All Activity

- Past hour

-

Hopefully, Orange Boy keeps his promises tonight .... SD

-

The short answer is I think your bracket of 1.2-1.5 looks pretty accurate these days (how the stock is actually trading). I think @Txvestor’s post above is spot on. Fairfax has been executing/performing exceptionally well for about 5 years now. IMHO, the current multiple range of 1.2-1.5x does not reflect that strong performance. As Fairfax continues to perform strongly - and their track record extends to 10 years - it makes sense to me the stock should trade at a higher valuation. But I really have no idea. My focus is fundamentals and capital allocation. Those topics… I have strong opinions.

-

Yes, the joys of running public money. I hear it from investors that question why we are sitting in a flat stock for over a year while tech is running every month but that's the job! Hopefully they give me that 5-10 year time frame!

-

I don't disagree. However, here is my lay man perspective as to why Fairfax does deserve a higher multiple of book value than it receives. 1) BV is understated, that's not just an estimation, it's based on publicly verifiable value of associates. And occasionally surfacing valuation of subsidiaries. Even if you exclude the latter there's $150-200 of value which management constantly reports about each quarter. 2) It has a higher insurance float per share compared to many other companies in their cohort. Same when you look at Float/insurance equity, they skew higher. Closer to Berkshire. 3) Their insurance operations have clearly reset to a better quality, we can for sure say they did in the hard market, and await confirmation as the market softens, but it seems to have materially shifted and the market has not acknowledged that fully and certainly isn't awarding it the appropriate multiple. But that realization if accurate will eventually come. Probably gradually. 4) Everytime they do a transaction involving one of their Insurance subs. You get a window into their actual value. You can basically take your pick of the transactions over the last decade ie Pethealth, First Capital, ICICI Lombard. They all happened at valuations significantly above 1.25BV, more like between 2-3x. These valuations were significantly above when they listed shares in Odyssey re and Northbridge in the 2000s at the 1.16 BV region (when the underwriting was arguably more inferior). Quality insurance franchises are worth paying up for and if they do transact, do so at a premium to where they trade. They are great value add engines so are seldom sold. 5) There will always be a holding company discount to their shares, this is something structural for any holding company, including Berkshire. That discount, whatever it is tends to be insignificant over longer periods of time as even if it persists, it doesn't affect the eventual returns. Companies buying back shares and looking at this as a capital allocation vehicle, constantly exploit this to their remaining shareholder benefit. And keep causing the IV and BV to diverge. Fairfax has been one of the more active participants in this area. 6) We are in a pricey stock market and finding even 10% compounders at a reasonable multiple is not that easy. Insurance is one of those industries where if you can take a long enough view of an investment, you tend to have such or better on average returns based on how it all works out with interest rates and investments etc. My guess is it will reset from 1.25 BV or so where it sits currently to closer to 1.75 BV or so over the next 5-10yrs. But it will be a very gradual process and one where management will get the opportunity to keep buying back a meaningful number of shares over time. If you have a 5-10yr time frame it's not a bad outcome.

- Today

-

Doesn't look like Mr. Market will agree with 2x book or 15x PE anytime soon!

-

A few observations from the Argentina Egyptian match. 1. Benz is amazing when you walk in the place … go to the FIFA.swag stands… There was only FIFA and Argentina gear couldn’t find any Egyptian. 2. Place was full of Argentina fans very few Egyptian, my buddy and I decided to root for Egypt because the 2 cute girls in front of us were rooting for Egypt. What was fun ?the flow of the game…. There was a long stretch where you can see the Argentinian fans, players and coaches had very tight, sphincter muscle .. 3. fan stay twenty minutes to thirty minutes after the match just cheering the Argentinian team and the Argentinian team was cheering themselves. That was amazing. 4. If all footballers are like the ones that played this game, they are all amazing actors, especially when they get touched. 5. Loud!!! It was a great experience and glad I went. and glad I wore earplugs.

-

Trump is a stupid tyrant.

