All Activity

- Today

-

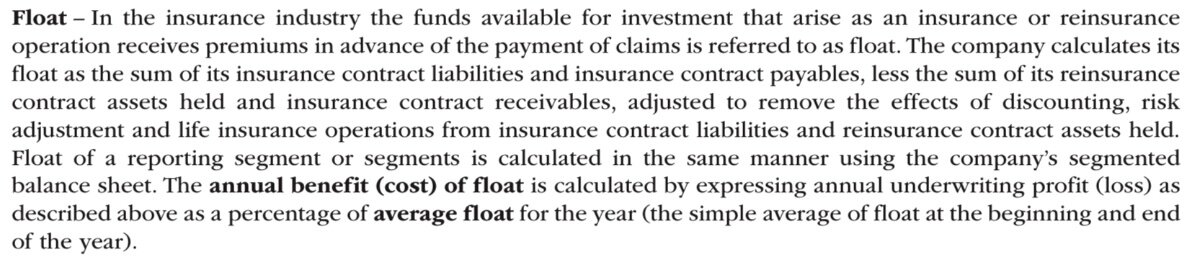

@Cigarbutt, thanks again. This is a quick follow up in relation to a question that was posed in the Q1 24 Conference call regarding the potential to rotate into equities from the fixed income portfolio during a market sell off. Running the numbers again based on Fairfax’s definition of float as provided in the annual, agree with you ratio of around 1.3 as follows: Your Calc Step 1: Calculate the approximate insurance float Insurance contract liabilities (Note 8): $45,918.1 million Insurance contract payables: $1,065.0 million Reinsurance contract assets held (Note 9): $10,808.6 million Insurance contract receivables: $811.0 million Float = Insurance contract liabilities + Insurance contract payables - Reinsurance contract assets held - Insurance contract receivables = $45,918.1 + $1,065.0 - $10,808.6 - $811.0 = $35,363.5 million Step 2: Calculate the total cash and fixed income portfolio Holding company cash and investments: Holding company cash and investments (including assets pledged for derivative obligations): $2,496.4 million Portfolio investments: Subsidiary cash and short term investments: $7,801.6 million Bonds: $36,131.2 million Subtotal: $43,932.8 million Assets pledged for derivative obligations: Bonds: $115.5 million Total cash and fixed income portfolio = Holding company cash and investments + Portfolio cash and fixed income investments + Assets pledged for derivative obligations (Bonds) = $2,496.4 + $43,932.8 + $115.5 = $46,544.7 million Step 3: Calculate the ratio of cash and fixed income portfolio over insurance float Ratio = Total cash and fixed income portfolio / Insurance float = $46,544.7 / $35,363.5 = 1.32 Based on the information provided in Fairfax's Q1 2024 interim consolidated financial statements, the company's cash and fixed income portfolio is approximately 1.32 times its insurance float. However, as mentioned earlier, the float calculation is subject to adjustments for discounting, risk adjustment, and life insurance operations, which are not provided in the interim financial statements. As a result, the actual ratio may differ from this approximation. At least I agree with your starting number of 1.3, thanks MCT Approach with lots of assumptions (I think this might be flawed too) Ran the numbers in Chat GPT and end up with $3.6 bn realllcation based on MCT. The asset weightings and hence MCT ratios were completely different to Claude. So unfortunately it is numberwang. Not to mention we have two approaches MCT and RBC. FWIW based on RBC it looks like this and solving for an RBC ratio of 300% (320% currently) gives you the following table: Conservative RBC Ratio Standards: - Very Strong: 400% and above. This level is often seen as very conservative, providing a substantial cushion against potential losses. - Strong: 300% to 399%. This is still considered a robust conservative level, offering good financial stability and less risk of breaching lower thresholds under normal market conditions. The National Association of Insurance Commissioners (NAIC) in the U.S., which introduced the RBC system, sets various action levels based on the RBC ratio. Here’s a general overview of these levels: 1. Company Action Level: When the RBC ratio falls to 200% of the required minimum, the company must submit a comprehensive financial plan outlining how it will improve its capital situation. 2. Regulatory Action Level: If the ratio falls to 150% of the required minimum, state regulators may intervene more directly, possibly requiring changes in operations or financial restructuring. 3. Authorized Control Level: At 100% of the required minimum, regulators may assume control of the insurer to protect policyholders and creditors. 