All Activity

- Past hour

-

Interesting we can pay reparations to Iran

-

Managing a Concentrated Portfolio - How do you do it?

73 Reds replied to Cor's topic in General Discussion

As mentioned before, its really no different than a business owner maintaining most or all of his/her wealth in the business. The advantage is the business owner has complete control, but otherwise the issues are the same and it would be silly to advise a business owner to sell or take on partners unless necessary or desired. -

Yes looks like you're right here. The Andrew Peller release is more clear on this. And I agree it's a good thing as the managers have skin in the game. "Andrew Peller Limited (“Andrew Peller” or the “Company”) (ADW.A / ADW.B) announced today that it has entered into a definitive arrangement agreement (the “Arrangement Agreement”) with a newly-formed and wholly-owned subsidiary (the “Purchaser”) of Fairfax Financial Holdings Limited (“Fairfax”), and Fairfax, as guarantor, in respect of a transaction (the “Transaction”) whereby the Purchaser will acquire all of the issued and outstanding Class A Non-Voting shares (the “Class A Shares”) and Class B Voting shares (the “Class B Shares”) of the Company (other than the Rollover Shares (as defined below))"

-

Also gives Fairfax partners who know the company best that have skin in the game.

-

Yes thats what I read it to be. And how I arrived at ~$65M. Ie 5.2M x $8 and 2M x $12. Everyone else gets cash.

-

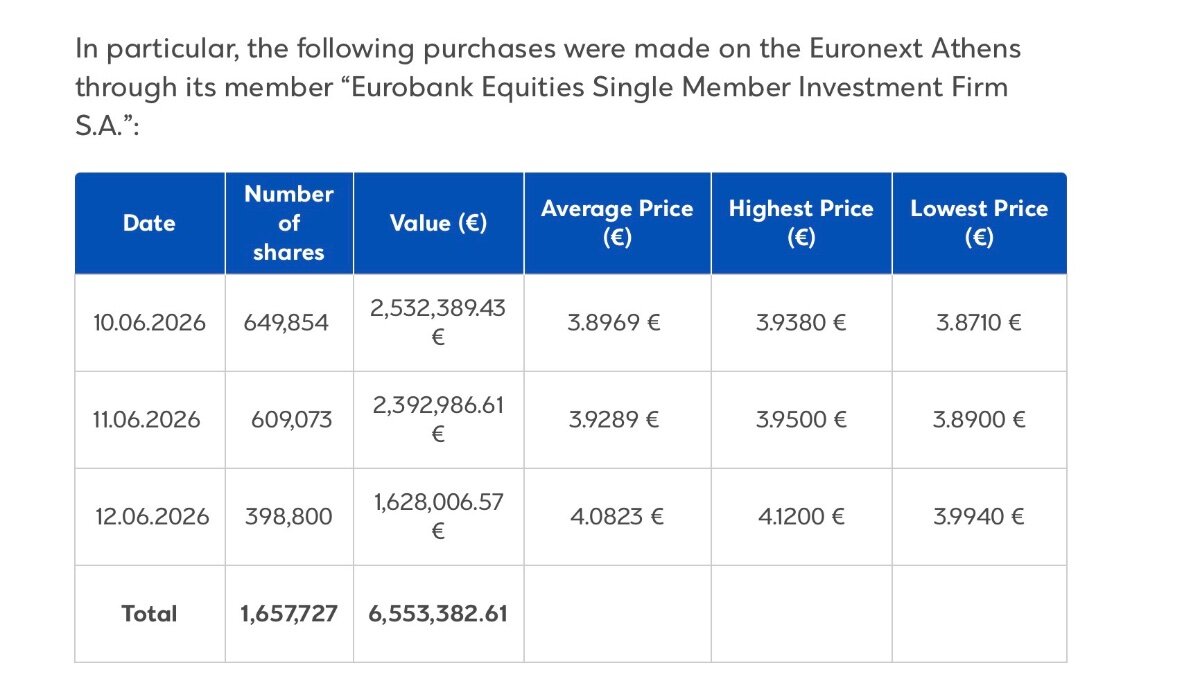

With all due respect, those are really miniscule numbers given their market cap in the range of $15B. €6.5M is less than 0.05% over 3mths.

