UK

-

Posts

2,644 -

Joined

-

Days Won

15

Content Type

Profiles

Forums

Events

Everything posted by UK

-

https://eurasiantimes.com/ukraine-russias-nuclear-capable-kh-55-missile/

-

https://www.bloomberg.com/news/articles/2022-11-17/oaktree-s-marks-sees-great-bargains-coming-as-recession-looms Marks predicts US inflation has likely peaked, and expects rates to stay near the 5% mark in the next 5 to 10 years. An accompanying shift in consumer appetite alongside higher borrowing costs will lead to “significant distress” at many companies, he said. “A year ago the outlook was considered flawless and I think we’re going to reach a point where they consider it hopeless,” he said of investors. “And that’s when you get the big buys. That’s when you get to be a buyer of assets cheap and a maker of loans at high yields with safety.” Credit markets have seized up as the Federal Reserve hikes rates at the fastest pace since the early 1980s. Banks that agreed to backstop loans at one price months ago are finding that appetite has changed and funds are demanding higher yields. That’s prompting firms specializing in distressed debt to prepare for a potential boom. And while corporate America as a whole is not highly levered, the distress is piling up, he said. “This is going to be a buyer’s market and a lender’s market. We’re going to have much better opportunities,” he said, adding that tech buyouts over the last 13 years have led to an accumulation of debt. “We’ll be looking among the ruins for great bargains.” https://www.institutionalinvestor.com/article/b20q0fnk434bpg/ackman-made-2-billion-this-year-betting-on-rising-rates Today Ackman is still betting that interest rates will continue to rise, saying they are “meaningfully below where they are going to go. That is a risk for equities.” He believes that inflation is going to be structurally higher than it has been historically. “We don’t believe the Fed is going to get back to 2 percent,” Ackman said, referring to the inflation target the Fed has historically used. Various factors, including de-globalization, will keep inflation at a higher level in the U.S. “We had the benefit for many years of outsourcing of production to low-cost labor markets,” he said, but that era is over. The Covid pandemic alone has made the U.S .reconsider “distant supply chains.” “A lot more of that business is going to come closer to home,” he said. “It’s more expensive to do business here.” Ackman also thinks “the transition to alternative energy is going to be expensive.” All of that means that the cost of debt will continue to rise for companies. “Locking in a 4 percent fix rate for 30 years is going to be difficult to do,” he said.

-

https://www.wsj.com/articles/u-s-vows-to-tackle-visa-delays-as-frustrations-mount-11668718834 WASHINGTON—A top State Department official pledged Thursday that wait times for tourist, student and work visas would shorten significantly in the next year as the department ramps up processing to meet crushing demand for entry to the U.S. The State Department has been struggling to keep up with visas since 2020 when the Covid-19 pandemic forced the closing of U.S. consulates around the world, bringing the application process for entry into the country temporarily to a halt. Two and a half years later, some consulates are still offering only emergency appointments. Though visa issuance has mostly rebounded to prepandemic levels, demand for visas is so high that appointments for anyone looking to apply are often booked months or even years out, and the Biden administration has faced mounting anger from business groups, Silicon Valley companies, universities, hospitals and the travel industry over the delays. The wait times are worse than anything the State Department has seen before, said Deputy Assistant Secretary Julie Stufft, who briefed reporters Thursday.