4. Mandatory Control Level: If the RBC ratio falls below 70% of the required minimum, regulators are typically mandated to take over the insurer The Risk-Based Capital (RBC) and Minimum Capital Test (MCT) are both regulatory standards used to ensure that insurance companies maintain adequate capital to support their risks, but they differ in their scope, methodology, and geographical usage. Here’s a detailed comparison: Geographical Usage - RBC: Primarily used in the United States, established by the National Association of Insurance Commissioners (NAIC). - MCT: Used in Canada, specifically designed for Canadian insurance companies. Purpose and Scope - RBC: Designed to establish minimum required capital for insurance companies to support their overall business operations while covering various risks, such as underwriting, credit, market, and operational risks. RBC aims to provide a buffer against insolvency by requiring higher capital for higher risks. - MCT: Similar to RBC, MCT measures the sufficiency of an insurance company's capital, focusing on its ability to withstand financial instability or claims. It also looks at various risks but is tailored to the specific regulatory environment in Canada. Methodology - RBC: Uses a formula-based approach where different risk elements (C1 through C4) are quantified: - C1 (Asset Risk): Reflects the risk of default and changes in market values of assets. - C2 (Insurance Risk): Covers risks associated with underwriting liabilities and pricing. - C3 (Interest Rate and Market Risk): Addresses the potential for asset and liability mismatches due to changes in market conditions. - C4 (Business and Operational Risk): Concerns with business operations and management risks. - MCT: Also formula-based, MCT quantifies assets, liabilities, and off-balance-sheet exposures, assigning them into various categories with corresponding risk factors. The calculation considers: - Assets Quality: Different assets are assigned risk weights based on their likelihood of loss or impairment. - Liabilities: Liabilities are evaluated for their potential impact on capital, including insurance liabilities and operational liabilities. Calculation Outputs - RBC: Produces a capital ratio that insurers must meet or exceed, which is set by regulatory authorities. Insurers are required to take corrective action if their RBC falls below the mandatory threshold. - MCT: Produces a similar ratio, the MCT ratio, which indicates the capital adequacy relative to the risks the insurer holds. A threshold is set, and if an insurer’s MCT ratio falls below this, they must increase their capital or reduce their risk. Regulatory Actions - RBC: If an insurer’s RBC ratio falls below regulatory thresholds, a range of actions can be triggered, from requiring a comprehensive business plan to direct regulatory intervention. - MCT: Similarly, falling below the MCT ratio can lead to enhanced regulatory supervision and may require the insurer to submit plans on how they will improve their capital position. Adjustments and Sensitivity - RBC: Highly sensitive to changes in asset values and risk profiles, requiring frequent updates and recalculations. - MCT: Also requires updates based on changes in the company's financial condition and market dynamics, but may differ in how sensitivities are treated under Canadian regulations. Both systems aim to protect policyholders and ensure market stability by preventing insurance company failures, but they do so through region-specific frameworks that reflect local market conditions, regulatory environments, and insurance practices.

-

@Cigarbutt thanks for the handholding appreciate it. I will post a reply to a separate thread in order not to clutter up this thread further https://thecobf.com/forum/topic/20743-market-sell-off-equity-reallocation/

-

Haha so at 36 I am up for the next 20 most unhappy years of my life... Funny but that unhappy age category is also the age when people have kids and have to work

-

It's worse than that. They took the Israeli offer and changed the language and now say they accepted it. Israel: We want 33 live hostages Hamas: We will give 33 live or dead hostages Hamas: OK we accept! There are few other things language changes that basically cancel out all the non-negotiables for Israel.