-

I feel sorry for the suckers.

-

No, the purchaser is a new subsidiary that has been created to acquire the company.

-

Managing a Concentrated Portfolio - How do you do it?

Longnose replied to Cor's topic in General Discussion

God i love how you can simplify thoughts into such a blunt object. #gregisrighttoday -

maybe I am not reading it correctly but it sounds like John Peller is exchanging his shares for the “purchaser’s” shares. Wouldn’t that be Fairfax shares? https://ir.andrewpeller.com/news/news-details/2026/Andrew-Peller-Enters-into-Definitive-Agreement-to-be-Acquired-by-Fairfax/default.aspx In connection with the Transaction, John Peller and certain affiliates (collectively, the “Rollover Shareholders”) have entered into an equity rollover agreement with the Purchaser, pursuant to which they have agreed to exchange all 5,246,517 Class A Shares and 1,994,212 Class B Shares beneficially owned and controlled by the Rollover Shareholders (the "Rollover Shares") for shares in the capital of the Purchaser or an affiliate thereof. The Rollover Shares represent approximately 15% of the issued and outstanding Class A Shares and approximately 25% of the issued and outstanding Class B Shares

-

There is just a certain type of people in this world. War with Iran was every permabulls wet dream, as was closure of the strait. Kinda funny, even I’m surprised it didn’t spike higher. Part of it was Trump’s shit talking, he talked prices down.

-

Managing a Concentrated Portfolio - How do you do it?

Gregmal replied to Cor's topic in General Discussion

End of the day it's as simple as making the position as big as you're personally comfortable with and holding it until you dont want to hold it anymore. Beyond that it's kind of a waste of time having hard rules and all that because the whole point of being in the market is to capitalize on opportunity. -

I don’t think so. The dividend capacity is based on what regulators will allow them to dividend out without seeking additional approvals based on excess capital. Selling one equity investment like Poseidon to buy ADW doesn’t change that.

-

Managing a Concentrated Portfolio - How do you do it?

Red Lion replied to Cor's topic in General Discussion

I see a lot of value investors say this, but if you're an affluent individual living off of your taxable portfolio, and you can match the S&P performance with 2% positions, this gives a lot of wiggle room for tax efficiency. The big IF is whether you could match the S&P performance, but there have been great investors that had lots of stocks. If you have all your money tied up in 3 stocks that are all sitting on gains, and you're holding them for decades, you have no choice but to sell stock, take margin on a super concentrated portfolio, or hope they pay dividends. If you pick the right 3 stocks, great. If you're taking a buy and hold approach, or buy/hold/tax loss sell the losers, you're more likely to hit some huge long term winners if you get 50 chances. Retirement accounts I think would be a much higher hurdle, since I suspect the highly concentrated portfolio with event driven type ideas probably shows the highest return if well executed. -

Managing a Concentrated Portfolio - How do you do it?

TwoCitiesCapital replied to Cor's topic in General Discussion

Concentration is how you make/lose money. Diversification is how you protect it. Over time, investment management is an exercise in both. I found early on that it was often my smallest positions that outperformed the most and my largest positions that would lag. Had I just equal weighted the portfolio, I'd have done much better. I made adjustments to my approach as a result. I never equal weighted, but set a limit on my largest positions as a % of my net worth to force more money to funnel down into the smaller ideas. The hope was I'd prevent some damage if I continued to be wrong, but still give myself grace in getting better/more right over time. As such, I typically start positions at ~1% of my net worth, a full allocation would be ~3-7%, and I only have two investments at the ~10% limit which have largely grown there and weren't allocated there. -

Managing a Concentrated Portfolio - How do you do it?

Intelligent_Investor replied to Cor's topic in General Discussion

Don't own anything in a concentrated portfolio you wouldn't be comfortable owning if the market is closed for a decade. 2% position is pointless for individual positions, at that point just buy index funds. -

Managing a Concentrated Portfolio - How do you do it?

