Spekulatius

-

Posts

19,041 -

Joined

-

Last visited

-

Days Won

39

Content Type

Profiles

Forums

Events

Everything posted by Spekulatius

-

80% loan to deposit is a very normal number for a bank and would never really be a problem. They could either draw on a FHLB line back then (which was cheap during ZIRP) or sell their securities portfolio. Now FHLB can still be done but costs ~4.5% and selling securities hits regulatory capital. Now keep in mind that PNC (and other banks) have some interest rate hedges and PNC seems to have a decent amount of near term maturities in their security portfolio as mentioned above. They also have a pretty diverse business mix. I think their liability matching looks pretty good.

80% loan to deposit is a very normal number for a bank and would never really be a problem. They could either draw on a FHLB line back then (which was cheap during ZIRP) or sell their securities portfolio. Now FHLB can still be done but costs ~4.5% and selling securities hits regulatory capital. Now keep in mind that PNC (and other banks) have some interest rate hedges and PNC seems to have a decent amount of near term maturities in their security portfolio as mentioned above. They also have a pretty diverse business mix. I think their liability matching looks pretty good. -

Russia taking China is laughable. If anything it’s going to be the other way around and China chops of some pieces from Russia.

-

After doing 5 min of in depth due diligence, this one seems interesting: https://fundresearch.fidelity.com/mutual-funds/summary/936793827 High expense ratio though (1.51%).

-

Volkswagen has been around for a while it's not going anywhere. Neither does Porsche. VW did not spin off the shares because they wanted some cash in exchange.

-

the problem with India is that there is no good vehicle to do so. Fairfax India is an lousy way to invest in India with high fees and the closed end structures which leaves the possibility of a creeping takeunder. The individual investor can't invest in individual securities there.

-

A PNC presentation that is worthwhile to flip through as it also shows data from the overall banking sector. They did state that they believe bank reserves will get scarce toward the end of 2023. https://d1io3yog0oux5.cloudfront.net/_76cee45995c2946cacec1a8e73ca7025/pnc/db/2222/21444/presentation/JPM_Investors_March2023_FINAL.pdf PNC has a substantial security portfolio, but it is of relative short duration.- 28% will run off by YE 2024.

-

The growth in China has been there, but for shareholders China has been a dud and there are many reasons why. high GDP growth does not mean good shareholder returns.

-

Commentary from Dimon in his shareholder letter regarding the banking crisis is worth reading: BANKING TURMOIL AND REGULATORY GOALS The recent failures of Silicon Valley Bank (SVB) in the United States and Credit Suisse in Europe, and the related stress in the banking system, underscore that simply satisfying regulatory requirements is not sufficient. Risks are abundant, and managing those risks requires constant and vigilant scrutiny as the world evolves. Regarding the current disruption in the U.S. banking system, most of the risks were hiding in plain sight. Interest rate exposure, the fair value of held-to-maturity (HTM) portfolios and the amount of SVB’s uninsured deposits were always known – both to regulators and the marketplace. The unknown risk was that SVB’s over 35,000 corporate clients – and activity within them – were controlled by a small number of venture capital companies and moved their deposits in lockstep. It is unlikely that any recent change in regulatory requirements would have made a difference in what followed. Instead, the recent rapid rise of interest rates placed heightened focus on the potential for rapid deterioration of the fair value of HTM portfolios and, in this case, the lack of stickiness of certain uninsured deposits. Ironically, banks were incented to own very safe government securities because they were considered highly liquid by regulators and carried very low capital requirements. Even worse, the stress testing based on the scenario devised by the Federal Reserve Board (the Fed) never incorporated interest rates at higher levels. This is not to absolve bank management – it’s just to make clear that this wasn’t the finest hour for many players. All of these colliding factors became critically important when the marketplace, rating agencies and depositors focused on them. As I write this letter, the current crisis is not yet over, and even when it is behind us, there will be repercussions from it for years to come. But importantly, recent events are nothing like what occurred during the 2008 global financial crisis (which barely affected regional banks). In 2008, the trigger was a growing recognition that $1 trillion of consumer mortgages were about to go bad – and they were owned by various types of entities around the world. At that time, there was enormous leverage virtually everywhere in the financial system. Major investment banks, Fannie Mae and Freddie Mac, nearly all savings and loan institutions, off-balance sheet vehicles, AIG and banks around the world – all of them failed. This current banking crisis involves far fewer financial players and fewer issues that need to be resolved. These failures were not good for banks of any size. Any crisis that damages Americans’ trust in their banks damages all banks – a fact that was known even before this crisis. While it is true that this bank crisis “benefited” larger banks due to the inflow of deposits they received from smaller institutions, the notion that this meltdown was good for them in any way is absurd. Let’s be very thoughtful in our reaction to recent events. While this crisis will pass, lessons will be learned, which will result in some changes to the regulatory system. However, it is extremely important that we avoid knee-jerk, whack-a-mole or politically motivated responses that often result in achieving the opposite of what people intended. Now is the time to deeply think through and coordinate complex regulations to accomplish the goals we want, eliminating costly inefficiencies and contradictory policies. Very often, rules are put in place in one part of the framework without appreciating their consequences in combination with other regulations. America has had, and continues to have, the best and most dynamic financial system in the world – from various types of investors to its banks, rule of law, investor protections, transparency, exchanges and other features. We do not want to throw the baby out with the bath water.