-

SD - I respect many of your opinions, but you are out of depth on this one. There are very few IDF conscripts that are refusing to go to Rafah (I have a relatively large Israeli family across the political spectrum, with a couple serving in Gaza, or are about to go to Gaza). And ever fewer consider it a war crime. And in reality, going into Rafah is not a war crime at all.

-

Bernie should know better. His time in US Gov't will soon come to an end and with it all of his loonie ideas. Though Bernie is probably the least harmful of the bunch that includes AOC, Ilhan Omar, etc.

-

Movies and TV shows (general recommendation thread)

DooDiligence replied to Liberty's topic in General Discussion

Probably already been mentioned but... -

-The 2.7B may be the right number and looking at this from several perspectives does help. -If interested look at FFH's 1990, 1991 and 1992 (much smaller insurance operation then) and see their equity exposure relative to capital... -The reference to BRK and the "ratio" is because it's a simple measure and easy to compute. At BRK, there is probably an embedded margin of safety which may be an adequate reference given FFH's past history during some transitions (many episodes requiring selling stock below intrinsic value, reaching for a line of credit etc). -The numbers about float need to take into account the definition of float as mentioned in FFH's annual reports: "Float is essentially the sum of insurance contract liabilities and insurance contract payables, less reinsurance contract assets held and insurance contract receivables, on an undiscounted basis excluding risk adjustment." So you need to subtract reinsurance contract assets (among other less important adjustments) to calculate float. -Questions and comments -i guess the idea is to (sell high and buy low) switch funds when equities become available at lower prices. If this idea applies, then the value of those regulatory measures become relevant ie they require a margin of safety. But then, you need a dynamic picture as bonds assets (including mortgage loans) can get downgraded or even default and other equity instruments (including the very significant total return swap on its own stock) can lose value. These changes impact regulatory capital to a very significant degree. -As a concept, moving funds from bonds (lower risk-weight) to equities (higher risk-weight) should impact negatively the MCT ratio. Why not in your example? You are right, this was not well phrased. The risky assets ratio is an indicator of potential future capital impairment. In a downturn, the risky asset ratio may go up if for example many bonds held get downgraded (have a higher risk weighting) or if unimpaired equities become impaired but the ratio may go down as a result of what you describe or if the company sells risk assets and fly to safety. However, when starting with a high risky assets ratio, the risk of capital impairment (including regulatory capital impairment) is higher, which is why FFH is close to the BBB category, a riskier posture for an insurer.

-

Berkshire Hathaway Annual Meeting 2024

xboojum replied to good-investing's topic in Berkshire Hathaway

Buffett had people for that -- Harry Bottle was the fixer at Dempster Mill, for instance. -

Movies and TV shows (general recommendation thread)

Saluki replied to Liberty's topic in General Discussion

It's a silly show but by better half and I are watching "Girls 5 Eva" and it's funny and light. -

Movies and TV shows (general recommendation thread)

Xerxes replied to Liberty's topic in General Discussion

“Spies of Warsaw” on Prime is an okay show. Covers the few years leading right up to Molotov-Ribbentrop pact and the invasion of Poland. Sadly much like BBC tv shows, all nationalities speak English for our sake. Except Germans who speak Germans. -

It is incredible. Buffett presented the now infamous slide in 2020’ AGM, where he showed the world biggest Japanese companies in late 1980s, and contrasted that to the FANG era, yet he kept and let Apple run for 4 more years and just now he started his “trim” for tax reasons. Berkshire is happy to pay tax, but Buffett is also very happy to arbitrage against potential corporate tax increases and offset with Paramount tax losses.

-

I know nothing about this but looking at it logically, why would this ratio go up in a downturn. When those risky assets are either in a down marked or forcibly marked down, their dollar amount will go down and, therefore, their proportion compared to the rest of the assets will go down and thus risky assets ratio going down may improve rating.

-

Charlie gave him crap for the tiny AAPL sell a few years back. WEB replied it would likely be a mistake. Then this.

-

He rambled, but it was tax rate arbitrage. Also, you have to wonder if he isn’t trying to give Greg optionality with the larger cash position and a less ridiculously sized single equity position.