-

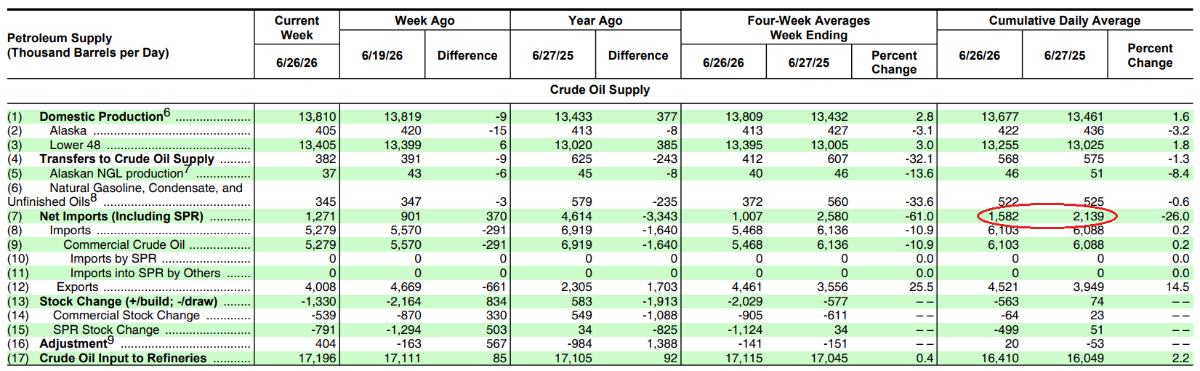

Despite record domestic oil production levels, the United States is still a net importer of about 1.6 million barrels of crude oil a day: EIA: Weekly Petroleum Status Report

-

Oh I was born and raised here lol. I just had a shitty family situation and my work became the escape from it. So in my 20s family was not a distraction since I didnt have much of one myself at that point.

-

I think my age, ethnicity and country of origin are already well known to the members of CoBF. It has indeed been helpful with folks reaching out to me on immigration workflows etc. Since you've given me the free pass to rant about NYC.. Fuck NYC. Four grand a month is a mortgage on a house with a yard in most of the country, a yard where nobody would say a word about you smoking, grilling, or doing whatever you want. In NYC it gets you 400 square feet and a rulebook. Imagine paying $4k/mo + amenities and not being able to smoke on the terrace. I don't smoke indoors as that's something only imbeciles do, but on your own private terrace? Something very wrong with the real estate market. Greg, I thought you were born and raised here 🫨. Learn something new everyday. Punani not getting in any man's way in today's hypergamous, hybristophilic world.

-

I bought Panthera Resources (PAT - LSE), <1% position, essentially a lottery ticket on the results of their litigation process against India. $70M mkt cap, litigation claim is $1.6B but it will updated since gold price is ~25% higher now than when they filed initially. From what I read, they should have a strong legal basis. They are backed and fully funded by LCM (litigation capital management) who are highly selective in the cases they agree to support and have a good track record. Final hearing in Jan 2027, expected outcome announced by end of 2027. Wish me luck!

-

My first real job was a 9-month internship with Quantum, a disk drive manufacturer that had since bankrupted (i think the remaining pieces sold to WDC, but not sure). So i think i know a bit about disk drives. Even back then, 20’years ago, seagate is the leader in technology. I remembered no matter what we do, we cant beat seagate in term of “disk seeking speed” (which is how fast the disk head find a data on the disk and read it). In terms of stx vs wdc, the thesis of HDD is they are not spending more money to expand factories. Instead, more capacity will come from per disk density. As stx sells more HAMR drives , price per drive also goes up. There are some YouTube video about how these hamr drive works. Very cool. And a lot of existing drives will get upgraded over time — more cash for stx without additional factories. STX’s hamr technology is very unique and wdc cant do it. Wdc’s current method of increasing density per disk is just adding more disk platters. They are years behind. as the AI being used by more individuals, people already start buying CPU stocks because more cpus will be needed per user. But i think storage will explode too. U need to store those context from everyone’s projects. And Flash memory is so expensive, HDD will be used more (solvable though software optimizations to use flash more efficiently and move more stuffs to HDD)

-

yeah. I never got the “newfy” thing myself and lived in QC for decades. But I use to hear it in high school as a joke. I never been in St John, maybe it is the undiscovered Vancouver of east coast, without the Chinese money inflow (not expensive) but lots of snow PS: fun fact, we (QC) buy a lot of electricity from Labrador on the cheap (which is part of Newfoundland) and resell to the north east States in the U.S. for massive profit.

-

Oh look, oil being pumped on a news piece! Hopefully this time people learn that this is speculation bidding up the price...not supply and demand.

-

@whatstheofficerproblem, Alone the fact that you've now posted your origin here on CofB&F may possibly end up being of tremendous help for you, not that this to be understood as CofB&F are divided into national groups, but it always helps to get to know someone - at least it can'r hurt.