-

I think this happens more often than we thins. T&T buy something and may sell even and then Buffett digs in and decides to make it a major positions. It did happen with CVX which I think T&T bought and sold in 2020 and Buffett went all in in 2021/22.

-

Yes. Having free unused storage capacity is actually a huge advantage if you want to trade crude (buy low, sell high)

-

I use the WSJ to look for financial news but completely ignore the political part and the opinion pieces. Al Jazeera is quite good for foreign news that is typically ignored in the US. I snoop a bit around in German news sources too. The Christian science monitor has pretty interesting articles but I rarely check in there. I don't have access to the FT.

-

I used to read ZH and John Mauldins newsletter starting in 2008 or so. They both sound clever, but if you go down these rabbit holes they are digging you end up wasting a lot of time and even worse, probably lose a lot of money just through opportunity cost if you actually start to believe the financial doomsday porn they are writing. In my opinion, it's important to have some basic media hygiene in terms of what you are consuming. While it is probably a good idea to look at some alternative news sources from time to time, but if you start to dig into these fringe newsources there is a good chance you start to convert your thinking into conspiracy mush where Occam's razor has no chance to cut through any more.

-

NVDA really looks like a bubble, but looking at puts, I need to pay ~$10 for a $200 strike for 10/2023. That's a ~$190 breakeven or down 32% from the current $280 share price. Looks more like a candidate for straight up shorting but I don't short.

-

I followed ZH in past the GFC for a while. The news / blogs were mostly about financial topics back then and there were some interesting morsels of information here and there. however, even back then I found following this counterproductive after a while, since there were so many half truth and biased information there, that it was not worth following. The site morphed from being a dominantly financial newsite to a general and conspiracy site that became increasingly friendly towards Russia and hostile toward the US. If you read stuff like this, you just go down many rabbit holes to nowhere and at best waste your time and worst become a loony.

-

Ukraine: What Everyone Needs to Know - Serhy Yekelchyk

Spekulatius replied to Spekulatius's topic in Books

The country has a tortured history that is very closely connected to Russia. it wasn't called Little Russia for no reason. Since the USSR broke apart, they have slowly moved away from Russia in fits and starts - 1992, 2004 (Euromaiden I, 2014 Euromaiden II, subsequent invasion of Crimea and Donbas, 2020 War are all steps towards independence and moving towards the West. Putin does not like it and tries to reverse it, but it seems to me that he is failing (hopefully). Ukraine inherited some of the same baggage than Russia did - a dysfunctional economy, Oligarchism, Corruption, but much less resources, but they are trying. Russia isn't even trying, they have fallen back into some Czarist authoritarian state where I don't I don't see much of a future other than becoming perhaps a version of Venezuela in the long run. The book gives you a better perspective where the Ukraine is coming from and where they might be going. -

Fascinating background story on the “alternative news” website Zerohedge: https://newrepublic.com/article/156788/zero-hedge-russian-trojan-horse

-

How much capital is required to support this carry trade? The return may not be that great. Banks do not have a liquidity risk in general, but I think there is a risk from the cost of deposits/ financing rising faster than the interest income (NIM squeeze).

-

I Need a Laugh. Tell me a Joke. Keep em PC.

Spekulatius replied to doughishere's topic in General Discussion

Yup: -

Got this one on my birthday and finally got through reading it. It contains a wealth of information and background about recent Ukraine history (all pre-war) and helps to understand the situation better. It sort of a bone dry read though. https://www.amazon.com/Ukraine-What-Everyone-Needs-Know®/dp/019753211X

-

I think AI bots will be a supplementary business for cloud providers basically. That means MSFT, AMZN, GOOGL maybe Alibaba in China. They already have the server and computing capacity.