-

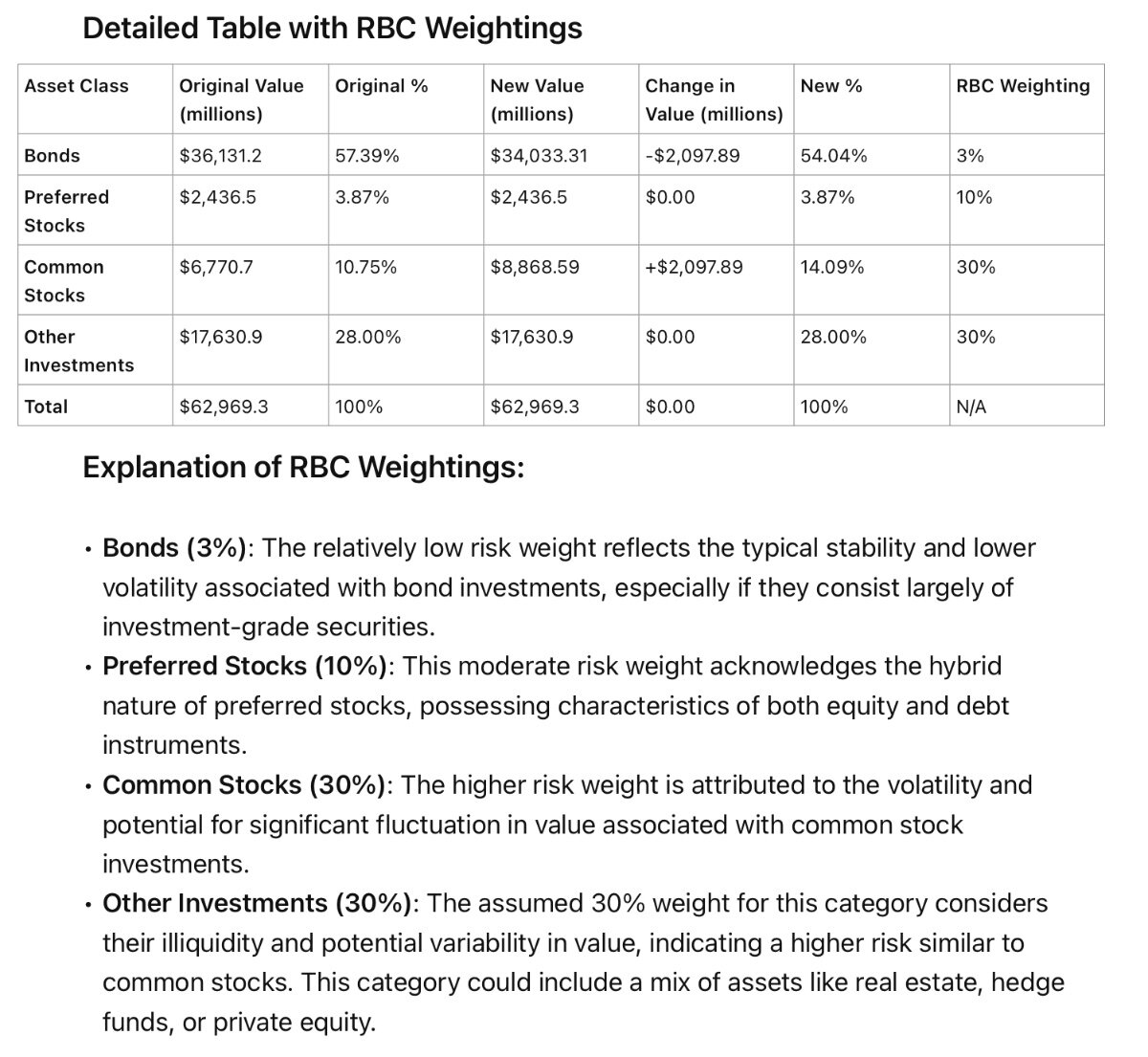

Thanks @Cigarbutt That was very helpful to kickstart my thinking. Ultimately the management at FFH has their arms fully around this. However it prompted me to give your numbers a revisit and also do some quick and dirty numbers of my own Key point Statutory requirements for insurance companies typically include risk-based capital (RBC) ratios, which measure an insurer's capital adequacy relative to its risk profile. In the United States, the National Association of Insurance Commissioners (NAIC) recommends a minimum RBC ratio of 200%. In Canada, the Office of the Superintendent of Financial Institutions (OSFI) requires a minimum Minimum Capital Test (MCT) ratio of 150%. Assuming Fairfax maintains a conservative RBC ratio well above the minimum requirements (e.g., 300% or higher), the company might have some flexibility to reallocate a portion of its bond portfolio to equities during a market sell-off. However, the exact amount would depend on various factors, such as: The overall capital position and RBC ratios of Fairfax's insurance subsidiaries The liquidity and credit quality of the bond portfolio The expected impact of the reallocation on the company's risk profile and capital adequacy Regulatory restrictions and approval from the relevant insurance regulators Rerunning your numbers - we must be calculating different things Using the ratio of the company's cash and fixed income float portfolio over its insurance float reserves as a proxy for the Minimum Capital Test (MCT) ratio is an interesting approach, but it has some limitations and may not provide a fully accurate representation of the company's capital adequacy. The insurance float represents the funds generated by insurance operations that an insurer can invest until claims are paid out. Fairfax's float primarily consists of the following components: Insurance contract liabilities: $45,918.1 million as of March 31, 2024 Insurance contract payables: $1,065.0 million as of March 31, 2024 The cash and fixed income float portfolio includes: Holding company cash and investments: $2,496.4 million as of March 31, 2024 Subsidiary cash and short-term investments: $7,801.6 million as of March 31, 2024 Bonds: $36,131.2 million as of March 31, 2024 Calculating the ratio: (Cash and Fixed Income Float Portfolio) / (Insurance Float Reserves) = ($2,496.4 million + $7,801.6 million + $36,131.2 million) / ($45,918.1 million + $1,065.0 million) = $46,429.2 million / $46,983.1 million = 0.99 This ratio of 0.99 suggests that Fairfax's cash and fixed income float portfolio is nearly sufficient to cover its insurance float reserves. However, it's important to note that this ratio does not fully capture the company's capital adequacy for several reasons: It does not consider other types of investments, such as preferred stocks, common stocks, and investments in associates, which may also be used to support insurance liabilities. It does not account for the risk characteristics of the assets and liabilities, which are a key component of the MCT ratio calculation. It does not include other components of the MCT ratio, such as available capital, surplus allowance, and eligible deposits. It does not reflect the specific regulatory requirements and risk factors used in the MCT ratio calculation. While this ratio provides a simplified view of Fairfax's ability to cover its insurance float reserves with liquid assets, it should not be considered a substitute for the more comprehensive MCT ratio. The MCT ratio is a risk-based