-

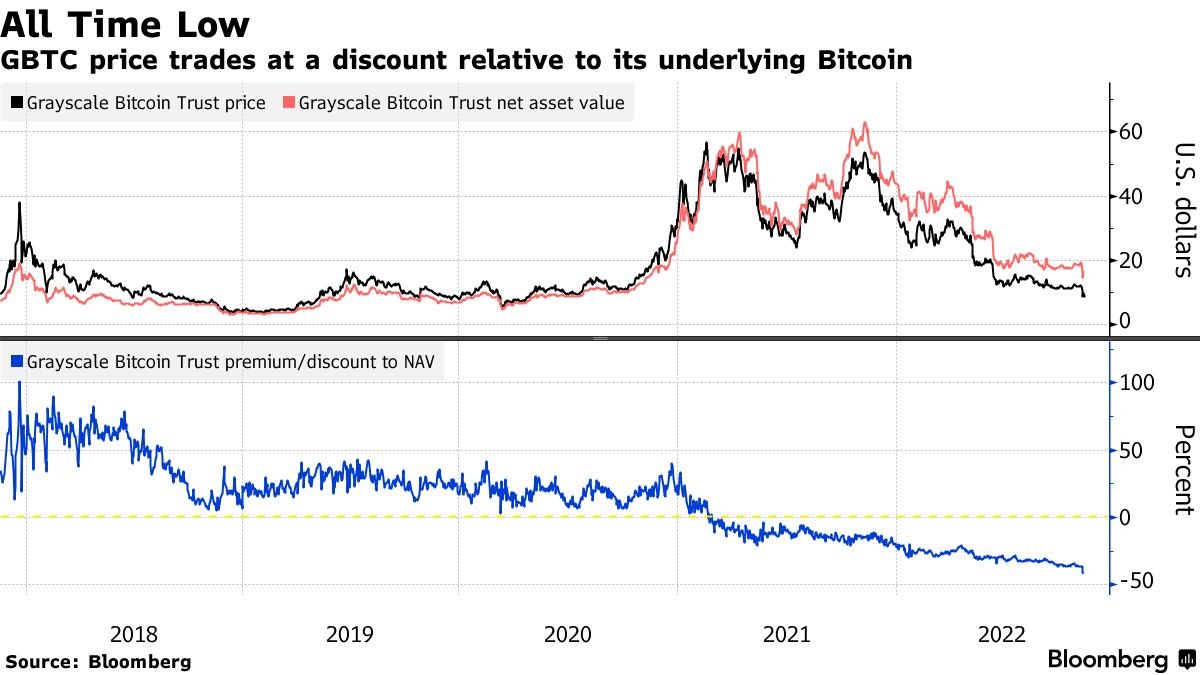

OK so this perhaps answers the question on why not GBTC:)

-

https://www.economist.com/europe/2022/11/17/ukraine-has-momentum-what-it-needs-now-are-munitions More ambitious still is the third option: a major attack south from Zaporizhia towards Melitopol and beyond to sever Russia’s so-called land bridge to Crimea, and possibly thence along the Sea of Azov coastline to Mariupol. Mr Zelensky had pressed for such an offensive in the summer, but was talked out of it by his own generals, after American and British wargaming showed how difficult and costly such a thrust would be. Russia evidently sees this as a possibility. It is churning out miniature concrete pyramids, known as dragon’s teeth, and probably laying them around Mariupol to block oncoming armour. Satellite images show excavators digging zig-zag trenches at the entrance to Crimea. These entrenchments and fortifications are “old-fashioned and static”, says a Western official, “but also fit for purpose”. There is no doubt that Russia’s army is in poor shape. Ukrainian intelligence says that Russia has only around 120 Iskander ballistic missiles remaining in its arsenal. The situation with artillery ammunition is even worse. Western officials have told The Economist that Russia has around a month’s worth of it left—one reason why it decided to abandon the Kherson front. But Ukraine faces some of the same limitations. It is running short of many different types of ammunition, including the air-defence interceptors needed to parry Iranian-supplied drones and Russian missiles. It has been on the offensive since August. It has also taken heavy casualties. Mark Milley, the chairman of America’s joint chiefs of staff, said on November 9th that Ukraine, like Russia, had suffered approximately 100,000 casualties, either killed or wounded. Sceptics, including General Milley, argue that Ukraine’s main offensives are probably over for the winter. They argue that Ukraine’s ground offensives in Kherson were not much different from Russia’s in Donbas—slow, crude and relatively ineffective—and that the earlier breakthrough in Kharkiv occurred only because Russian lines were woefully undermanned, a condition that is unlikely to obtain elsewhere as mobilised recruits arrive in greater numbers and Russia redeploys more than 30,000 soldiers freed up from Kherson. Optimists point to Ukraine’s advantages. It has 200,000 to 300,000 combat-capable troops, against fewer than 100,000 Russians in the field. Morale among Ukrainian forces is sky-high, a key factor in winter warfare, in which soldiers must bear acute hardship. It also has the edge in precision firepower, thanks to gps-guided shells and rockets, such as Excalibur artillery rounds. Ukraine’s success in Kherson ultimately offers reasons for both optimism and caution, says Michael Kofman of cna, a think-tank. It shows that Ukraine, if adequately supplied, can take back territory over time, but also that future offensives are more likely to be slow, attritional battles than Kharkiv-like Blitzkrieg. Ammunition, for artillery and air defence, is “the most decisive factor”, argues Mr Kofman. Ukrainian units on the attack will eat through more of it than Russian ones on the defence. They are already consuming a majority of America’s monthly production of gmlrs, the gps-guided rockets fired by himars, according to one source. The good news is that America and its European allies are beginning to expand ammunition production. The bad news is that Ukraine may not feel the benefit until next summer. Mr Zelensky might note that after Churchill more modestly pronounced the end of the beginning after the second battle of El Alamein in 1942, the war still had three long years to run. https://www.economist.com/leaders/2022/11/16/russia-needs-a-respite-so-the-west-must-help-ukraine-fight-on Some American officials are showing signs of nerves. Mark Milley, America’s top general, has likened the conflict to the stalemate of the first world war. He has cast doubt on Ukraine’s ability to shift the front lines farther and suggested that it should consider negotiations with the Kremlin. His diagnosis and prescription are both flawed. Russia’s army is in dire shape and on the retreat. Its withdrawal from Kherson earlier this month reflects a serious shortage of artillery ammunition. Precision munitions are running out, which is why Russian attacks on Ukraine’s energy grid rely on Iranian drones. And even as the seasons bring mud and bitter cold, Ukraine, well stocked with Western winter gear, will keep fighting. Russia needs a pause. It should not be given one. For Ukraine to press its advantage, it requires a steady supply of Western arms, ammunition and equipment. Top of the list is air defence. As its Soviet-era systems run low on ammunition it needs additional Western launchers that can be replenished more easily—including longer-range Patriot batteries. Air defences can also spark a virtuous circle that would allow Ukraine to ramp up its own arms production without fear of having factories destroyed. Its army hopes to raise as many as a dozen new brigades for a future offensive. They will need a large fleet of armoured vehicles. On November 15th the Biden administration asked Congress for over $37bn in emergency aid to Ukraine—more than the defence budgets of Australia, Canada or Italy. Europe must show the same sense of urgency. Russia’s air attacks should serve as the trigger for the dispatch of tanks, such as German Leopards. European allies should create a fund to support the provision of Sweden’s Gripen fighter jets, which are easy to maintain and well suited to Ukraine’s flexible operation. This week’s incident, and the danger that setbacks on the battlefield will lead Russia’s president, Vladimir Putin, to escalate, including with nuclear weapons, show the importance of maintaining channels of communication with Russia. That is why Bill Burns, the director of the cia, was right to meet his Russian counterpart in Turkey on November 14th. The door to a future diplomatic settlement, when both Ukraine and Russia are ready for one, should be left open. But a ceasefire now would be deeply disadvantageous to Ukraine, halting its momentum and giving Russia breathing space to restock its arsenal and prepare a fresh army. This is not the moment to let up.