-

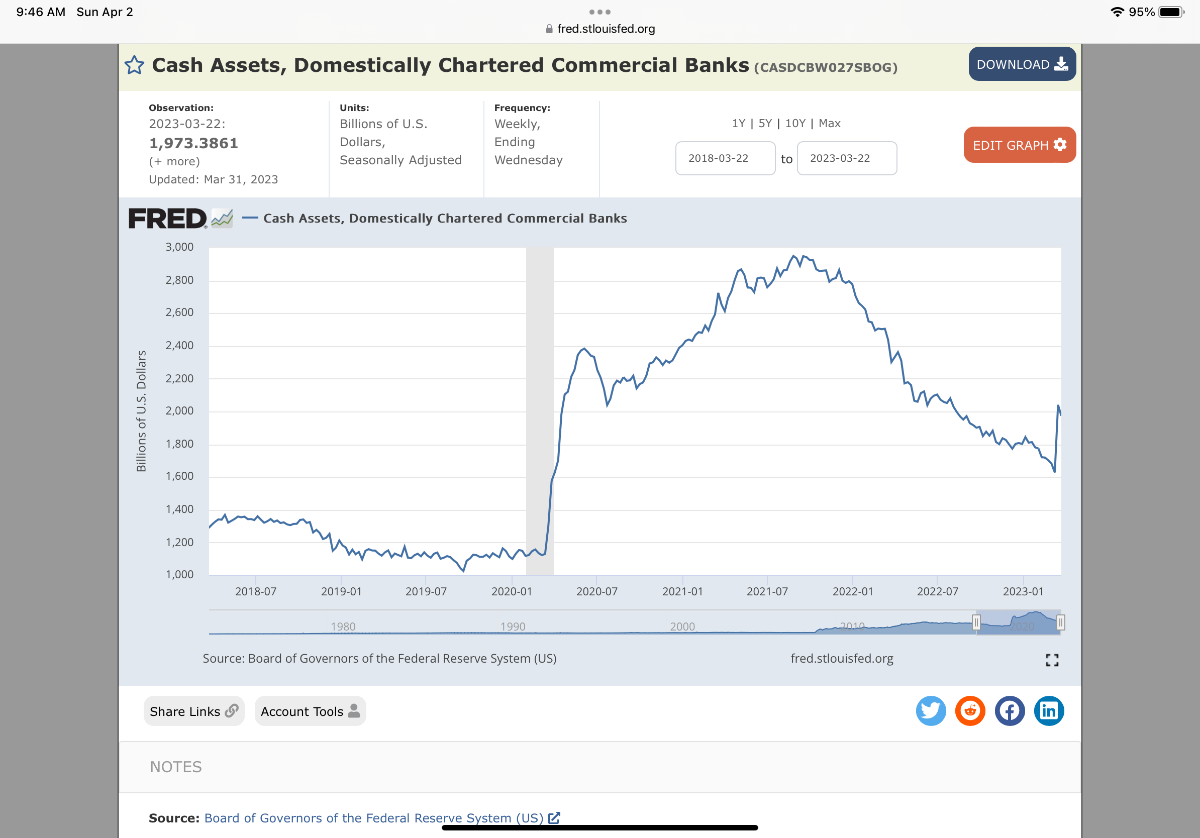

@Cigarbutt I think in terms of MM flows, the current situation is similar to 2005-2007. At that time, we also had come Competition for deposits heating up because MM fund were yielding ~5% by the end of 2006. As I recall, we never saw a dramatic outflow in deposits into higher yielding vehicles. We will see if this time will be the same or different. As for cash levels at banks, we can get all this data from FRED. It’s weekly updated so the recent cash increase from the bank Panik shows already. https://fred.stlouisfed.org/series/CASDCBW027SBOGAs As I mentioned before, banks used to sell securities when they wanted to lend and couldn’t increase deposits. This time, it’s not an option, they have to wait for them to mature, or take huge losses hitting regulatory capital.

-

My guess is that any AI model will have blind spots that somebody figures out how to brutally exploit and make a lot of money. It’s a dog eat dog world in finance, especially if it’s a zero sum game.

-

Phenomenal businesses that don't require any capital

Spekulatius replied to LearningMachine's topic in General Discussion

Tobacco / Nicotine is very capital light, but it doesn’t matter because the business is shrinking by volume - at least combustibles do. So there isn’t really any incremental dollar to invest. The alternatives like heated tobacco and vaping area different story and require significant capital and marketing dollars to win market share. This business is not capital light at all. -

Einhorn claims in the last “Invest like the best” podcast that “Value investing doesn’t work any more”. I think it’s strong statement and sort of funny as if Mr Market has any obligation to agree with his view when he put in a 100 page slide presentation. Or reversely, I guess it’s a problem for him, if he present a short and the Markt yawns and the stock stays where it is or even goes up. For a while 10 years ago, he could move markets and just be right because a lot of people followed his coattails and stocks went his way after he present a thesis. Now he is just treated like everyone else and Mr Market yawns and now it’s like “Value investing does not work any more” because he can’t move market any more. I think there is a certain arrogance in this way of thinking.

-

Bakeries Are Essential To The French Way of Life

Spekulatius replied to Parsad's topic in General Discussion

Thee baguettes are so cheap - 1.3€ for a baguette. It would be 3x as much in the US. I guess they just have to raise prices.