capital adequacy measure that considers a wider range of factors and is specifically designed for property and casualty insurance companies in Canada. In summary, while the ratio of cash and fixed income float portfolio over insurance float reserves can provide some insight into Fairfax's liquidity and ability to cover its insurance liabilities, it is not a perfect proxy for the MCT ratio, which is a more comprehensive and risk-based measure of capital adequacy. Taking a stab at MCT I take it MCT and RBC are actually confidential. Makes sense you don’t want to be giving your opposition a leg up in terms of capacity to write. However upper level (and treat the numbers with contempt) To calculate Fairfax's Minimum Capital Test (MCT) ratio based on the asset classes detailed in the Q1 2024 report, we will make assumptions about the risk factors associated with each asset class. Please note that these assumptions are for illustrative purposes only and may not reflect the actual risk factors used by Fairfax or its regulators. Assumptions: Available Capital: We will assume that Fairfax's available capital is approximately 70% of its total equity. Minimum Capital Required (Risk Factors): a. Cash and cash equivalents: 0% risk factor b. Short-term investments: 1% risk factor c. Bonds: 3% risk factor (assuming a mix of high-quality government and corporate bonds) d. Preferred stocks: 15% risk factor e. Common stocks: 20% risk factor f. Investments in associates: 30% risk factor (assuming illiquid investments) g. Derivatives and other invested assets: 10% risk factor h. Insurance risk: 20% of net premiums written Calculation: Step 1: Estimate Available Capital Total Equity as of March 31, 2024: $27,643.5 million Assumed Available Capital = 70% × $27,643.5 million = $19,350.5 million Step 2: Estimate Minimum Capital Required a. Cash and cash equivalents: $7,023.2 million × 0% = $0 million b. Short-term investments: $2,266.0 million × 1% = $22.7 million c. Bonds: $36,722.3 million × 3% = $1,101.7 million d. Preferred stocks: $2,447.8 million × 15% = $367.2 million e. Common stocks: $7,172.5 million × 20% = $1,434.5 million f. Investments in associates: $6,833.6 million × 30% = $2,050.1 million g. Derivatives and other invested assets: $1,574.2 million × 10% = $157.4 million Total Minimum Capital Required for Assets = $0 + $22.7 + $1,101.7 + $367.2 + $1,434.5 + $2,050.1 + $157.4 Total Minimum Capital Required for Assets = $5,133.6 million h. Insurance risk: Net premiums written (Q1 2024): $6,249.3 million Annualized net premiums written = $6,249.3 million × 4 = $24,997.2 million Risk factor for insurance risk: 20% Minimum Capital Required for Insurance Risk = 20% × $24,997.2 million = $4,999.4 million Total Minimum Capital Required = $5,133.6 million + $4,999.4 million = $10,133.0 million Step 3: Calculate the MCT Ratio MCT Ratio = (Available Capital) / (Minimum Capital Required) MCT Ratio = $19,350.5 million / $10,133.0 million MCT Ratio = 1.91 or 191% Based on the asset classes detailed in the Q1 2024 report and the assumed risk factors, Fairfax's estimated MCT ratio would be approximately 191%. This suggests that the company would have sufficient available capital to cover the assumed risk exposures associated with its investments and insurance operations. However, it's crucial to reiterate that this calculation is based on illustrative risk factors and limited information from the Q1 2024 report. The actual risk factors used in the MCT calculation would be determined by the regulatory guidelines and the specific