-

https://www.wsj.com/articles/mark-milley-and-the-coming-civil-military-crisis-joint-chiefs-ukraine-negotiation-russia-politics-president-11668634194

-

It is like a different galaxy, former Valeant's corporate cotrol looks like almost taintless comparing to this:))) https://www.wsj.com/articles/ceo-overseeing-ftx-restructuring-calls-it-an-unprecedented-mess-11668707836?mod=hp_lead_pos1 “Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here,” Mr. Ray said in the filing. “From compromised systems integrity and faulty regulatory oversight abroad, to the concentration of control in the hands of a very small group of inexperienced, unsophisticated and potentially compromised individuals, this situation is unprecedented.” On Wednesday, the news website Vox posted an article featuring screenshots of direct messages exchanged on Twitter between Mr. Bankman-Fried and a reporter, Kelsey Piper. In a part of the exchange, he said “f— regulators” and asserted that “they make everything worse.” He also implied that his advocacy for better crypto regulation in Washington was “just PR.”

-

https://www.bloomberg.com/opinion/articles/2022-11-16/-next-warren-buffett-curse-hit-sam-bankman-fried-but-it-isn-t-always-fatal

-

Seems like some friendly fire after all. However, not sure how much it is true, but it also seems that a very high percentage of Russian rockets from the last barrage were very successfully taken down by improving Ukraine air defense. Germany and other western countries have some really effective hardware:)

-

I think that price of oil it is not so important at this point, especially for core inflation. Housing and shelter and prices of goods will be two positive things reducing inflation from now on. Not sure about servIces but the bigest problem I think is wages, which are somewhat programed to still increase for some time Just look at all these ongoing labour union disputes and negotiations.

-

Interesting. I am not sure if I understand this chart correctly, but if inflation really soon will be decreasing as the chart suggests and will reach 2-3 range sometime after start of 2024, would not that be extremely bullish for the next 2 years? And before 2025 just go back to BRK and cash again:)))

-

Very interesting, thanks for finding this out. So how sure we could be, that purchase was made by WB? 99 per cent?, 50/50?

-

Interesting, never heard about them. Do you know how their portfolio looks like or what are their top positions? Also foundthis one on them: https://youtu.be/Zs0ZDbmpIOk

-

Thanks for response!

-

I was just guessing, but also thought that maybe it was T or T, who sold his share of USB and bougth TSM. Now, if WB bought TSM himself it would be a great news, since it is cheap and very strong business, but also it would mean, that his circle of competence has increased quite substantially! To make decisions about all thes extreme ultraviolet things is quite something comparing to water and sugar. So interesting and great news anyway!

-

Yes, oil bet is big and definately Buffett's. PARA I would guess is not his bet. Also it is possible, that USB was bought by WB and also later by one of T. If TSM was bought by WB himself, it would be quite a surprise, but it is almost to large for T or T, but maybe their allocations of BRK portfolio were increased?

