sure they can benefit from credit crunches and take advantage of dislocations in equity prices if they are short term, but if they persist longer, which would be likely with higher interest rates, then I think these type if business models will suffer.