characteristics of Fairfax's assets and liabilities. Additionally, the MCT ratio is a comprehensive measure that considers various other risk factors, such as interest rate risk, foreign exchange risk, and operational risk, which are not captured in this simplified calculation. In summary, while this calculation provides a more granular estimate of Fairfax's MCT ratio based on the asset classes reported in the Q1 2024 report, it remains an illustrative example based on assumed risk factors. The actual MCT ratio would need to be determined using the specific regulatory guidelines and a more comprehensive risk assessment of Fairfax's operations. Equity Reweighting To determine how much could be reallocated from bonds to equities while maintaining a conservative approach, we will target an MCT ratio of 200%, which is comfortably above the regulatory minimum of 150%. We will also assume that the risk factors for the other asset classes and insurance risk remain constant. Given: Current MCT ratio: 191% Target MCT ratio: 200% Current bond allocation: $36,722.3 million Risk factor for bonds: 3% Risk factor for equities: 20% Step 1: Determine the excess available capital at the target MCT ratio Target Minimum Capital Required = (Available Capital) / (Target MCT Ratio) Target Minimum Capital Required = $19,350.5 million / 2.00 Target Minimum Capital Required = $9,675.3 million Excess Available Capital = (Current Minimum Capital Required) - (Target Minimum Capital Required) Excess Available Capital = $10,133.0 million - $9,675.3 million Excess Available Capital = $457.7 million Step 2: Calculate the amount that can be reallocated from bonds to equities Reallocation Amount = (Excess Available Capital) / (Difference in Risk Factors) Difference in Risk Factors = Equity Risk Factor - Bond Risk Factor Difference in Risk Factors = 20% - 3% = 17% Reallocation Amount = $457.7 million / 0.17 Reallocation Amount = $2,692.4 million Therefore, based on the assumptions and the target MCT ratio of 200%, Fairfax could reallocate approximately $2,692.4 million from bonds to equities while maintaining a conservative capital position. After reallocation: Bond allocation: $36,722.3 million - $2,692.4 million = $34,029.9 million Equity allocation: $7,172.5 million + $2,692.4 million = $9,864.9 million It's essential to note that this calculation assumes that the reallocation would not impact the other risk factors or the available capital. In practice, any significant changes to the investment portfolio would need to be carefully analyzed to assess their impact on the company's overall risk profile and capital adequacy. Furthermore, it's crucial to consider that this reallocation is based on a static view of the MCT ratio and does not account for potential changes in market conditions, asset valuations, or insurance risks over time. Any reallocation decisions would need to be made in the context of Fairfax's long-term investment strategy, risk appetite, and regulatory requirements. In summary, based on the conservative target MCT ratio of 200% and the assumed risk factors, Fairfax could potentially reallocate approximately $2,692.4 million from bonds to equities. However, this calculation is for illustrative purposes only and does not consider the dynamic nature of capital adequacy or the specific factors that may influence Fairfax's investment decisions. Final Take So after all that and probably too many assumptions, and no doubt some AI hallucinations, the answer is 2.7 bn. i.e not much and below the $4bn the questioner suggested.