-

I was in a similar situation starting off...they were technically here, as in location...present, but otherwise not relevant in my life, and it's such a huge advantage getting off the ground. Honestly, the less you have, the more drive and focus there is to go get something for yourself. You're gonna do quite well if you just stay focused. Dont let the punani get in the way either LOL

-

Haha, ty @John Hjorth. I think a lot of NYC's shortcomings are as much related to the sheer population density as is the politics. Haven't seen a city so packed since I left India.

-

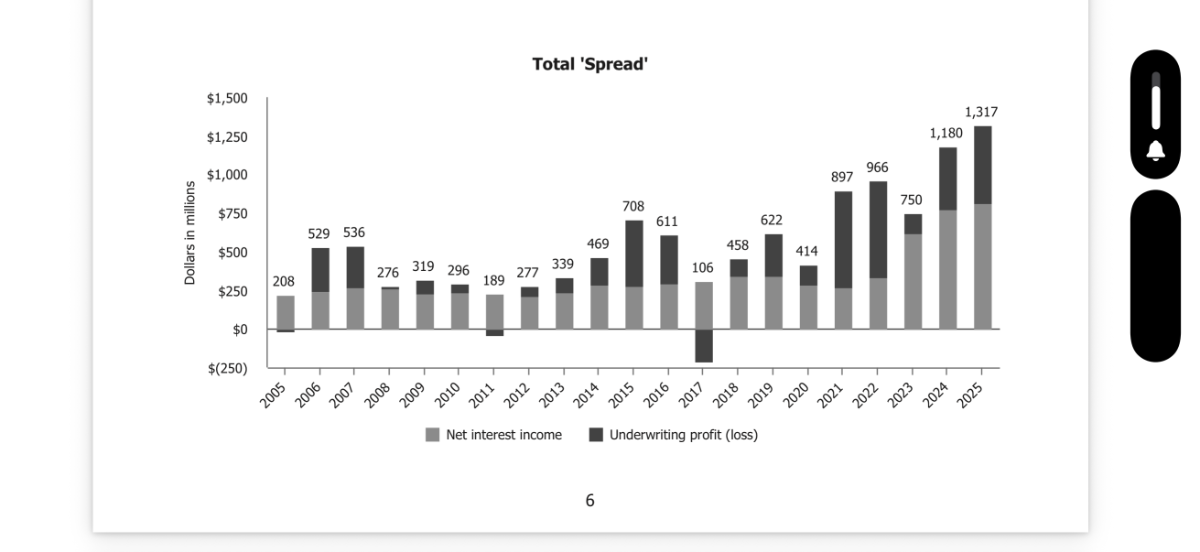

Insurance - The Engine That Drives Fairfax

Hamburg Investor replied to Viking's topic in Fairfax Financial

They have mentioned it but definitely less than BRK and FFH. Tom has something to say about the BRK model, maybe he uses his own words and own framing, instead paraphrasing Buffett? E. g. here, where he writes about the „spread“ in his 2025 shareholder letter. https://s202.q4cdn.com/749045284/files/doc_financials/2025/ar/MKL-12-31-2025_ARS.pdf BTW: I really like the 5 year financial results table in Toms shareholder letter.

-

@Whensthepaintdry?, Yeah, I remeber that, too, and on Reddit a Q&A is called an AMA [Ask Me Anything]! <John, quite happy & proud to post a material contribution here> - - - o 0 o - - - In short, she lost access to Warren Buffett after the release of 'Snowball'.

-

any particular reason for STX over WDC or better tech. etc. Tks.

-

I sincerely wish you the best of luck going forward, @whatstheofficerproblem !, With that said, you're also forgiven to post push back to NYC dirt & trash talk in this topic, which it's over time evolved to become!

-

The lower loonie is bullish for Canada economy https://www.msn.com/en-ca/money/other/canada-s-trade-surplus-in-may-sharply-up-to-a-four-year-high/ar-AA27oucx Exports to countries other than the U.S. continued to shrink, although at a lower rate in May than April, and imports from non-U.S. countries rose. This widened Canada's trade deficit with countries other than the U.S. to C$7.4 billion in May.

-

I've personally been holding my breath the last couple of days related to the Ankara NATO summit ... - how would it go, and how would it turn out related especially the relationship of NATO to USA, and here we go - To me personally, it certainly could have turned out much, much more worse than this : NATO - Press Office [July 8th 2026] : The Ankara Summit Declaration - 8 July 2026 - - - o 0 o - - - By now, released about a half an hour ago.

-

Sorry .... but no trade secrets SD

-

I am a data science major. I have already been working for a subscale hedge fund out of college, been a year now. Moving to bigger firm now. No family here, moved to this country on my own when I was 19.