-

https://www.bloomberg.com/news/articles/2022-11-14/-broken-crypto-fund-hits-record-42-discount-as-etfs-hum-along What about this one? Would it be possible to liquidate it some day if SEC denies approval? At least an extra 40 per cent discount? Why not vs BTC? “As far as GBTC goes, I don’t know what stops this thing from sinking into a further discount,” said Bloomberg Intelligence ETF analyst James Seyffart. “There’s also an argument to be made that the widening discount is reflective of a lower probability or at last a longer time frame before GBTC is able to convert to an ETF.”

-

Thanks!

-

Re 2. Or is still not to large to be for T or T? Interesting pick nevertheless. Some really deep tech:)? At what time or where do you see information on Charlies interview?

-

What is your estimate of "significantly higher"? ~500 K USD if ~on par with gold? It would mean we just went from possible upside 10x to 30x in say 10 years? But even more important question: how low it go down further? Is it possible for BTC to trade below 10.000 USD at some point in the future? 1.000 usd?

-

I think even Munger already aknowledged, that BTC is like gold. At the same time they are saying similar things about gold as of Bitcoin. Also on art etc. Since those are not productive assets, Buffett an Munger is probably right in a very long term. Even super art items have lousy long term returns vs productive things. But that does not mean one can not make some money speculating them. But as Dealraker said it is quite difficult to understant difference between 20 or 1 M USD? What is a good price for BTC?

-

https://www.telegraph.co.uk/world-news/2022/11/14/russias-spy-chief-talk-us-g20-leaders-meet-discuss-ukraine-war/

-

What obvious implications possible war ending would have in terms of economies and markets? Perhaps it would be somewhat disinflationary at least in short/mid term? Also bullish for Europe? https://www.wsj.com/articles/as-ukraine-retakes-kherson-u-s-looks-to-diplomacy-before-winter-slows-momentum-11668345883 The imminent onset of winter—coupled with fears of inflation spurred by mounting energy and food prices, the billions of dollars of weaponry already pumped into Ukraine, and the tens of thousands of casualties on both sides—has prompted talk in Washington of a potential inflection point in the war, now in its ninth month. The U.S. and its allies are pledging to continue supporting Ukraine, but top officials in Washington are beginning to wonder aloud how much more territory can be won by either side, and at what cost. Some European officials, meanwhile, are more bullish on Ukraine’s chances. “There has to be a mutual recognition that military victory, in the true sense of the word, is maybe not achievable through military means, so therefore you need to turn to other means,” Army Gen. Mark Milley, the chairman of the Joint Chiefs of Staff and the top U.S. military officer, told the Economic Club of New York on Wednesday. “There’s also an opportunity here, a window of opportunity, for negotiation.” “It remains to be seen whether or not there’ll be a judgment made as to whether or not Ukraine is prepared to compromise with Russia,” Mr. Biden said at the White House. He added: “They’re going to both lick their wounds, decide…what they’re going to do over the winter, and decide whether or not they’re going to compromise.” Washington has signaled to Ukraine that at a minimum Kyiv needs to appear open to a negotiated solution. Mr. Biden’s national security adviser, Jake Sullivan, conveyed that message to President Volodymyr Zelensky and his lieutenants in Kyiv on Nov. 4, suggesting that Kyiv would gain leverage by showing openness to negotiations, according to people familiar with the discussions. Two European diplomats briefed on the discussions said Mr. Sullivan recommended that Mr. Zelensky’s team start thinking about its realistic demands and priorities for negotiations, including a reconsideration of its stated aim for Ukraine to regain Crimea, which was annexed in 2014. Officials in some European countries, particularly in the east and north, have said that publicly pressing for talks could hurt Ukraine’s efforts and play to Russia’s aims of dividing the alliance. “We need to talk about the cost of peace,” one northern European official said. If the war ends now, “The message the Ukrainians would get is that their fight was meaningless. The message Russia would get is that this is time to refit and to rebuild economically. No one believes [Russia] will stop until they achieve their strategic objective.” Mr. Putin has said that Russia is open to peace talks and argued that if Washington ordered Mr. Zelensky to sit down for negotiations, Kyiv would do so. With the latest setbacks in the battlefield, Western officials have said the Kremlin appears to have backed away from its previous preconditions for talks, such as accepting Russia’s annexation of Ukrainian territory.

-

Thanks, nice to know. I am quite familiar with this bank and totaly agree with you. Just read another day, how they are now reflecting on how banks are "overearning" and on this oligopoly situation, which was further strenghtened after GFC debacle. I agree that in Ireland and some other countries banks are day and night vs some other EU countries.

-

https://markets.businessinsider.com/news/currencies/crypto-ftx-collapse-spread-icahn-siegel-erian-summers-novogratz-roubini-2022-11