-

On the weekend, Buffett talked some about investing in China and elsewhere outside of the U.S. He said as long as he's there, it is unlikely that Berkshire will invest significant sums outside of the U.S. Younger management may choose to do so when he's gone, but culturally he has no advantage investing outside of the U.S., nor does he have any real need to since many of Berkshire's investments and businesses have substantial operations outside of the U.S. After my experiences with China, and considering the size of investments I'm making, Buffett's position is extremely similar to my own thinking. Cheers!

- Yesterday

-

Hamas: I want X Israel: I want Y Hamas: Ok, I accept X Media: Hamas accepts ceasefire. LOL

-

Berkshire Hathaway Annual Meeting 2024

Eldad replied to good-investing's topic in Berkshire Hathaway

Possibly. I always thought their business counterculturalism of doing less was what set them apart. Now you love this guy because he flys all over the country and works 15 hours a day like every other ceo. I thought that way of managing had been the butt of their jokes for forever. -

My guess is Warren and Charlie had their proxies doing the whip cracking - at least when they were younger. They spend all day doing financial analysis- if they look at their wholly owned businesses and see their labor or materials or whatever costs are X% higher than a competitor, don’t you think they will somehow prod that? These guys are shrewd- they just do it in a way that doesn’t come back to them.

-

Berkshire Hathaway Annual Meeting 2024

Hektor replied to good-investing's topic in Berkshire Hathaway

The phone rang for WEB and CTM, but will it ring for the new guy(s)? I doubt it rang for BRK. He probably is saying that the new guy(s) must go hunting than await a elephant or a horse or a sheep. Also, they might have to work at cultivating the relationships so that the phone rings for them too. Some speculation. -

https://www.amazon.com/Happiness-Curve-Life-Better-After/dp/1250078806

-

Berkshire Hathaway Annual Meeting 2024

Eldad replied to good-investing's topic in Berkshire Hathaway

WEB has always been very hard for me to read and he often says contradictory things. He says Greg understands business so will be a good investor. That seems to fly in the face of everything WEB and Charlie have espoused for their whole time talking to their partners. He says Greg has boundless energy and so can accomplish so much more than me as manager. After saying for the past 60 years that sitting on their butts waiting for the phone to ring has been the secret to their success. Just odd. -

Sure. Unless you believe Bitcoin has inherent risk anything like MBS (speculation) or ESG (political)? Or you believe he's learned nothing from his experience? Or doesn't wish to go out on top? And even so, if does end in disaster, isn't there money to be made in the runup?

-

Berkshire Hathaway Annual Meeting 2024

Hektor replied to good-investing's topic in Berkshire Hathaway

This could be a risk, post WEB.