Malmqky replied to Cor's topic in General Discussion

What's the company? Something like Berkshire, Fairfax, or even CSU is easier to concentrate in due to the diversified nature of the companies. Something like Warrior Met Coal is tougher to concentrate in for obvious reasons. You need to get a few drawdowns of 50% under your belt before you really can feel comfortable concentrating. Otherwise it's gonna be tough for you. The fact you're questioning "how to do it" tells me you're going to have a hard time next market crash holding/not diversifying, etc - Today

-

Managing a Concentrated Portfolio - How do you do it?

Longnose replied to Cor's topic in General Discussion

To add when it comes to heavy concentrated positions I only see 2 real reasons to be this concentrated. Your chasing extreme returns. You have extreme conviction in the company. Maybe you should ask yourself questions around why am I so concentrated in "SaaSco" I usually wont go super deep into a company unless I have extreme conviction in my analysis. It still hurts to be early. But i often feel like I'm having this conversation with my devils advocate in my head. I often feel like burry where i cite the numbers and I'm like the numbers don't make sense the market must be wrong. so i just keep holding. The volatility doesn't bother me. But i do read and seek lots of material for my opposite hypothesis. I don't want to be blinded by bullishness to where I hold into the ground. I have abandoned a few concentrated in the past after admitting to myself that my analysis was wrong. -

sold about half my position in RMS at the open in Paris.

-

I agree. I think the company was just trying to ensure it didn’t die, so that it would be able to keep a string of annual results moving forward in the future. In a series of annual performance figures, the only thing worse than a number of subpar or negative years would be a zero, meaning the company had died. I can think of a number of value investing phrases that are apropos in this regard, such as “to finish first, one must first finish.” A company is an artificial person, with one significant advantage over the human beings who manage it: it can be immortal as long as its managers don’t allow it to be killed. Charlie Munger was known to share the thought that “All I want to know is where I’m going to die, so I’ll never go there”. I appreciate the fact that the human beings who manage Fairfax think about how and where their company might die, and try to manage its affairs so that it doesn’t go there. In doing so, they increase the likelihood that it will survive and continue to compound value for its shareholders well beyond their own lifespans. Sometimes they purchase insurance against catastrophes that happen, such as buying CDS’s in advance of the GFC, or keeping bond durations low in periods of historically low interest rates so that mark to market losses won’t hinder the company’s financial strength and solvency when rates began to rise again. Other times they purchase insurance against catastrophes that didn’t occur, such as global deflation after the GFC. These were all decisions to purchase insurance against events that could kill or severely injure the company. Since the company is still alive and thriving, I consider them all to be successful, whether the feared for events occurred or not.

-

I don't understand the reasoning here. Take this Peller deal, if the deal never materialized, wouldn't the insurance subs now have $4b + $400MM to dividend up to holdco?

-

Managing a Concentrated Portfolio - How do you do it?

thepupil replied to Cor's topic in General Discussion

what are the consequences of selling? what's your basis as a % of market value does it have a listed options market? are you a candidate for the numerous wealth mgt solutions for this? how many years of savings does it represent? Are we walking like "I have $20K of SaaSco and save $50K / year" or "I have $2 million of SaaSco and save $50k / year?" Why hold it? if you're not comfortable with a >50% position, then why have it? -

Managing a Concentrated Portfolio - How do you do it?

Cor replied to Cor's topic in General Discussion

Thanks guys. Sounds like Paarslaars and Longnose just hold through the pain believing their conviction will be rewarded at some point? I do believe the stock I’m holding is an industry leader and quite profitable. I have no reason to doubt that leadership will not hit their revenue goals in the stated timeline and analyst estimates for when they do are so much higher than price today. Sigh. I guess I’ll start praying too. -

Is that right that they are issuing Fairfax stock to the controlling stakeholders? I didn't see that part. I read all cash deal. edit: Oh I see you are probably referencing the equity in the private winemaker the sellers are retaining. Not the same thing as getting or issuing Fairfax shares

-

Eurobank got busy on the buyback again post dividend payout last week.